For more than a decade and a half, my friend Alexander Green has been educating and entertaining investors as editor of numerous popular newsletters, many of which I’ve cited in my own writing.

Also read:

- Q2/H1 Hedge Fund Letters – Letters, Conferences, Calls, And More

- Baupost Letter Points To Concern Over Risk Parity, Systematic Strategies During Crisis

- AI Hedge Fund Robots Beating Their Human Masters

For those of you subscribed to one or more of his services through the Oxford Club or Investment U, I’m sure you’ll agree that Alex is among the finest financial writers working today. His articles are brimming with intelligence, humor, wisdom and candor—all of which he brings to his public appearances at investment conferences.

This week it was my pleasure to speak one-on-one with Alex, and together we touched on subjects ranging from our favorite books on investing to the secret lives of millionaires to business moats.

Below are highlights from the interview, but this is only the first of two parts. I’ll conclude it next week in a Frank Talk, which you can subscribe to here.

Enjoy!

You didn’t go into politics or medicine or law. What triggered you to go into the investment world?

At the time, I was living in Orlando. I got a copy of the Orlando Sentinel, and on the front page of the business section was a headline that read: “The average stockbroker in the U.S. makes $187,000 a year.” This was in 1985. Thirty years later, that’s still a substantial amount of money. I remember thinking: “If the average stockbroker makes $187,000, what do the good ones make?”

I crammed the article into my wallet and started telling everyone that I was going to become a stockbroker. Someone then told me that he had just sold a phone system to a broker in Winter Park, Florida, and he was looking to hire someone.

I went out and talked to him and got my first job in the money management business. At the small firm where I started, I was writing research reports and client communications. I discovered I enjoyed research and writing even more than dealing with clients, so when the opportunity arose to become a time financial writer, I took it. That was about 17 years ago.

You’ve published four books so far—The Gone Fishin’ Portfolio, The Secret of Shelter Island, Beyond Wealth and An Embarrassment of Riches. Tell us about the genesis of one or two of them.

I was speaking at a conference in Phoenix about 10 or 12 years ago, and when I came off stage, this older gentleman was waiting for me. He poked his finger at me and said: “Money, money, money. You’ve made a lot of money over the years, but I have to ask, do you ever think about anything else?”

At first I thought he was kidding, but come to find out, he really felt that I thought about nothing but money all day long. I realized then that I write hundreds of columns a year, and virtually every single one is about stocks or bonds, currencies or commodities, interest rates or economic growth. This guy figured I thought about nothing except money and how it’s made.

Of course, we all have our outside interests, and we hope for some kind of balance in our lives. And so when I went back home to Baltimore, I came up with the idea to write something expressing the idea that life isn’t just about making money. I wanted to talk about living a rich life, not just about getting richer.

This led to a column I initially called “Spiritual Wealth.” That name, though, became a problem since the word “spiritual” is one of the most nebulous words in the English language. It can mean any number of different things to different people.

I eventually changed the name to “Beyond Wealth,” which is probably more accurate anyway. It turned into a series of reflections on things that I thought were important—things I’d read or done that I felt were of interest. All of it had very little to do with money. Those articles became one of the most popular things we do, and the eventual book turned out to be a bestseller. I was glad to have found a wider audience out there.

At this year’s FreedomFest conference in Las Vegas, you debated with The New York Times’ Robert Frank about meritocracy and luck. Robert argued that our success in life is mostly due to luck, and you disagreed. Could you talk about that?

A good book to read on this subject is Thomas Stanley’s The Millionaire Next Door. Dr. Stanley spent a lifetime researching the habits and characteristics of the nation’s wealthiest individuals. I might add here that the Spectrum Group revealed that, as of the end of 2016, one out of every nine households in the U.S. had a net worth of $1 million or more. What Dr. Stanley found is that these millionaires have many characteristics in common. Primarily, they do everything in their power to maximize their income and minimize their expenses. They religiously save and invest the difference, then leave the money alone to let it compound for years, if not decades.

That’s how most people become millionaires, regardless of their color, sex or orientation—not by establishing a software company in their garage or making a hit record or playing third base for the Yankees. Most people just work hard, save, invest and compound.

How does that thinking apply to the market?

A few years ago, a guy named Burton Malkiel wrote a book called A Random Walk Down Wall Street. He said that it’s very difficult to beat the market, and even those who do beat it do so because of luck, not skill. So you can see we’re coming to the same sort of argument as Robert Frank.

The independent Hulbert Financial Digest has ranked our Oxford Communiqué in the top 10 investment newsletters in the nation for 16 years now. We beat the market for one year, two years, five years, 10 years, 16 years now. People would say: “Well, you’re just lucky.” It’s a tough thing to argue against. But when enough time goes on, and you continue to beat the market, it should clue someone in that there’s more than luck at play.

Would you say that Warren Buffett is just simply lucky? No, he’s a financial genius who’s taken actions that others haven’t, and he’s reaped the rewards. When Roger Federer won his 19th singles major title recently, nobody said: “Wow, he’s really lucky.”

I admit, everyone has certain amounts of good and bad luck in their personal and professional lives. But to say that luck is the only determining factor is dispiriting to people who have come the furthest. It’s demeaning to say that it’s all luck, not education or hard work or persistence.

