Global Quality Edge Fund presentation titled, “Tail-Risk Hedging Strategy.” How to leverage the end of the business cycle without exposing our fund to permanent capital loss?

Objective:

- Understand the current convergence between business cycle and the long term debt cycle.

- Empathize the benefits of Tail Hedging as a means to shield from capital loss. We began implementing this strategy in Q4-2018 to protect the fund from significant market downturns, similar in scale to the ones seen in 2000 and 2008. The fund could even see positive returns in a big stock market crash.

Q4 hedge fund letters, conference, scoops etc

* Global Quality Edge fund is an ideal investment alternative to steer clear from permanent capital loss, at a time when the business cycle is shifting without missing out on possible gains from market upturns.

*See my interview with ValueWalk for further details on my investment philosophy and 2 recent investment ideas.

The Fund:

- Global Quality Edge Fund is a concentrated equity fund that invests only in extraordinary companies with global focus, sustainable competitive advantages, high recurring revenue, good capital allocators, aligned interest with CEO and shareholders and with preference for SMid Cap stocks. The Fund Manager speaks regularly with the management of the companies in portfolio, regardless of their geographic location.

- The Fund uses tail risk strategies as a hedge only when the business cycle changes from deceleration to recession phase, buying OTM PUT index options that trade 20- 30% below current market prices.

Macroeconomic negative/positive views.

- What are today’s market concerns?

– European economic slowdown.

– Fiscal stimulus promoted by the U.S. administration coming to an end in 2019.

– Hawkish message warnings by the Fed.

– Drop in oil prices.

– Increased geopolitical risk: Italy, France, Brexit, among others.. - What is today’s reality?

+ World growth is slowing but the OCDE remains optimistic by forecasting 3.7% and 3.5% in 2019 and 2020.

+ Even though the American economy shows signs of slowing down, the underlying fundamentals (profits) remain intact..

+ Trade tensions between China and the U.S. remain high but a resolution could be agreed during Q1-2019 between the 2 countries.

+ The drop in oil prices could delay the Federal Reserve’s plans for raising interest rates, amid inflation concerns..

+ Despite the decline in leading economic indicators for the U.S. and Europe, there is no clear evidence we are heading towards a recession..

+ Leading economic indicators in China suggest a slight improvement in its economic outlook. .

