JDP Capital Management’s letter to Teekay Offshore Partners L.P. (NYSE:TOO) Special Committee, dated May 21, 2019.

Attached is an open letter to the Special Committee that will decide to allow Brookfield Business Partners to under-bid for the remaining stub of Teekay Offshore they don’t own at a 70% discount to what the company is worth. This is different from other activist letters..

Q1 hedge fund letters, conference, scoops etc

Teekay Offshore Partners L.P.

c/o Teekay Offshore GP LLC, its general partner

Fourth Floor, Belvedere Building

69 Pitts Bay Road

Hamilton, HM 08 Bermuda

Attn: Members of the Conflicts Committee of the Board of Directors of Teekay Offshore GP LLC

Re: Minority Unit Holder response to the proposed acquisition of all outstanding publicly held Common Units of Teekay Offshore Partners L.P.

Cc: Bruce Flatt, CEO Brookfield Asset Management (NYSE: BAM)

Cyrus Madon, CEO Brookfield Business Partners (NYSE: BBU)

Jaspreet Dehl, CFO Brookfield Business Partners: (NYSE: BBU)

David Levenson, Managing Partner, Brookfield Business Partners (NYSE: BBU)

Bradley Weismiller, Managing Partner, Brookfield Business Partners (NYSE: BBU)

Ingvild Sæther, CEO, Teekay Offshore (NYSE: TOO)

Jan Rune Steinsland, CFO, Teekay Offshore (NYSE: TOO)

William L. (“Bill”) Transier, Board Member, Teekay Offshore (NYSE: TOO)

Bill Utt, Board Member, Teekay Offshore (NYSE: TOO)

Ian Craig, Board Member, Teekay Offshore (NYSE: TOO)

Kenneth Hvid, Board Member, Teekay Offshore (NYSE: TOO)

Craig Laurie, Board Member, Teekay Offshore (NYSE: TOO)

David L. Lemmon, Board Member, Teekay Offshore (NYSE: TOO)

Jim Reid, Board Member, Teekay Offshore (NYSE: TOO)

Denis Turcotte, Board Member, Teekay Offshore (NYSE: TOO)

Walter Weathers, Board Member, Teekay Offshore (NYSE: TOO)

Dear Special Committee:

This letter represents the views of JDP Capital Management and 25+ funds and individuals who have expressed interest in participating in a response to the Brookfield Business Partner’s (BBU) letter sent to your committee, which requests approval for a take-under bid of Teekay Offshore (TOO) at a price of $1.05 per unit.

Although we are not an official group, the stakeholders listed at the end of this letter collectively own at least 5% of Teekay Offshore common units. Some of those not listed below have opted to write their own letter directly to Bruce Flatt and/or Cyrus Madon of Brookfield.

The purpose of this letter is to respond and oppose BBU’s unjustifiably low bid, and express a deep concern for BBU’s judgment for making such an egregious effort to take advantage of minority unit holders.

BBU’s offer is a 58% discount to what BBU paid for control of TOO in July 2017 (almost two years ago) BEFORE the balance sheet was stabilized, BEFORE Brent crude prices had rebounded, and BEFORE TOO was strategically positioned to take advantage of a strong rebound in Offshore North Sea, Canada and Brazil drilling activity (TOO’s customers).

JDP believes TOO is worth at least $4 per share today based on existing cash flow, asset quality, counterparty profiles, unique duopolistic market position in its shuttle tanker fleet, highly profitable Brazilian FPSO JVs, and a balance sheet that has been de-risked.

We are asking that the Special Committee consider a much higher offer that more fairly represents the going concern value of the company, peer valuation multiples, and longer-term value minority investors will give up by missing out on TOO’s recovery.

Alternatively, we would be happy to continue owning the public stock—even at the currently depressed price—we know that the company’s economic value will be reflected in the stock over time.

In the event of deciding to move forward with a buyout, we request that the Conflicts Committee require the Brookfield Consortium to publicly disclose its own fair value opinion of Teekay Offshore.As well, the Conflicts Committee should hire an independent third party to evaluate and publicly disclose their opinion of TOO’s fair value. It would be irresponsible to base fair value on the pricing of a private block trade from a distressed seller, as happened with Teekay Corporation’s recent sale of their TOO stock; this is not a standard or credible valuation framework for a fair acquisition bid.

Is this the new way Brookfield makes money?