Similarly, the people who consistently beat their benchmarks are not just lucky. If you do it long enough, it’s clearly evidence of skill.

Tell us about your “Gone Fishin’” portfolio. How do you look for investment opportunities?

The Gone Fishin’ portfolio is based on the idea that, since nobody knows with any certainty what the economy or market is going to do, it’s sensible to make the foundation of your portfolio a diversified, asset-allocated basket of index funds. You want to make sure your expenses are low and that you have high tax-efficiency and your asset classes are properly represented. Simple and straightforward.

The idea is that there are 10 different asset classes in the portfolio, and you invest according to various percentages: 30 percent in U.S. stocks, 30 percent in foreign stocks, 10 percent each in high-grade bonds, high-yield bonds and Treasuries, and 5 percent each in real estate investment trusts (REITs) and gold shares.

Then, at the end of every year—or on your birthday or anniversary—rebalance the portfolio to bring all the target percentages back into alignment. That reduces your risk because you’re cutting back on what’s depreciated the most and adding to what’s depreciated the least. Over time, this adds to your return while reducing the portfolio’s volatility.

What would you say to someone right now who’s nearing retirement age or who has just retired?

I don’t think enough people think about this, to be honest, Frank. Like you, I’ve been invested in the market for over 30 years, and when I was in my 20s, 30s and 40s, we had horrific selloffs like the stock market crash of ’87, the financial bust that happened when the internet media ended, and then of course the financial crisis. When you’re younger, you realize you’ve still got decades ahead of you, and you can take actions that allow you to be comfortable with whatever your long-term scenario might be.

But as you get older, after you reach the age of 50 or so, it becomes necessary to reevaluate your goals. There’s a bus out there waiting for us as we cross the street. The thing about getting older is, you have to reduce your risk. You’re not going to be working that much longer—or maybe you’re in retirement already—and you just don’t have the time to make it back should there be a market crash. I always say to make your portfolio as conservative as you can live with once you reach this stage of your life. It might crimp your returns, but it’s also going to save your butt if we go into another financial crisis like we did in 2008.

Are there any books on investing you’d like to recommend? How did they help you?

|

One book I would recommend is How to Make Money in Stocks by William O’Neil, the founder of Investor’s Business Daily. It’s probably 30 years old and has gone through some updates since then. O’Neil is looking for companies that have high sales growth, 25 percent or better compounds in earnings, higher returns on equity, great product innovation, good management and sustainable profit margins.

But to be honest, I think there’s only so much you can learn from books. I say that because you have to learn the hard way and actually feel the terror of a down draft, or fight the instinct to be greedy when you go through a long, full market as we’re in now.

So who do you look to? Where do you get your wisdom and insight?

In the mid-80s, there were three legendary investors: Warren Buffett, Peter Lynch and John Templeton. I started reading and listening to everything I could—all the Berkshire-Hathaway reports, but also tapes of Templeton and Lynch speaking at conferences.

No one knows what the economy or stock market is going to do, but Buffett, Lynch and Templeton knew to identify a business that was selling for a lot less than what it was worth and hold it until the market recognized that value. That sort of became the mantra for me from then on.

It was then that I realized I was not going to play this guessing game about what GDP growth is going to look like, what inflation’s going to be, what the Fed or stock market is going to do. That’s all a distraction. What really matters is individual businesses beating Wall Street expectations. That’s what drives stocks higher in the long term.

I often tell investors at conferences that, if you look back through history, you’d be hard-pressed to find a single example of a company that increased its earnings, quarter over quarter, year after year, and not see its stock tag along. It doesn’t matter what kind of market we’re going through or what kind of economy we’re in, those stocks tend to appreciate really strongly.

One of the publications you edit is the Momentum Alert. Can you tell us what that is?

Speaking of beating Wall Street expectations, this is exactly what we focus on in the Momentum Alert.

These companies tend to be superbly managed, but most important, they have a moat around the business. Let me give you three examples. Blockbuster, Radio Shack and Borders all went bust. There was no way for those companies to protect their margins, whether they were renting video tapes, selling electronic equipment or selling books and CDs. They had nothing to protect them from competition coming in and doing it on a bigger scale or doing it online.

Winning businesses tend to have something that protects margins. That could be a copyright or trademark or patent. Profits attract competition just as honey attracts bears. You’re not going to come across a really profitable niche and find that other people don’t want to exploit it also. You need something to keep them at arm’s length.

Think of the difference between IBM and Apple. IBM made its systems compatible, so other companies—Dell and Compac, for example—came in and made IBM-compatible machines.

No one makes an Apple-compatible machine because Apple never leased its patents to another company. All of those profits for the iMacs, iPhones, iPods and so on all go straight to Apple. That’s the kind of magic that can really help propel a stock up for longer periods of time.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.84 percent. The S&P 500 Stock Index fell 0.65 percent, while the Nasdaq Composite fell 0.64 percent. The Russell 2000 small capitalization index lost 1.20 percent this week.

- The Hang Seng Composite gained 0.86 percent this week; while Taiwan was down 0.08 percent and the KOSPI rose 1.67 percent.

