Here is the gov’t response to Fairholme:

Gov’t response RE Fannie-Freddie

The gov’t case to dismiss boils down to this:

A- Court of Federal Claims is the wrong court

- the gov’t claims that when the FHFA steps in as conservator, it acts ads the entity, not the gov’t, just as when the FDIC step in at banks. Since the Claims court only hears cases against the US, this does not qualify

- the Claims Court cannot hear cases that “sound in tort”. since the Fairholme Fund (MUTF:FAIRX) suit alleges the FHFA abused its authority, that “sounds in tort” and thus the Claims Court cannot hear it

- further they claim that the Claims Court cannot hear a case where a simultaneous action is taking place in another court, although they admit in the past Judges have ruled that the timing of the two suits matter and in this case Fairholme Fund (MUTF:FAIRX) got the timing right (Claims Court case was filed first)

B- Shareholders lack standing to file suit

- The HERA (Housing and Economic Recovery Act) granted the FHFA “exclusive authority to act on behalf of the shareholders while in conservatorship”

- They argue because of this, shareholders cannot sue

- Shareholders cannot sue based on denial of dividends or valuation degradation

- cannot sue over a taking claim because the shares still trade, they still have them

C- The court may not consider claims that are not ripe

- until the conservatorship is over, there can be no claim as we do not yet know the final outcome of the action

They use as their prime example the FDIC when it takes over banks. In those circumstances shareholders have no rights to then sue the FDIC for its actions. But I see material weaknesses in that line of thinking.

- The FDIC, when it takes over banks does not operate in conjunction with or partner with the US Treasury

- The FDIC does not give the US Treasury a controlling interest in those banks

- Banks are not Chartered by the US Congress

- Banks are not “government sponsored entities”

- Congress does not directly oversea banks operations

- When the FDIC liquidates banks, the assets are sold to other banks, not given to the US Treasury

- When the FDIC enters bank, it does so with an express plan, that plan is not altered unilaterally when the initial goal is in fact being accomplished

- When the FDIC takes over a bank, it does not then encourage the public to continue to make investments in the securities of that bank

- If the bank is being rehabilitated, the FDIC does not alter terms of investments to favor one investor over every other investor

- The FDIC does not need gov’t approval to take over a bank, in no way could they unilaterally against towards to GSE’s

Despite what the US Gov’t is trying to do here, the lines are VERY, VERY blurred and by no means can we simply rely on past precedent to determine rulings. Why? There has never been a case like this before so in effect, there is no precedent, this case will set it. Yes, shareholders in other entities have sued regulators for their actions but never (to my knowledge) have shareholders in a government entity sued the gov’t for “taking” that entity.

The government also has some material fact wrong in the filing. They state:

First, plaintiffs fail to allege that Government action resulted in economic impact upon their dividend or liquidation rights, in that they do not contest that the Enterprises were placed into conservatorships because they were insolvent and needed to be “restored to sound and solvent condition” due to the “steep reduction in the book value of their assets and a loss of investor confidence in the mortgage market broadly.” Compl. ¶¶ 4, 71. Plaintiffs acknowledge that the Enterprises “agreed to conservatorship,” and in doing so, “ceded control of the assets and powers of the [Enterprises] to FHFA as conservator.” Id. at ¶ 5. Plaintiffs also acknowledge that the “conservatorship of Fannie [Mae] and Freddie [Mac] achieved the purpose of restoring the [Enterprises] to financial health.” Id. at ¶ 13. Plaintiffs also concede that Treasury’s infusion of hundreds of millions of dollars of taxpayer funds into the insolvent Enterprises was a critical element of the conservatorships. See id. at ¶ 60. Thus, because plaintiffs have not alleged, nor can they, that they are worse off as a result of the conservatorships than they would have been had the conservatorships not been imposed, dismissal of the complaint is required. Seiber v. United States, 364 F.3d 1356, 1370 (Fed. Cir. 2004) (“the existence of economic injury is indispensable to demonstrating a regulatory taking”) (citation omitted).

