Shares of Saint Louis based retailer Build-A-Bear Workshop, Inc (NYSE:BBW) rose 22.6% on Thursday following a strong third-quarter results release which included a guidance upgrade. The rally today brings BBW’s stock back into positive territory for 2022, with a year-to-date gain of 14.4%.

Investors should be pleased with the small-cap’s share price movements over the year, outperforming broader equity markets. With a cheap PE ratio of 7.61, the Fintel platform ranks BBW in the top 20% of 19,263 companies that have the most attractive valuations.

Q3 2022 hedge fund letters, conferences and more

Find A Qualified Financial Advisor

Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to 3 fiduciary financial advisors in your area in 5 minutes.

Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests.

If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

Build-A-Bear’s Q3 Earnings

During the third quarter, Build-A-Bear grew revenues by 9.9% to $104.5 million from $95.1 million in the prior year. The growth would have been higher without the negative currency impact which reduced sales by $2.5 million.

BBW was able to hold gross margins firm over the year with 52.0% vs 52.1% in 2021.

Selling general and admin expenses of $44.4 million fell to a ratio of 42.5% of revenues from 43.8% in the prior year, resulting in bottom line margin expansion. EBITDA grew 13.4% over the year to $45.0 million from $39.7 million in 2021.

The retailer’s net profits grew 25.9% over the year to $7.46 million from $5.93 million in 2021. The net result equated to EPS of 51 cents compared to 36 cents in 2021.

BBW’s CEO and President Sharon Price John commented on the business’s positive performance, telling investors “With our fiscal 2022 third quarter, we have now delivered seven consecutive quarters of increased total revenues compared to the prior year’s period, with sustained profitability.

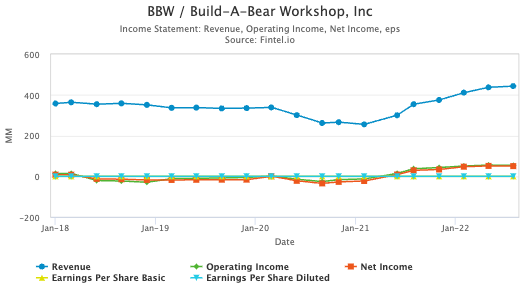

The chart to the right provided from the Fintel financial metrics and ratios page for BBW shows the recovery of sales and profits from lows during the pandemic.

Following the strong result, BBW’s management raised full year revenue guidance where it expects to generate sales of $455 to $465 million compared to previous guidance of $440 to $460 million.

BBW expects to finish the year with EBITDA in the range of $69 to $76 million, stepping up from prior guidance of $65 to $75 million.

Capex spending is expected to come in between $12 to 14 million and BBW expects to finish the year with inventory levels below FY21.

CEO John stated “we are raising our guidance and we are on track to deliver the most profitable year in our 25-year history, building on the 2021 results which set our previous high”

Analyst Eric Beder from Small Cap Consumer Research believes there is potential for further growth from the rollout out of new stores, product expansion and the ability to drive further operating leverage from the online segment. The firm remains ‘buy’ rated on the stock with a $33 price target.

Fintel’s insider sentiment score of 26.79 is bearish on the company based on weaker levels of insider build relative to other stocks.

Build-A-Bear has experienced 1 net insider who has sold stock over the last 90 days.vThe insider is an investment manager and activist investor, Cannell Capital who is the largest shareholder on the register.

The fund sold around ~75,000 shares in several transactions in early November following the stock’s swift recovery from annual lows experienced in September and October.

The investor also filed an amended 13D/A with the SEC earlier in the prior quarter, calling out management for a failed attempt at buying back stock and also suggesting a shake up of management who may not have investors’ interests best aligned.

Cannell Capital still owns 1.535 million shares following the sales equating to around 10.3% ownership of the float.

Article by Ben Ward, Fintel