- The 10-year Treasury bond yield rose slightly to 2.19 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector of the week, increasing by 1.25 percent versus an overall decrease of 0.41 percent for the S&P 500.

- Micron Technology was the best performing stock for the week, increasing 8.46 percent.

- Wynn Resorts stock was upgraded from “hold” to “buy” by Deutsche Bank on optimistic revenue forecasts largely stemming from the company’s operations in Macau.

Weaknesses

- Energy was the worst performing sector for the week, falling 2.65 percent versus an overall decrease of 0.41 percent for the S&P 500.

- Foot Locker was the worst performing stock for the week, falling 30.26 percent.

- Coach’s stock took a nosedive after the company released its fourth quarter earnings. Mixed fourth quarter results, coupled with disappointing fiscal year 2018 guidance, led the stock to drop by around 15 percent.

Opportunities

- Deere boosted its forecasts for sales this year amid increased demand for its farming equipment. The company said that “improving market conditions throughout the world” contributed to a 31.1 percent year-over-year increase in profits.

- While corporate share buybacks are the fuel that has kept the overall stock market rising, they’ve been a drag on the performance of the companies most active in executing them. However, that’s changing. Over the past two months, the companies with the most share repurchases have been beating the S&P 500. This points to a major turnaround for the group, which had been underperforming the benchmark since late 2013, according to data compiled by Bank of America Merrill Lynch.

- Gap reported better-than-expected, second-quarter results and raised its full-year profit forecast, helped by strong demand for Old Navy products and fewer discounts.

Threats

- Three U.S. pension funds sued six of the world’s largest banks on Thursday, including Goldman Sachs Group Inc. and JP Morgan Chase & Co, accusing them of conspiring to stifle competition in the more than $1 trillion stock lending market.

- While the U.S. stock market has shown resilience lately, it seems like there are some cracks forming under the surface. One measure called dispersion, which shows the degree to which the market’s best performers are diverging from the worst, is high right now, which some market experts think shows rising investor worry and risk aversion.

- Analysts at RBC Capital Markets aren’t convinced that Walmart can continue to grow. “Walmart’s productivity loop—operate for less, buy for less, sell for less, and grow sales—has been a very successful and powerful tool for the company, helping to create the biggest retailer on the planet,” they wrote in a note sent to clients Friday. “However, we believe that due to its already immense market share and the likelihood that everyone who was going to shop at Walmart already shops at Walmart, the company’s productivity loop has entered the phase of diminishing returns.”

The Economy and Bond Market

Strengths

- U.S. retail sales recorded the biggest increase in seven months in July as consumers boosted purchases of motor vehicles as well as discretionary spending.Retail sales jumped 0.6 percent in July versus a forecast of 0.4 percent. That was the largest gain since December 2016 and followed June’s upwardly revised 0.3 percent increase.

- Consumer confidence was better than expected in August, beating projections from economists. The University of Michigan consumer sentiment index rose to 97.6 in August. Economists estimated the index would climb to 94.

- The New York Empire State Manufacturing Survey strengthened to 25.2 for August from 9.8 previously. This was substantially above consensus expectations of 10.0 and the strongest reading since September 2014.

Weaknesses

- U.S. housing starts declined for the fourth time in five months, driven by a decline in multi-family housing construction. Total housing starts decreased 4.8 percent in July from the previous month to a seasonally-adjusted annual rate of 1.155 million, reports the Commerce Department.

- U.S. factory output fell 0.1 percent in July, pulled down by tumbling automobile production. Overall industrial production rose 0.2 percent, while economists had forecast industrial production increasing 0.3 percent in July.

- President Trump announced he was disbanding the Strategic and Policy Forum and a separate manufacturing council. A mass exodus of executives had made their end seem imminent.

Opportunities

- U.S. durable goods orders reported next Friday will confirm whether or not the recent recovery in business spending has legs.

- President Trump announced an executive order designed to streamline the approval process for building infrastructure by establishing “one federal decision” for major projects and setting a two-year goal for permitting. The administration plans to release a legislative packet this fall allocating $200 billion in federal dollars over 10 years to pay for large-scale and rural projects and to induce states, localities and the private sector to spend $800 billion.

- Millennials are finally buying homes and it means ‘pent up demand’ could last for years, extending the boom in the housing sector.