- This offer damages the Brookfield brand and sets a precedent of willingness to abuse control and take advantage of minority investors for even a small amount of potential return

- This offer introduces sponsor risk to all Brookfield publicly owned investments and partnerships with the would-be buyers or sellers of assets to any Brookfield entity

- This offer sets a terrible example for Brookfield’s investment model, which relies on trust and alignment of interest with other co-investors including large Canadian and American pension funds

- This offer also damages Brookfield’s future reputation for issuing debt, hybrid and equity capital for itself and affiliates

Teekay Offshore stock price suffers from BBU-inflicted issues unrelated to fundamentals

“We can see an improved offshore market. The increase in global oil prices has resulted in increased free cash flow for E&P companies, and this is supporting renewed interest and investments in offshore production and logistics… our customers are increasing their investment budget in our core markets being the North Sea and Brazil, we are quite optimistic about the opportunities that we expect to see for Teekay Offshore.” – Ingvild Sæther, CEO Teekay Offshore, 1Q transcript, April 30th, 2019

Summary Points

- Brookfield unfairly argues that market value of TOO should be based on a recent distressed block sale

- Brookfield changes the narrative on balance sheet risk to suit its needs

- Brookfield created its own capital markets risks

- Brookfield is asking minority investors to pay for its own poor capital allocation decisions

- JDP continues to see a minimum of $4 per share valuation today

1. BBU unfairly argues that market value of TOO should be based on a recent distressed block sale

Brookfield Consortium Claim:

“Given that Teekay Corporation (“TKC”) is a sophisticated, well-advised counterparty with intimate knowledge of TOO’s business, we believe that the $1.05 per Common Unit acquisition price paid to TKC is representative of a fair price for all of the outstanding TOO Common Units held by holders other than the Brookfield Consortium.” -Brookfield Business Partners letter to Conflicts Committee, May 17, 2019

JDP Counterclaim: Teekay Corporation was a forced seller of their 14% stake in TOO stock, which included a $25M loan and warrants, because they were struggling to refinance their own unsecured debt. The price paid by BBU for Teekay Corp’s TOO stake does not represent anywhere close to fair value. BBU is unfairly taking advantage of this distressed transaction to justify a similar bid for the entire company.

“The proceeds from this transaction allow us to further strengthen Teekay Corporation’s balance sheet and credit profile, while significantly enhancing our near-term financial flexibility and range of options to address our near-term bond maturity.” -Kenneth Hvid, Teekay Corporation’s President and CEO, April 30, 2019

2. Brookfield changes the narrative on balance sheet risk to suit its needs Brookfield Consortium Claim:

“Furthermore, in light of our assessment of TOO’s likely need for additional capital to support growth and address upcoming debt maturities” -Brookfield Business Partners letter to Conflicts Committee, May 17, 2019

JDP Counterclaim A): Brookfield has now changed the narrative on balance sheet risk to suit its needs. Brookfield declared TOO’s balance sheet “de-risked” just months ago, but it is now claiming Teekay Offshore requires capital to “support growth and address upcoming debt maturities.”

This new statement is contradictory and is intended to scare minority stock investors to support its take under agenda. In August 2018, while syndicating the $700 million Brookfield Consortium-sponsored Teekay Offshore unsecured debt to other participants, Brookfield painted a picture of a company with a balance sheet that would now be “de-risked”.

“I think, they issued a bond offering during a relatively choppy time for high-yield bonds, and we simply wanted to provide them with assistance and part of the reason is we are highly, highly confident this company continues to deleverage…

The credit profile will look very, very different from where it is today, and we just thought perhaps it was a little bit misunderstood in the market place. We’re very close to it. So we’re highly confident.”