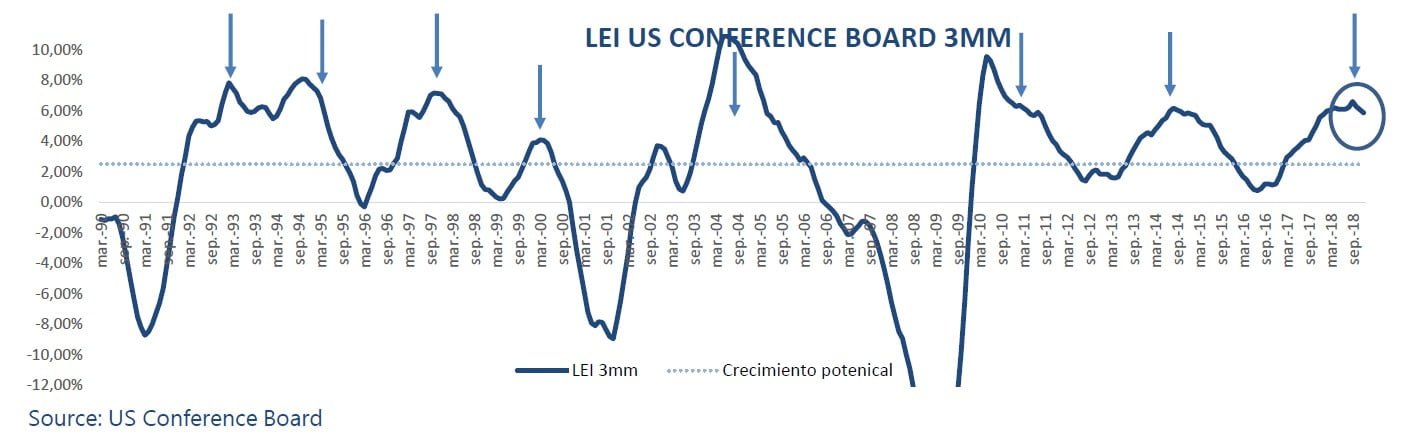

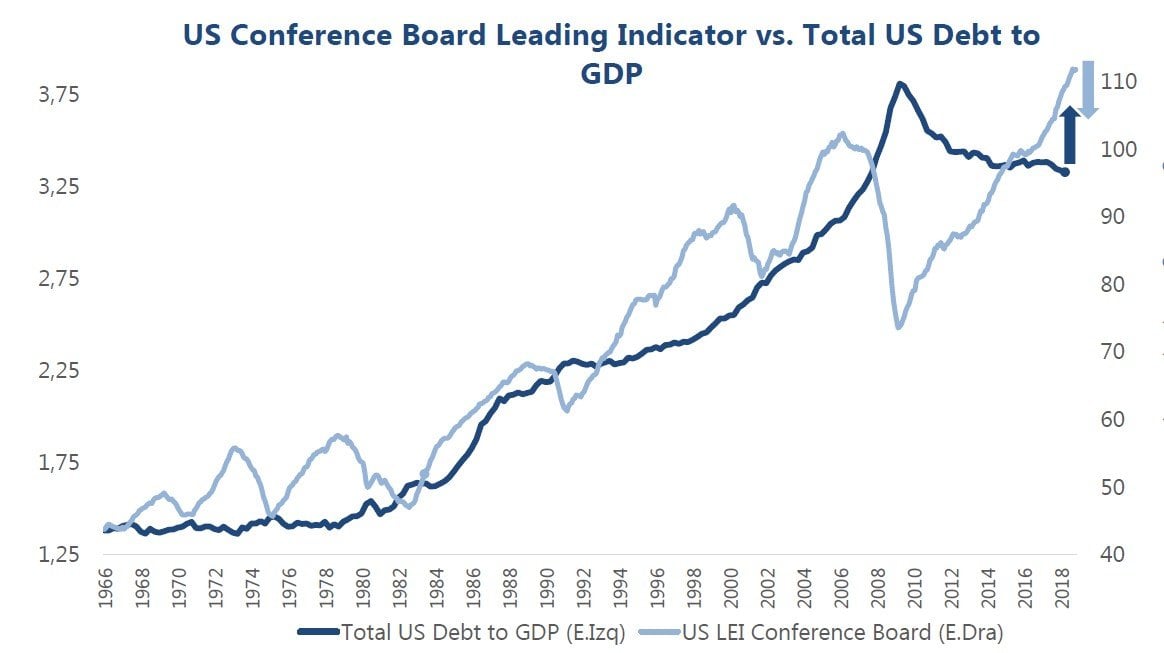

Macro view: U.S. Leading indicators and the business cycle.

- We use the U.S. Conference Board and the OECD Leading Indicators to determine the phase of the current business cycle.

- The key is to analyze and establish how the economy will grow in relation to its growth potential (U.S.: 2.5%-2.75%). To achieve this, we divide the business cycle in 4 phases.

- In our view, the economic cycle has recently entered into deceleration but not into recession, as some sectors in the stock market may suggest (Autos, commodities, small caps, etc.).