Threats

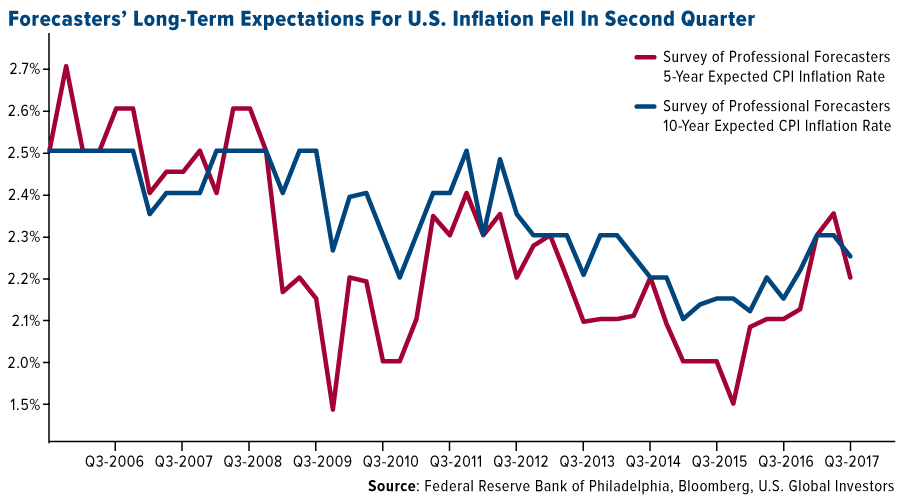

- Results from the Federal Reserve Bank of Philadelphia’s latest quarterly survey of professional forecasters revealed a drop in longer-term expectations for inflation. The decline in projections for average annual U.S. CPI increases over the next five years was the first since the fourth quarter of 2015, while 10-year expectations also moved lower. The results suggest less confidence than before among economists that Federal Reserve policy will bring about higher inflation on a sustained basis.

- Congress is on pace to be historically unproductive and that could be a headwind for the economy. If the slow pace of legislation continues, the confidence boost in the markets and economy due to Trump’s proposed policies may begin to fade. According to Michael Arone from State Street Global Advisors, “with no legislative victories to boast about and prospects for future wins dimming, concerns are growing that President Trump may pivot to the more controversial parts of his agenda where he doesn’t need Congressional approval, such as trade policy. At least in the short term, ill-advised trade policy won’t be good for the economy or markets.”

- Wednesday’s release of the minutes from July’s FOMC meeting showed most Federal Reserve officials support a move toward unwinding the Fed’s $4.5 trillion balance sheet at an upcoming meeting. This could prove a headwind for the bond market.

Gold Market

This week spot gold closed at $1,286.19, down $3.16 per ounce, or 0.25 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.51 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index rose 0.91 percent. The U.S. Trade-Weighted Dollar finished the week higher by 0.36 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-13 | China Retail Sales YoY | 10.8% | 10.4% | 11.0% |

| Aug-16 | Housing Starts | 1220k | 1155k | 1213k |

| Aug-17 | Eurozone CPI Core YoY | 1.2% | 1.2% | 1.2% |

| Aug-17 | Initial Jobless Claims | 240k | 232k | 244k |

| Aug-22 | Germany ZEW Survey Current Situation | 85.3 | — | 86.4 |

| Aug-22 | Germany ZEW Survey Expectations | 15.0 | — | 17.5 |

| Aug-23 | New Home Sales | 610k | — | 610k |

| Aug-24 | Hong Kong Exports YoY | 10.1% | — | 11.1% |

| Aug-24 | Initial Jobless Claims | 239k | — | 232k |

| Aug-25 | Durable Goods Orders | -5.7% | — | 6.4% |

Strengths

- The best performing precious metal for the week was palladium with a 3.42 percent gain. Citi forecasts a continued drop in diesel market share in Europe, while Russia’s largest palladium producer boasted of strong auto demand. Gold traders and analysts surveyed by Bloomberg are bullish for a ninth week, the longest run since March. Gold climbed higher this week after the dollar weakened following Federal Reserve minutes that showed lingering concerns over low inflation, reports Bloomberg. Worries over U.S. economic policy also pushed the yellow metal higher, after the nation’s top CEOs’ rupture with President Trump.

- Investors put $870 million into SPDR Gold in the second quarter, reports Bloomberg, bringing the fund’s assets to $34 billion. “Prospective risks are now rising and do not appear appropriately priced in,” Bridgewater’s Ray Dalio said in a LinkedIn post. Dalio recommends that investors allocate 5 to 10 percent of their assets in gold, the article continues.

- Bond funds added $3.5 billion in a twenty-second week of inflows in the last week, reports Bloomberg, while precious metal portfolios attracted $500 million of new money. On the flipside, equity funds posted their biggest outflow in 10 weeks. One potential market moving event next week will be the Fed’s summit on August 24-26 in Jackson Hole.

Weaknesses

- Platinum was the worst performing precious metal for the week, down 0.67 percent, as the positive views on palladium are negative for platinum. Last year Sibanye Gold Ltd., South Africa’s biggest gold producer, was bringing in money, sizing up acquisitions and plotting expansion projects. Today, however, the company is making losses and shutting mines, reports Bloomberg. The main difference between now and then is the rebound in the rand, which has strengthened about 23 percent since it changed direction in January 2016. Although a weaker local currency opens up more profitable gold to be mined, a stronger rand also means higher costs, the article continues. In some cases, this renders entire mines unprofitable.

- This week, tensions between the U.S. and North Korea moved from center stage, decreasing demand for safe-haven assets, reports Bloomberg. In addition, the Fed’s William Dudley signaled that he still favors another interest rate rise this year.

- Gold prices in India were at their widest discount to international prices in 11 months on Friday, reports the Times of India. The discounts are due to sluggish demand and an influx of the yellow metal sourced from South Korea. “South Korean supplies are distorting the market,” said N. Vijay, a bullion dealer from Salem in southern India. “Retail demand is still weak due to the price rise.”

