Pzena Emerging Markets Webinar Presented By Allison Fisch: Value Against Headwinds

Q1 hedge fund letters, conference, scoops etc, Also read Lear Capital: Financial Products You Should Avoid?

Transcript

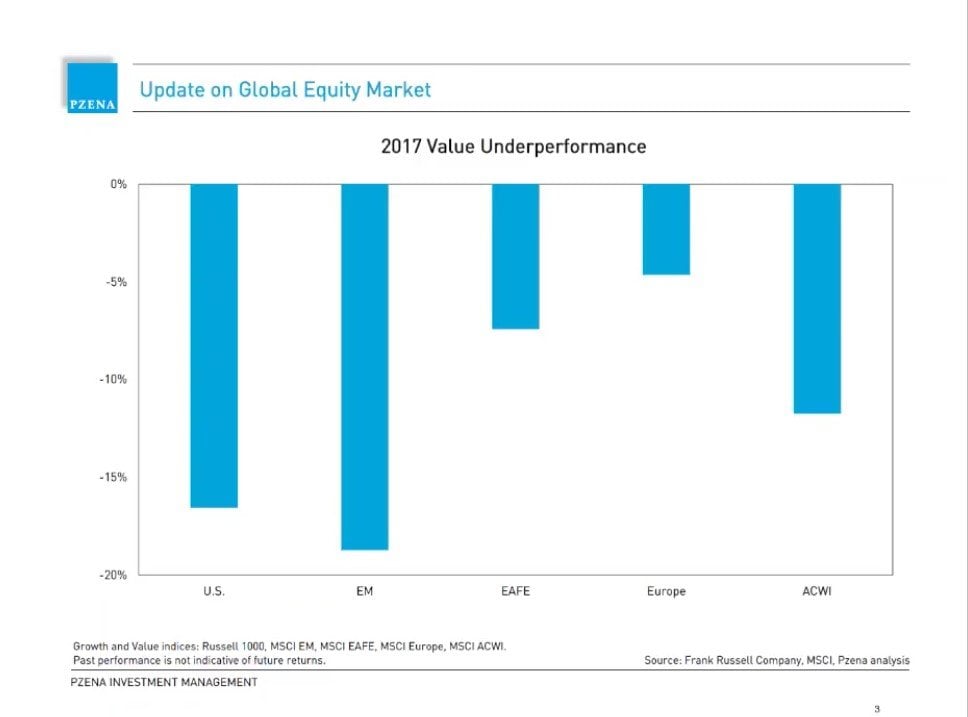

Good afternoon. Thank you everyone for joining us today. I’m Valerie Arnalds headed intermediary distribution and the Zeenat Investment Management. I’m here with Alison Desch a portfolio manager on our emerging markets and international value strategies. Alison has been with Pazin Investment Management for 17 years and she is that of her folia manager on our emerging markets focused value strategy. Since its inception in 2008 here at Casino we are solely focused on one thing value investing. The global research team of 26 professionals utilize fundamental research to build their portfolios from the bottom up company by company. What differentiates us from other investment managers is our relentless commitment to seek value investing under all market conditions. We have a unique team oriented culture that allows us to stay invested in the cheapest part of the market throughout an investment cycle which we believe provides the best long term outcome for our clients. And now let me turn it over to Alison. Thank you Valerie and thanks to everyone for joining us today on today’s call. I’m going to discuss our outlook on emerging markets how we are positioned today and what impacted our performance in the quarter. So 2017 was a rough year for value investing and nowhere was that more evident than in emerging markets where the MSCI emerging markets value index trailed its growth counterpart by 19 percent. A disproportionate amount of that outperformance was driven by just a few names.

Baidu Alibaba and Tencent which were up way to 96 percent in the year that outperformance has brought the top five holdings of the MSCI Emerging Markets Index which include the growth the names Alibaba Tencent and Naspers up to close to 20 percent of the index and you can see how that has grown over the past 40 years. In fact one company Tencent accounts for over a quarter of the entire return of the MSCI Emerging Markets Index over the last five years. And that number actually jumps to nearly 35 percent of the index’s return. A few of the Naspers which is the South African Equity whose entire value is basically the company’s stake in Tencent. So clearly there have been major headwinds for value investors recently. But over the longer term we found that by investing not only works in emerging markets it works even better than in the developed world. What you see here is a study where baskets of the most expensive and cheapest stocks are bought in both emerging and developed markets and then held over a three year period. In both developed and emerging markets the cheap stocks outperform the expensive ones and that value advantage grows with the longer holding period as well. Importantly the superior returns of the cheap stocks are even greater in emerging markets. Now you don’t find a lot of value investors in emerging markets which are thought to be all about growth. Perhaps that’s where the benefit comes from. The way we think about it though the underlying reason why value works anywhere is because investors are not entirely rational especially in the short term when they’re optimistic they get too optimistic and pay up and when they’re worried they get overly pessimistic and won’t want to invest often at any price.

