Tesla Inc (NASDAQ:TSLA)’s significant drop, 35% year to date compared to the S&P up 14%, has investors looking for answers. How this could have happened may best be explained by looking at how Tesla’s stock price got as high as it did. The last time Tesla traded at 200 was over 2 years ago. Following the March 31st, 2106 Model 3 reveal event and the Model 3 delivery event in July, Tesla continually climbed quickly passing 200 before settling and staying above 350. Elon Musk wasted no opportunity over the course of those 16 months to build hype and make promises that Tesla ultimately was not able to keep.

Based on guidance given by Musk and Tesla, it would not have been unreasonable for an investor in early 2017 to believe that at some point the next year Tesla would be producing 10,000 cars a week and with Model 3 have its first mass market car priced at $35,000 ( often touted as $27,500 after rebates ) with margins exceeding 25%. The counter to these claims was simple, how could Tesla possibly maintain such high margins on car that sold for half as much as a Model S? Musk quelled these concerns by explaining that Tesla would achieve unpresented savings by scaling up production and bringing automation to every part of the manufacturing process. Production numbers, however, failed to keep pace with Musk’s vision and by his own admission Tesla’s attempt at bringing more automation to its production lines was a failure. By mid 2017 the goal of “10,000 cars a week sometime in the next year”, a claim featured prominently featured in the top line of Tesla’s first investor letter of 2017, was looking less and less likely. With troubles mounting Tesla continued with the same guidance in their 2017 Q2 earnings letter released in August of 2017 and Musk would go on to strongly confirm those number in the conference call the same day saying:

Q1 hedge fund letters, conference, scoops etc

“What people should absolutely have zero concern about, zero, is that Tesla will achieve a 10,000-unit production week by the end of next year (2018).“

In the days following the 2017 Q2 earnings release Tesla was once again trading at all-time highs despite disappointing delivery numbers that quarter and mounting concerns about production. In hindsight, it is clear why Tesla was trading above 350. At the time, an investor taking Musk’s claims at face value would have expected Tesla to soon be producing cars at a rate of half a million a year. Given that level of production and a modest average sale price of $60,000 per car would equate to an annual revenue of 30 billion for Tesla’s automotive division alone. Astonishing growth given that in the same letter Tesla again guided for future production of 10,000 a week they only reported revenue of 5.5 billion for the first half of the year.

Unfortunately for Elon Musk and Tesla investors, 2018 is over and Tesla is nowhere close to making 10,000 cars a week. In the last quarter of 2018 and the first quarter of 2019 Tesla produced 163,555 vehicles, a rate of around 6,300 vehicles cars a week. Tesla now must face the reality that manufacturing cars is extraordinarily difficult. Despite two rounds layoffs to cut costs and pushing back release dates for lower priced trim varieties Tesla, still hasn’t been able to hit achieve their margin goals.

Tesla investors were initially sold on the pitch that Tesla would produce high priced luxury vehicles to pay for the production of a mass market vehicle that could be sold by the millions. The economies of scale would then equally high margins and make Tesla a true rival to established auto makers like Toyota and VW. That story has slowly died due to Tesla’s failure to ramp up production and lower costs. Tesla may offer a unique and exciting product, but the company faces the same production challenges and capital requirements as their competitors. If Tesla becomes just another car company, they face a strong headwind of a sector where P/E’s are often under 10.

Faced with a dying growth narrative what can a CEO do? Simple, change the story. Bring on the robo taxis! Musk has promised that Tesla will soon have a million driverless cars on the road earning their owner’s money as they sleep. Will investors buy in to the new story? Tesla’s latest equity raise at $243 a share showed there are still many who have faith that Elon Musk can navigate this new path but the drop to under 200 has shown there are plenty of skeptics as well. Convincing investors to fund Tesla’s foray into autonomy is not the only challenge, the company must execute as well. Musk has once again set the bar quite high by promising fully autonomous vehicles within a year. Will autonomous cars be Tesla savior or only serve to hasten their decline? We’ll discuss this and more in our next Tesla post.