Opportunities

- According to the head of precious metals at VTB Capital, a Russian investment bank, gold prices are set to jump to a four-year high of $1,400 an ounce by the end of the year, reports Bloomberg. Fueled by global political risks and buying from China and India, Evgeny Ananiev of VTB believes bullion could rise to $1,360 within three months before climbing even higher.

- India’s top maker of branded jewelry by market value, Titan Co. Ltd., expects sales from its Tanishq stores to rise 30 percent this fiscal year, reports Bloomberg. India’s tax overhaul is helping to attract more customers as the company expands its network. Titan saw shares rise to a record even as bullion prices fell. Sandeep Kulhalli, senior vice president for retail and marketing at the jewelry arm of Tata Group, noted that customers who once shied away from Titan due to higher prices (and who favored the flexibility of smaller jewelers), have changed their minds. Now, customers are shifting to branded stores because of their trustworthiness.

- The blockchain revolution is gunning for the gold market, reports Bloomberg. Many companies are seeing blockchain systems as a revolutionary way to verify and record transactions, and are rolling out platforms to bring gold into the digital age, the article continues. Over-the-counter settlements with gold can sometimes take days, leaving price risk for buyers and sellers. “Using blockchain promises more transparency, security and speedier deals,” Bloomberg notes.

Threats

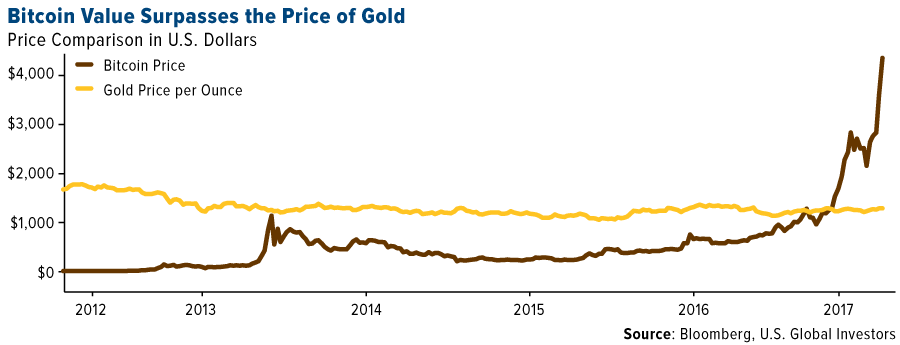

- Tim Price of Morgan Stanley notes in a research report this week that bitcoin’s value has lifted about five times since a period of relative stability pre- November 2016, to over $4,000 per bitcoin. As a commodity analyst, however, Price also notes that bitcoin is just another fiat money, not a commodity – so why flag it then? He says that beyond its ongoing price surge, some investors think bitcoin is better than gold as a hedge against inflation/uncertainty. He thinks that theory still needs to be tested though. A bearish risk for bitcoin’s price is few barriers to entry. “Over millennia, gold has demonstrated its ability to endure and preserve value under all circumstances. By contrast, bitcoin’s global platform literally requires the lights to stay on,” the report reads.

- Senate Republican Bob Corker told reports in his home state of Tennessee this week that President Trump needs to show more stability. “I think the president needs to take stock of the role that he plays in our nation and move beyond himself – move way beyond himself – and move to a place where daily he’s waking up thinking about what is best for the nation.” Corker’s words are some of the strongest Republican backlash to Trump’s suggestions that both sides bear blame in the Charlottesville incident, reports Bloomberg.

- President Trump announced that he is disbanding two advisory groups of American business leaders, reports Bloomberg, after two additional CEOs quit as the president faced blowback for failing to sufficiently condemn white supremacists. His remarks were a reversal of what he had said just one day before. Trump previously tweeted that he had plenty of CEOs who wanted to be on the panels to replace those who quit, and called the CEOs who left “grandstanders,” the article notes.

Energy and Natural Resources Market

Strengths

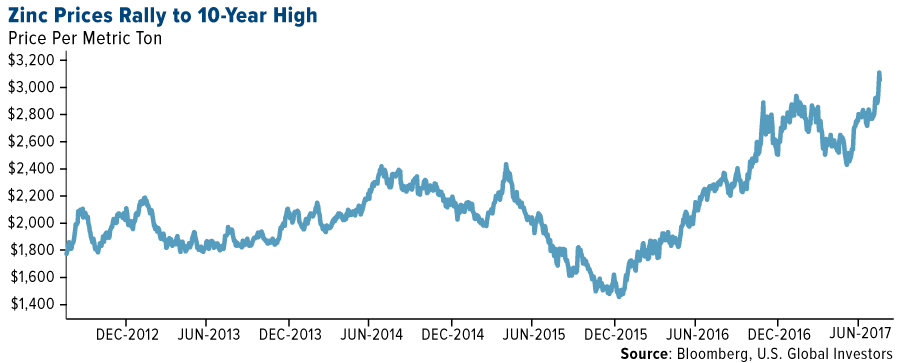

- Zinc was the best-performing commodity this week, rising 9 percent. The commodity hit its highest in almost a decade as Chinese infrastructure demand that has fed a rally in steel prices spills into markets for steelmaking raw materials.