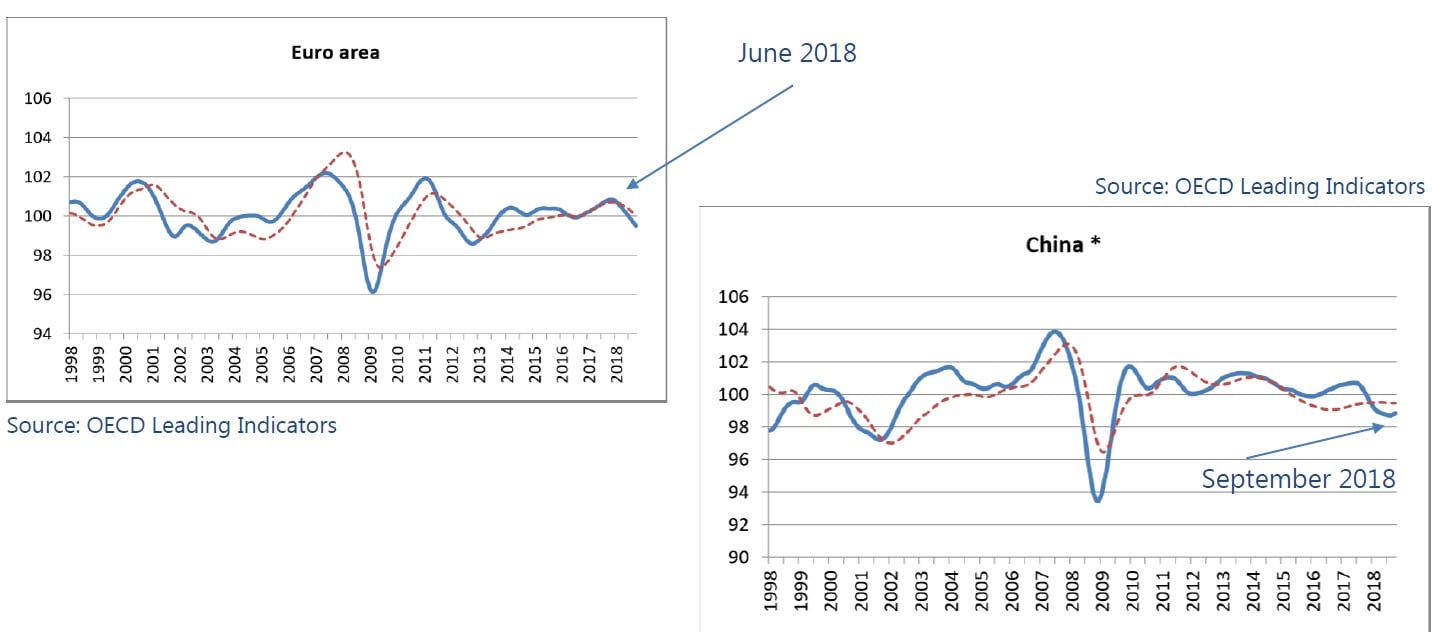

Macro view: Europe and China.

- Europe shows continued economic decline from the start of the summer in 2018 while emerging markets in Asia have stabilised and indicate early stages of improvement..

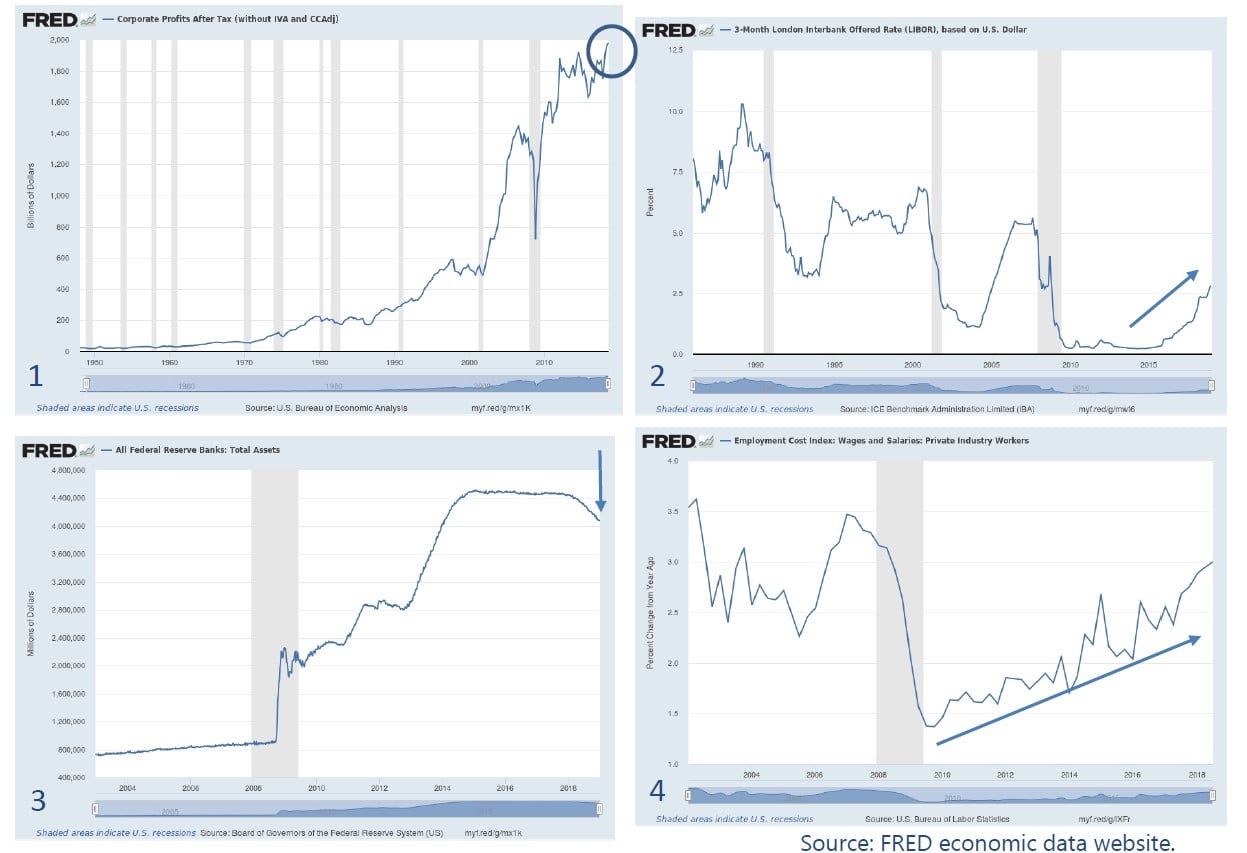

Macro: What happens during the 3rd or deceleration phase of the business cycle?

- Profits are reaching all-time highs and could eventually begin to drop (*Chart 1).

- Interest and inflation rates begin to rebound (*Chart 2).

- Asset inflation are at high levels (Stocks, bonds, etc.).

