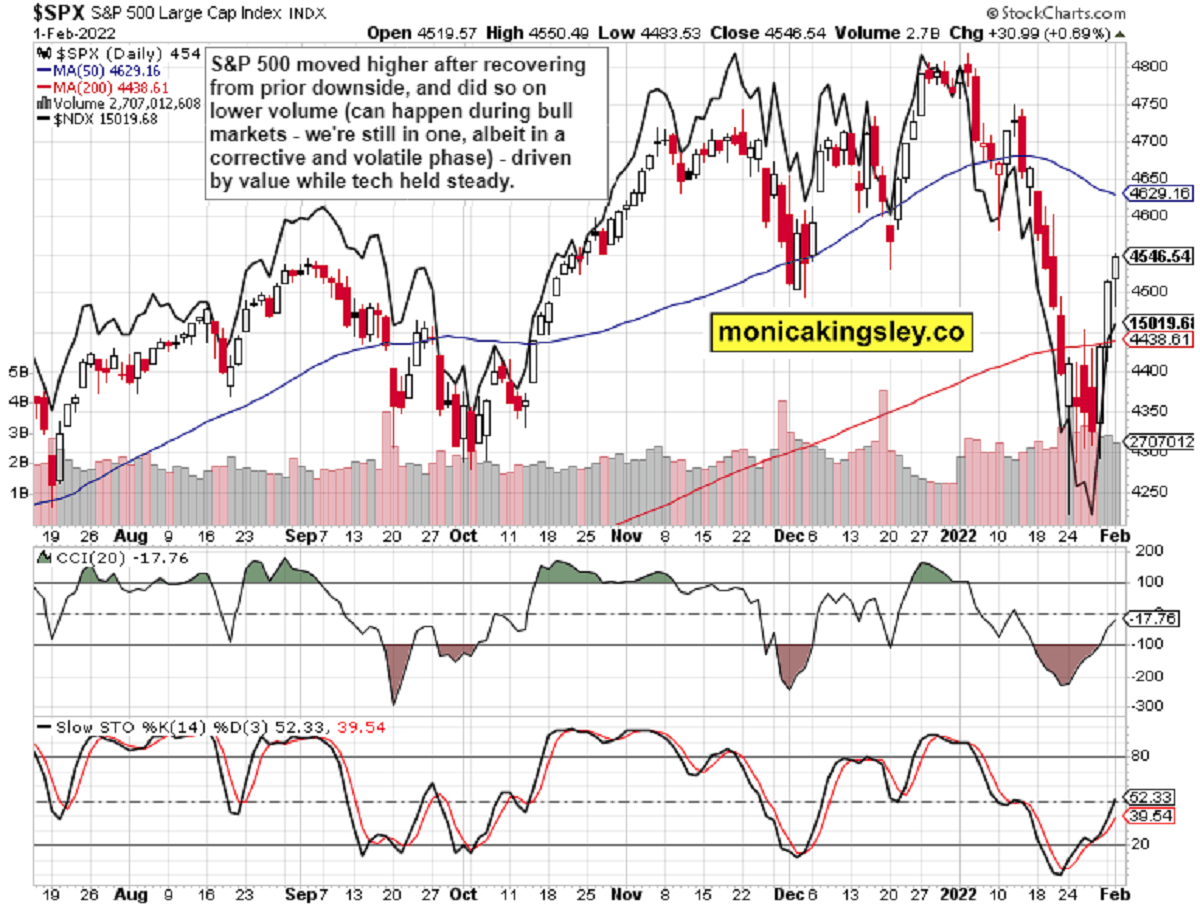

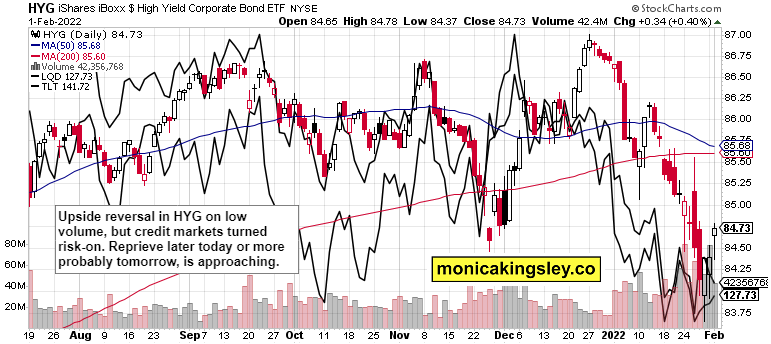

S&P 500 recoverd the opening setback at 4,500, and the low volume behind the upswing coupled with credit market reversal shows that the push towards 4,600 is next – but it would be fraught with internal vulnerability. It‘s that value has welcomed the risk-on turn while tech barely prevented lower values – the bond reprieve won‘t last, and is providing more fuel behind the commodities push higher, and precious metals recovery.

