Hayden Capital letter to investors for the first quarter ended March 31, 2018.

Q1 hedge fund letters, conference, scoops etc

Dear Partners and Friends,

Well, that was an interesting end to the quarter. Trade wars, Presidential tweets, administration shake-ups… the markets hate uncertainty, and this quarter delivered it in spades. Much of this is meaningless to us, given our 10-year investment lens. However, these events certainly cause volatility in the short-run, often driven by those without the luxury of the time horizon we have, who are trying to “trade around” it.

Whenever these events occur, I sit up and take notice. Not over the tweet storms coming out of the White House – but because it’s more likely some of the businesses in our research pipeline will get mispriced. It’s exciting times when I can get off my butt and finally put some capital to work.

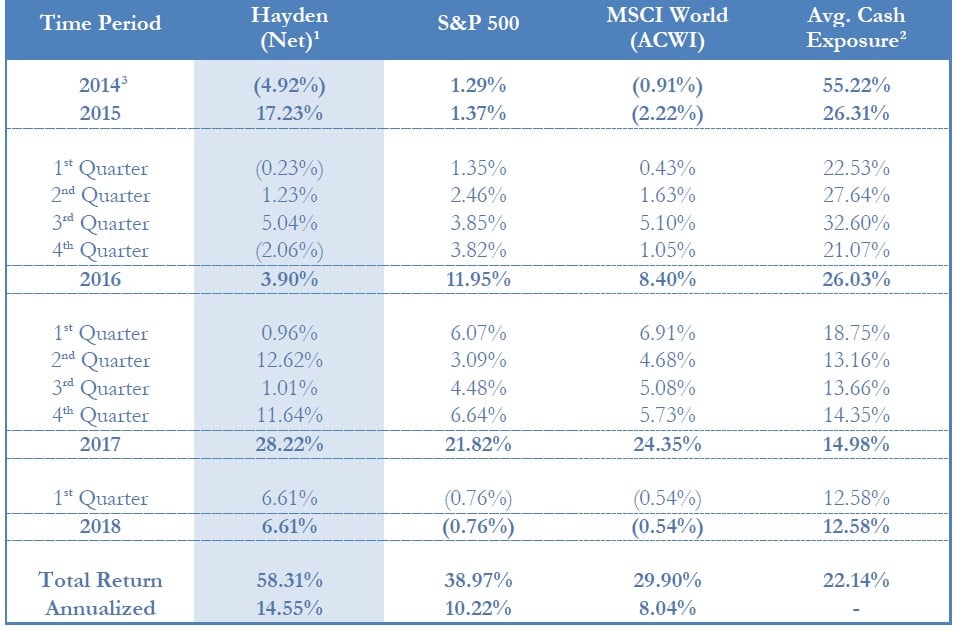

In this backdrop, our portfolio ended the quarter up +6.6% (net of fees) and carried one of the lowest cash balances since inception, due to the purchase of a new investment. Comparatively, the S&P 500 and MSCI World Indices lost -0.8% and -0.5%, respectively during this period.

Since inception, our portfolio has compounded at a rate of +14.6% annually (net of fees), versus +10.2% for the S&P 500 and +8.0% for the MSCI World Indices. Our average cash holdings during the quarter was 12.6% of the portfolio.

Not All Margins Are Created Equal

Over the last few years, I’ve become surprised at how few investors do the deep work necessary to understand the unit economics behind a business’s published financials. Or rarer still, the individual unit economics for each line of business. Yes, the company probably won’t give you the exact KPIs, so you won’t have the exact numbers the company’s own strategy team is looking at. But it doesn’t mean you shouldn’t try right? I personally suspect getting into the ballpark is already a significant edge, especially since most public markets investors don’t even try swinging.

The risk of failing to do so, is it leads many investors to think that 10% y/y growth at one company, is just as valuable as 10% y/y growth at another. Or equally faulty, that a low margin business is always worse than a high margin one. They fail understand the “why” behind these numbers.

For example, lets look at two types of margin profiles: what I’ll call the “reinvestment” scenario, and the “pricing power” scenario.

