Excerpted from Quality Shareholders by Copyright (c) 2020 Lawrence A. Cunningham. Used by arrangement with the Publisher. All rights reserved.

Q3 2020 hedge fund letters, conferences and more

“The goal is not to have the longest train, but to arrive at the station first using the least fuel.” This aphorism by Tom Murphy, former chairman and CEO of Capital Cities/ABC and longtime director of Berkshire Hathaway, describes the goal of successful capital allocation.

Murphy, widely considered a master of capital allocation, cautions against buying up as many companies as possible or otherwise growing for the sake of growth alone, but to get the most bang from every buck in acquisitions and other investments.

In The Outsiders, Will Thorndike, a student of master capital allocators, encapsulated Murphy’s approach: focus on industries with attractive economic characteristics, selectively use leverage to buy occasional large properties, improve operations, pay down debt, repeat.

To drive the fastest and most efficient train, CEOs should understand capital allocation. QSs are attracted to those who do.1 Capital allocation is a technical term that simply denotes how corporate dollars are invested. Capital can be allocated to many different ends concurrently: fortifying the balance sheet by repaying debt or building cash reserves, funding initiatives to maintain or grow existing businesses, making acquisitions, buying back shares, or paying dividends. QSs value strong track records in capital allocation, measured by return on invested capital, and companies whose managers explain their views.

Capital allocation is, however, a practice or habit of mind learned through training and experience in investing. Although not all corporate leaders have investing backgrounds, as many rise through research, engineering, production, or sales ranks, the skill is vital and can be learned. In his 2017 letter to shareholders of Cimpress, Robert Keane stressed the link between capital allocation and success as a CEO:

I wish that I had figured out the importance of capital allocation many years ago, but the reality is that Cimpress is just now entering our fourth year of making capital allocation an explicit focus area of our management routines so we are still learning and revising our internal processes. But better late than never: as CEO, founder and a significant shareholder, I now spend a major amount of my time on activities related to capital allocation and consider it a critical responsibility.

Phil Ordway, a quintessential QS, advocates making capital allocation an explicit corporate priority.2 In papers and speeches, he highlights a dozen exemplary companies. These include Amazon, AutoNation, Cimpress, Credit Acceptance, Henry Schein, Morningstar, Netflix, Phillips 66, Post Holdings, Texas Instruments, and Wabco Holdings.