- Central banks reduce the money supply (credit) and therefore the liquidity in the system. (*Chart 3).

- The cost of labor shows a steep rise and companies will be forced to reduce it in the long-term. (*Chart 4).

Phase 3 is perhaps the most risky for investors because stock markets will tend to correct previous excesses, in terms of monetary policy.

Macro: What happens during the 3rd economic cycle?

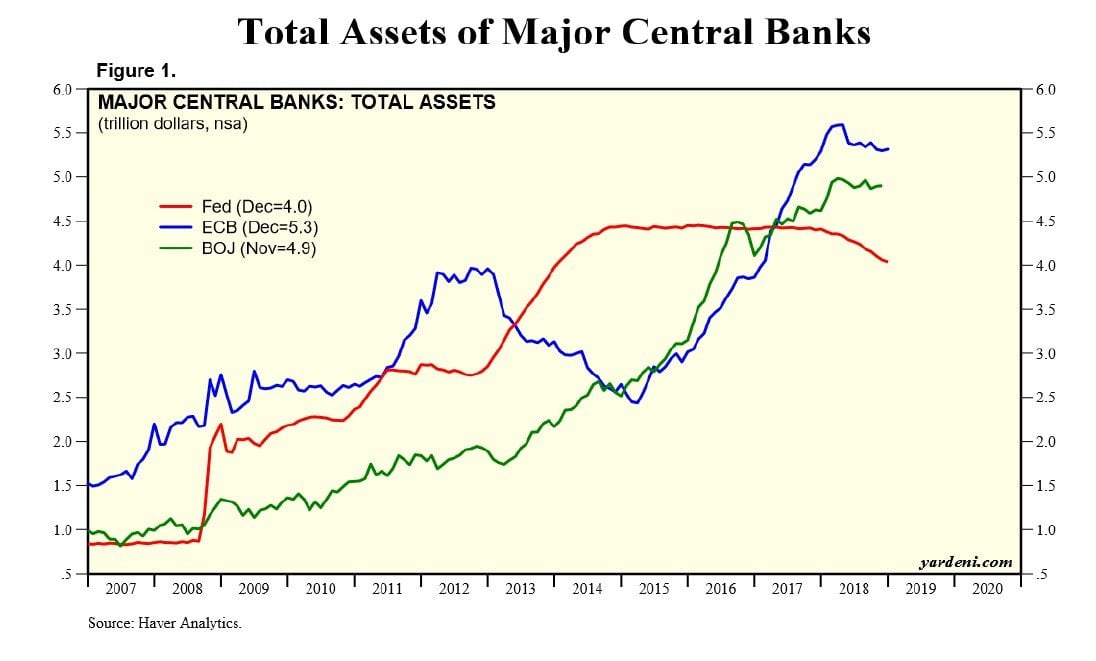

Macro: What about the level of main central bank balance sheet assets?

- In Japan, Total Assets are above 100% of GDP .

- The U.S. and Europe are below 50%.

- We see the same dynamic in the main central banks across the world, which is why it seems

that their running out of ammunition; if they haven’t already!

Macro: Are there any other risks? Yes, we need analyse the long-term debt cycle.

- The long-term debt cycle (50-75 years) – made up of mini-cycles lasting 5 to 7 years – show how central banks follow the same pattern reducing interest rates and – when no other measure is possible – by printing money and buying up debt (1929-1933 and 2008-2009).

- As a result, the previous scenario increases prices on financial assets disproportionately (1933-1937 and 2009-2018), forcing banks to apply a more ‘hawkish’ or restrictive monetary policy.

- Everything seems to indicate that we are entering the final phase of the economic cycle which also coincides with the final phase of long-term debt; when financial assets and the economy are more vulnerable to a reduction in credit and central banks are left will very few tools to stimulate growth.

How is the global debt level going to be decreased without hindering economic growth?

- If debt is used to generate returns on feasible projects, there is an overall benefit for the economy. If projects are not profitable and there are no other means to reduce debt: “Houston, we have a problem!”.