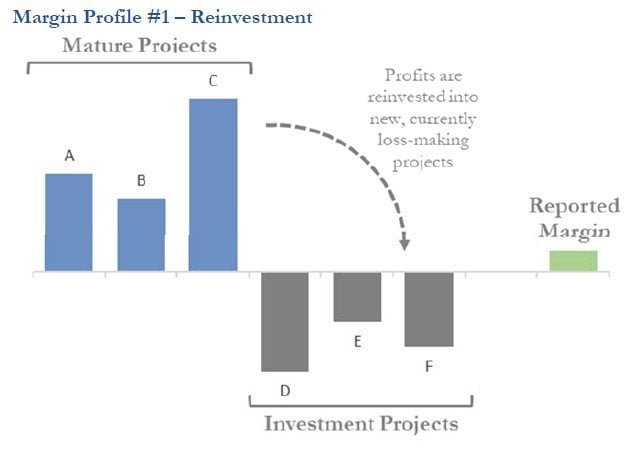

In the reinvestment scenario, a company is taking profits from highly profitable lines of business, and investing them into newer lines of business. This makes the overall margins seem very low, or even negative.

For example, imagine a real estate developer who is taking profits from their exist portfolio of 5 properties, and using it to develop a new apartment complex. During the first year, the developer is going to show very little profits. Materials, labor, permits, these all eat into the business’ cash flow while the new apartments are being built. It might even lose money and need to take on debt. But after a year or two, the project will finally start generating profits as new tenants move in, and the company’s overall margins will begin going up again. Then eventually, the profits from the now 6 properties will be used to build yet another apartment complex, and it starts all over again. The idea is that when the business is mature and no longer growing, the margins will be closer to that of Projects A-C (see below exhibit), rather than today’s reported margin. By breaking down the unit economics for the different projects and recognizing the different profiles of A-C vs. D-F, we can get a glimpse into what this “normalized” margin looks like.

Additionally, if the investments are smart, low margins may even be a positive sign of that the company is investing in its future. When investing in companies, the longevity of the cash flow stream is just as important as the absolute amount of annual cash flows, for a stock’s valuation.

Under the “Reinvestment” margin profile, the key questions are:

- Will the investment projects ever be cash flow positive?

- If so, how long will this take? What does the margin look like at maturity?

- If it’s unsuccessful, is management smart enough to shut it down? What are the signs to watch for, as indications of failure?

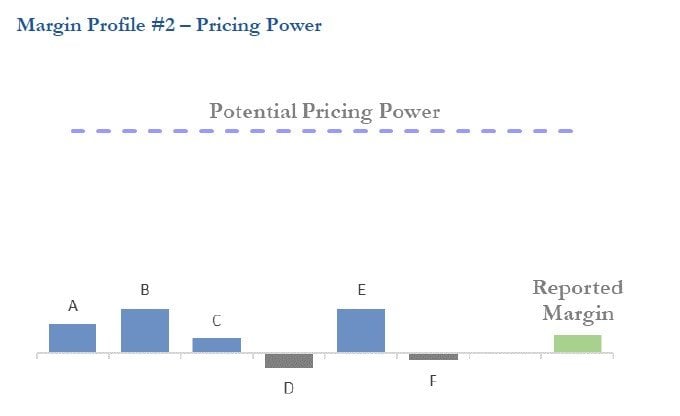

The second type of margin profile, is that of pricing power. The idea is that as customers start to depend upon a company’s products or services, the company has the ability to ask for more from its customers.

Sometimes, companies may even give away their products for free, hoping to get customers addicted to the service (for instance, software companies sometimes give free licenses to schools for this reason, hoping the students will become reliant and encourage their future employers to purchase licenses later on). It also keeps potential competitors away until the company has already “won” its market. After all, how do you compete with “free”? Once customers are hooked and can’t live without it, the firm will start to slowly raise prices.

We can see this today with many platforms, such as Facebook or WeChat, who eventually incorporate ads once users are sufficiently addicted. Amazon Prime is another notable example. Just a few days ago, Amazon announced it’s increasing the price to $119 a year. This is only the second price increase since the program launched 13 years ago (the first increase was in 2014, from $79 to $99 a year).