Framework and Measures

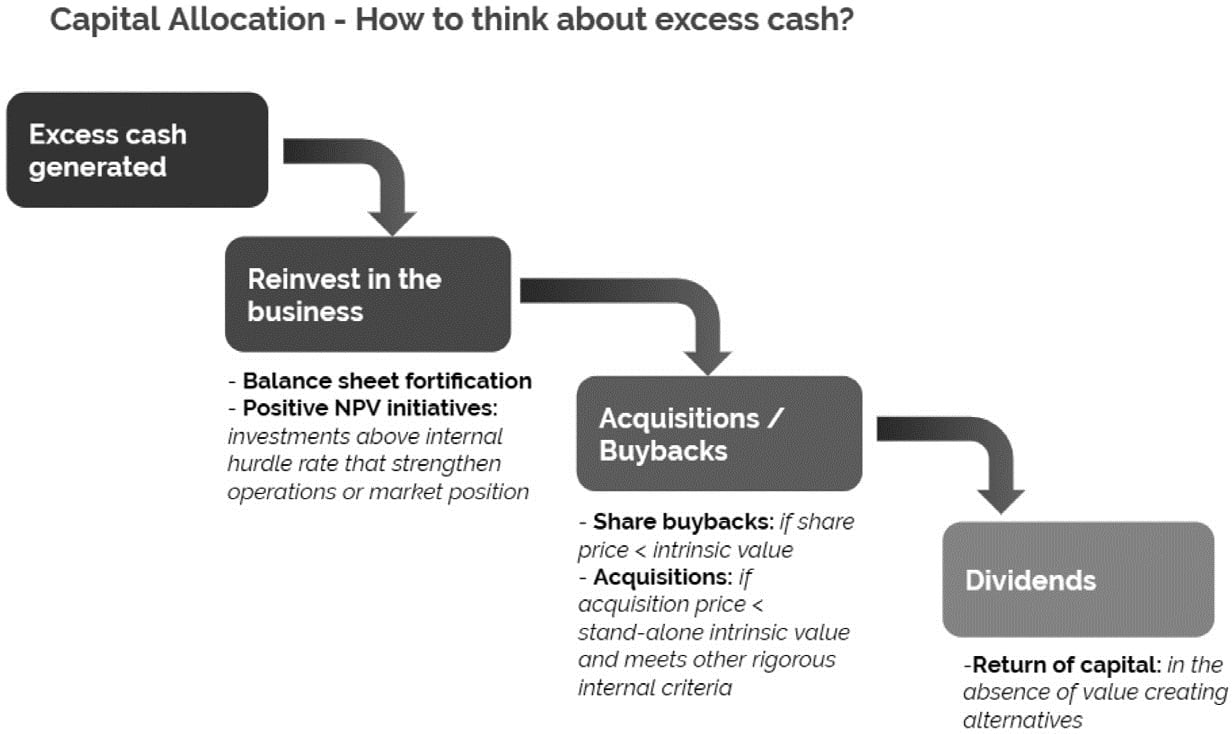

Figure 9.1 presents a framework for thinking about capital allocation and organizing discussion. It is not a directive or road map, as optimal priorities among the depicted choices will differ among companies and managers at different times. In fact, the various uses of excess cash are neither mutually exclusive nor sequential— funds can be optimally allocated to all uses and priorities given to those anywhere on the chart.

FIGURE 9.1 Capital allocation framework

Source: Author’s own data.

It’s best to start with a general approach to measuring capital allocation effectiveness.3 First, for any given year, calculate the corporation’s average invested capital available. Begin with an estimate of the amount of money shareholders have invested. Then, each year, update by adding net income and the proceeds of any share issuances, subtracting any dividends, and adjusting for any compensation paid in shares.

Thereafter, measure overall performance as a return on the average invested capital. For example, take net income as a percentage of invested capital as an ultimate measure of capital allocation effectiveness.

To maximize return on invested capital (ROIC) on an ongoing basis, measure every corporate project accordingly. Track every allocation, including reinvestments and acquisitions, on a projectby-project basis using conventional after-tax internal rates of return (IRRs—the rate where the net present value of project cash flows are zero). Be sure all company personnel are trained to be familiar with this tool. For oversight, have the board periodically set the required hurdle rate for all project types (the minimum required IRR to green-light the proposed capital allocation).

As rigorous as this sounds, beware that IRRs are complex and future oriented and require judgment. Managers charged with related measurement may naturally tend to overestimate. To compensate for this, compute an additional measure of overall annual capital allocation effectiveness. Consider one that is simpler, historical, and less judgment laden: add annual ROIC to annual growth in organic revenue (not acquired) and compare the sum to the hurdle rate.

The tools can be adapted to all of the capital allocation opportunities presented in figure 9.1. Such an approach is an excellent way to attract QSs.

Management at Texas Instruments has done so. It sees capital allocation as a top priority. The company has long been a conscious and successful cultivator of QSs. In fact, among its original investors, in a private placement, was Phil Fisher. That quintessential QS never sold the stock, adding to his position over the years to make it one of his largest.

Today, while Texas Instruments faces the usual ownership by the major indexers (together owning some 20 percent), an impressive QS cohort accompanies them: Prime Capital Management, Massachusetts Financial Services, T. Rowe Price, Capital Research Global Investors, Capital World Investors, Henderson Group, Capital International Investors, Franklin, AllianceBernstein, State Farm, Bessemer Group, and Davis Selected Advisers. A concise statement of capital allocation is easily accessible on the investor’s section of the Texas Instruments website, excerpted below. Such transparency and accountability are compelling to QSs.

