Crescat Capital commentary for the month of June 2018.

Q1 hedge fund letters, conference, scoops etc, Also read Lear Capital: Financial Products You Should Avoid?

Dear Investors,

We strongly believe that the global macro investment cycle is turning down right now. We think it’s a critical time to take investment action if you are not already prepared. At Crescat, we are positioned to capitalize on a variety of bearish macro themes:

- China currency and credit bust

- Emerging market contagion

- Bursting of Australian and Canadian housing bubbles

- US stock market late-cycle valuation top

- European disunion

- Precious metals valuation bottom

We are positioned to capitalize on these themes in unique ways across all three of our investment strategies:

- Crescat Global Macro Fund: A multi-asset class hedge fund with a currently significant short emphasis, including a net short position in global equities, sovereign debt, and Chinese yuan

- Crescat Long/Short Fund: A global long/short equity hedge fund currently with a significant net short position

- Crescat Large Cap: A long-only separately managed account strategy, currently with high cash and precious metals exposure

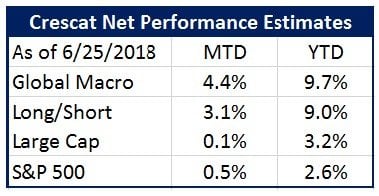

All three Crescat strategies have a long-term track record of beating the S&P 500 net of fees since inception, even including after the long bull market since early 2009. We are not perma-bears, but we are certainly macro bears today and positioned as such. It is paying off already, even in an up market. We think this is strong evidence that our time has arrived. Imagine what we can do when the S&P 500 breaks down again like it only started to in February.

How can Crescat Capital’s two highly short hedge funds be beating the S&P 500 that is up year to date? Because global market breadth has already been falling apart and many of our shorts therefore have been working. Emerging market stocks have already been breaking down in the face of wrong-footed investor shock. China is starting to unravel. Europe is similarly in turmoil again as a populist Italian government has taken control and reignited the European sovereign debt crisis. Housing bubbles in Canada and Australia are already beginning to burst. It is happening, and it is happening right now in our strong view. We believe our bearish themes are only just starting to play out.

Crescat Capital had the number-one performing global macro hedge fund in February 2018 according to BarclayHedge while a broad swath of money managers across all stripes lost money. Our Global Macro Fund was up 8.6% net that month while the S&P 500 was down 3.7%. Crescat Long/Short fund was up 8.0% that month. That was just a glimpse of what we believe is only starting to unfold.

Investor greed combined with global central bank liquidity have achieved the largest global financial asset bubble ever. The Federal Reserve, the arbiter of the global reserve currency, has already pulled the liquidity punch bowl away, but global investing party-goers are still intoxicated. They are near-record long and do not know how to sell. They certainly do not know how to sell short. Their judgment is impaired. If ever there was a time to be positioned counter to masses of teetering long investors, we think it is now.

As macro thematic hedge fund managers and principled value investors, we are determined to capitalize on the coming downturn in global financial asset prices.

The credit bubble in China is the largest the world has ever seen. Fed tightening and Trump trade war threats are the catalysts that are finally bursting it. Our China yuan short inside the Crescat Global Macro Fund has been working this year (see the profit attribution above for this month alone), but it’s only the beginning. In our strong view, it is the biggest opportunity in the currency markets ever, and we think it is only just starting to play out right now. Crescat/Long Short Fund also has exposure to a yuan depreciation through its China equity shorts.

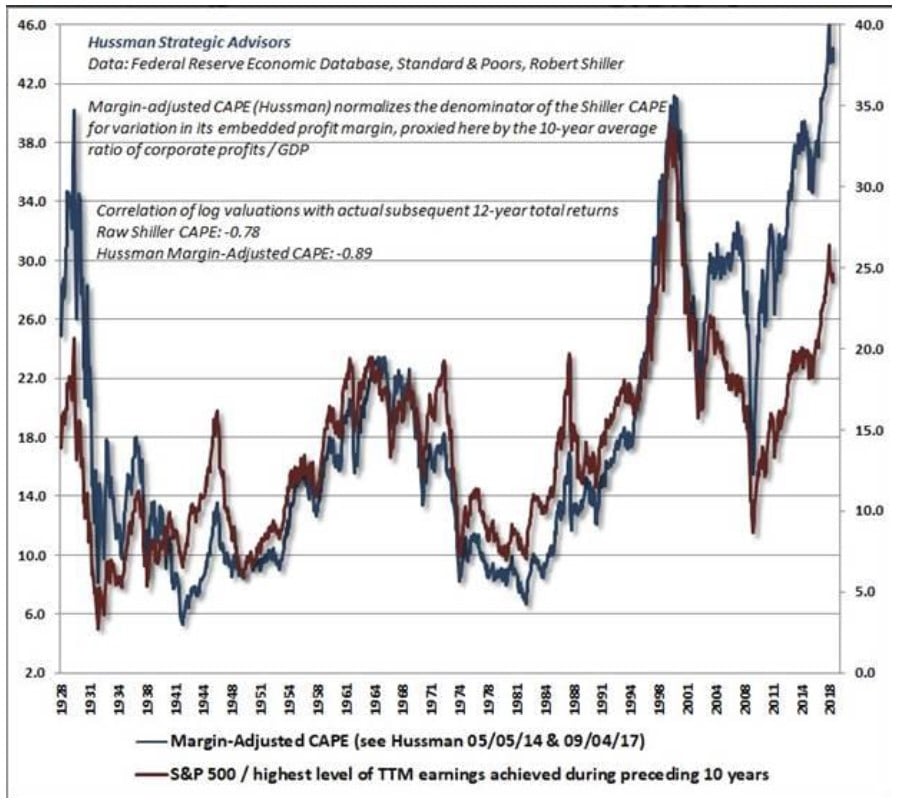

This month, US stocks have essentially been re-testing their January highs. We think unsuspecting investors have been sucked back into the market in a classic bull trap. We believe January was a real top and there are big down months like February just ahead. We are at historic valuations across essentially every fundamental dimension, as we showed in a recent quarterly letter. Simple price-to-earnings ratios do not show it, however. They are a value-trap at peak profit margins. Cyclically-adjusted P/Es (CAPEs) are the P/E ratios that matter today, as John P. Hussman, Ph. D, shows in his chart below. CAPE is a Nobel-prize winning formula. S&P 500 margin-adjusted CAPE already peaked with the January market top. These valuations are setting the market up for failure right now at the same time as we have late cycle Fed tightening.

US stocks are ripe for a major correction, a continuation of the one that already started to unfold in January of this year.

On the long side of investment opportunities, gold appears to have made a beautiful five-year consolidation and basing pattern. It is historically cheap compared to the global fiat monetary base. Meanwhile, global central banks have fostered a record debt bubble. It’s a historic macro imbalance that is unsustainable. Gold should skyrocket when this imbalance unwinds.

Crescat Large Cap is heavily tilted toward precious metals today. Crescat Large Cap can hold gold and silver as a proxy for cash. It has record cash and precious metals holdings today, as well as a large concentration in the biggest and best precious metals miners. We intend to capitalize on this classic haven trade for the coming bear market. Crescat’s hedge funds are long precious metals too.

If you are interested investing with Crescat, please reach out to Linda Smith at (303) 228-7371 or [email protected] for more information.

Sincerely,

Kevin C. Smith, CFA

Chief Investment Officer

Tavi Costa

Emerging Markets Analyst

Nils Jenson

Energy and Materials Analyst

© 2018 Crescat Capital LLC

{kind=link}