And when you look back and you look around the world nowhere are these cycles of fear and euphoria more pronounced that in emerging markets so where does that leave us today and how are we positioned. Well looking at our exposures you can see that our largest sector weights which are financials and information technology budgets income port to keep in mind that our holdings here look quite different than the index in financials. We try to focus on regions that are currently under earning and we’re lending growth hasn’t been excessive. That leads us to places like Korea and Abu Dhabi whereas we are notably underweight Chinese financials for example and within technology you won’t find a lot of new new economy exposure here. Our largest positions are foundry giant TSMC and the 800 pound gorilla of electronics contract manufacturing Halm Hai regionally our largest exposure is to Asia. But you know digging underneath that you find that we’re significantly underweight China with higher relative weightings to Korea India our largest relative overweigh on a regional level is Europe where we are virtually overweight every emerging European country. When we look around the world for value using our proprietary valuation metric of price normalized earnings Europe is one of the cheaper regions so no big surprise we should find plenty of interesting opportunities in emerging Europe as well. So last year during a very tough time for value our portfolio underperformed the general index as you can see but it did beat the value index by a large margin in the first quarter. However our portfolio underperformed the index broadly driven by short term stock specific issues and less of a style issue here.

The top trackers in the quarter were China Mobile State Bank of India and Grant Boushey bashing Ondo China Mobile the largest telecom player in China with a 70 plus percent market share and nearly all the profit in the industry. But its stock price suffered in the quarter as there were government calls to remove roaming charges reduce data prices. We believe this is an overreaction as the level of price declines. The government is calling for is actually consistent with the pricing plans. The company has been offering anyway and service revenues continue to rise thanks to fantastic plasticity and data usage. State Bank of India is the largest public sector bank in India as well as being the strongest and best fraud but this stock weakened in the quarter due to stricter provisioning requirements by the central bank as well as the revelation of a large fraudulent loan loss of another public sector bank Punjab National Bank which negatively impacted the whole sector stocks despite the fact that State Bank of India had nothing to do with the fraud itself. Finally Grant bashing Audo is a car dealership that work in China which reported strong earnings in the quarter as both revenue and margins continued to improve. But the stock weakened on concerns of slowing auto demand growth in the short term we continue to hold all these stocks as we believe the stock price paid in the quarter is temporary. On the positive side our largest contributions came from Hyundai Heavy Lukoil and pacific basin and heaviest Korea’s largest and most efficient shipbuilder. The stock had fallen at the end of the year as the company announced a large capital raised just prior to the last trading day in Korea. And then those losses were recouped as the market better understood the equity raise in order trends proved to be quite positive.

Lukoil a privately owned Russian energy giant rose in the quarter as the company announced a share buyback program and improved its capital return policy to shareholders. Finally Pacific Basin a dry bulk shipping company continued to benefit from the improving shipping rate environment while were not happy to have underperformed in the quarter. We are very excited about the portfolio we hold today and its diverse opportunities said peaky Moulson. Regionally house InterMune dream had started to drill down a little more and where you’re seeing opportunities. Sure you’re not seeing opportunities for sure. Here let’s go back here. Here’s our regional split. So as I mentioned you know within Asia we have an under age of China and a relative overweight to Korea and India were also a bit underweight to Taiwan. And then within Europe you know we’re overweight basically everywhere. As I mentioned but I should add that we do have within our European exposure a few companies that are domiciled Europe but but where are the economic exposures are actually to other areas for example into the Gasa which is actually a copper miner shows up as UK domiciled but the assets are basically all in Chile. We also own Standard Chartered which is again the UK domiciled bank but its exposures are to emerging Asia. Under Africa and Middle East that reflects smallholdings in South Africa and also the United Arab Emirates were overweight the latter and quite underweight the former. So a big underweight to South Africa and then you can see a big underweight to latte.