Q4 2021 hedge fund letters, conferences and more

The Kashkari effect and good ISM Manufacturing PMIs have worked fine, but the services data awaits. And I‘m looking at it to throw a spanner in the works, a modest one. For now, controlling the overall risk is key – fresh portfolio highs were achieved yesterday as new S&P 500 long profits were taken off the table – and commodities with precious metals are likely to do well in this extended (sticking out like a sore thumb) rally off oversold levels (in tech). The other key thought expressed in the linked tweet is that S&P 500 hasn‘t entered a bear market, that it hasn‘t rolled over to the downside for good. It‘s that I expect the return of the bears in the not too distant future, and a smoother sailing in 2H 2022.

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

S&P 500 and Nasdaq Outlook

S&P 500 bulls prevailed, but the question still remains – where would the upswing stall, or at least pause? Still the same answer as yesterday – ahead soon, still this week.

Credit Markets

HYG reversed higher, and the pace of its coming gains, would be valuable information. Volume tells a story of a modest setback only thus far – greater battles await.

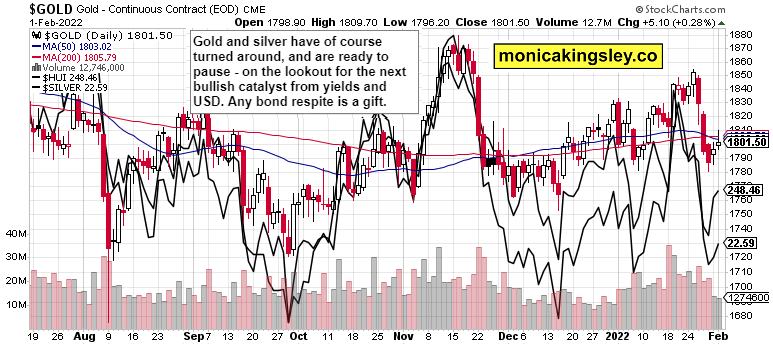

Gold, Silver and Miners

Gold and silver staircase recovery goes on, showing that further retreat was indeed unlikely. The long consolidation would be resolved in a bullish way, it‘s only a question of time. Great performance this early in the tightening cycle – look for PMs upswings once the rate hikes get going.

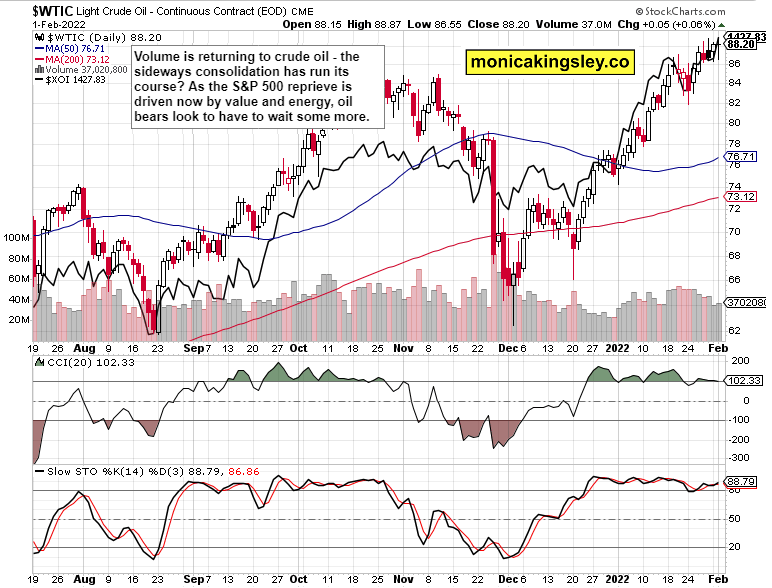

Crude Oil

Crude oil bulls aren‘t wavering as the whole energy sector attests to. Black gold hasn‘t dipped yet below $86, and keeps marching and leading the other commodities $100 is approaching.