-Cyrus Madon, CEO, Brookfield Business Partners, August 3rd 2018

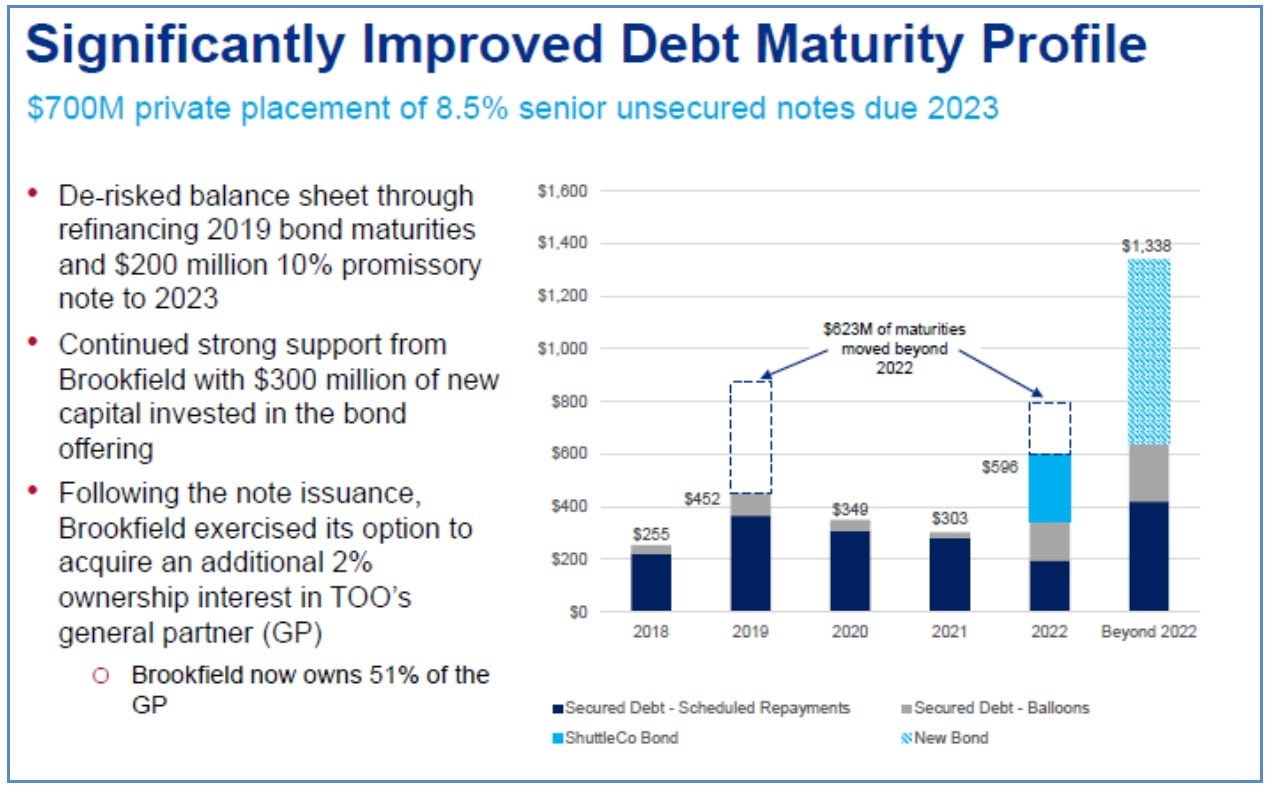

Counterclaim B): Brookfield has stated that TOO’s debt maturity profile has “significantly improved”

“The recently completed […] $700 million unsecured bond offering has de-risked our balance sheet and significantly improved the partnership’s debt maturity profile -Tim Cowan, SVP, Brookfield Asset Management and Interim Teekay Offshore CFO, August 2018

2Q 2018 Earnings presentation slide #8, Brookfield Consortium and Teekay Offshore

Counterclaim C): Brookfield publicly commits to supporting its investments

“Teekay’s business plan is to substantially deleverage over time, which should support stronger debt and equity valuations…[W]e will always support our businesses.” – Cyrus Madon, CEO, Brookfield Business Partners, August 3rd 2018

Counterclaim D): TOO’s management has executed well on recent debt refinancing

a) Counter to the Brookfield Consortium’s recent claims, but in line with BBU’s own claims last in August 2018, Teekay Offshore’s access to debt capital markets and ability to service its debt maturities has been improving rather than deteriorating

b) In April 2019, Teekay Offshore’s management secured a $414M shuttle tanker facility that represents 15% of Teekay Offshore’s total outstanding net debt.

This facility was financed at highly competitive L + 225 bps, 18-year blended profile and is 90% non-recourse to Teekay Offshore

“We are grateful for the continued strong support we receive from our growing bank group, as represented by our new $414 million debt facility” – Ingvild Sæther, President and CEO of Teekay Offshore Group Ltd., April 2019

a) Refinancing of $450M revolving credit facility with commercial banks, L + 250 bps and improved amortization from $100M to the $54M, offering was “substantially oversubscribed” per Teekay Offshore Management. Closing in May 2019

b) Secured FPSO refinancing with three-year tenor at L+ 300 bps closed April 2019

3. Brookfield created its own capital markets risks

Brookfield Consortium Claim:

“…TOO [has] limited options for obtaining additional capital from either the public equity or debt markets…” – Brookfield Business Partners letter to Conflicts Committee, May 17, 2019

JDP Counterclaim: Brookfield created its own capital markets risks that have been the primary drag on TOO stock. The absence of a public commitment by Brookfield on their intent to protect minority stakeholders resulted in confusion and distrust over long-term goals and alignment of interest.

