Nike Inc (NYSE:NKE) stock analysis shows how Nike is definitely a great business – we share 6 key fundamental factors that show how Nike stock represents a great business, from a dividend growth stock to improving margins across low capital necessities.

Q1 2020 hedge fund letters, conferences and more

However, Nike’s stock price is really expensive from a fundamental perspective given the PE ratio of 36, likely going higher after next earnings, and due to the growth rate that is not as high as it was in the past.

Over the last years, NIKE’s revenue growth was around 6%, much below the usual 9% over the past 15 years. Therefore I would dare to say Nike is not a good stock to buy now. But, given the free money environment, you will decide for yourself whether Nike is a stock to buy or sell based on the fundamentals analyzed.

Nike Stock Analysis – Flying High Likely To Fall

Transcript

Good day fellow investors. Welcome to another stock analysis with Sven Carlin. In this video we’re going to analyse Nike. Give an example why it definitely is a great business. But we’ll also do an investing analysis because the great can fall also. So it’s not just great businesses also buying at a fair price. Nevertheless, this is a picture of Nike Town, Nike’s Central London store. Now that the current situation has improved a little bit in the UK. This is the line for the store. It’s insane. But it shows how Nike has an extremely strong brand which leads into a strong business, which leads to great fundamentals that we are going to discuss here.

The three key takeaways from this video analysis will be of course, the excellent businesses, an example we’re going to go through six key factors to look when you’re looking for excellent great businesses to own, also, we’ll discuss how and when a great business can fall. It’s not just about the metrics, and then I’ll discuss also my investment thesis on Nike, based on the fundamentals will analyse despite the fact that it is a great business, how there is a 94% chance of underperforming returns from the current levels.

So it all started when this guy signed for Nike, as you can see here he wished to sign for for Adidas, but Adidas wasn’t in a good place. So he signed for Nike. They expected to sell a few hundred thousand of his shoes. They sold in the first year about 3.5 million and the rest is history. Also, if we look at what happened since when MJ signed, the price was what 15 cents adjusted for splits, so this is almost a 500 bagger even more you can’t even count to this.

This is insane what was the stock price, but the stock took flight, but not that fast here 1990s with the globalisation probably of the MBA of the first jump in growth of the middle class, more consumption, better marketing, etc, globalisation, internet, and then the actual boom came in the last decade. So if you wanted a 10 bagger, you had 20 years to buy Nike, and then you could have enjoyed the 10 bagger. So this is a great business.

Now the question is whether investors can expect great returns from this level. This is really an epic performance. You only need one company like this in your portfolio. But the fundamentals are now a little bit different price earnings ratio of 36, probably lower after the earnings that are coming in soon and the dividend yield is just 0.99%. So this is an Excel file that we make for most companies that we analyse here are the models and everything data, I’ll show you the data, also outsource from this one from book value from various models, DuPont lease analysis, I will not bother you with all the details, I’ll just extract six factors that explain this company in the best way.

Don’t ask me for these models because I once spoken with an analyst with 40 years of experience and he said, Sven, never never ever share your models because there’s too much value, people don’t understand it and you’ll just get into trouble explaining all the questions about the numbers because it takes years years of the experience to know what and when to look at. So I’ll extract from this six factors that will give you a great indication about the company.

The six factors we’re going to discuss our book value, dividend growth, altman score, which is a nice factor to look at, improving profit margins, return on capital employed, and owners earnings. And we’ll put this great business that Nike definitely is into an investing perspective after we look at this factors.

So book value per share. Now you would say book value per share is extremely low compared to the stock price stock price of $100 compared to 5.6 dollars in book value, but this is also an example of what a great business is because they don’t need much capital to do their business which is a great business, as Warren Buffett always says, a business that can reward shareholders is a great business and a business that eats a lot of capital is not such a great business.

This decline in book value is because of the share buybacks as the stock price increases. The buybacks are detrimental to book value, but the focus is on the earnings and cash flows and growth not so much on book value in this investment scenario.