- The best-performing sector this week was the S&P/TSX Diversified Metals and Mining Index. The index rose 4.9 percent tracking the record setting rally in zinc and other base metals prices.

- Vereinigte BioEnergie AG, a German manufacturer of biodiesel and bioethanol fuels, was the best performing stock this week, finishing up 13.1 percent. The company rallied as courts have failed to resolve anti-dumping complaints filed against Argentina and Indonesia which continue to favor domestic EU producers.

Weaknesses

- Natural gas was the worst-performing commodity this week, dropping 2.8 percent. Despite a much smaller than expected inventory build this week, the commodity slid the most among peers as weather forecasts show cooler temperatures will prevail over the Great Lakes.

- The worst-performing sector this week was the S&P 1500 Oil & Gas Exploration & Production Index. The index fell 3.8 percent after crude oil prices posted a third-consecutive weekly drop.

- The worst performing stock for the week was K+S AG. The German fertilizer producer and marketer dropped 8.5 percent to its lowest level of the year after the company abandoned its target of making €1.6 billion in profit by 2020, acknowledging that potash prices were unlikely to recover sufficiently.

Opportunities

- Gold rallied on Wednesday after Federal Reserve meeting minutes showed most participants preferred to defer the decision on ending reinvestments until an upcoming meeting while accumulating additional information on the economic outlook. With items such as the debt ceiling coming up within the next few weeks, there is room for further delays in the tightening cycle, which could provide a necessary boost for gold to break above the $1,300 per ounce resistance.

- U.S. crude inventories dropped for a seventh consecutive week, falling 8.95 million barrels last week to 466.5 million barrels to their lowest since January 2016. The draw was far more than double the 3.1 million barrel decline in crude inventories that analysts had forecast.

- U.S. President Donald Trump on Tuesday signed an executive order that would speed approvals of permits for highways, bridges, pipelines and other major building efforts. The American Petroleum Institute and the National Association of Home Builders praised the administration’s move.

Threats

- China’s home price growth slowed in July, with Beijing declining for a second straight month, reinforcing expectations that property price growth may stagnate over the course of the year. Compared with a year ago, new home prices rose 9.7 percent in July, easing from a 10.2 percent gain in June and marking the slowest growth since August 2016.

- Demand for crude oil may be weakening on the back of reports highlighting Chinese oil refineries operated in July at their lowest daily rates since September 2016.

- Iron ore and zinc may be reaching bubble territory according to certain investors. A number of reputable asset managers have voiced concern over the “bubble” in China’s commodities market. This week’s record-setting rise in base and industrial metals prices took place in spite of broadly disappointing macro data releases in China. With this weakening trend in mind, the asset managers in question believe iron ore and zinc provide compelling short-selling opportunities over the next six months.

China Region

Strengths

- Growth domestic product in the Philippines rose by 6.5 percent in the second quarter from a year earlier, reports Reuters. The economic pickup, which topped analyst expectations, can be attributed to a government-led construction boom and an extended rebound in the farm sector taking some “of the sting off a peso currency wallowing at 11-year lows,” the article continues.

- Shares in Sunny Optical surged to an all-time high in Hong Kong trading this week, reports Barron’s. The company’s net profits for the first six months of the year came in at RMB1.161 billion, which is a 149.7 percent year-on-year increase.

- Alibaba Group Holdings Ltd. beat projections in the June quarter, reports Bloomberg, with revenue jumping 56 percent and profit nearly doubling. The impressive sales numbers are fueled by “a core commerce business that’s adding users and increasing how much they spend,” the article reads.

Weaknesses

- A number of economic data out of China missed expectations for June, reports CNBC. Industrial output rose 6.4 percent, missing expectations of a 7.2 percent rise. July retail sales also missed forecasts slightly, coming in up 10.4 percent from a year ago rather than 10.8 percent. Fixed asset investment also rose 8.3 percent, against a Reuters’ poll of 8.6 percent. Despite the slowdown, the article continues, economists note the numbers aren’t “terrible.”

- In its annual review of China’s economy, the International Monetary Fund (IMF) projected that debt racked up by the Asian nation’s government, companies and households, will balloon to nearly 300 percent of GDP by early next decade, reports Bloomberg. China will eventually have to accept slowing growth. The IMF directors “noted that economic activity had recently firmed and saw this as an opportunity to accelerate needed reforms and focus on the quality and sustainability of growth,” the article continues.

- New home prices rose in fewer cities in China for the month of July. Prices climbed in only 56 of 70 cities tracked by the government, down from 60 in June.

Opportunities

- This week China Unicom, China’s second-largest mobile carrier, announced an $11.7 billion share sale as part of the ongoing government aim to privatize and streamline China’s various state-owned enterprises, or SOEs. Bloomberg reports that more than a dozen investors—including Internet behemoths Tencent and Alibaba—will collectively purchase a 35-percent stake in the company. While the state will remain the largest single owner, the share sale will relinquish the state’s majority holding and open board seats to the outside investors.

