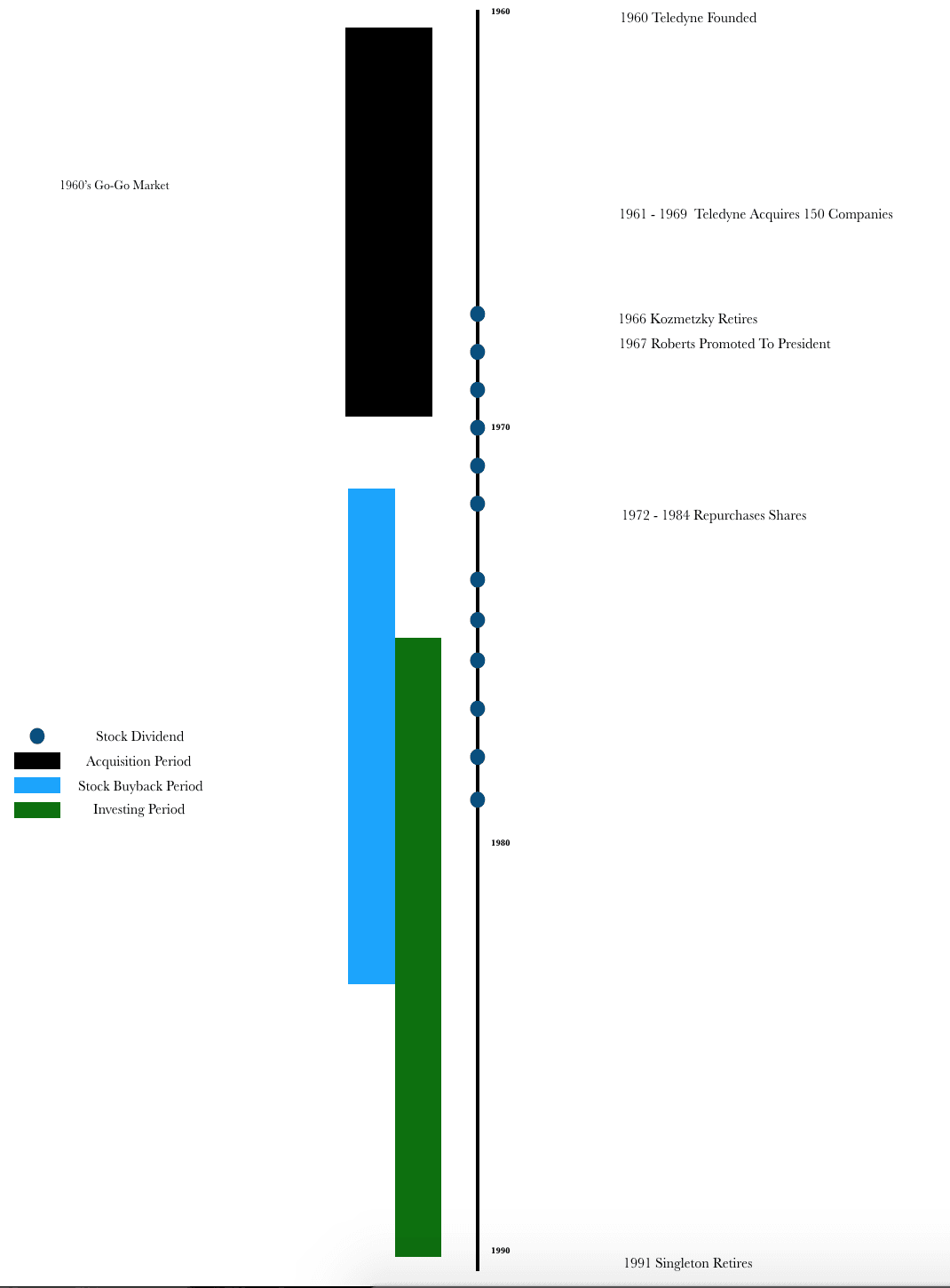

In the summer of 1960 an engineer and educator teamed up to launch what would eventually be known as one of the greatest conglomerates in business history. The duo turned an initial investment of $450,000 into an enterprise that generated annual sales of over $450 million while acquiring over 150 operating businesses. Dr. Henry Singleton was the engineer, Dr. George Kozmetsky was the educator, and Teledyne was the company.