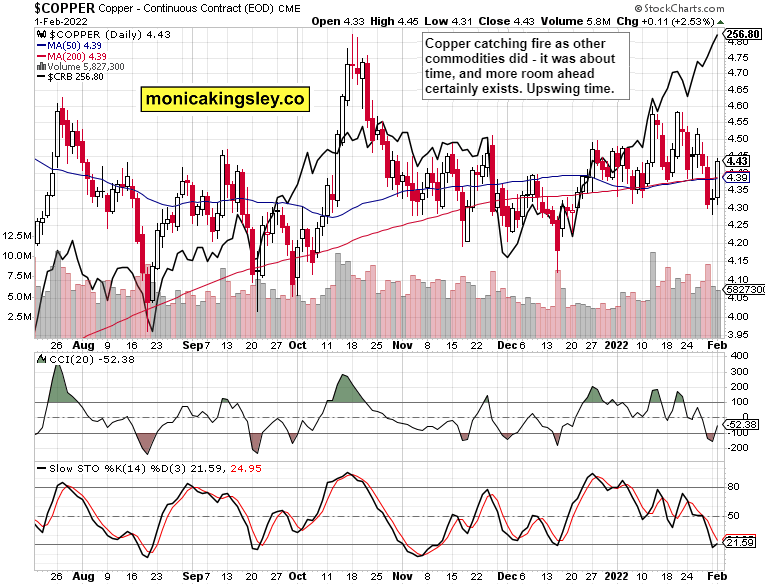

Copper

Copper‘s recent red flag was indeed dealt with decisively, and higher prices prevailed. Still great room to catch up with the rest after the preceding reprieve across other base metals as well.

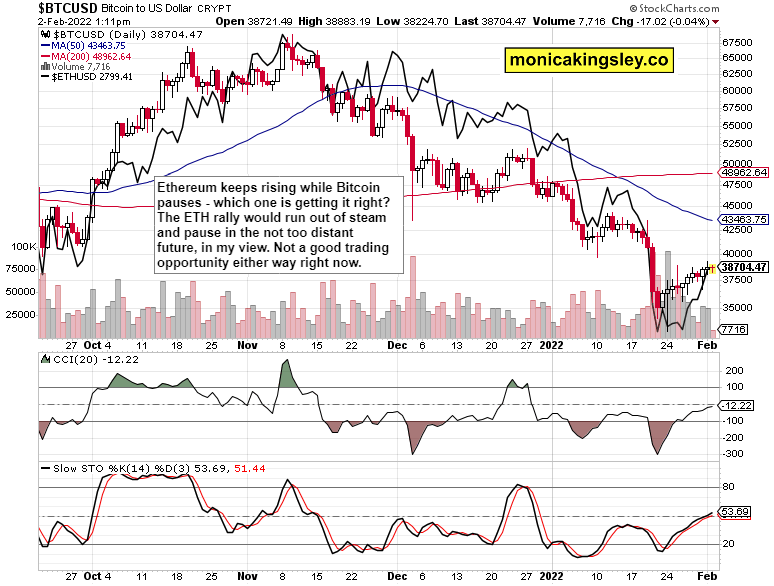

Bitcoin and Ethereum

The narrow crypto trading range continues – I‘m still not looking at the Bitcoin and Ethereum buyers to succeed convincingly. Time for a downside reversal is approaching – will happen just when Ethereum loses the bid.

Summary

S&P 500 bulls again scored gains yesterday, but the sectoral rotation and credit market turn would build a vulnerability going into Friday when value would suffer. Before that, I look for the bears to gradually start appearing again, taking probing bites, but not yet being decisive. VIX has some more room to decline indeed, confirming my earlier thoughts – the volatility return would happen on non-farm payrolls inducing a fresh guessing game as to the Mar rate hikes – 25 or 50bp? Inflation, precious metals and commodities would though still emerge victorious. For now, overall risk management is key – fresh portfolio high was reached yesterday.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for all the five publications: Stock Trading Signals, Gold Trading Signals, Oil Trading Signals, Copper Trading Signals and Bitcoin Trading Signals.

Thank you,

Monica Kingsley

Stock Trading Signals

Gold Trading Signals

Oil Trading Signals

Copper Trading Signals

Bitcoin Trading Signals

All essays, research and information represent analyses and opinions of Monica Kingsley that are based on available and latest data. Despite careful research and best efforts, it may prove wrong and be subject to change with or without notice. Monica Kingsley does not guarantee the accuracy or thoroughness of the data or information reported. Her content serves educational purposes and should not be relied upon as advice or construed as providing recommendations of any kind. Futures, stocks and options are financial instruments not suitable for every investor. Please be advised that you invest at your own risk. Monica Kingsley is not a Registered Securities Advisor. By reading her writings, you agree that she will not be held responsible or liable for any decisions you make. Investing, trading and speculating in financial markets may involve high risk of loss. Monica Kingsley may have a short or long position in any securities, including those mentioned in her writings, and may make additional purchases and/or sales of those securities without notice.