Tons of good info in here. Below is the full document in scribd. Big H/T to Street of Walls

Quick Street of Walls Takeaways:

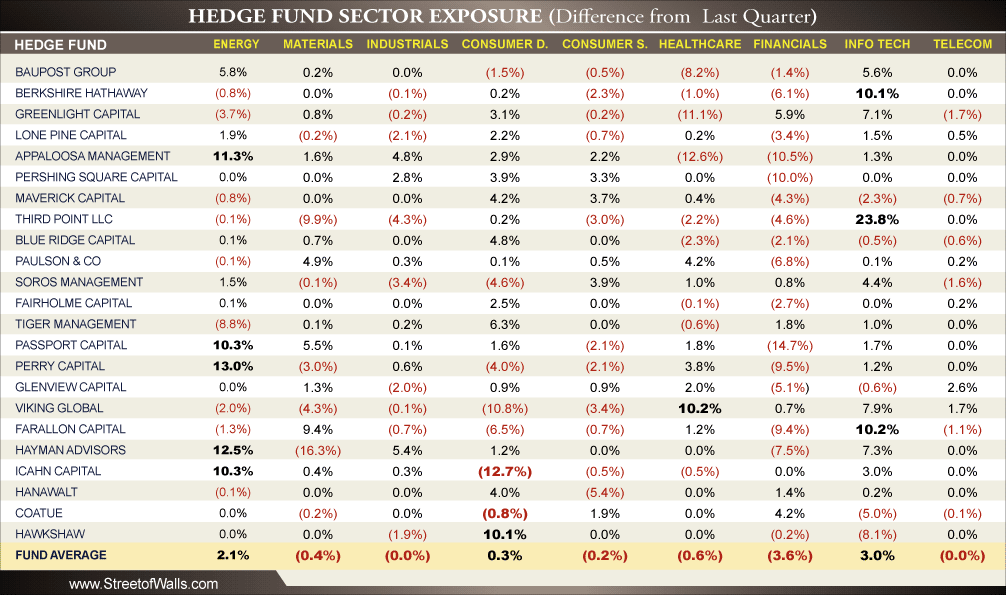

- As we saw last quarter Hedge Funds piled into Technology again as valuations exploded in the wake of high profile IPOs such as Pandora, Groupon, and LinkedIn. Berkshire made a very surprising entry into the technology sector buying new positions in IBM (57mn shares) and Intel (9mn shares). Other technology participants in the quarter included Third Point doubling their stake in Sandisk and Farallon Capital buying new positions in VSEA, NETL, and adding to MSFT.

- Energy was another sector that saw a lot of out performance and M&A activity during the quarter. On average our hedge fund universe increased allocation to this sector by 2.1% during 3Q. Funds most active in energy during the quarter included Appaloosa, Passport, Perry, Hayman, and Icahn.

- Hedge fund continued to poor out of Financials during the quarter, funds on average allocated 3.6% less to financials in 3Q. Financial stocks have massively underperformed the market due to pressure on Net Interest Margins due to low interest rates, large overhang on mortgage put-backs, capital issues regarding new Basel III rules, and continued litigation. We saw double digit declines in allocation from Appaloosa, Pershing Square, and Passport Capital. It is interesting to note that only 6 funds out of 23 we tracking increased allocation to Financials.

