Enhancing Dividend Yield

SUMMARY

- Buying high yielding and selling low yielding stocks is not an attractive strategy

- Combining Dividend Yield with Quality & Growth factors improves the performance

- Interestingly Dividend Growth adds relatively little value

Check out our H2 hedge fund letters here.

Introduction

According to MorningStar assets under management of smart beta products breached $1 trillion in 2017 and more than half of the assets were invested in just three factors: Value, Growth and Dividend Yield. Naturally there is a significant amount of empirical evidence that suggests Value stocks generate positive excess returns across time, but much less evidence for the latter two factors. We published a research note in 2017 – Resist the Siren Call of High Dividend Yields – where we highlighted that buying high yielding and selling low yielding stocks has been a highly unattractive strategy over the last century. High dividend yields typically indicate high risks and investors have not been compensated for taking these, especially on an after-tax basis. However, perhaps the risks can be mitigated by combining high dividend yields with other factors. In this short research note we will analyse various Dividend Yield factor combinations.

Methodology

In this research report we focus on six factors namely Dividend Yield, Value, Momentum, Quality, Growth and Dividend Growth. The factors are created by constructing long-short beta-neutral portfolios of the top and bottom 10% of stocks of the US stock market. The factor combinations are based on the intersectional model, which selects the stocks in the intersection of the factors. Only stocks with a market capitalisation of larger than $1 billion are included. Portfolios are rebalanced monthly and each transaction occurs costs of 10 basis points.