Q1 hedge fund letters, conference, scoops etc

For value investors, Dr. Henry Singleton needs little introduction. His track record and decision making are consistently revered as an example of one of the all-time greats among capital allocators. Notable investors such as Seth Klarman, George Soros, and Charlie Munger have all mentioned him from time to time as a figure to study. Even Warren Buffett is said to have studied Singleton extensively.

“Henry Singleton has the best operating and capital deployment record in American business…if one took the 100 top business school graduates and made a composite of their triumphs, their record would not be as good as Singleton’s – Warren Buffett, 1980.

In this post, we will explore the history of Teledyne and what lessons can be learned from Dr. Singleton’s style of capital allocation.

If you read Henry Singleton’s accomplishments prior to the start of Teledyne, you would swear he would steer nowhere near a business career. Growing up with a disposition towards math and science, Singleton attended MIT where he earned his Ph.D. in electrical engineering. Singleton’s brilliance around math was so evident that in 1939 he was awarded the Putnam Medal, an award distinguishing the top mathematic student in the country. Aside from excelling in academia, his hobby of chess allowed him to excel to the ranks of only 100 points shy of a grandmaster level. After completing his Ph.D., he immediately entered research doing a few short stints at General Electric Co and Hughes Aircraft. It wasn’t long before he was recruited to Litton Industries where he invented a guidance system for commercial and military aircraft. Singleton excelled at Litton, but it was evident after being passed up for a leadership position that his career there had an enviable ceiling.

In July of 1960, Singleton decided it was time to venture out on his own. He and another Litton Industries colleague by the name of George Kozmetsky scraped together an initial investment to form Teledyne. In the 1960’s American business was in an interesting phase. WWII had created a catalyst for new technologies and industries. Most of these businesses were no longer in the “startup” phase, but profitable enterprises. Owners of these companies were either looking for capital to expand or a new owner so they could retire. Singleton and Kozmetsky recognized the growing importance of digital semiconductors and used that as a launching point for their company. With $450,000 in capital, the duo started by acquiring three small electronic companies. This base of three companies allowed them to secure a naval contract successfully.

Henry Singleton And Teledyne: Acquisitions

Singleton did not waste time. In just a year after starting, Teledyne became a public company. Whether Singleton foresaw the boom of the Conglomerate age or just had lucky timing, the fact that Teledyne was public and on an acquisition spree of diversified companies put the company in prime position during the Go-Go era. The Go-Go era for conglomerates was a dream. Conglomerates were a favorable asset among investors and their acquisitive nature created a somewhat self-fulfilling prophecy. Conglomerates saw higher valuation multiples on their stock which allowed them to create an arbitrage opportunity when buying other companies. Using their own stock, conglomerates would go out an acquire a new business only to see the new earnings of that company elevate their own stock price even more. Like other conglomerate managers, Singleton saw his stock as an inflated currency that allowed him to scoop up operating businesses in a favorable manner. Rather than shelling out cash, Singleton used Teledyne stock to acquire these businesses and expand operation income. However, even with a high flying currency at his disposal, Singleton was disciplined in his spending. He never paid more than 12 times earnings and chose to acquire profitable, growing companies as opposed to turnaround situations.

In 1966, Singletons partner and cofounder, Dr. George Kozmetsky, retired from Teledyne, taking up an opportunity to serve as the Dean of the University of Texas Business School. The departure of Dr. Kozmetsky put Singleton in a somewhat hefty role of carrying out operations and capital allocation. Fortunately, a year later, Singleton found a solution in his acquisition of Vasco Metals. Singleton spent $43 million to acquire the company and with it came George Roberts. Roberts took over the role of President for Teledyne, taking on the day to day operations of the company. The addition of Roberts led Singleton to take on the positions of CEO and Chairman with a focus on what he seemed to be doing best – capital allocation.