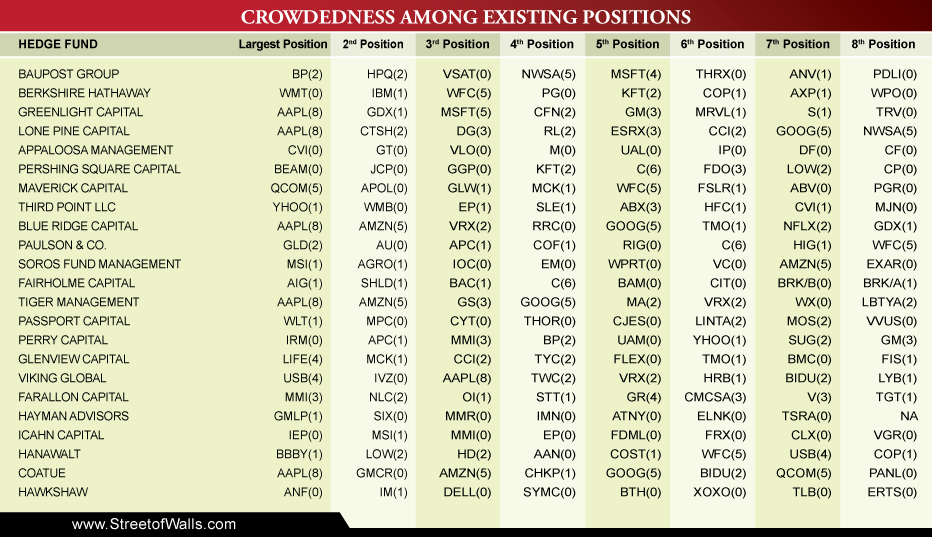

- We found a majority of hedge funds largest positions were shared amongst the hedge funds in our universe. AAPL was by far the most crowded position in the top 8 holdings for hedge funds: Greenlight, Lone Pine, Blue Ridge, and Tiger all have AAPL as the largest position in their holdings. Other large crowded positions include AMZN, GOOG, NWSA, MSFT, and WFC.

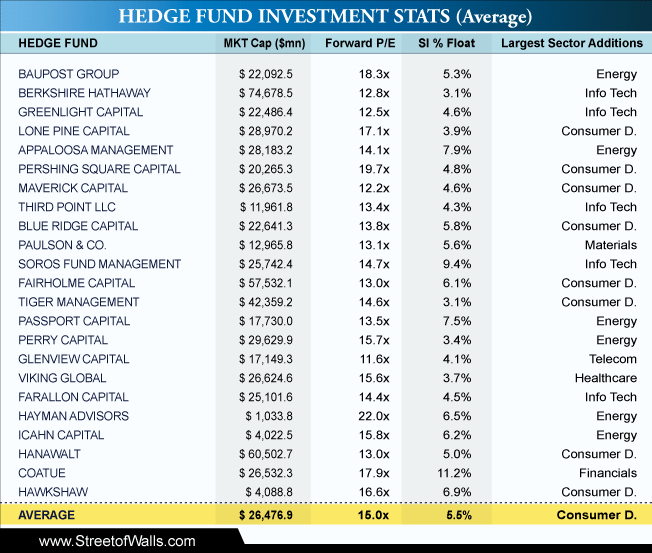

- On average the funds listed below bought companies with a 2011 forward price to earnings ratio of 15.0x. Hayman and Pershing bought into the higher valuation stocks at 22.0x and 19.7x respectively while Maverick and Glenview bought into much lower valuations at 12.2x and 11.6x respectively. Short interest as a percentage of publicly traded floating shares was an average of 5.5% across the 23 funds. Coatue and Soros had the highest short interest with 11.2% and 9.4% while Berkshire and Tiger had the lowest with 3.1% and 3.1%. Owning stocks with high short interest is a sign of contrarian investing.

Introduction on 13F Filings: Registered hedge funds over $100 million are required by the Securities and Exchange Commission (SEC) to file quarterly updates on portfolio holdings. These holdings are filed online through form 13-F at sec.gov. Hedge funds are required to file these holdings no later than 45 days after the end of the calendar quarter. The Street of Walls team compiled very detailed analyses on 20 of the top Hedge Funds in the industry. This report focuses on hedge fund positions at the start of 3Q 2011 and looks at meaningful changes from the previous quarter. The report is based on 20 of the top hedge funds.