The problem with that is that in the Fairholme suit, none of that applies and the argument is irrelevant (Fairholme was not even a preferred shareholder until 2013). At no place in the suit does Fairholme challenge the Conservatorship. The issue is the 2012 Sweep Agreement. Further just because they are not challenging the conservatorship itself does not mean the Sweep Agreement is then somehow validated. Shareholders at that time (2012) had a reasonable expectation based on every public comment from officials that the main goal was the rehabilitation of the GSE’s. The net worth sweep agreement effectively ended at the rehabilitation of the entities as they can never rebuild capital with their net worth being taken each quarter. THAT is what they are arguing.

In all reality the Net Worth Sweep weakened the GSE’s rather than “conserving” or rehabilitating them which is a direct violation of the conservatorship. Without the ability to build capital or repay the Senior Preferred Shares held by Treasury, they will forever be dependent on the Treasury for support. THAT is the taking. It isn’t the loss of shareholder value or dividend, (in fact I don’t see Fairholme argue that anywhere) it is that the entire enterprises were effectively absorbed into the Treasury. When Fairholme speaks of dividends, they speak of the GSE’s ability to begin to pay them again given their current financial condition absent the Net Worth Sweep. Not past ones. Much of the defense here defends arguments Fairholme never makes.

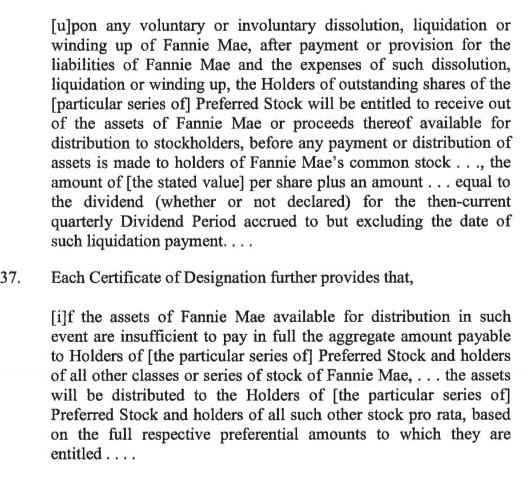

The gov’t even has a problem with their claim they have “all shareholder rights”. See the preferred share agreement:

Because the gov’t elected not cancel or suspend these shares, the shares should maintain their rights. The gov’t can’t have it both ways. If they want to use the FDIC as an example, and if this was the goal, then trading in the shares should have been suspended pending a resolution of the GSE’s.

The gov’t in their filing quoted the FHFA’s statement on Sept 2008 many times to seemingly back their motion but seem to have left this gem out:

Therefore, in order to restore the balance between safety and soundness and mission, FHFA has placed Fannie Mae / Federal National Mortgage Assctn Fnni Me (OTCBB:FNMA) and Freddie Mac / Federal Home Loan Mortgage Corp (OTCBB:FMCC) into conservatorship. That is a statutory process designed to stabilize a troubled institution with the 0objective of returning the entities to normal business operations. FHFA will act as the conservator to operate the Enterprises until they are stabilized.

In 2012 it was clear that the entities were in fact “stabilized” and soon would begin producing significant profits (record profits as it turned out). It was then the FHFA and Treasury enacted the Net Worth Sweep. Shareholders had every right to rely on official statements from both the Treasury and FHFA (Treasury Secretary Paulson’s statement) that the conservatorship would end when the entities were stabilized. .

So, how do we figure this out? I don’t think the judge can simply dismiss because the line between regulator/government/shareholder here are so blurred and intertwined. Perhaps we depose some folks to see just how much influence Treasury had in the initial decisions masking process? Did FHFA step outside of its defined and stated goals at the behest of anyone in the Treasury? Congress? If so it can then be argued that the action was in fact the governmental action and not simply a regulator functioning in is role.

I also found it interesting in its 50 page motion not once did the gov’t admit the GSE will have paid back the entire amount advanced to them by Q1 2014.

Fairholme’s response is due Jan 9th

Via: valueplays