David Einhorn’s Greenlight Capital has made some big changes in Fannie Mae holdings. In his Q2 2021 letter to investors (full copy of Greenlight’s investor letter can be found here), Einhorn states:

Q2 2021 hedge fund letters, conferences and more

During the quarter, we had a loss in the preferred stocks of Fannie Mae and Freddie Mac (“GSE preferreds”). We had bought them in 2014, partially hedged by shorting common stock. Our thesis was that we could do well if the companies were recapitalized and released from conservatorship, and that shareholders had valuable claims against the U.S. government, which had unilaterally changed the deal and essentially nationalized the companies right as they were about to recover. We believed that under the Trump administration, there was substantial interest in settling the lawsuits and releasing the companies.

In January, the GSE preferreds fell when it became clear that the Trump administration had left without putting the GSEs on a clear path to being released. Nevertheless, we remained optimistic about the legal case, which had reached the U.S. Supreme Court. In the lower courts, Democratic-appointed judges had tended to support the government and Republican- appointed judges had tended to support the shareholders; so we were surprised in June when the Supreme Court ruled in the government’s favor in all the important aspects of the case. This caused the GSE preferreds to collapse. In the earlier years, the position had been quite profitable and we reduced it at favorable prices. While we achieved a low double-digit IRR over the life of the position, it was a loser in 2021.

Q2 2021 hedge fund letters, conferences and more

David is also betting on some commodities, such as single family detached housing, air freight, copper, titanium dioxide, cement, thermal coal and natural gas, and paperboard, Einhorn states:

We know what the President wants – if you are having trouble finding enough labor, “pay them more.” Sounds like a wage inflation policy to us.

As for the Fed policy response, the market seems to think that by simply noticing inflation and, perhaps, making modest changes to monetary policy, inflation will be brought under control. But what if what’s needed isn’t merely tinkering? Reported inflation last month annualized at a double-digit rate. What if the need is an immediate end of quantitative easing and a rapid increase in rates? The so-called Taylor rule4 says the correct Fed funds rate today would be about 5%.

We think the answer is, if that is what is needed, it won’t be done. Chairman Powell is committed to remaining very accommodative for a long time and then only gradually tightening. We believe he will find whatever excuse he needs to do so, no matter what the data shows.

The result, we believe, is that inflation won’t be aggressively addressed. So, the risk is to the upside. In our macro book, we hold inflation swaps and gold. The former will benefit from reported inflation being higher than the market expects. The latter should benefit as the market realizes the Fed is behind the curve and has no plans to catch up.

Q2 2021 hedge fund letters, conferences and more

Single Family Detached Housing

From 1960 through 2002, an average of 1.1 million single family homes were constructed in the U.S. per year. During the bubble years of 2003 to 2007, that grew to an average of 1.5 million. So, if average demand is 1.1 million, an extra 2 million houses were constructed over those 5 years. It was a bubble.

Post-GFC, construction has averaged just 700,000 new homes a year. Over a dozen years, the reduced construction helped absorb the 2 million extra houses and created a housing deficit of a similar amount, assuming no long-term change in the demand for single-family housing despite a growing population.

COVID exposed the shortfall. Average house prices are up about 20% year-over-year and there are record low inventories. It will be difficult for the industry to catch up. First, zoning and land development have become much more difficult, time-consuming and expensive. Second, land developers and homebuilders are not being showered with cheap equity capital to expand rapidly to take advantage of strong market conditions and reverse the shortfall. In fact, on a national basis, there are 17% fewer active homebuilding subdivisions than there were a year ago.

While many investors are worried that demand will wane and home prices will fall, as evidenced by awarding builders single digit P/E multiples on earnings estimates that are likely to be dramatically exceeded,2 we think it is much more likely that the inability to satisfy demand will persist and lead to even higher prices.