Of course, the next step for Nike Stockis dividend growth, which often vary usually over the long term equals stock growth, the dividend was 9 cents in 2004. Now it is 93 cents so it is a 10 bagger. If we look at the stock in 2004, it was around $9. Now, it is around $99. So the dividend increased 10 times the stock did the same. So this is dividend growth investing also if the dividends keep on increasing, it’s very likely the stock will keep on increasing. And that’s also the key investment thesis with Nike. So great dividend increases here, which again are a factor showing that this is a great business that can increase dividends and reward shareholders.

Altman Z score, how likely it is that the company goes bankrupt. This is over the last 15 years. If it’s below 1.81, then the company might be in distress, above 3 is regarded as safe. Nike has almost also 10-11 which is insane. So it’s really, really safe company. And in this environment, investors love safe companies.

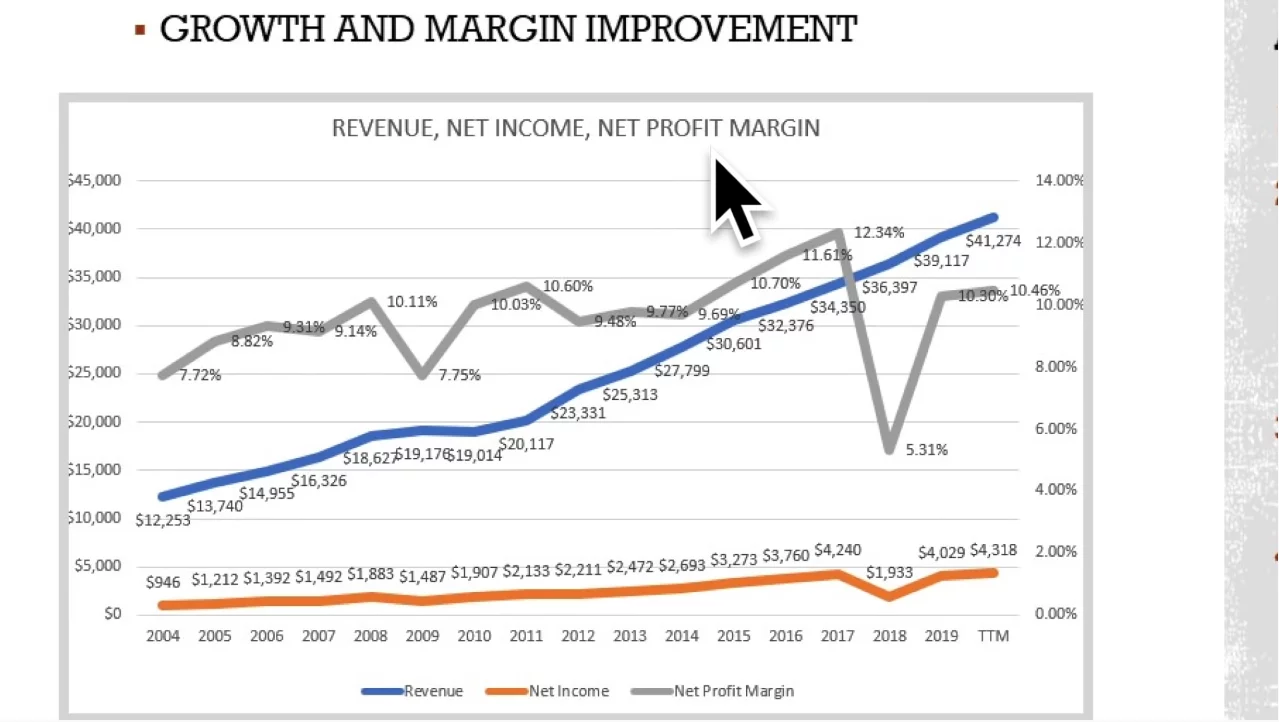

Now, let’s look at the growth in revenue, net income and net profit margins. Given that Nike is a great business they managed to triple revenues are a little bit more than that over the last 15 years from 12 billion to 40 something billion, they managed to also quadruple a little bit more net income from 946 million to 4.3 billion.

