Top execs utilize trading window to increase stakes in telecom networking equipment maker on weakness

SEC Form 4’s filed for telecom and networking equipment maker DZS Inc (NASDAQ:DZSI) after the Thursday, Feb. 23 market close revealed the group’s CEO, Charles Vogt, and CFO, Misty Kawecki, had purchased shares on market after the stock plunged on weak fourth quarter results. Shares were up 0.7% in the trading day following the news.

Q4 2022 hedge fund letters, conferences and more

The transactions were initially spotted on Fintel’s latest CEO purchases page, later on Thursday evening.

DZS shares closed -23.1% lower on Feb. 17 after the company reported a Q4 earnings miss accompanied by underwhelming guidance against market expectations. After the share price started showing signs of recovery last week, Vogt and Kaweck utilized the officer trading window and increased their stakes.

CEO Charles Vogt purchased 20,000 shares on Feb. 22 at an average prcie of $10.98 per share for a total transaction value of $220,000. Vogt’s owns a total of 83,705 shares following the purchase.

CFO Misty Kawecki bought a total of 10,000 shares across three transactions on Feb. 22 and Feb. 23 at prices ranging from $10.64 to $10.84 per share, and an average price of $10.695 apiece. The transactions had a total value of $106,950 and increased Kawecki’s total share ownership to 22,107 shares in the Plano, Texas-based company.

When company officers buy shares with their own money, it usually signals a vote of confidence in the company’s outlook. In this instance, while the company has provided below-expected guidance, the company officers may be bullish on the medium-term outlook beyond 2023.

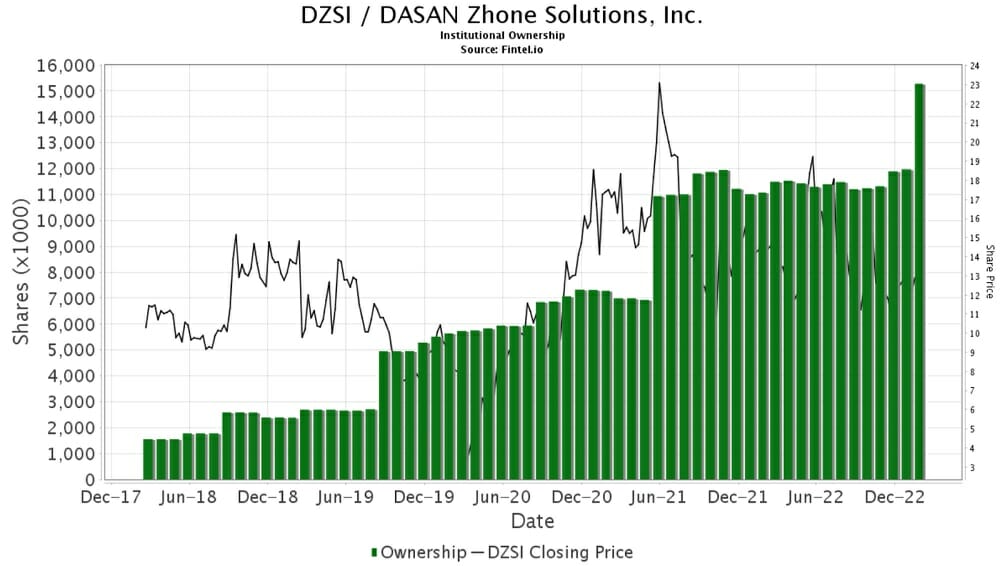

For some comparison on the institutional investor front, the company has experienced above average levels of interest as indicated by Fintel’s bullish fund sentiment score of 84.52. This score ranks DZSI in the top 6.2% out of 36,094 globally screened companies for the highest levels of fund buying activity.

The chart to the right shows the growing level of institutional ownership in the stock over the last five years.

There are 211 institutions on the register that hold around half of DZSI’s float of 15.42 million shares. The largest institutions on the register are AIGH Capital Management LLC, Royce & Associates LP, AWM Investment Company, BlackRock Inc, Vanguard Group Inc, King Luther Capital Management Corp, Divisar Capital Management LLC, and Hodges Capital Management Inc.

For the final quarter of 2022, the company generated $100.2 million in sales, down 4% from Q3 and falling short of analyst polled forecasts of around $115 million.

Revenue in the Access Networking Infrastructure division fell 4% from Q3 to $87.8 million and the Cloud Software & Services segment sales declined 21% over the quarter-to-quarter to $12.4 million.

The company reported adjusted EBITDA of minus $3.1 million for the quarter, well below analyst forecasts expecting a positive figure above $5 million.

Orders of $90 million were healthy, coming off a record figure of $134 million in the same quarter of 2021. The company told investors that it had a backlog of $321 million, significantly higher than the $234 million backlog at the end of the preceding year.

For 2023, DZS’s management set market expectations for sales of $420 million to $450 million with positive adjusted EBITDA of $25 million to $40 million.

B Riley Securities analyst David Kang is still bullish on the company with a ‘buy’ recommendation on the stock. Kang told investors that 2022 results were impaired by supply chain and foreign exchange headwinds that continue to weigh down earnings.

He continues to believe that a strong backlog balance with solid bookings can drive solid sales growth in 2023. As a result of the update, B Riley’s ‘buy’ call target price was reduced to $23 from $28, still more that double current levels, after factoring in the performance and outlook.

Fintel’s consensus target of $23.12 suggests the stock see 110% upside in 2023. Our consensus target is made up of three strong buy calls included in eight total buy calls and one hold call on the stock.

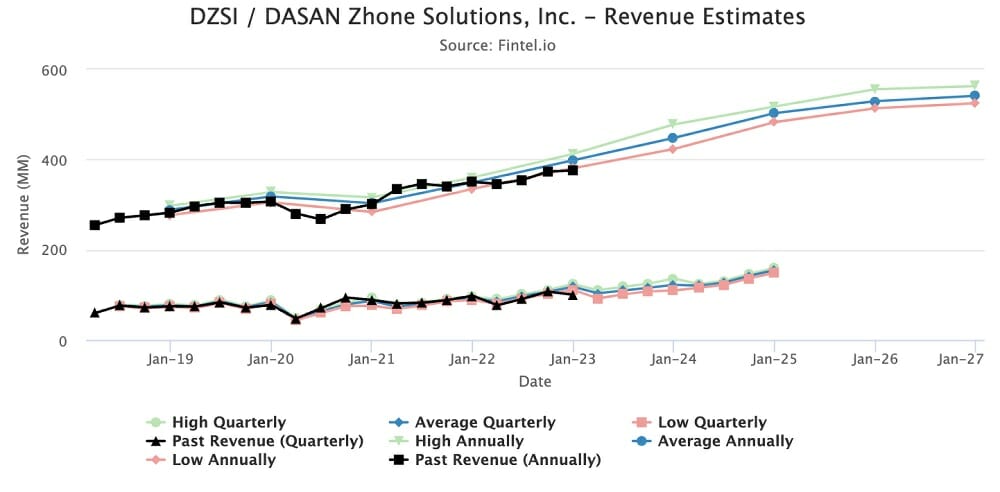

The chart below from Fintel’s forward estimates page shows analyst’ forward revenue expectations for the next five years.

Article by Ben Ward, Fintel