Note, this type of margin increase also tends to be riskier, as you risk alienating your customer. The company needs to be confident that the value it provides will far surpasses the price charged for the service.

We own both types of companies in the portfolio, and depending on the situation, one isn’t necessarily better than the other. But the questions to answer, and “signposts” to watch for are different.

Under the “Pricing Power” margin profile, the key questions are:

- Does the company actually have the ability to raise prices? How sticky are our customers, and how will they react?

- If the company has pricing power, why haven’t they already raised prices? What needs to change to alter their strategy?

- If they raise prices, does this give room for new competitors to enter the business?

- What will the additional profits from the price increase be used on?

- Will it be returned to shareholders, or invested to provide even more value to customers? If invested, how much value do these new projects actually provide customers relative to the price increase?

However, what if by raising the price, you can actually widen / increase the value for the customer (i.e. the Customer Value to Price ratio)? Such a price increase would actually accelerate the company’s growth (rather than slow it down, like Economics 101 would teach you).

So long as the company reinvests the higher cash flow from the increase wisely (like Amazon has done with video; LINK), it may attract even more new customers since the value from the new investments appeal to an even wider customer base.

Because of this dynamic, the most interesting companies are actually those that have both “reinvestment” and “pricing power” characteristics. You can get “double benefits”, as price increases give the company more cash flow to invest, which speeds up the growth rate, and in turn generates even more cash when those projects mature. We can see this with Amazon Prime for example, and them investing in ever-faster shipping speeds and video content selection. These companies will leave their competitors in the dust.

On top of this, the market usually doesn’t “look under the hood”, and can’t see past the current low-margin. It sometimes values them like any other permanently, structurally impaired, low-margin business. Investors who do the work though, can usually spot these differences, and buy the shares for cheap.

**

Recently, I came across Tom Colicchio’s cookbook, “Think Like a Chef” (LINK)4. It’s unlike any other cookbook I’ve seen before. What’s interesting, is that his goal isn’t to teach you recipes step-by-step at all. Instead, the book instead focuses of “techniques” and building a repertoire of skills that can be applied to any ingredient5.

It starts with the basics – roasting, braising, sautéing, etc., then shows how you can use those building blocks as the foundation to create something more complex. For example, roasted tomatoes from the first chapter are then used later on as the basis for a tomato tart. In a nutshell, it teaches you how to think in “frameworks” (sautéing an onion is very similar to sautéing a carrot), rather than simply handing you step-by-step instructions. Once you master the basics, the idea is you can encounter a brand-new ingredient and immediately know what methods / combinations of flavors will pair best with it.

I found this to be very similar to how I think about investing and learning about business models. Once you understand the key drivers of an e-commerce platform, for example, it’s very easy to see a brand-new ecommerce stock and pick out / focus on the 1 – 3 factors that matter. Everything else is just noise. Charlie Munger has a similar idea regarding multi-disciplinary learning and is why he talks about “mental models” so often. Without that “framework”, you wouldn’t know where to start.

This in turn, it got me thinking about how similar portfolio management is to the restaurant business. First, there’s thousands of restaurants in NYC, just like there are thousands of investment firms in the world. They all have the same goal – putting food into your hungry stomach / providing investment returns for customers. Both are very competitive fields.

Now, within these thousands of options, they all try to accomplish the same goal but in different ways. A restaurant may serve Italian, Chinese, Sushi, Japanese Izakaya, “New American”, “Old American”, or French cuisine. Some restaurants may serve tiny 3-star Michelin tasting courses at $300 a person (or what I like to call expensive vegetable foam…). Or it may serve $6 delicious tasting, halal mystery meat from a street corner.

Likewise, investment firms might specialize in low-cost ETFs, socially responsible investing, hedged portfolios, long-only portfolios, emerging markets, or US-only portfolios.

