In this post, we will explore Afterpay Touch Group (APT.AX) business model, and the topics discussed are the following:

Q2 hedge fund letters, conference, scoops etc

- The Economics of Credit Cards and AfterPay:

- Network Effects and AfterPay’s Leverage over Business Merchants:

- Card Competition: It won’t replace credit cards

- Global Competition

- Is Amazon a threat, ally, or investor?

The economic’s of credit cards.

To understand how Afterpay’s business model is in Clime’s words, ‘flipping the economics of credit cards on their head’, we first need to understand the economics of credit cards.

Credit Cards are a type of short-term loan. To satisfy our need for instant gratification, using a credit card to buy something now that we couldn’t afford until next payday, was one of the main choices we had as a consumer. The cost to us consumers for this instant gratification was the high-interest payments.

The credit card merchants, think Visa & Mastercard, enjoyed fat margins as a result. The business merchant also benefited at the cost to the consumer, as Clime pointed out; ‘Whilst the consumer needs to eventually pay back their loan, the merchant receives the full benefit upfront. What’s more, credit card users typically have larger basket sizes and conversion rates compared with others using alternative payment methods.’

Jay Abraham is an American marketing guru, and one of his most successful sales tactics that he teaches business owners is called Risk Reversal. In all sales transactions, one party is assuming more risk than the other party, and Abraham tells business owners to assume more risk than their clients/customers. For example, offer a 30 risk-free day free trial or try before you buy offer. This only works if the business owner is selling genuine products/services that benefit the consumer.

So how does Afterpay flip credit card economics on its head?

Afterpay offers consumers two months interest-free repayments, and it charges business merchants a 4-6% transaction fee. There are late fees for missed payments on due dates. Clime wrote; ‘This, in turn, leads to consumers again having larger basket sizes and conversion rates than other payment types, even credit cards.’

By transferring the transaction fee from the consumer to the business merchant, Afterpay lowers the risk and cost for the consumer while also earnings fees on all transactions, which I suppose would be any reason why consumers basket sizes have increased.

By transferring the transaction cost from the consumer to the business merchant Afterpay gains leverage over the business merchant.

Purchasing in-store only requires flashing a barcode for the sales assistant to scan, as you can see by my fine photography skills.

However, why should the business merchant accept this extra cost of business?

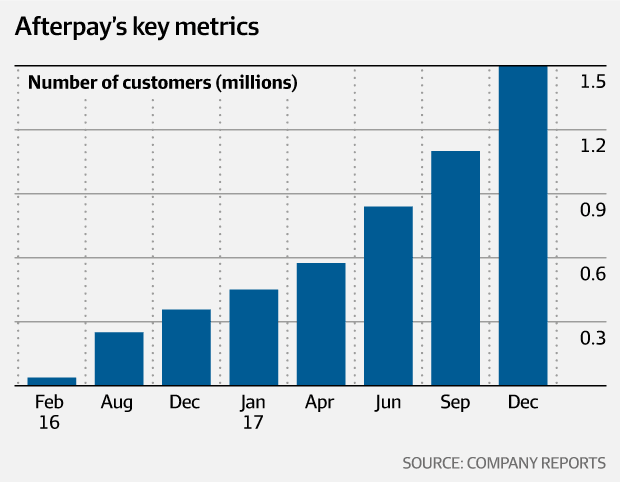

Simply, because Afterpay has amassed over one million users and their collected valuable data on the purchasing behaviour of their users, as Clime wrote:

What initially attracted us to Afterpay in 2016 was the fact that the company established a customer base of 1 million customers and almost 9,000 integrated merchants whilst spending less than $1 million on marketing. This is highly unusual and suggests network effects at play.

Yes, network effects are definitely in play to Afterpay’s advantage.

Free advertising and social proof. Afterpay being advertised on Urbanoutfitters.com

With no need to carry around a credit card, download the free app and flash the barcode, Afterpay reduces their own cost of business. Moreover, to a degree, creates the switching costs for the consumer.