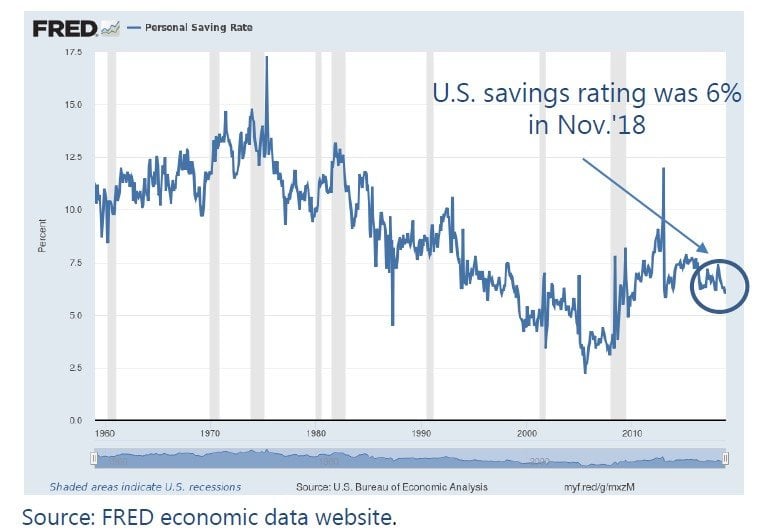

- Savings rate at its lowest, leading to lower payment capacity [debt (principal + interest), taxes, etc.) for consumers and lower forecast on future spend (consumption). Remember that consumer spending accounts for 70% of the U.S.’ total GDP.

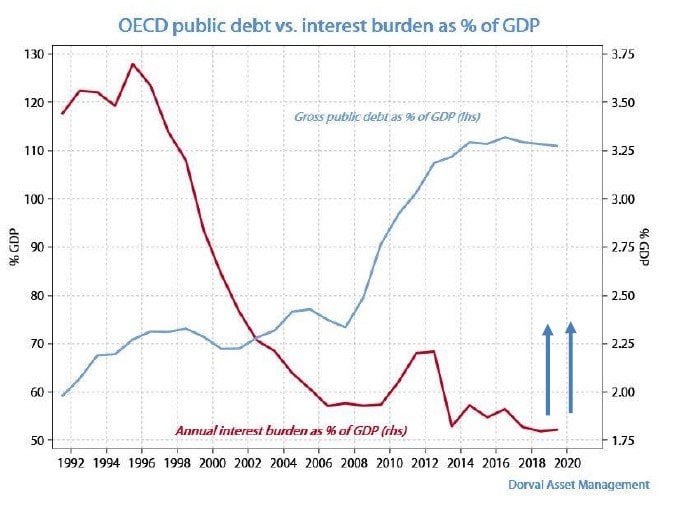

- Artificially low interest rates have led to low interest expense but this may well change soon.