The result was a self-fulfilling prophecy of sponsorship risk that led to a higher cost of capital, inability to access equity capital markets, and the perpetuation of a confusing story, which then made the stock uninvestable for a majority of minority investors.

Teekay Offshore-BBU has never had an investor day, or a significant non-deal roadshow. To make the narrative worse, BBU has never provided any public goals, plans or strategy for Teekay Offshore.

BBU has profited enormously off its own debt and fees

4. Brookfield is asking minority investors to pay for its own poor capital allocation decisions

Brookfield Consortium’s Claim:

“…TOO [has] limited options for obtaining additional capital from either the public equity or debt markets…” -Brookfield Business Partners letter to Conflicts Committee, May 17, 2019

JDP Counterclaim: We do not see a funding gap that is not manageable with internal resources. With the recent progress in expanding commitments in TOO’s bank debt, a ~$6bn revenue backlog with investment grade counterparties and no significant non-secured debt maturities until 2022, we believe any funding gap is being driven by Brookfield backing away from its commitment to invest in shuttle tankers per its 2017 strategic investment goals.

Under Brookfield’s sponsorship, Teekay Offshore entered into $820M in shuttle tanker newbuild growth projects for delivery in 2019 – 2021. Brookfield’s strategic partnership in 2017 was designed to enable TOO to “invest in [its] market leading shuttle tanker franchise.”

Fast forward to just 19 months later, before taking delivery of any shuttle tankers, Brookfield is now backing away from its prior financing commitments for these same projects and claiming Teekay Offshore cannot adequately secure financing for these growth projects.

If Brookfield committed to facilitating shuttle tanker investments, it should continue to honor this commitment with a reasonable cost of capital.

A history of misguided capital allocation

- In 2017 TOO Management + BBU claimed growth projects were fully funded through Q1 – 18

- Shortly after, at BBU’s authorization, TOO orders six new shuttle tankers for ~$820M to be delivered from 2019 and 2021

Strategic Partnership with Brookfield presentation slide #6, Brookfield Consortium and Teekay Offshore

The $820M in newbuild funding costs should have been easily anticipated and managed:

- Long newbuild construction times (2-3 years) means capex is easily anticipated

- TOO management was able to solidly execute in obtaining low-cost bank debt

- Significant free cash flows from TOO ~$6.5Bn in backlog (at the time) with investment grade counterparties

- Brookfield’s expertise from “100 years of experience as a leading global investor, operator and manager of real assets”

- TOO’s board was slow to implement the dividend cut early on which contributed to CapEx mismanagement.

Any potential funding gap claim today is self-inflicted by the Brookfield Consortium’s back-tracking on committing to fund their 2017 Strategic Investment Goals around TOO’s core shuttle tanker fleet.

[W]e will always support our businesses.” -Cyrus Madon, CEO, Brookfield Business Partners, August 3rd 2018JDP continues to see a minimum of $4 per share valuation today based on dramatic improvements in TOO’s fundamentals since the BBU recapitalization. This is the same predictable cash flowing infrastructure business BBU paid $2.50 per share to control before fixing the balance sheet nearly two years ago.