Secondly, when deciding on a menu or portfolio concentration, there isn’t a “right” answer. For example, some restaurants have a menu that’s 10-pages and 100 items long. Others have a simple, concentrated menu of 10 items, which they put all their effort into cooking superbly. I think the choice between managing a diverse portfolio vs. a concentrated portfolio is similar.

The key is to recognize these restaurants have different goals and are serving different needs. One is going for diversity of options / offering something for everyone, while the other is providing the highest quality and best tasting food po sible within its niche. Neither is necessarily the “right” answer or has a higher chance of success (they’re not even trying to accomplish the same goal anyways).

For us, our “success” is defined as providing the highest, most durable returns, over a full-market cycle. I’m very biased that our method of finding investments and way of structuring the portfolio is the best way to achieve that. But it’d be illogical for me to say our method is better vs. another firm’s method, if for example their goal is to provide steady, low-volatility, income-like returns in any market environment.

Rather, the probability of success is highly dependent on the “chef’s” personality traits and skillset. You wouldn’t want a diner chef to be cooking at that 3-star Michelin restaurant6. Or a classically trained Italian chef serving Malaysian food.

In both the restaurant business and the investment business, the key is to find a loyal set of customers who appreciate what you’re serving. Your offering will never appeal to everyone out there, nor will it be appropriate for them. The goal is to find core customers who encourage and support you, so that you can continually hone your chosen craft, keep improving the quality of the “menu”, and provide the best solution to what your particular set of customers are looking for7.

Portfolio Updates

Undisclosed Position #1: This quarter, our partners will notice a new investment in their portfolios (it’s our first new investment in over a year). We are still building the position, so I’ll refrain from publicly speaking about the opportunity in detail8.

However, I’ll note that this is a recent IPO, and is one of the earliest points in a company’s lifecycle that I’ve ever invested at before. The firm has been operating for over 8 years, still unprofitable, and faces intense competition from well-funded rivals (it’s currently neck-to-neck for the #1 spot).

While all of our research indicates that it has every “right to win”, with a clear path to monetization, it hasn’t proven this out yet. Investors tend to be the “show me” type and are waiting to give it credit. But within five years, I think it will be in a drastically different competitive position and investors will view it with a very different lens. We chose to participate earlier in the company lifecycle, because the risk-reward of the situation was too good to pass up.

In terms of valuation, it’s trading at a very large (even irrationally large, in our view) discount to its most comparable peer – even after accounting for the differences in business model, industry competition, ARPU per user, etc. In terms of relative valuation, this peer trades at 3x the multiple (or a “30-cent dollar”). This is particularly surprising, seeing as our company is growing 20% faster than its peer (we expect 40% CAGRs), in a more nascent market, and only in the beginning innings of monetizing its user base. Given this, we have a pretty clear idea of what “winning” would do for the stock’s valuation.

The [potential amount (i.e. margins)] x [runway (i.e. duration of cash flows)] for profitable growth is magnitudes larger, but the market is missing it since most investors are overly focused on the next few years of short-term competition and losses9. In terms of re-investment returns, I estimate the company is earning as high as 500% returns on its most profitable projects. Additionally, I expect the distribution of returns between low-performing and high-performing investments to narrow over time, as the company collects more data on its users and their habits. This enables them to invest / bid more accurately for projects, which provides greater selection and customer value, and in turn provides more data to hone the project selection process – thus completing a “data-driven” flywheel effect.

Shares dropped as low as -15% from its IPO price, and we were buying on this opportunity. But given its early stage, don’t expect this company to become one of our top positions anytime soon. Instead, I view it like investing in a Series B venture round – it has a real business model, proven financials, users who value the service, and a roadmap to profitability. But it hasn’t necessarily “won” yet10. Similar to venture investing, I plan to size the position small for now, and “double-down” as the company continues to hit our KPIs and prove that the thesis is on track11.

Once I’m comfortable with the position size, I’ll discuss the investment in more depth, in subsequent letters and/or write-ups.

JD.com (JD): There’s been renewed concern recently, about JD’s near-term margin profile for 2018-20. In the latest earnings call, the company guided to a 1 – 2% operating margin for 2018, which is below what the street had modeled12. The primary reason given for the slower margin expansion, is increased investment in logistics and technology capabilities. Investors took this as a sign of increasing competition from the likes of Alibaba, and thus shares have sold off over -20% since the call, reaching the lowest levels in a year.