Macro: Will monetary expansion; therefore, carry its own risks? Yes, a few…

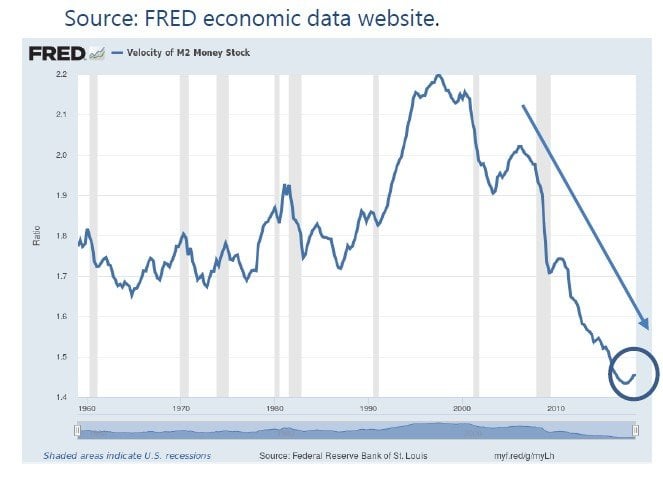

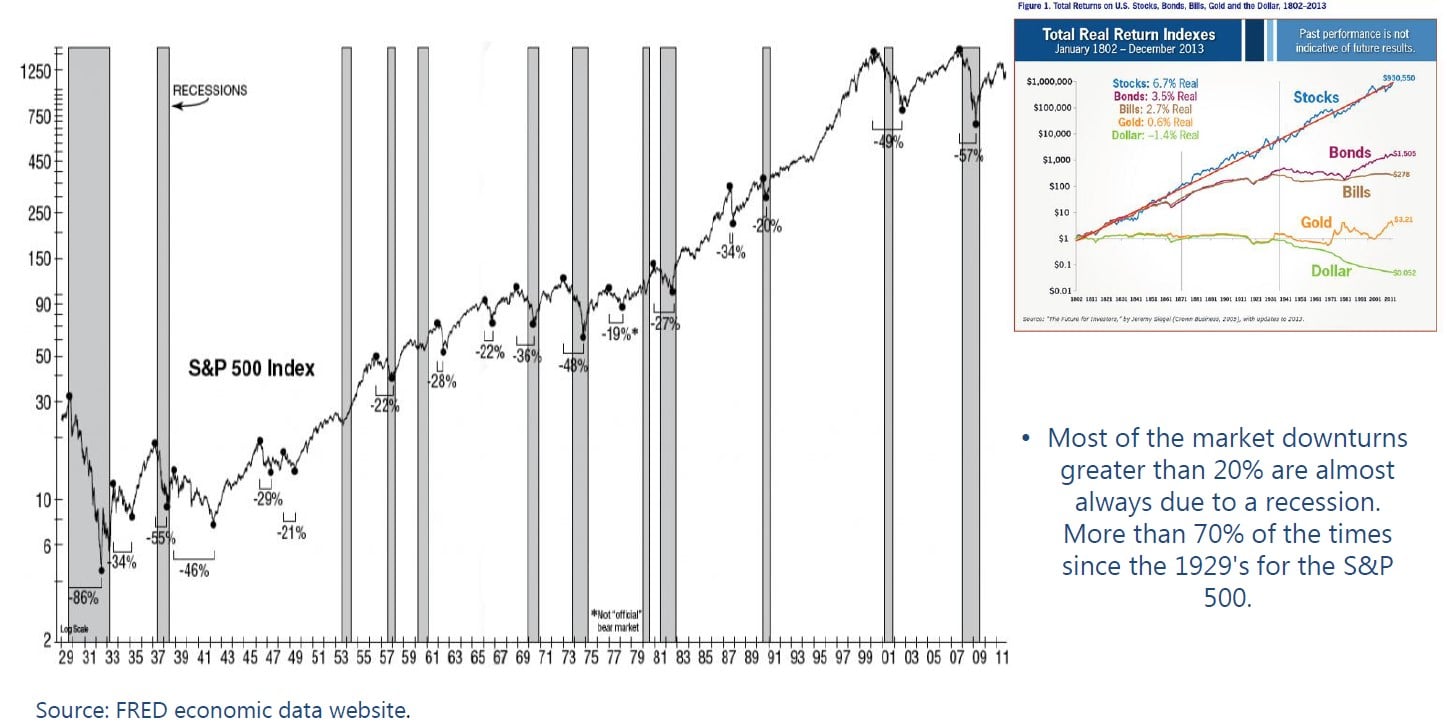

Source: FRED economic data website.

- Central banks have created a large fake monetary stock (debt) which has not been of any or little help in spurring GDP growth; especially in Europe.

- Printing money should only ever be an extraordinary measure and not a recurring one..

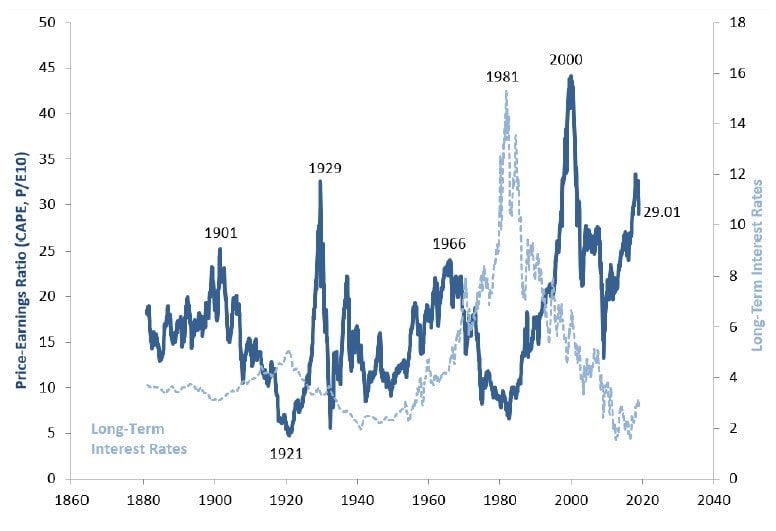

- The CAPE ratio serves as a good measure to see how much financial assets (markets) are overvalued; a situation which could last a number of years within a range of all-time highs.