- According to Bloomberg, HSBC Holdings Plc has hired three Goldman Sachs executives to help strengthen its equities business in the Asia-Pacific region, people familiar with the matter said. According to the unnamed sources, Michael Chandler has joined HSBC as head of equity sales for the region (he was formerly Goldman Sach’s co-head of Asia-Pacific research sales). HSBC became the first foreign bank to win permission for a majority-owned securities joint venture in China, something its competition has been unsuccessful at securing, the article continues.

- A crackdown on China’s shadow banking has provided an opportunity for Chinese lenders, reports Bloomberg (and as seen in the chart below). Despite shadow banking taking a hit, people are now borrowing more from traditional banks as bond issuances have hit an eight-month high.

Threats

- Though Malaysian GDP surprised to the upside this week, coming in up 5.8 percent year-over-year for the second quarter, the economy may remain susceptible to souring sentiment in the event of another drop in energy prices.

- U.S. President Donald Trump authorized on Monday an inquiry into China’s alleged theft of intellectual property, reports Reuters. Officials from the Trump administration estimate theft of intellectual property by China could be close to $600 billion. “The investigation is likely to cast a shadow over relations with China, the largest U.S. trading partner, just as Trump is asking Beijing to step up pressure against Pyongyang,” the article reads.

- Aside from North Korea, CNBC reports a similarly worrisome situation between China and India squaring off over their shared border. On Tuesday, Reuters reported that Chinese and Indian troops were involved in a tussle in the western Himalayas, with Chinese soldiers attempting to enter Indian territory. Both countries have amassed troops in the area following a disagreement over the Chinese building a road in the disputed territory, the article continues.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 1.1 percent. Second quarter economic growth unexpectedly accelerated to 4.5 percent on a year-over-year basis, with a very strong pickup in growth of 2.3 percent in the second quarter. This was way above Bloomberg’s survey calling for a growth of only 0.8 percent in the past three months. The central bank hiked its main interest rate recently, and the probability of additional rate hikes is increasing.

- The Russian ruble was the best performing currency this week, gaining 1.4 percent against the U.S. dollar. Morgan Stanley recommends buying the ruble as the Bank of Russia is keeping real yields high. Two-year Russian government bonds are yielding 7.7 percent while inflation came down to 3.9 percent. Russia has the highest real rates, followed by Greece and Turkey.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 70 basis points. According to Capital Economics’ research, Russian activity data for July was a bit softer than expected. However, overall the report suggests Russia’s economy continued to grow by over 2 percent year-over-year at the start of third quarter. Industrial production growth slowed to 1.1 percent year-over-year last month from 3.5 percent in June, due largely to a slump in manufacturing.

- The euro was the worst performing currency this week, losing 50 basis points against the dollar. European Central Bank (ECB) minutes from the July meeting revealed that the bank is worried about the euro strengthening in the future. Stronger inflation weighs on inflation by making imports cheaper. July inflation stood at 1.3 percent in July, below the bank’s 2 percent target. Year-to-date the euro has gained almost 12 percent.

- Real estate was the worst performing sector among eastern European markets this week.

Opportunities

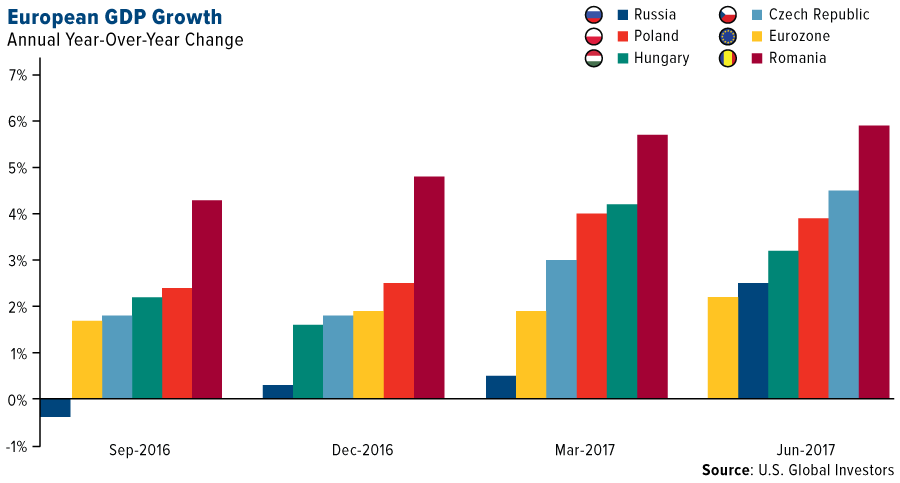

- Central emerging Europe economies continue to grow, outpacing the richer west. Economies in most of the European Union’s eastern wing exceeded expectations as consumer spending and an increase in investments push growth higher. Romania led the pack, with gross domestic product surging to 5.9 percent from a year earlier. While Hungary was slowest at 3.2 percent, but still outpacing the euro area’s annual growth of 2.2 percent.

- According to JPMorgan research, second quarter earnings season has seen 62 percent of companies in the MSCI EMEA (Europe, Africa and Middle East) beat Bloomberg consensus by an average of 16 percent. In Turkey, earnings have been a positive surprise, 11 percent above consensus on earning per share and on top-line. In Poland, overall earnings are broadly in line. In Russia, earnings are 20 percent above consensus. JPMorgan remains bullish on emerging markets equities supported by strong growth in earnings.