The market’s bear case is: JD has to invest all this money back into the business, just to stay in place / defend market share. Competition from Alibaba has “woken up” to the JD threat, and is posing more of a challenge (for example, its recent $9.5BN acquisition of Ele.me to help in-source its logistics fleet; LINK). This year’s margin guidance is just the latest evidence of that.

Well, that all sounds scary… if we believed it was true. But we’re confident the incremental ~$2.8BN plowed back into the business over the next 3 years, isn’t just to stay still (i.e. “maintenance” investments or capex). Rather, we’re confident this capital will be used to enhance its lead in categories such as FMCG, and logistics delivery capabilities13.

For example, similar investments have drastically raised JD’s mind-share with China’s most affluent consumers in the last year. Recent surveys indicate as of end of 2017, close to 60% of Chinese consumers prefer shopping on JD.com vs. Alibaba’s Tmall14. In fact, Tier 1 city data is even stronger, with 68% of shoppers preferring JD over Tmall. What’s noticeable, is the large jump of 10% over the last year (from 50% to 60% overall), which coincides with increased investments in JD’s logistics capabilities and launch of new categories.

The negative is, that they have lost share with Tier 3-6 city consumers, where they’ve lost ~5% share in the last year. This indicates that there’s an increasing bifurcation in Chinese shopping habits – richer, urban, and more demanding customers prefer JD.com, while those less-affluent and value-conscious consumers prefer Alibaba15.

However, as China’s economy continues to expand, and GDP per capita grows 5-6% y/y, it will only be a matter of time before lower-tier residents have the same shopping habits as those in Beijing, Shanghai or Shenzhen16. Product selection, quality, and delivery speeds remain the top criteria – JD beats out Tmall and Taobao on the last two and is rapidly catching up on the first.

**

In terms of valuation, it’s important to note that we recently got indications of private market values for the two subsidiaries, JD Logistics and JD Finance. The company separated these businesses out of the core business over the last few years, and has been raising capital for these divisions externally.

We’ve been fortunate to have access to latest investor deck for JD Logistics, and can confirm the latest round was done at a $10.9BN valuation or ~$6.20/share. For JD Finance, we don’t have exact details, but the rumors are that the latest round is at a $20BN valuation or ~$5.60/share (LINK)17. The company has also made ~$3/share of investments in other strategic firms (VIPS, Bitauto, Yonghui, etc), and another ~$3/share of net cash.

Altogether, this equates to ~$18/share of total value, which lies outside of JD’s core retail business. Even though I typically don’t underwrite sum-of-the-parts based theses, I think it’s attractive that this equates to almost 50% of the stock’s value (shares are trading ~$36 as of this writing). This implies the Core Retail business is valued at only $26BN, for a company that will do $75BN in sales this year and growing at a 25-30% CAGR.

Even if we look at the entire market cap, it’s trading at trough multiples of 0.6x Price-to-Sales, and 0.25x Price-to-GMV. Just see the charts from Goldman Sachs below. It’s unfathomable that shares are now trading at valuations similar to what traditional Brick & Mortar stores trade at (some of which only grow slightly more than GDP)… despite growth rates 4x as high, and a massive secular tailwind from shifting demographics. The last time shares were at these valuations in 2016, there were rumors that the company was facing a liquidity crisis and may have trouble keeping the lights on (which is not the case this time). After the concerns passed, shares subsequently rose +150% over the next year.

Lastly, there is a possibility of a dual-CDR listing in China as early as this summer, with the first batch being the large tech companies (Alibaba, JD, Baidu, Netease, etc) (LINK). If it happens, this will likely provide a major catalyst for these low multiples18. As I’ve said before, my thesis is that many of these Chinese US-listed tech companies are trading at lower multiples than they should be, since the majority of their Chinese customer-base can’t invest in these foreign-listed shares due to capital controls, and US investors have never used these platforms (LINK).