Texas Instruments: Capital Allocation Principles

Our capital management strategy reflects our belief that free cash flow growth, especially on a per-share basis, is most important to maximizing value over the long term, and that free cash flow will be valued only if it is productively reinvested in the business or returned to owners. Our business model and competitive advantages have enabled our company consistently to generate solid free cash flow margins. Our free cash flow per share has been steady and growing over the past 10 years despite, at times, difficult macroeconomic or market environments.

Our strong balance sheet enables us to fully fund pensions and have access to low-cost debt. With interest rates still low, we plan to continue to hold debt as long as it makes economic sense. Even then, we use debt judiciously such that we avoid concentrated maturities while we maintain our strategic flexibility. Combined, these elements allow us to invest for our future and still have excess cash available to return to owners. Over a 10-year period, 2009– 2018, we allocated $77 billion across these areas:

- $32 billion on R&D, sales and marketing, capital expenditures, and cash used for inventory to support the organic growth of our businesses. Our R&D expenditures are disciplined and focused on markets we believe have the greatest growth potential. . . .

- $25 billion on consistent share repurchases, intended to generate the accretive capture of free cash flow for long-term invesWe focus on consistent repurchases when the stock price is below the intrinsic value, using reasonable growth assumptions.

- $13 billion on dividends, designed to appeal to our broader set of investors, with a focus on sustainability and dividend

- $7 billion on acquisitions to fund inorganic ……… We look at an acquisition opportunity through two lenses. First, it must be a strategic match, which for us translates into an entity that is analogand catalog-focused with a high exposure to industrial and automotive. Second, it must meet certain financial performance levels such that it generates a return on invested capital greater than our weighted average cost of capital, as one example, in about four years. . . .

Our goal is to return all of our free cash flow to owners in the form of dividends and stock repurchases. We have a robust model to allocate returns between dividend growth and stock repurchases.

Let’s turn to some particulars.

Reinvestment

While there is fluidity to capital allocation, the first priority ought to belong to reinvestment in current businesses to increase competitive advantage. The chief concerns for corporate leadership and QSs are managerial rationalizations about the prospects of such a use of capital. Managers are often optimistic, usually a desirable trait in an entrepreneur, but not in excess. Standard measurements, such as IRR and hurdle rates, along with related oversight, help keep them in check.

Another aspect of reinvestment is fortifying the balance sheet. Companies need sufficient liquidity to be prepared for economic distress as well as to take advantage of fruitful opportunities. As the Tisch family executives at Loews Corporation point out, it’s easier to raise money when you can than when you need to.4 Striking the happy medium is key, however, as hoarding too much cash on the balance sheet could be embarrassing to directors and officers alike.