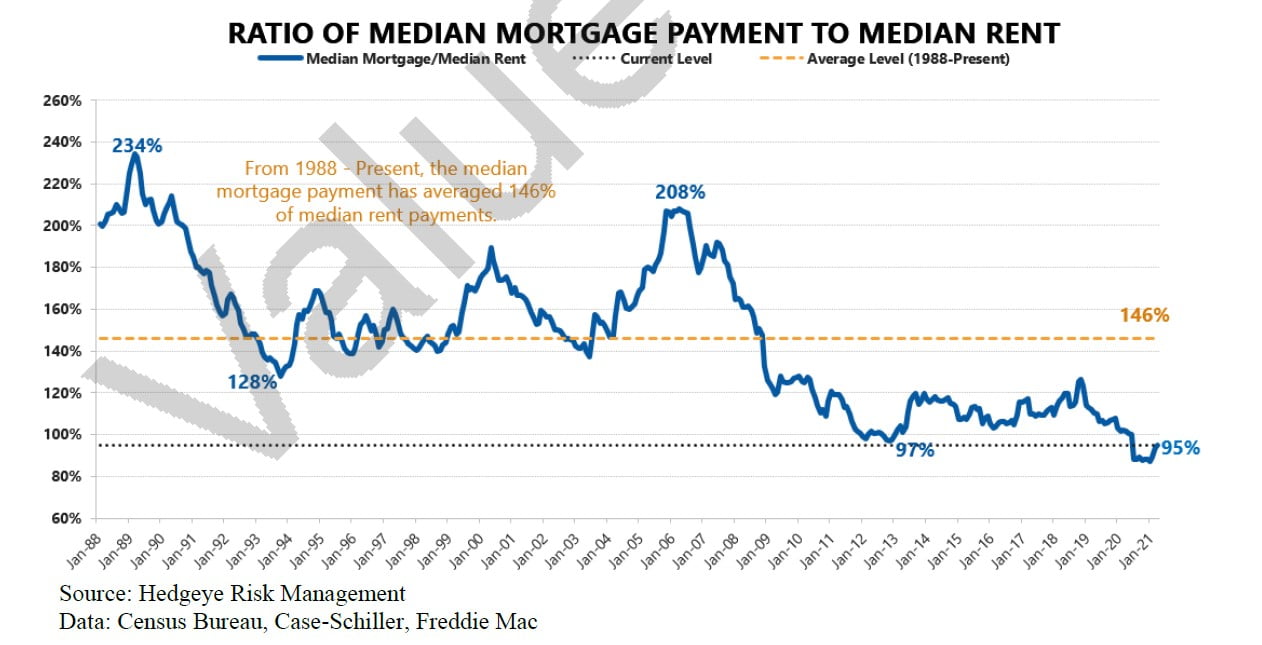

The following graph illustrates that despite the recent increase in home prices, home ownership in the U.S. remains historically attractive relative to the cost of renting:

We haven’t even begun the process of higher home prices begetting additional demand as homeowners commence cash-out refinancing and use the appreciation from existing homes to move into more expensive homes. Rising prices will also attract current renters, who come around again to the notion that owning a home is an attractive lifetime investment. Further, we expect the Biden Administration to possibly turbocharge an already tight market by attempting to expand home ownership opportunities.

A small tweak in monetary policy isn’t going to resolve the decade-long underinvestment in housing. Green Brick Partners (NASDAQ:GRBK), our largest investment, is poised to benefit from this dynamic. It trades at around 7x this year’s consensus earnings estimates.

Q2 2021 hedge fund letters, conferences and more

Air Freight

COVID caused a dramatic reduction in passenger aviation. Passenger planes often carry freight in their bellies. With planes grounded, capacity came out of the industry. At the same time, freight demand expanded both due to the recovering economy and growing ecommerce, which often emphasizes air shipments. While there has been some recovery in passenger aviation, airlines are emphasizing narrow-body planes, which carry less freight than wide-body planes. Compared to 2019, current air freight demand is about 10% higher and capacity is about 10% lower. The result is that cargo rates have exploded.

Supply will be slow to come on-line. Some passenger planes are being converted to freighters, but conversion capacity for wide-bodies is limited and the aggregate impact of this will be modest. Meanwhile, air freight companies trade at tiny multiples of what investors assume to be peak profits. The implied cost of equity is quite high, which makes it difficult to justify adding assets. As a result, air freight companies are in no rush to order new planes, and in any case, new orders would take several years to build. The result is rates and profits are likely to be higher than expected for quite some time.

We own Atlas Air Worldwide (NASDAQ:AAWW), which is poised to benefit. It trades at around 5x this year’s consensus earnings estimates.

Q2 2021 hedge fund letters, conferences and more

Copper (and other basic materials)

The last boom in mining ended badly in 2009. The result is that mining companies have been loath to develop new mines over the last decade. The current development pipeline of new copper mines is down 60% from what it was in 2008. While a few mines are set to come online in 2022 and 2023, by mid-decade, supply is expected to start shrinking. It takes about 8 to 10 years to develop a copper mine.

Meanwhile, the electrification of the automobile industry and expansion of green energy will create substantial new demand for copper. Prices are up some already, but it is difficult to see why they won’t be much higher a few years from now.