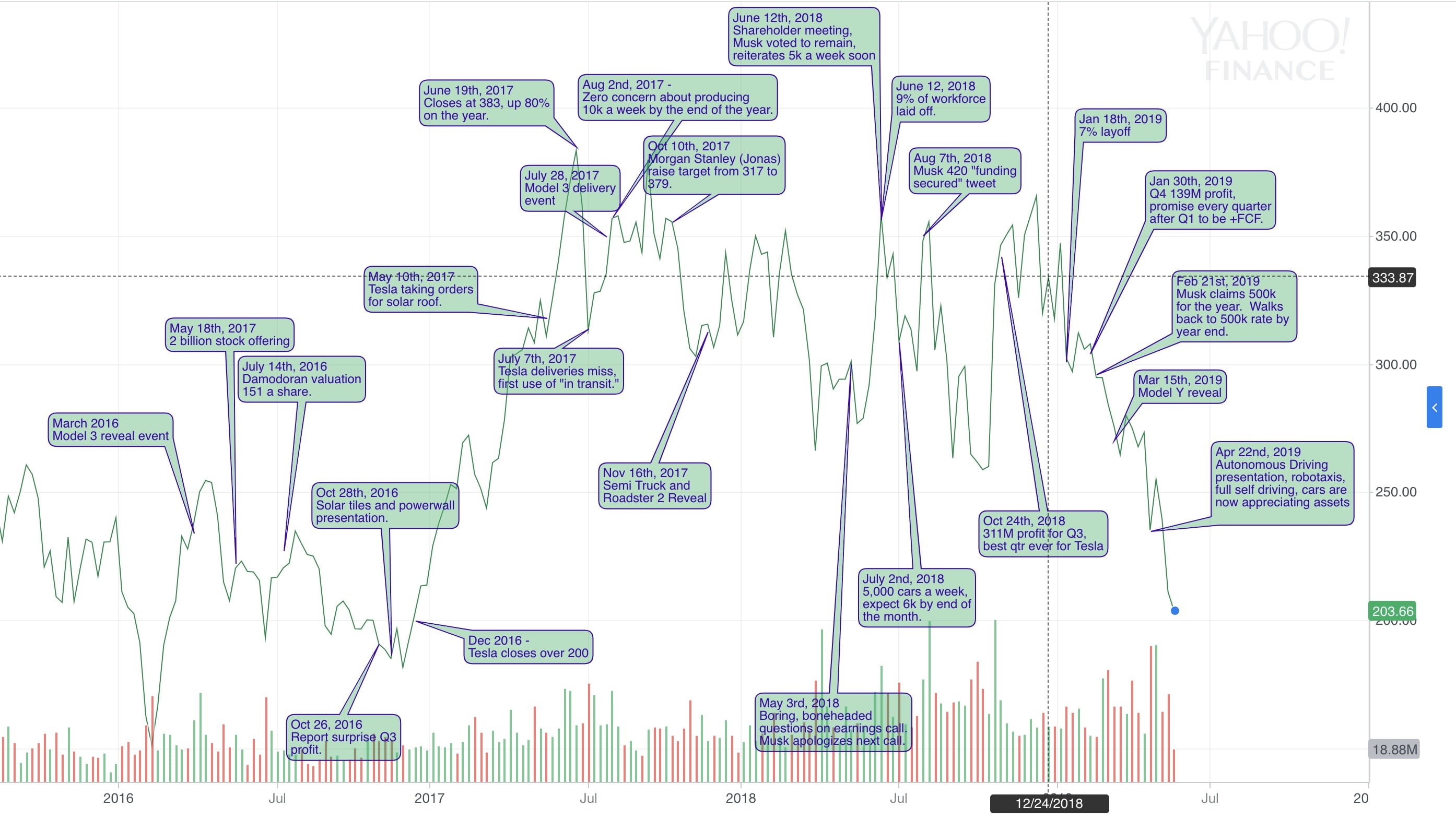

Finally, as a handy tool, we attach a chart showing the Tesla stock price and most of the major announcements regarding the company.

{kind=link}