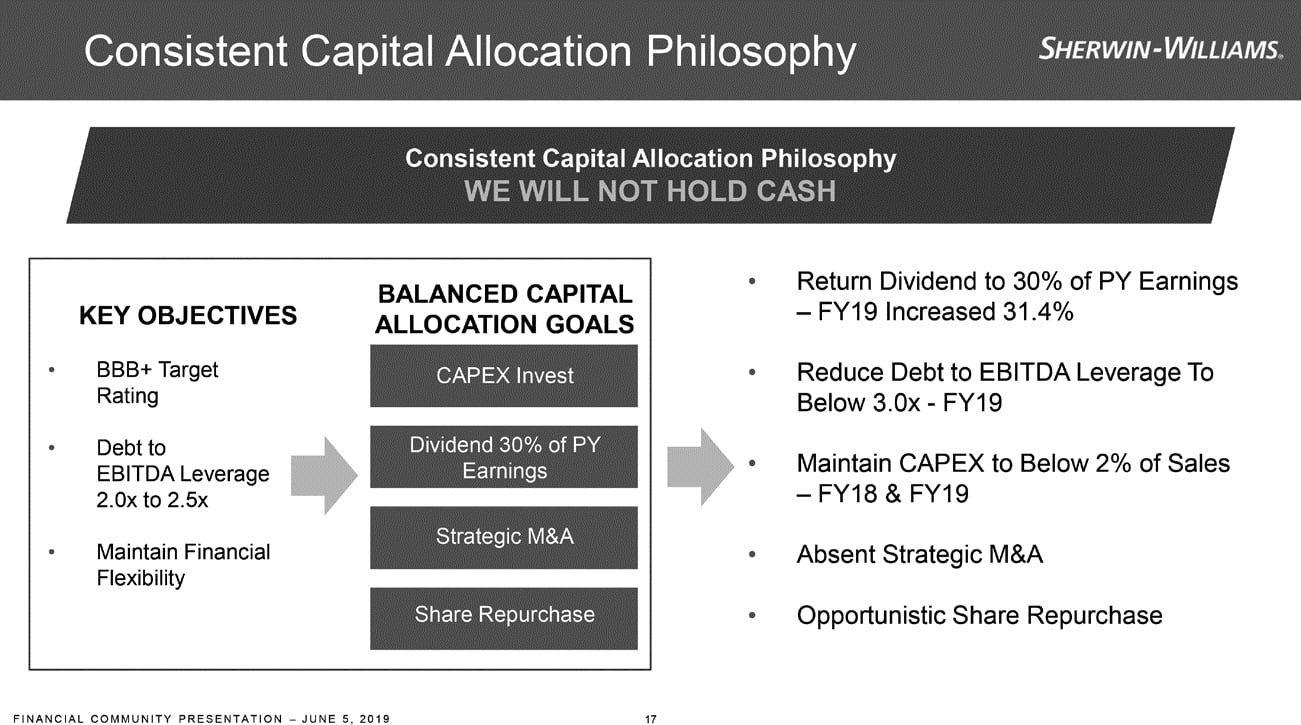

Leadership at Sherwin-Williams adopts and explains a clear and consistent capital allocation philosophy. It takes a somewhat extreme position in its aversion to holding cash, preferring other uses or distributions to shareholders (figure 9.2, a slide from a 2019 Sherwin-Williams’ CEO presentation, emphasizes this point). Not all companies will find this approach congenial, as many prefer to strengthen the balance sheet or preserve capital for opportunities down the road.

FIGURE 9.2 Consistent capital allocation philosophy

Source: Sherwin-Williams, “Financial Overview,” Financial Community Presentation, June 5, 2019, https://investors.sherwin-williams.com/doc/fcp_financial_overview_2019.

The takeaway: it works for Sherwin-Williams; the company has explained its framework and how that framework suits its business, culture, and goals. And there is a track record, including an enviable roster of QSs at the top of the shareholder list: Capital World Investors, Massachusetts Financial Services, FMR, Fiera Capital, Henderson Group, AllianceBernstein, T. Rowe Price, Meritage Group, Findlay Park, Capital Research Global Investors, Farallon Capital Management, and Chilton Investment Company.

Acquisitions

Next up are acquisitions of new businesses. The capital allocation test is simple: whether the acquisition makes current shareholders wealthier on a per-share basis. That means paying a price less than the target company’s stand-alone value, ideally delivering an expected return (IRR) that exceeds a preset hurdle rate.

Despite the simple test, acquisitions are a common source of capital destruction. What’s essential in this step is skepticism of optimistic scenarios, such as forecasts of value arising from synergies or other opportunities expected to materialize postacquisition.

Improving an acquired company’s operations postacquisition is a source of value creation. But managers do not always provide investors with sufficient information to evaluate proposed acquisitions completely or objectively. They provide projections that look compelling and business rationales that seem logical.

Yet acquisitions can be emotional, exciting managers and stoking optimism. Managers cultivate QSs by playing down expectations from acquisitions, skipping talk of synergies and other often-elusive veins of value. An even better approach: conducting ongoing, constantly updated postacquisition analysis to compare expected IRR with actual ROIC and determining reasons for the difference.

Another source of discipline is using cash in preference to stock to pay for acquisitions. Using stock can inflate the price, often felt as play money, more like poker chips than cash.

Henry Schein, a dental and health-care products and distribution business, has had some fantastic results in using a value-based approach in capital allocation, including when evaluating acquisitions. It has made more than two hundred acquisitions in recent decades and invested heavily in organic growth, new product lines, and new geographies. A baker’s dozen from 2015 to 2019 were presented as “key,” noted in figure 9.3.