As oppose to consolidating operators into Teledyne post-acquisition, Singleton and Roberts focused on keeping them independent. Singleton believed people were key to business and they should be given autonomy and freedom to do their job well. Both Singleton and Roberts liked to keep companies small, with the philosophy that smaller operators allowed better opportunity to identify problems and generate greater returns. In fact, many of Teledyne’s acquisitions were of companies with no more than a few million in revenue. Once a new company was purchased by Teledyne, the manager was given extreme ownership to produce results for his operations. As long as the manager hit his goals, Singleton and Roberts stayed out of their business.

Singleton did impose some factors on the businesses he acquired. Returning capital to headquarters was of the most important factor. Compensation for managers was structured to award cash flow. The “Teledyne Return” was the benchmark metric, calculated by taking the average cash return and profit (as opposed to just profit which doesn’t always result in actual cash). Teledyne instructed it’s management to grow margins and keep excess spending low. Any new spending above $5,000 was sent to headquarters for approval. Additionally, management was given a firm 20% hurdle rate for return on assets to justify any cash that was not returned to headquarters. From time to time, Singleton was criticized for starving his operating businesses of necessary capital expenditures. His expectation of management was that operations should improve from ingenuity as oppose to throwing cash at everything. Overall, Teledyne operated with a highly decentralized structure. Headquarters took care of taxes, legal and capital deployment while leaving operators the independence to hit their goals in their own way.

The acquisition binge carried out by Singleton was of great success. From 1961 to 1971 Teledyne’s Sales grew from $4.5 million to over $1.1 billion, a 244.4 times increase. The net income of the company went from $100,000 to $32.3 million, a 555.8 times increase. Earnings per share grew 64.8 times from $0.13 to $8.55.

Stock Repurchases

As more conglomerates deployed the tactic of acquiring operators with their shares as currency, demand for opportunity drove up pricing. Being a stickler for value, Singleton refused to chase higher valuations. In 1969, Singleton and Roberts decided to wind down their acquisition machine. Up to that point, Teledyne had acquired over 150 companies that were generating quite the amount of cash flow.

From 1969 to 1972 Singleton searched for ways to redeploy all the cash that was piling up on Teledyne’s balance sheet. Ultimately Singleton concluded that the best investment opportunity was in Teledyne’s stock itself. Thus began what was and still is considered one of the most aggressive buybacks of corporate history. As Charlie Munger put it; “No one ever bought in shares as aggressively.”

In October of 1972, Singleton launched his first tender offer for one million shares at $20. As he tells it:

“In October, 1972, we tendered for one million shares and 8.9 million came in. We took them all at $20 and figured it was a fluke, and that we couldn’t do it again. But instead of going up, our stock went down. So we kept tendering, first at $14 and then doing two bonds for stock swaps. Every time one tender was over the stock would go down and we would tender again, and we would get a new deluge.”

Over the buyback period, Singleton deployed over $2.5 billion on purchasing Teledyne’s stock. Over a 12 year span, the company purchased a staggering 90% of outstanding shares while achieving a 42% compounded annual return for shareholders.

Singleton didn’t rely solely on the use of cash for the buybacks. Teledyne bonds were swapped for shares on four separate occasions, capitalizing on investors hunger for fixed-income assets at the time.

Ultimately, Singleton proved to be trailblazer launching the buyback tactic when it was highly unpopular on Wall Street. Singleton saw it a more advantageous way to return capital shareholders as a cash dividend would have been heavily taxed.

Stock Dividends

Despite Singleton’s despise of issuing traditional cash dividends, he did, in fact, allow Teledyne to issue stock dividends. In Henry’s belief, a stock dividend would allow the investor to choose when he would assume the tax liability based on his timeline for selling the shares. From 1967 to 1967 to 1979, Teledyne issued stock dividends with yields anywhere from 3% to 10%.

Investing

During his short experience at General Electric, Singleton spent time studying the business model of the company. He concluded that for a corporation to grow with a superior financial base, it needed to have some play in a financially oriented institution. Putting this plan in motion, Singleton acquired 52% of the insurance company, Unicoa Corporation in 1968, his first move towards controlling financial oriented institutions. He would go on to acquire several other insurance operations, making the companies an integral part of Teledyne.