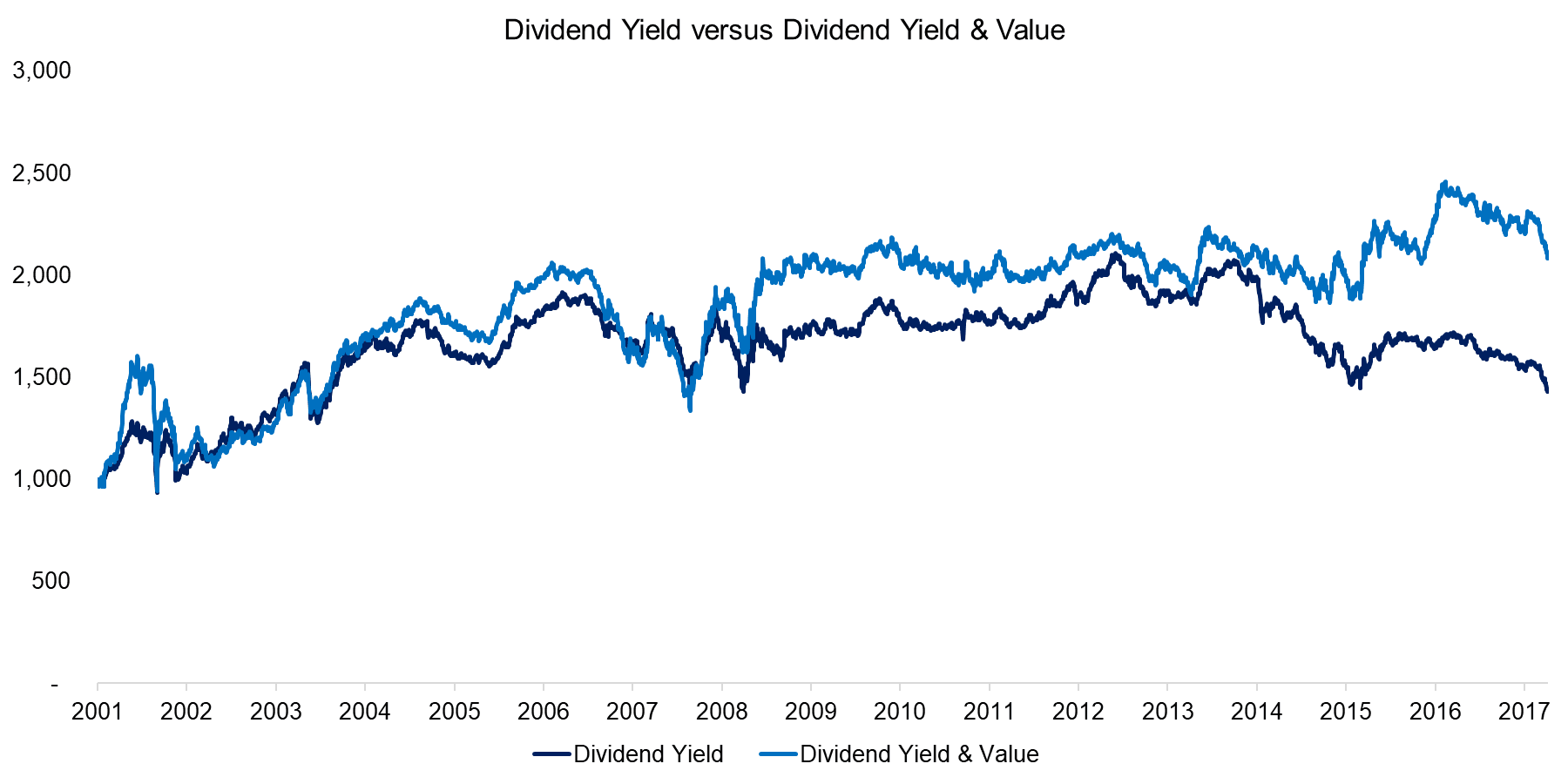

Dividend Yield Versus Dividend Yield & Value

The chart below shows the performance of a long-short portfolio based on the Dividend Yield factor and an equal-weight combination of Dividend Yield and the Value factor, e.g. the long portfolio will contain stocks that are high yielding and cheap on price-to-earnings and book-value multiples. We can observe that both profiles are comparable, which is not unexpected given that Dividend Yield can also be considered a Value metric.

Source: FactorResearch

Dividend Yield Versus Dividend Yield & Momentum

Given that Dividend Yield and Value are positively correlated, investors might want to combine Dividend Yield with a factor that offers a low or negative correlation. Momentum fulfils that criteria and we can observe that this combination looks substantially different to the Dividend Yield factor on its own. However, the performance does not look particular attractive and we can clearly identify the Momentum crash of 2009.

Source: FactorResearch

Dividend Yield Versus Dividend Yield & Quality

One of the key concerns of yield-seeking investors is reductions in dividends. Investors can therefore look for stocks that are high yielding and quality companies, which we define as corporates with high returns-on-equity and low debt-to-equity ratios. The chart below shows the combination of the Dividend Yield and Quality factors, which highlights a more consistent performance compared to Dividend Yield on a stand-alone basis.

Source: FactorResearch

Dividend Yield Versus Dividend Yield & Growth

As an alternative to looking for high yielding, quality companies, investors can also consider companies that are showing high growth rates in sales and earnings, which should mitigate the risk of a dividend reduction and potentially even lead to increases in the dividend. The chart below shows the combination of the Dividend Yield and Growth factors, which highlights a relatively consistent performance.

Source: FactorResearch

Dividend Yield Versus Dividend Yield & Dividend Growth

Instead of focusing on quality and growing companies, investors can also select stocks with high dividend yields and growing dividends. Interestingly this combination does not improve the performance and can be explained by that Dividend Growth, which we define as the annual growth in dividends, shows an almost flat performance since 2000. The long portfolio of Dividend Growth consists of companies that rapidly increased their dividends, i.e. represents companies that likely restructured their business recently, while the short portfolio comprises companies that recently cut their dividends, i.e. stocks that likely have been declining for a while as dividend cuts tend to reflect ailing businesses. Dividend Growth effectively represents a combination of the long side of the Value factor and short side of the Momentum factor, which we have seen in the analysis above as not accretive to the Dividend Yield factor.

Source: FactorResearch

Dividend Yield Combinations: Risk-return Metrics

In addition to observing the performance of the dividend yield combinations, we can also analyse the risk-return ratios for the period from 2001 to 2017. All combinations show higher risk-return ratios than the Dividend Yield factor on a stand-alone basis, which highlights diversification benefits. The factors that likely mitigate the risk of dividend reductions, i.e. Quality and Growth, improve the risk-return ratios most.

Source: FactorResearch

Further Thoughts

This short research note highlights various combinations of Dividend Yield and other factors, where the Quality and Growth factors lead to the highest increases in risk-return metrics, which is intuitive. Naturally this implies avoiding the stocks with the highest yields, which can be emotionally challenging in this yield-starved environment.

About The Author

Nicolas Rabener is the Managing Director of FactorResearch, which provides quantitative solutions for factor investing. Previously he founded Jackdaw Capital, an award-winning quantitative investment manager focused on equity market neutral strategies. Before that Nicolas worked at GIC (Government of Singapore Investment Corporation) in London focused on real estate investments across the capital structure. He started his career working in investment banking at Citigroup in London and New York. Nicolas holds a Master of Finance from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon, Mont Blanc, Mount Kilimanjaro).

Article by Factor Research

{kind=link}