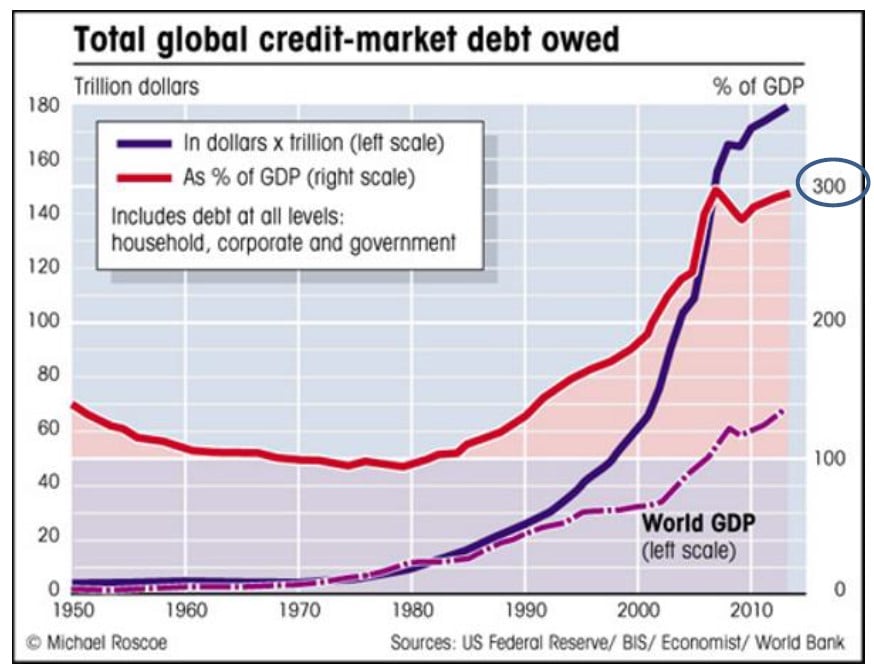

Macro: Business cycle and long-term debt cycle

- Total U.S. Debt to GDP 3.32x April’18.

- Debt breakdown in the U.S.:

- Corporate 45,62%

- Government 32,87%

- Families 21,51%

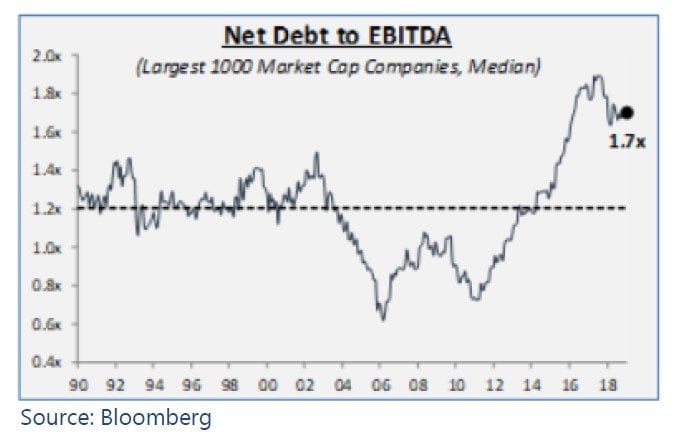

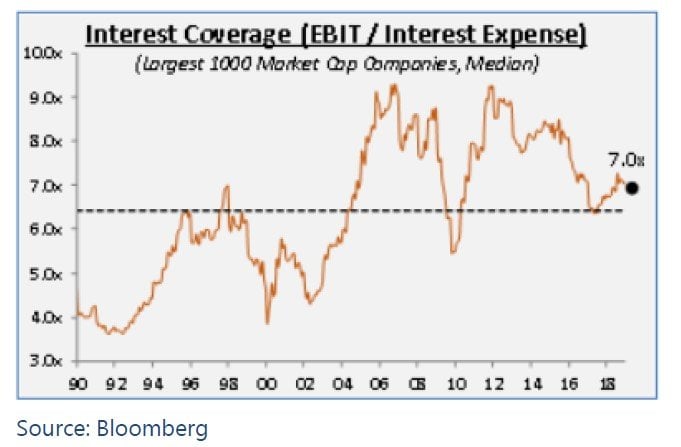

- A slowdown in the business cycle added to unsustainable debt to GDP levels lead to exponential rises in risk for financial assets.

- The debt of non-financial companies has not stopped growing since the last financial crisis (2008).

- Although interest rates remain low, a slowdown in the economic cycle or a rate hike could have a direct impact on corporate profits.

- Although today the coverage of financial expenses seems manageable, it would not be in a recessionary environment.

- From a long-term point of view, we identify a potential risk, although to date there are still no tensions in loan defaults and credit spreads.

Macro: What options do governments and central banks have?

1) Austerity.

2) Debt defaults and restructuring.

3) Print money to buy government debt.

4) Transfer money from wealthier classes to less well-off.

- The solution lies in finding the right balance for all options, despite the fact governments never achieve to do so.

- In light of the current situation, we decided to trigger our Tail-risk hedging strategy in the last quarter of 2018, which will continue until: 1) restrictive monetary policies come to an end and leading indicators return to the Expansion phase (the economic cycle is not always lineal) and 2) The economy enters into recession and stock prices broadly reflect this new scenario.

TAIL RISK HEDGING strategy: the stock market will always rise in the long-term…

- Over time, even though shares are perhaps the most profitable assets in which to invest, there are periods where our portfolio requires hedging; as the market experienced in the crisis at the end of 90s, 2002 (Dot-com bubble) and 2008 (financial crisis).

TAIL-RISK HEDGING strategy: How is the idea initially conceived?

- At Global Quality Edge Fund, we implement a tail-risk hedging strategy, inspired by Mark Spitznagel – famous value investor of Universia Investments LP – to shield investments in a similar fashion as an insurance policy would. However, the strategy would only be put into practice when the economy slows and there is a reasonable probability of dipping into recession.