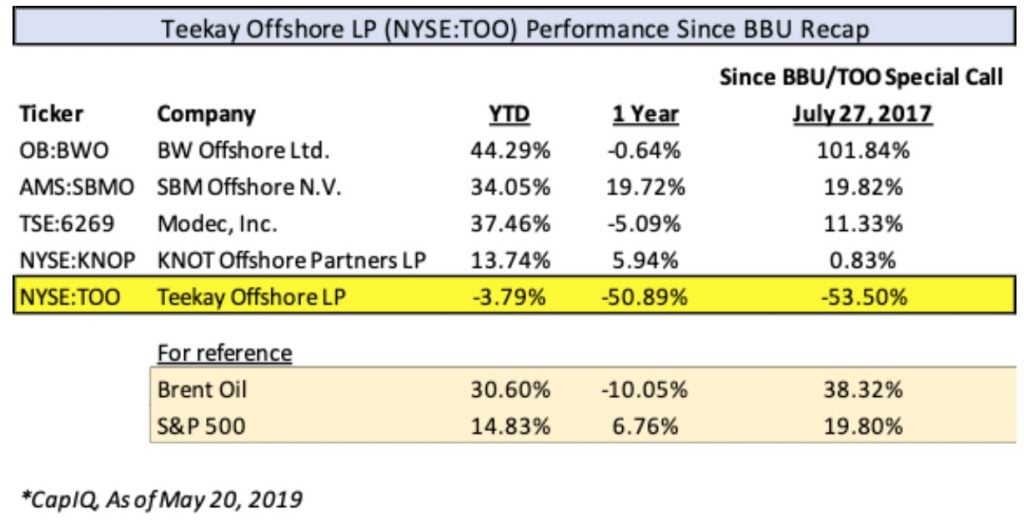

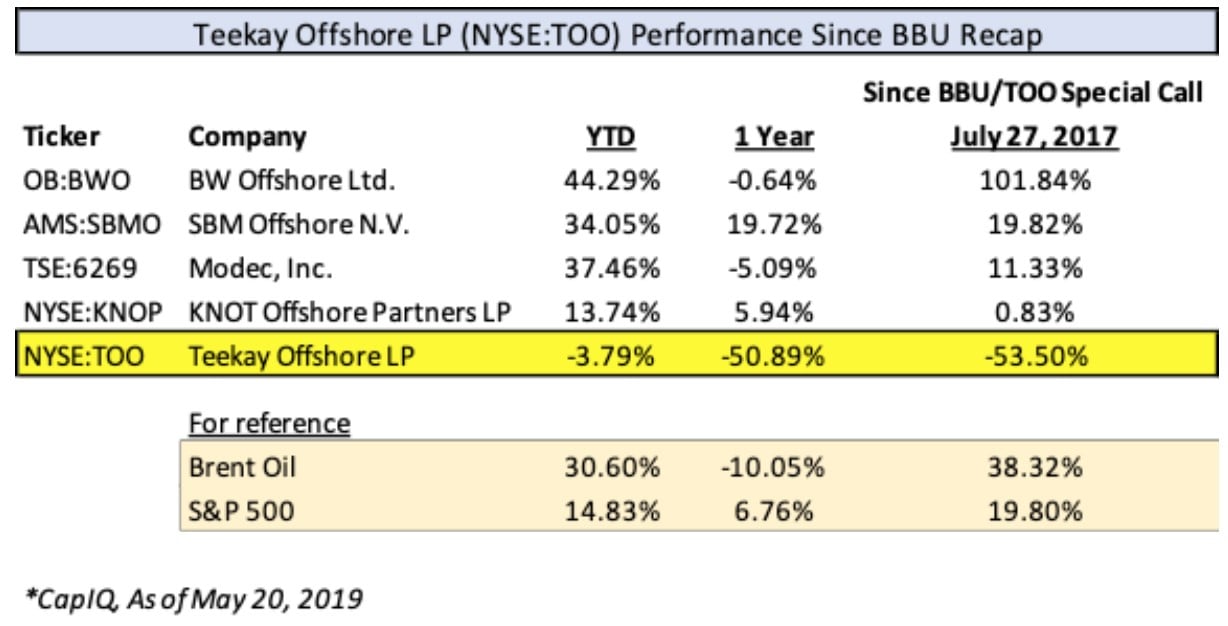

Since the BBU transaction on July 27 2017, TOO’s adjusted EBITDA is up ~50%, leverage ratio is down 12% with an improved maturity profile. Yet the stock has lost 53% of its value while its peer group has added over 50% on average. Brent Crude is also up over 38% and S&P is up nearly 20% in the same period.

Key improvements since Brookfield 2017 Strategic Transaction:

a. Leverage Ratio improved 38% from ~7.4x to ~4.5x currently, below peers and in-line with management’s stated target

b. No meaningful debt maturities until 2022

c. Adjusted EBITDA increased ~48% from 2017 to 2018 ($782M, including settlement)

d. Industry fundamentals have improved dramatically

JDP would be happy to discuss TOO’s valuation with the Committee based on both run-off and going concern value.

Sincerely,

Jeremy Deal

Managing Partner

Teekay Offshore LP unit holders in support of this letter and NOT in support of Brookfield Business Partner’s $1.05 offer for the remaining public shares

JDP Capital Management, New York City

Aquamarine Fund, Zurich

Guardian Fund, Amsterdam

Ambient Sound Investments, Tallinn

Neptune Capital, Pembroke

Rhizome Partners, New York City

Franklin Watson Investments, Zug

David Stone, San Diego

Massif Capital, Charlotte

Bonhoeffer Capital Management, Rochester

Bradley Jacobs, London

Milestone Capital Management, Wayzata

Matthew Turk, San Diego

Noster Capital, London

Konstantin Othmer, Bay Area

Elton Crowder, Seattle

Peterson Capital Management, Los Angeles

Evergreen Gavekal, Bellevue

This article first appeared on ValueWalk Premium