The only exposure we have there is to Brazil and you know as always that’s due to valuation as we just haven’t found cheap enough opportunities in other places and quite frankly we’ve been reducing our exposure to those Brazil evenings because they perform quite well over the last year or so and then finally that North American exposure that you see there that’s actually companies where the economic exposure is not to North America but again that they happen to be domiciled here and that would be companies like a couple of Indian I.T. outsourcers that we serve. Any I.T. outsource for that we’ll have as the per cent at the end x represented that is have five names compared to developed markets. So it’s a lot lower so it’s sort of in developed market indices it’s I would say hovering in the sort of 10 to 12 per cent range. And part of that is is due to the composition of these indices over all the emerging markets index has tended to be much more concentrated than develop market indexes in general. But you can see that that concentration has really grown in the last few years because of the strong performance of the biggest names how do you deal with the higher volatility in emerging markets and the unpredictability of corporate behaviour. Yes. So this really goes back to how do we think about risk both for each individual name as well as for the portfolio overall.

So for us you know the risk is really about what’s the risk that we lose our equity stake in this investment not about short term stock price volatility that means that we really obsess about the downside and each investment that we make and we think not only about what’s our base case valuation levels for each stock but what’s the potential reasonable range of outcomes. You know how the bullet Rees-Mogg barricades as well as a reasonable bullish case and that’s very important when we think about each stop then when we add that up and build an entire portfolio. That’s part of the reason why compared to Zena’s other focused value portfolios this portfolio has a slightly larger number of names within it and the maximum position size is a bit smaller here within emerging markets. Our largest position size at cost is 4 percent 6 percent of market whereas in most other focused value strategies that’s five and seven and a half. Can you tell us more about your proprietary valuation metric sure that’s a price to normalize earnings. That’s what we focus on. And the reason for that is that usually we’re coming across businesses that are in pain to something very bad has happened and the earnings level has collapsed. Now if you are using a naive valuation metric by P E the P would be very high on the stocks in general because of the low. So you missed the chance of buying a lot of businesses in pain. If that’s the metric you focus on we find normalized earnings to be more powerful for that reason. Similarly if you wanted to use other valuation metrics such as price to book or with price to book you have to labor problems one is young mis buying a lot of great businesses that aren’t book value based you know a lot of services businesses hardly have any books so they’ll always love expensive price. And then the other side of that coin is when you’ve just come off of a big investment cycle and things are looking peachy.

Sometimes the book value can be overstated. For these businesses. So those type of cheap price pick up. But actually it’s that the B of the book is overvalued. Question comparing the current valuation of the market compare it to history. Yes so merging markets. The valuations have recently moved up certainly 2017 was a great year even for the value investor. But compared to developed markets versus their own history emerging markets actually don’t look that expensive. And the other thing that you see that’s a bit different in emerging markets is where they are in their earnings cycle so if you look at returns on equity for the emerging markets equities what you see is that there was a huge boom in profitability during the late 2000s and then it came way down new beginning in 2011 profitability really fell and it didn’t bottom out until the beginning of 2016 and now we’re seeing that recovery and profitability which has been accompanied by an improvement in the stocks as well. But first is a long term average returns on equity are still a little bit below that which which is not what you see in the developed world. Can you comment on the potential Trump parent plan and its possible impact on your Chinese holdings. Sure sure. So you know I would caution ourselves and everyone to not sort of run away with this too much because we still don’t know what ultimately will be implemented. You know how much of this is posturing both by our country as well as others. I mean will we have an all out trade war.

It’s a bit hard to say but I would say if you look at our exposures within the portfolio we do have some Chinese companies that are involved in export but they’re very interconnected with their US partners. So it’s harder to see them be affected in a negative way you know for example as I mentioned we own Haun high which is the world’s largest E.S. company. Now the number one product that this company assembles is Apple iPhone’s so you know it would be hard to see that company particularly harmed. You know with potential trade wars moving forward do you have any comments on the Russian sanctions and implications for the portfolio. Yes so as I mentioned we are overweight Russia. We own a number of energy names and then in the materials space we also own Norilsk Nickel. So some of our names are are more effective than others you know in the case of Norilsk. The stock took a big hit a few weeks ago because one of the major shareholders was on the sanctions list himself. Now this does not affect the company’s earnings at all or its operations. And he’s not on the board and doesn’t have any control of the company. So we actually took advantage of that relative price move to raise our position in that particular stock and we took a away out of some of our other Russian holdings so we didn’t want to raise our exposure to Russia overall quite frankly. You know this is a political moment and it’s you know we don’t have any special knowledge about the outcome of it.

However the relative attractiveness of this company given what we don’t see as particularly enhanced risk within the operation has made it a bit more attractive to us. I think the last question How long has the Zeenat invested in emerging markets. So we started our first standalone EMEA strategy the IOM focused value strategy back in 2008. However we’ve been investing in global and international strategies going back to 2004 and both of those were always included in the emerging market component. So we’ve been researching names going back then and so it’s been 14 years. Thank you everyone for joining the call today. And I greatly appreciate your interest in our firm.

{kind=link}