JD.com Share Multiples

From Goldman Sachs, JD Research Report (Published April 24, 2018)

It’s as if Amazon were listed in China, US-based investors weren’t allowed to invest in it, and Chinese shareholders had never used the site19. What type of valuation do you think Amazon would get in that situation? For these Chinese tech companies, it’s the same situation, just in reverse.

The Chinese government is unhappy that its own citizens haven’t been able to participate in the growth of its most innovative companies, and is rapidly changing domestic listing requirements to fix that. Additionally, CDRs provide another avenue for Chinese to citizens to utilize their ever-growing pile of savings and discourages them from taking it outside of the country.

Currently, there are only a few options for households to invest their savings: 1) over-valued real estate, 2) sketchy and often unregulated “wealth management / peer-to-peer” products, 3) unproductive hard assets like art, gold, cash, etc, or 4) domestic A-share stocks, many of which are low quality and subject to manipulation.

Opening the door to these blue-chip (or in this case “red-chip”) stocks will help provide a more productive use of savings in society, and I anticipate demand for these shares will be high (at least at higher multiples than US-investors are paying today). There are even hints that the CDRs and ADRs will be fully arbitragable, thus ensuring the shares trade at 1-to-1 valuations20.

Again, I never underwrite our investments based on “multiple re-ratings” and are typically even allergic to such notions. However, this is a nice “free option” to have and likely to have a big impact if it happens. I’m surprised how few people are paying attention to this development. Needless to say, we’ve recently been accumulating shares at these levels.

Conclusion

In the last few years, I’ve had the pleasure of welcoming many new partners to the “Hayden Capital Family” – whom I’m excited to develop relationships with and to embark upon this investing journey together. I’ve mentioned in the past, that as we expand, we’ll be forced to raise our minimums to ensure our existing clients continue receiving the high-quality of service that they deserve.

Unfortunately, that time has come. Starting this quarter (Q2 2018) our minimum has increased to $100K per new client. Our new fee structure is 2% per annum for $100K – $250K relationships, and 1.5% per annum for $250K and above. Just like before, there are no performance fees associated with any of these fee tiers, so clients have a completely transparent fee structure from the outset. Terms for existing relationships will not change.

I’ve been asked a few times, why we don’t charge performance fees, when it has the added benefit of aligning the manager’s incentives with that of the client21. The truth is, I’m not necessarily against performance fees. Rather, I’m against what I view as the excessive compensation of this industry, for what far too often amounts to too little value-add in return. Research has shown that these additional fees don’t necessarily correlate to better research or performance. In fact, Bloomberg recently reported that almost half of hedge funds’ fees typically go to marketing & placement services (LINK).

That business model doesn’t quite sit right with me… Honestly, I’d rather operate with a low-cost structure, and pass these savings (50%!) back to our clients. I far prefer to operate under the Amazon (low-cost, highvalue) model, then the Louis Vuitton (brand & marketing centric, high-margin) model. I think our client-base would agree22.

The bulk of our resources should be devoted to research and generating what our clients are here for – durable, superior performance over a multi-decade time frame. So far, judging by our returns since inception, our partners are already benefitting from this decision.

So, whether it’s a fee-only structure, or a performance-only structure, I think the ability to charge both won’t last much longer. It’s inevitable that the industry’s fee structure will face pressure – I’d rather provide value for our clients today, rather than only when we’re forced to.

**

Recently I re-read, Phil Fisher’s book “Common Stocks and Uncommon Profits”. On this particular passing, one section of the book stuck out to me, which I hadn’t noticed before. On the subject of idea generation, he wrote:

“The first original idea for almost four-fifths of the investigations and almost five-sixths of the ultimate payout had come from [other fellow smart, able, investment managers]. Across the nation I had gradually come to know and respect a small number of men whom I had seen do outstanding work of their own in selecting common stocks… In many instances I might not agree at all with the conclusions of any of these men as to a stock they particularly like, even to the point of feeling it worthy of investigation… However, because in each case I knew their financial minds were keen and their records impressive, I would be disposed to listen eagerly to details they might furnish concerning any company within my range of interests that they considered unusually attractive for major appreciation.” – Philip Fisher, “Common Stocks & Uncommon Profits” (1960 ed.)