Also lower the number of shares outstanding, which increases earnings per share, but they also managed to increase the net profit margin from an average of seven 8%. Bring it higher, this was one off events bring higher to 10-11%. And if a company can increase margins while growing, while increasing profitability, then it is definitely a great business, a well managed business.

So improvements in profit margins there are plenty of growth stocks that simply cannot improve or even reach positive profit for the net profit margins and are still growing but this is a great business that can grow and connect to increase the profit margins, increase the profits and distribute more to shareholders.

Further, Charlie Munger says that the return on investing usually is correlated to the return on capital employed. This is a little bit higher than the actual return on investing which was around 15%. But if we adjust for the leases, which is also capital employed, but not until a few years ago, included in the balance sheet, then we can take off 5 percentage points from here and then we come to the 15-20% return on investment that investors have been enjoying over the last decades.

So return on capital employed, what is their return on the capital that the company is using? Nike is and lean, mean, return on capital employed machine. So again, an indication of a great business.

Then again, owners earnings, the growth in owners earnings reflects the share price over the long term owners earnings have grown 15% per year. So if they continue to grow like that, then they will likely be at $10 per share in 2030, given the current price of $100.

And if they keep growing at 15% per year, it’s unlikely that it will be at 100 it will likely be at 300-350. Given the same valuations, but if we look here at the owners earnings per share the blue line and the share price over time, look at the trend lines, the linear trends that I have extrapolated here, those are perfectly correlated.

So the share price has been growing at the same rate as owners earnings. And that’s also for the future if they keep growing earnings at the same rate, the share price will likely continue to grow at 15% per year with ups and downs. And this also summarises the thesis.

Warren Buffett always keeps saying, your investment returns depend on how the owners earnings of the business develop over the long term. So that is his investment thesis. Charlie Munger always says invest in great businesses and you have nothing to fear. But he also adds at a fair price.

And this is something we have to see whether Nike is fairly priced or not. As we said, it all depends on whether the owners earnings are going to continue to grow like this. If not, you’re paying a price earnings ratio of 40 if the growth isn’t there, so it’s all about the growth of Nike in the future and if I go to the investor relations page. What are they saying first, Nike is a growth company.

This is the first thing that boom hits you on the head when you not see Serena here. But oh, she’s also hit by the growth company there. Sorry, Serena. So that’s what they are promoting themselves. And that’s also what happens if we look at this chart.

However, the growth over the last five years has been slowing down. And they’re doing whatever they can from various financial engineering, things to show love, like they are still growing at the same rate they have been growing. In the past, of course, given globalisation, China, a lot of people entering the middle class and buying Nike they managed to grow extremely fast in the past, but over the past five years, this growth has been slower and just 6.5 percent over a year. That’s not 15%. And they are trying to improve the earnings and everything with financial engineering. And that’s also an indication of how the mighty can sometimes fall and this is what investors have to keep in mind when investing in Nike.

The main question is, well, is this a fair price? Can they keep growing faster? Look at the shares outstanding, they have lowered it by approximately the number of shares outstanding through buybacks by approximately 25% over the last 10 years. But as the share price increases, the return is much much lower when you compare when the price was $50 per share a few years ago and now at $100 per share.

The buybacks the share is twice as expensive, which means that the return on buybacks and capital allocation is much much smaller and to finance the growth they have been used to the financial engineer it will cost much, much more. And at some point in time, it will not be possible if revenue is not growing at 15%. And we have seen the revenue is growing just at 6.5%. So, this is what worries me from a fundamental perspective. It’s still a great business, but to be fairly priced. I would like to see higher revenue growth rate on the same fundamentals we have already discussed.