In 1974 the insurance operations ran into a problem. Citing a large miscalculation in the insurance malpractice underwriting, Teledyne’s insurance companies were facing disaster. Preparing for the inevitable, Singleton liquidated all of the insurance portfolio investments to hold only cash. Luckily the disaster never struck, but a new problem arose – what to do with all that cash? It was at this time that Singleton took on the role of portfolio manager. Just like during his period of acquisitions, and share buybacks, Singleton sought to deploy cash in a value oriented manner. He quickly moved into highly concentrated positions of both conglomerates and insurance, both businesses he knew well. He also was not afraid to take a large position in a troubled company. When his former employer Litton, fell into trouble, Singleton put 25% of his entire equity portfolio into Litton. As he put it;

I felt Litton was a sound investmet,” Singleton says. “It’s good to buy a large company with fine businesses when the price is beaten down over worry about one problem.” (He refers to Litton’s costly and protracted shipbuilding fracas with the U.S. Navy) He adds “Litton’s problem was not a general one but an isolated problem—as ours was with Argonaut Insurance. To me it was hard to believe the heads of a $3 billion or $4 billion business would not be able to handle one business problem.”

Singleton did not stop there… He found that investing in bargain stocks presented greater returns then plowing cash back into Teledyne operation units. He also preferred the value premium in buying individual pieces of publicly traded companies as opposed to acquiring the entire company;

“There are tremendous values in the stock market, but in buying stocks, not entire companies. Buying companies tends to raise the purchase price too high. Don’t be misled by the few shares trading at a low multiple of 6 or 7. If you try to acquire those companies the multiple is more like 12 or 14. And their management will say, “If you don’t pay it, someone else will.’ And they are right. Someone else does. So it is no acquisitions for us while they are overpriced. I won’t pay 15 times earnings. That would mean I would only be making a return of 6 or 7 percent. I can do that in T-bills. We don’t have to make any major acquisitions. We have other things we are busy doing. As for the stocks we picked to invest in, the purpose is to make as good a return as we can. We don’t have any other intentions. We do not view them as future acquisitions. Buying and selling companies is not our bag. Those who don’t believe me are free to do so, but they will be as wrong in the future as they have been about other things concerning Teledyne in the past.”

To some, Singleton looked sporadic in his moves. To many outsiders, it seemed inappropriate to starve Teledyne’s businesses of necessary R&D and Capital Expenditure funds to build a robust equity portfolio. However, Singleton stuck to his principles of allocating capital where he saw the most value potential. He prided himself on staying flexible and doing what he thought was best at any given time;

“I know a lot of people have very strong and definite plans that they’ve worked out on all kinds of things, but we’re subject to a tremendous number of outside influences and the vast majority of them cannot be predicted. So my idea is to stay flexible.” To the BW reporter, he explained himself more simply: “My only plan is to keep coming to work every day” and “I like to steer the boat each day rather than plan ahead way into the future.”

Overall, Dr. Henry Singleton produced an astonishing track record during his tenure. When Teledyne stock traded at a premium, he used it as currency to acquire cash producing assets. When Teledyne stock traded at a discount, he invested in the value by deploying cash from operations to buy back shares. He gave operators independence and the autonomy to hit goals on their own but provided systematic frameworks that would ensure capital was redeployed in the most efficient manner. When he managed the equity portfolio, he bought not what was in style but what was value oriented plays with low margins of error. A dollar invested with Singleton would have grown to $180.94 at his retirement, making him one of the greatest capital allocators to ever exist.

Sources:

Thorndike, W. N. (2012). The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success. Boston, MA: Harvard Business Review Press.

Roberts, G. A., & McVicker, R. J. (2007). Distant force: A memoir of the Teledyne Corporation and the man who created it. Place of publication not identified: Publisher not identified.

The Singular Henry Singleton by Robert J. Flaherty, Forbes (July 9, 1979)

Article by Carter Johnson, Finbox.io