Those who know me, know that I’ve always said my best ideas were found via a “curated” group of fellow investors, whom I speak to on a regular basis. After all, it’s like having a group of 40 analysts working for you, for free, without the negative incentives associated with a Portfolio Manager – Analyst relationship. Likewise, when we have an “original” idea, it’s often bounced off the group after all research is complete and an opinion formed, to stress-test the idea23.

This doesn’t mean we can slack on research just because we heard it from an “reputable” investor. Rather it’s the opposite – we often need to do even more work to make sure we aren’t being biased and to deliberately mitigate any risk of group-think.

But given the thousands of public stocks in the world, this method remains one of the best returns on our time. I find it more valuable to spend resources on “carefully examining what’s under a well-curated group of rocks”, rather than spending the majority of time “turning over rocks.” It’s very interesting (and a bit validating) that someone as talented as Mr. Fisher had come to the same conclusion 60 years earlier.

It’s for this selfish reason, that I’m always open to grabbing coffee with fellow smart investors24 (okay, maybe not the only reason… I like meeting new people, hearing different viewpoints, and learning about industry trends elsewhere in the world too). For example, looking at my calendar over just the past 3 months, I had 37 coffee chats with individuals, or on average ~3x a week. Just like a good VC firm, I think of this as my proprietary “deal flow”.

I’m always learning something new from each conversation. By speaking to more people and taking in more data-points, I hope to put together the investment puzzle faster, and eventually return valuable insights to everyone who contributed25. By collaborating, we can all learn together and reach conclusions we couldn’t individually.

**

Over the next few months, I’ll be in Omaha for the Berkshire weekend in early May, ValueX Vail in late June, and Asia (Seoul, Hong Kong / Shenzhen, Singapore) in late July / early August. If you would like to grab coffee in any of these locations or anytime you’re in NYC, please drop me an email. Besides the reason above, I truly enjoy meeting with smart, passionate individuals from diverse backgrounds.

While in Omaha, I’ll also be hosting an Emerging Manager “Round-table” discussion with my friends at Overlook Rock too. If you manage an investment firm and am interested in attending the event, please let me know. I look forward to meeting many smart investors over the course of the weekend.

Similarly, we’re always open to new, thoughtful partners who appreciate our investment approach. If you know someone who you think would be a good fit for our strategy and Hayden Capital, please have them reach out. I’d be happy to meet in Omaha, Asia or NYC to learn more about their interests.

As always, I can’t thank our partners (both new & existing) enough for placing their trust in us. I strive uphold the values I’ve outlined, and continue to build a differentiated, value-add firm, for my partners every day.

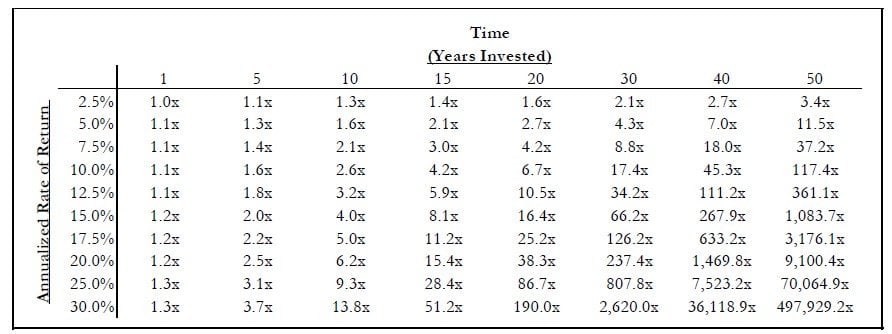

With that, I’ll end with this lovely table. As my partners, I hope you’ll aim to be on the right-hand side of the chart… and as your manager, my job is to bring us closer to the lower-end of the chart. When these two factors are combined, it’s what gives us the ability to generate some truly outsized returns.

Sincerely,

Fred Liu, CFA

Managing Partner

See the full PDF below.

{kind=link}