- The main difference with Sptiznagel’s strategy is that we use the U.S. Conference Board leading indicators to better predict changes in the economic cycles; whereas Spitznagel himself relied on the CAPE and Q Ratio. The latter is a measure devised by Nobel laureate in economics, James Robin, that examines the over/under valuation of the market in the long term.

We are pleased to announce our close collaboration with a private institution, renowned internationally in the derivate market, in a detailed study of Tail-Risk Strategy. We believe this will be truly groundbreaking in Spain and continental Europe and significantly relevant; especially at a time when we are experiencing the end of the business cycle in U.S.

TAIL-RISK HEDGING strategy: How to build and implement.

- The strategy involves buying Out of The Money (OTM) put options with the whole purpose of hedging against a significant market downturn caused by a recession. It is not; however, triggered to protect from market corrections (less than 20%).

- Premium costs to be paid are low (1%-3% annually) and do not excessively penalize the total return of the fund if these keep rising or there is no dip into recession.

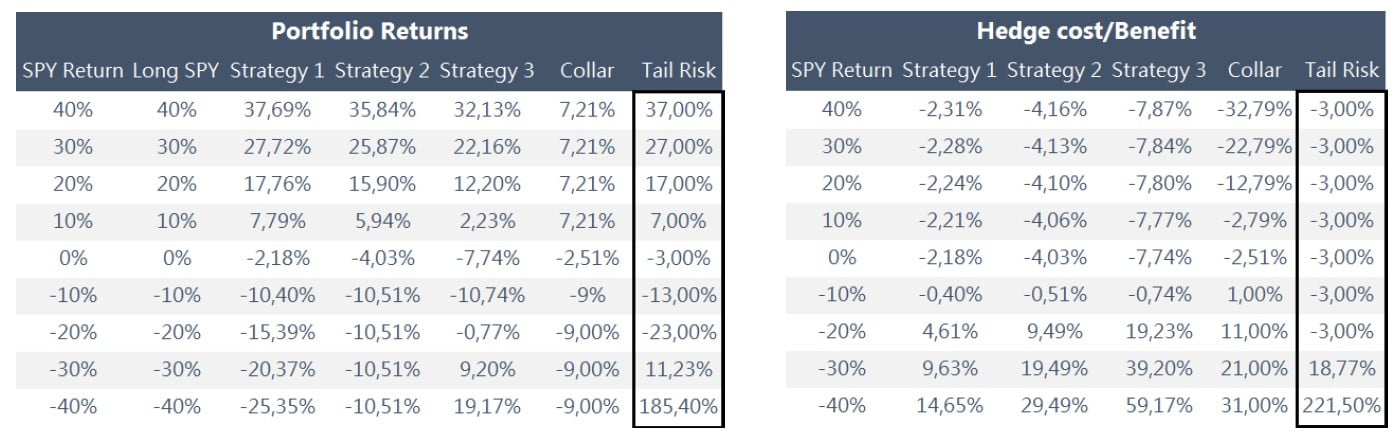

Theoretical exercise to shield from risk with different strategies involving options and Long SPY across an entire year. These may vary according to the value hypothesis used when applying Black-Scholes’s formula. The first strategy assumes a partial hedging (2 SPY options), the second applies a full hedge (4 SPY options), the 3rd strategic scenario assumes hedging levels over 100% (8 SPY options). The Collar assumes the purchase of a PUT option financed by selling a CALL option. The Tail-Risk assumes buying a PUT on SPY 30% out- of-the-money (OTM). To select the options, we used the underlying ETF of the SPX (SPY). The cost of the premiums is a proxy but this will range from 1.5% to 3% annually, depending on the implicit volatility when buying and selling options. The strategy simulates buying 2 months option expiration, monthly roll-over expiration and held during one year.

Source: ZeroHedge

TAIL-RISK HEDGING strategy.

- We believe it is a novel and good alternative for a pure equity fund; given the current business cycle we are experiencing. At Global Quality Edge Fund, investors can continue to enjoy market increases through a portfolio of extraordinary high recurrent revenue and cheap shares, but unlike other pure equity funds, it has an insurance that protects the fund from a permanent loss of capital.

“Governments, they think they can borrow for free. But they have had to borrow a lot. We have had to borrow more than $1trillion dollars…and we’re paying some $300billion in interest”

“You can enter a spiral. In my mind, it’s when governments have to borrow more and more to pay interest – like a Madoff scheme”

“Years ago we had a debt crisis….in 82’ it started in Latin American countries…today it’s hitting the core, it’s no longer the periphery…look at countries like Italy…but it’s getting close to us”

“In 2008, we transferred debt from individuals to the states…now the years later, we’re starting to raise rates. We have to raise rates. It’s unhealthy to keep rates at zero. So someone is going to have to pay the price”

Nassim Taleb – 11/04/2018

This article first appeared on ValueWalk Premium