- Germany’s general election campaign kicked off over the past weekend and Chancellor Angela Merkel’s center right alliance has a 15-point polling lead over its closest challenger, the center-left Social Democratic Party of Martin Schulz. Merkel already led Germany for the past 12 years and could be re-elected for another four years. Her victory may contribute to further economic strength in Germany and integration of the EU. Elections are scheduled for September 24.

Threats

- According to the research team from Capital Economics, the strong growth in Central and South Eastern Europe will soon come to an end. Growth is likely to pick up in the next quarter, and start to slow down toward the end of the year (and throughout 2018 and 2019 as higher inflation and interest rates will start to weight on domestic demand). Factories are running near maximum capacity with a tight labor market, making it harder for economies to expend further.

- According to a new consensus forecast of Russian and foreign analysts, the Russian economy will have a hard time recovering from the slump it saw during the crisis in the long term. Analysts have raised the growth forecast for 2017 to 1.4 percent from 1.1 percent, but have lowered their growth forecast for after 2018, predicting that the country will not even achieve 2 percent growth rates in the period through 2023. Long-term prospects have worsened, partly due to sanctions.

- Another terrorist attacked took place in Europe this week. A van drove into a crowd at Las Rambles in Barcelona, killing 13 and injuring more than 100. A few hours later police killed five suspected terrorists in the confrontation at the Spanish seaside town of Cambrils, 75 miles south of Barcelona. The Financial Times pointed out that Spain is one of the world’s most visited tourist destinations after France and the U.S. Tourism accounts for about 13 percent of all jobs in Spain and the number of visitors is up 12 percent this year.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| Russell 2000 | 1,357.79 | -16.44 | -1.20% |

| S&P Basic Materials | 336.20 | +1.42 | +0.42% |

| Nasdaq | 6,216.53 | -40.03 | -0.64% |

| Hang Seng Composite Index | 3,695.54 | +31.34 | +0.86% |

| S&P 500 | 2,425.55 | -15.77 | -0.65% |

| Gold Futures | 1,291.10 | -2.90 | -0.22% |

| Korean KOSPI Index | 2,358.37 | +38.66 | +1.67% |

| DJIA | 21,674.51 | -183.81 | -0.84% |

| S&P/TSX Global Gold Index | 196.74 | -2.67 | -1.34% |

| SS&P/TSX Venture Index | 769.76 | +6.95 | +0.91% |

| XAU | 83.90 | -0.19 | -0.23% |

| S&P Energy | 457.09 | -12.46 | -2.65% |

| Oil Futures | 48.65 | -0.17 | -0.35% |

| 10-Yr Treasury Bond | 2.19 | +0.00 | +0.14% |

| Natural Gas Futures | 2.90 | -0.09 | -2.92% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,358.37 | -71.57 | -2.95% |

| Hang Seng Composite Index | 3,695.54 | +26.50 | +0.72% |

| Nasdaq | 6,216.53 | -168.52 | -2.64% |

| XAU | 83.90 | +1.29 | +1.56% |

| S&P/TSX Global Gold Index | 196.74 | +5.70 | +2.98% |

| Gold Futures | 1,291.10 | +42.30 | +3.39% |

| S&P 500 | 2,425.55 | -48.28 | -1.95% |

| S&P Basic Materials | 336.20 | -12.94 | -3.71% |

| DJIA | 21,674.51 | +33.76 | +0.16% |

| Russell 2000 | 1,357.79 | -83.98 | -5.82% |

| SS&P/TSX Venture Index | 769.76 | +3.81 | +0.50% |

| Oil Futures | 48.65 | +1.53 | +3.25% |

| S&P Energy | 457.09 | -28.37 | -5.84% |

| Natural Gas Futures | 2.90 | -0.17 | -5.54% |

| 10-Yr Treasury Bond | 2.19 | -0.08 | -3.39% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,358.37 | +69.89 | +3.05% |

| Hang Seng Composite Index | 3,695.54 | +269.53 | +7.87% |

| Nasdaq | 6,216.53 | +132.82 | +2.18% |

| Natural Gas Futures | 2.90 | -0.36 | -11.06% |

| Gold Futures | 1,291.10 | +27.60 | +2.18% |

| S&P 500 | 2,425.55 | +43.82 | +1.84% |

| S&P Basic Materials | 336.20 | +7.78 | +2.37% |

| S&P/TSX Global Gold Index | 196.74 | -15.28 | -7.21% |

| XAU | 83.90 | -1.26 | -1.48% |

| DJIA | 21,674.51 | +869.67 | +4.18% |

| Russell 2000 | 1,357.79 | -9.54 | -0.70% |

| SS&P/TSX Venture Index | 769.76 | -37.14 | -4.60% |

| S&P Energy | 457.09 | -41.06 | -8.24% |

| Oil Futures | 48.65 | -1.68 | -3.34% |

| 10-Yr Treasury Bond | 2.19 | -0.04 | -1.88% |

Article by Frank Holmes

Save

{kind=link}