We own Teck Resources (NYSE:TECK), which is one of the few copper miners that are poised to expand to take advantage of this dynamic as it has a new mine coming on-line in 2022. TECK trades at 7x this year’s consensus earnings estimates that obviously don’t include contribution from the pending new mine. We presented this thesis more fully at this year’s Sohn Conference.3

Q2 2021 hedge fund letters, conferences and more

Titanium Dioxide

Titanium dioxide is the chemical that makes coatings and plastics white or opaque. There was substantial capacity added in China between 2011 and 2013, but little since. In fact, some Chinese capacity has been shuttered for economic and/or environmental reasons. The last plant built in the U.S. came on-line in 2016 and added 2.8% to global capacity. There had been no Western capacity built for many years prior to that, and presently, no Western company has announced plans to build new plants. The post-COVID construction boom (possibly followed by an infrastructure boom) has left the world structurally short titanium dioxide. Spot pricing is up substantially this year in the face of supply shortages.

We own Chemours (NYSE:CC), which is one of the few industry players with some spare capacity and is poised to benefit from higher prices and volumes. It trades for around 10x this year’s consensus earnings estimates.

Cement

A new greenfield cement plant hasn’t been built in the U.S. since 2009. The permitting is nearly impossible. Again, we are in the early stages of a construction boom (possibly followed by an infrastructure boom). It is a concentrated industry, with local oligopolies. Prices have risen steadily over the years (47% since 2011), and the latest inflation data showed a 1.8% monthly increase. Anecdotally, we have heard that supply in many markets is tight and prices are poised to rise further. High shipping costs make imports less competitive.

We own Buzzi Unicem (BIT:BZU), which is an Italian company with a global footprint, although it generates about half of its EBITDA in the United States. BZU will likely end 2021 with net cash on its balance sheet and currently trades at around 10x current year consensus earnings estimates.

Q2 2021 hedge fund letters, conferences and more

Thermal Coal and Natural Gas

ESG investing is inflationary, as green energy is simply more expensive than hydrocarbons. Hydrocarbon energy companies are starved for capital and are being told to change their ways. The result is less exploration and drilling. Even with benchmark oil prices surging over the last year, companies are loath to drill more. Normally, the cure for high prices is high prices. With ESG in the proverbial driver’s seat, we might need much higher prices still in order to increase investment to meet demand.

There is almost nothing less popular than thermal coal. From 2011 to 2020, U.S. coal production declined by 51%. U.S. demand has fallen as we’ve shifted to alternative sources of electricity. As unpopular as coal is though, it still makes up about 20% of U.S. electricity generation. Globally, coal demand is growing modestly as China and India add power generation capacity faster than the West is reducing it. Even so, reduced oil and gas drilling has caused natural gas prices to advance and coal prices are following. Seaborne thermal coal prices are up 140% year-over-year and at the highest levels since 2011, and Northern Appalachia thermal coal prices are catching up, rising 23% in the last month alone.

We own CONSOL Energy (NYSE:CEIX), the lowest cost, most efficient miner in Appalachia, which is poised to benefit from rising coal prices. It trades at 12x consensus earnings estimates that look stale to us, as they do not reflect recent coal price gains.

We also own Gulfport Energy (NYSE:GPOR), an Appalachian natural gas driller that recently emerged from bankruptcy and is poised to benefit from higher natural gas prices. Currently, there are no analyst estimates for GPOR.

Q2 2021 hedge fund letters, conferences and more

Paperboard

The U.S. has added so little paperboard capacity that the average mill in this country is over 30 years old. The industry operates at around 93% capacity and demand is growing both with consumption and due to ESG-driven substitution of paper packaging instead of plastics and Styrofoam. The industry is consolidated with just a few players, capable of exerting pricing power. We don’t expect anyone to build a new plant anytime soon. We own Graphic Packaging (NYSE:GPK), which is the lowest cost producer with the largest market share and is poised to benefit from rising prices. It trades at 13x consensus earnings estimates.

The point is, we believe we have reached a structural change in inflation. Part of that is driven by public policy, but part of it has been driven by capital markets and ESG mandates. The enormous emphasis on investing in often money-losing businesses in disruptive areas like technology has left traditional industries starved for growth capital. The result is they haven’t grown capacity and now they cannot meet demand. The more these “value” stocks are starved of capital, the higher prices are likely to go and the longer the inflation is likely to last.

And this doesn’t even begin to address the rising cost of labor. Currently, there is a labor shortage and there are approximately 9 million open jobs according to the latest government data. In the coming months, unemployment benefits will be cut. This will drive some of the unemployed back into the workforce. Deflationists believe it will be enough to end the labor shortage. However, since people can collect benefits without being required to look for work, it is unclear how many benefit collectors are happy to receive benefits, but have no plans to rejoin the labor force. It will take time to determine how much of the labor shortage is structural.