FIGURE 9.3 Dental market—key acquisitions

Source: Henry Schein, “Q3 2019” investors’ presentation, https://www.henryschein.com/us-en/images/Corporate/IRPresentation.pdf.

At least one capital allocation decision can directly improve the quality of the shareholder base: share buybacks. When companies buy their own shares, the most likely cohort interested in meeting the demand are transients, who by definition are prepared to sell at all times. That automatically increases the proportion of shares held by longer-term shareholders, such as QSs.

But share buybacks are only rational for shareholders if the company pays a price less than a conservative estimate of the company’s per-share intrinsic value. If so, that is prudent capital allocation; if not, it is capital squandering.

Buybacks were uncommon through the 1970s and 1980s, as dividends were the popular route for corporate distributions to shareholders.5 Pioneers stood out, including Roberto Goizueta at Coca-Cola, Larry Tisch at Loews Corporation, Henry Singleton at Teledyne, and Kay Graham at the Washington Post Co. In that era, these companies followed the textbook, repurchasing shares as a capital allocation exercise, when no better alternatives existed and price was below value.6

By the late 1990s, buybacks had become a common practice across corporate America. Such proliferation raised a new concern: whether managers possessing superior valuation information exploit selling shareholders when buying at a discount. To address this, managers must provide shareholders with all relevant valuation information. Otherwise, insiders take advantage of uninformed shareholders, confiscating their interests at pennies on the dollar—anathema to QSs.

The advice Warren Buffett gives to investors applies equally to managers making capital allocation decisions: be fearful when others are greedy, and greedy when others are fearful. The most obvious application of this investment principle in the context of capital allocation concerns share buybacks. Companies make errors of both commission—buying no matter how high the price—and omission—failing to buy when prices plummet.

Two exemplary exceptions to the latter problem win honors in this area. One is Sherwin-Williams, the paint manufacturer, whose policy of holding no cash and buying shares back cheaply paid off during the financial crisis of 2008–2009. Financial markets swooned, despair was in the air, and many companies put the brakes on their share buybacks. Not Sherwin-Williams, whose persistent buying through the crisis generated considerable shareholder value for continuing owners—a practice QSs applaud and one that is almost certainly attributable to having in place a clear and consistent capital allocation policy.7

Another honorable mention for opportunistic share buybacks in adherence with a capital allocation framework goes to Wabco, an international trucking technology company. In late 2011, the Euro crisis loomed, casting a pall over much of the continent, especially in Greece. Talk of a double-dip recession punished equity prices across the market, falling particularly heavily on Wabco. The company went bullish, increasing repurchases substantially. When reporting on the enhanced program, the company also stressed confidence, assuaged fears, and clarified some misconceptions.

Buybacks automatically increase earnings per share (EPS) and tend to boost stock prices. QSs are alert to these effects and oppose managers whose buybacks are motivated by such results rather than by rational capital allocation. They are therefore skeptical of buyback formulas or quotas. Moreover, since buybacks automatically boost EPS, if that metric is an important part of managerial performance reviews or compensation, boards must be especially vigilant to deter share buybacks designed to boost executive pay.

Finally, when choosing between paying a cash dividend or buying back shares, the effects on shareholders and option holders differ greatly. Dividends increase returns to shareholders but decrease the value of options, while buybacks boost earnings per share and therefore increase option value. A conflict of interest looms between what is best for managers holding options and all other shareholders. That’s why QSs are skeptical of companies with significant executive stock option compensation coupled with significant share buybacks. In many such cases, a better capital allocation for shareholders would be dividends.

Dividends

Dividends are another capital allocation decision that can directly shape the shareholder base. Regular dividends give shareholders a reason to stick around during troubled patches—they can be a useful magnet that lengthens holding periods and sometimes induces taking larger positions. This point was stressed by one of the more frenetic and diversified stock pickers, Peter Lynch, who gained fame as both a stock picker and author.8

Excerpted from Quality Shareholders by Copyright (c) 2020 Lawrence A. Cunningham. Used by arrangement with the Publisher. All rights reserved.