However, I don’t see it replacing credit card in the near future. I don’t see many baby boomers jumping on the bandwagon but’s very popular with millennials.

Clime correctly pointed out the following;

Further, we saw early evidence that Afterpay was building a moat around its business through its substantial retail and consumer dataset, its rapidly growing loyal customer base and its ability to be the largest or second largest (after Google AdWords) referrer of traffic to retailer’s websites. Not even PayPal receives the brand exposure Afterpay receives from its merchants, who advertise its service on every single page, even before their users reach the online checkout.

If the business’ operational trajectory continues, it could find itself in a similar position to PayPal as an instrumental payments provider globally. The question for retailers could eventually evolve from ‘Is Afterpay worth the extra cost per transaction?’ to ‘Can we afford to not offer Afterpay?’

The company is now a major payments player in the Australian market, transacting 25% of all online fashion retail and over 8% of total online retail purchases in the country. 15% of Australian millennials and over 7% of the general population over 18 years old have an Afterpay account.’

Given its runaway success in Australia, the company recently turned its sights to the U.S. To help with execution in the US Afterpay partnered with technology specialist Matrix Partners to try and replicate the viral growth they saw here…

Users! Users! Users!

Network effects compound in the market leaders favour, the company with the largest market share of users, so Afterpay needs to adopt Facebook’s adage ‘move fast and break stuff’ in adding users. Moreover, this is especially true now that Afterpay has entered the U.S. market.

As clime wrote;

Since launching in the U.S. just over two weeks ago, the company has grown from 50 pre-announced retailers to over 250… Afterpay’s first customer was Urban Outfitters, the 14th largest fashion retailer in the country. Also supporting our view on its viral uptake in the States are its strong growth in social media mentions (particularly Twitter) and Google search volumes. Whilst it is hard to quantify the exact number of customers that will be added as a result of this, it is interesting to note that its search volumes are roughly 8 times larger than Sezzle, a copycat competitor that started a couple of years earlier with mostly smaller online retailers.

Search trends of Afterpay and Sezzle (U.S. competitor) in the United States

The U.S. population is 13 times larger than Australia’s, online fashion sales 14 times larger and in-store sales opportunities are 15 times larger, according to Clime.

Caution needs to be exercised before high jumping to conclusions, in regards to forecasting revenues. Yes, the potential is there, but as millennials are Afterpay’s largest gen user, I want to see more in-depth stats on their purchasing behaviours before I even try to estimate the potential sales revenues for Afterpay.

I believe this is where investors get carried away in valuing growth. Michael Mauboussin when he was at Credit Suisse produced a helpful handbook, with Dan Callahen and Darius Majd, called the Base Rate Book. It boils down to essentially this when forecasting a company’s future results, be it revenue growth, gross margins or cash flow compares to the base rate of all corporate results. This will improve your forecast accuracy and help you avoid a number of personal bias. I’ll go more in-depth when we discuss Afterpay’s valuation in the next post.

Clime assessed the following three risks;

Risks are ever present in the business world, and the main three we see for Afterpay are competition from an already established player (e.g. PayPal), a serious economic downturn or regulatory action regarding its onboarding process. We are keeping our eyes open for any potential signs that these issues could affect the business, but so far Afterpay’s trajectory appears to continue unaffected.

Is Amazon a threat, or an ally, or will they buy Afterpay?

After I registered with Afterpay, I checkout out how to use Afterpay for online shopping. From the screenshot above of Urban Outfitters, Afterpay is integrated into the business merchant’s online store. However, I can’t use Afterpay on Amazon.

That would be a great catch if they can convince Amazon to add their service. So I see a bit of a rivalry, but also as an ally. It would benefit them both, and this leads me to a possible outcome that Amazon may offer to buy Afterpay outright.

Let me know your thoughts in the comments section below.

Yours in Investing

Disclaimer: Clime Asset Management are shareholders, and I’m not.

Article by Searching For Value