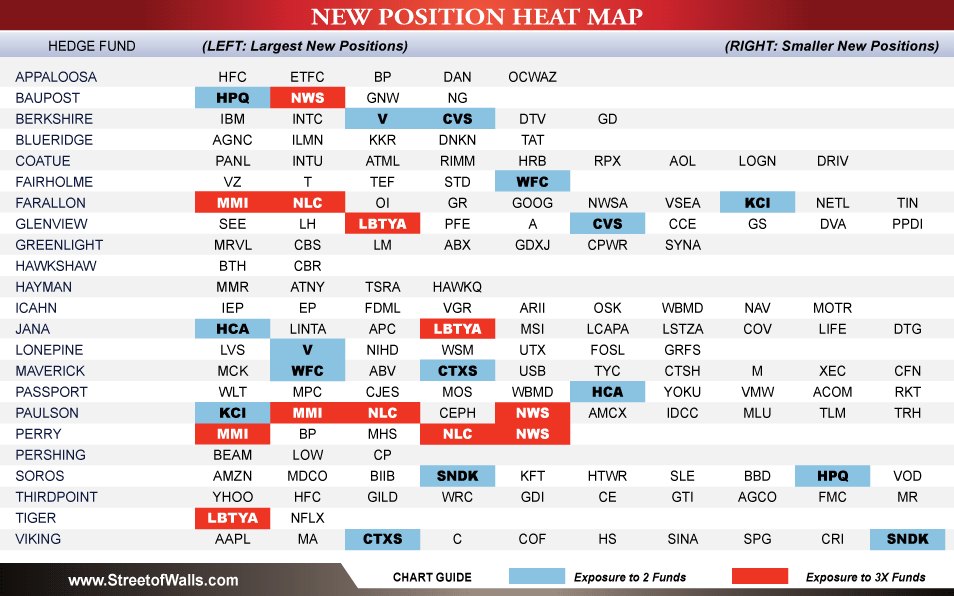

NEW Position Heat Map:

During 3Q11, the top 23 hedge funds entered many new positions. The Heat Map below identifies the top NEW positions added during the quarter. NEW names were not previously held in 2Q11. Tickers in Red represent common or “crowded” positions. The most crowded new ideas during the quarter were MMI, NLC, LBTYA, and NWS. Other new positions shared among hedge funds but with less overlap were HPQ, V, CVS, WFC, KCI, HCA, SNDK, and CTXS. Full Report:3Q HF Intelligence

Crowdedness Among Existing Positions:

Below we break-down the most shared stocks held in at the top 23 hedge funds. Crowded trades can lead to higher than normal share price volatility. We examined the number of positions that were shared among our hedge fund universe, giving us an understanding of how the herd is acting. For the top 23 hedge funds we cover, the most crowded books were from Viking, Maverick, Farallon, Lone Pine, Perry, and Glenview (lots of Tiger Cubs in there). The least crowded positions among the books were held at Icahn, Hayman, Coatue, Greenlight, and Hawkshaw. Full Report: 3Q HF Intelligence

Hedge Fund Sector Changes:

The percentages below show quarterly changes in sector weighting allocations (as defined by S&P GICS) for each hedge fund we cover. For example, as defined by publicly available data Baupost increased portfolio allocation ($ amount) into Energy by 5.8% from 2Q11 to 3Q11.

There was a big push within the quarter to Information Technology (+3.0%), Energy (+2.1%), and Consumer Discretionary (+0.3%) while Healthcare (-0.6%) and Financials (-3.6%) declined the most.

Fund managers may have found opportunity within the technology sector as valuations soared higher, while government reimbursement risks associated with the Healthcare sector and low rates and mortgage related put-back problems in Financials may have led managers to trim and exit positions within that space.Full Report: 3Q HF Intelligence

Hedge Fund Investment Characteristics:

Out of the 23 hedge funds examined, Consumer Discretionary was the leading sector for investment in 3Q11 (as a % of sector investments from last quarter) followed by Energy then Technology.

The average market capitalization of hedge fund portfolio companies was $26.5 billion. Berkshire and Hanawalt had the highest average market cap exposure while Icahn and Hayman Advisors had the lowest average market cap exposure.

On average the funds listed below bought companies with a 2011 forward price to earnings ratio of 15.0x. Hayman and Pershing bought into the higher valuation stocks at 22.0x and 19.7x respectively while Maverick and Glenview bought into much lower valuations at 12.2x and 11.6x respectively.

Short interest as a percentage of publicly traded floating shares was an average of 5.5% across the 23 funds. Coatue and Soros had the highest short interest with 11.2% and 9.4% while Berkshire and Tiger had the lowest with 3.1% and 3.1%. Owning stocks with high short interest is a sign of contrarian investing. Full Report: 3Q HF Intelligence

Hedge Funds 13F Filing 3Q11//

{kind=link}

{kind=link}

{kind=link}

{kind=link}