Plus as they are doing financial engineering to lower to increase the buybacks. The liabilities compared to the total assets went from 32% in 2010 to 65%. So they are taking on debt to improve the financial numbers through buybacks. Also, they made an accounting change change. So they changed revenue recognition policy in 2018. Now they recognise revenue on shipment, not on delivery. This is extremely important, because what is going on? How is the e-commerce world developing, you buy something you try it on, and then you return it.

Now they recognise on shipment, and they underestimated the number of returns by about 200 million last year, I think. So if I look at the 200 million misestimation, I compare it to the net income. So, look at the growth, the estimation goes the growth goes from 4 billion to 4.3 billion, so that’s 200 million.

That’s the misestimation, in returns that they have calculated, and included so such things, such as estimations changes in revenue recognition policies. Tell me okay, these guys are not growing at 15% anymore. They will do whatever it takes to simulate that they are still the same company they were 10-20 years ago, which they unfortunately aren’t.

So I think the market is pricing in hopefully future growth, like that the middle class in the world goes from 3.5 billion now to 5.5 billion in 2014. So that there are an additional 2 billion people buying Nikes and that the China growth story continues in the teens per year and that everything else competition, margins remains equal to the previous 10 years.

However, if I look at the revenue growth rate, this Orange Line, it was much higher than it is in the last five years. And these five years were great for consumer spending. So it went from of around 9-10 percent per year down to around 5.6%. This is a big decline and the company is trying to do whatever they can to keep having the perspective of growth and the revenue is growing. But this is a little bit more of financial engineering, rather than just doing great in business.

So, I think that Nike is priced as a 50% growth stock. You can compare this to Visa. I made a Visa growth stock analysis and I’ll put this into the link in description below on YouTube. Please check that video too. And you’ll see that Visa is growing at 15% and it was priced at the better price to earnings ratio than Nike, which is growing only at 6%.

The growth comes from financial engineering with questionable returns, for example, on buybacks at current levels, and at $100 per share, for me, it’s not a good risk reward investment perspective, but you never know. We are in an environment of free money and anything can happen and the 1% dividend yield Nikes giving with the growth can be a miraculous investment compared to zero with treasuries and without protection for inflation.

So the biggest risk for Nike Stock is that the market decides to price it as a slow growth stock of 6%, not 15%. And that’s something you really should keep an eye on when it starts changing, because also the big companies, all the growth companies go into this transition from being a growth company to being a slow growth company or a stalwart.

It’s still a great business, no doubt about that, but you have to avoid when the market figures this change out, when the market figures the transition from the growth company to the stalwart slow growth company. Because then the fundamentals will look much different.

People will focus on other things, and then the returns might be negative, which if I put it all in my statistical models, there is a 94% chance of underperforming based on the current and fundamentals that Nike is offering. And just a 6% chance of doing better. This doesn’t mean anything in this environment. As I said 1% dividend yield and and 35 price earnings ratio that is what 3.3% return.

Owning a great business can still be miraculous and the stock can also double thanks to all the Robinhood army speculators. But this is what I see. Also, from a fundamental perspective, there is a 56.8% chance of negative returns over the next years, so be careful. I don’t think Nike will fly sky high as it was the case in the 80s, 90s. Thanks to all what’s going on, even MJ is a little bit older, so no flying. He can probably still dunk. He’s still MJ. Nike will still do well, we can say bag it, Nike Stock but we can say okay, slow and steady. We are retired. Let’s grow this business slow and steady. And that’s what you should expect from this. Be careful for the changing perspective the market might have on Nike.

Thank you for watching. Don’t forget to check the Visa video please subscribe, click the notification bell for more such interesting videos on stock analysis, investment mindset and investment education. Also check my stock market free course in the link in the description below. If you’re interested in more stock analysis that I do, I’m currently analysing the Austrian market, please check my stock market research platform for more similar analysis that I don’t make videos on also my portfolios and everything. Thank you, and I’ll see you the next video.