ESG and Financial Performance: Aggregated Evidence from More than 2000 Empirical Studies

Deutsche Asset & Wealth Management

University of Hamburg

Alexander Bassen

University of Hamburg; University of Reading – ICMA Centre

October 22, 2015

Journal of Sustainable Finance & Investment, Volume 5, Issue 4, p. 210-233, 2015, DOI: 10.1080/20430795.2015.1118917

Abstract:

The search for a relation between environmental, social, and governance (ESG) criteria and corporate financial performance (CFP) can be traced back to the beginning of the 1970s. Scholars and investors have published more than 2,000 empirical studies and several review studies on this relation since then.

The largest previous review study analyzes just a fraction of existing primary studies, making findings difficult to generalize. Thus, knowledge on the financial effects of ESG criteria remains fragmented. To overcome this shortcoming, this study extracts all provided primary and secondary data of previous academic review studies.

Through doing this, the study combines the findings of about 2,200 individual studies. Hence, this study is by far the most exhaustive overview of academic research on this topic and allows for generalizable statements. The results show that the business case for ESG investing is empirically very well-founded.

Roughly 90% of studies find a non-negative ESG-CFP relation. More importantly, the large majority of studies reports positive findings. We highlight that the positive ESG impact on CFP appears stable over time.

Promising results are obtained when differentiating for portfolio and non-portfolio studies, regions, and young asset classes for ESG investing such as emerging markets, corporate bonds, and green real estate.

ESG And Financial Performance: Aggregated Evidence From More Than 2000 Empirical Studies – Introduction

Close to 60 trillion US Dollars in assets under management – or 50% of the total global institutional assets base – are currently managed by Principles for Responsible Investment (PRI) signatories (PRI 2015a).

On the one hand, this development clearly demonstrates the commitment of financial markets toward environmental, social, and governance (ESG) criteria within investment decisions.

However, on the other hand, far-reaching shifts of mainstream investors toward embracing sustainable investment practices remain rather slow (Reynolds 2014; Busch, Bauer, and Orlitzky 2015; PRI 2015b).

Less than a quarter of investment professionals consider extra-financial information frequently in their investment decisions (EY 2015) and just about 10% of global professionals receive formal training on how to consider ESG criteria in investment analysis (CFA Institute 2015).

For many, the business case for responsible investing seems not obvious (Feri 2009; Cohen et al. 2011; Riedl and Smeets 2015). Still, the question of how compatible ESG criteria are with corporate financial performance (CFP) has remained a central debate for practitioners and academics alike for more than 40 years.

Though there are many positive examples for the ESG–CFP relation, researchers often claim that results are ambiguous, inconclusive, or contradictory (Aupperle, Carroll, and Hatfield 1985; Griffin and Mahon 1997; Rowley and Berman 2000; van Beurden and Gössling 2008; Hoepner and McMillan 2009; Revelli and Viviani 2015).

Scholars and practitioners are, in particular, undecided about the general effect including its measurement and durability (Barnett 2007; Devinney 2009; Wood 2010; Orlitzky 2011; Borgers et al. 2013; Orlitzky 2013; Reynolds 2014; Authers 2015).

Thus, there is an ongoing debate about the role and the impact of the financial sector on the natural environment and society (Weber 2014). In order to derive a more comprehensive picture, several review studies summarize primary ESG–CFP studies.

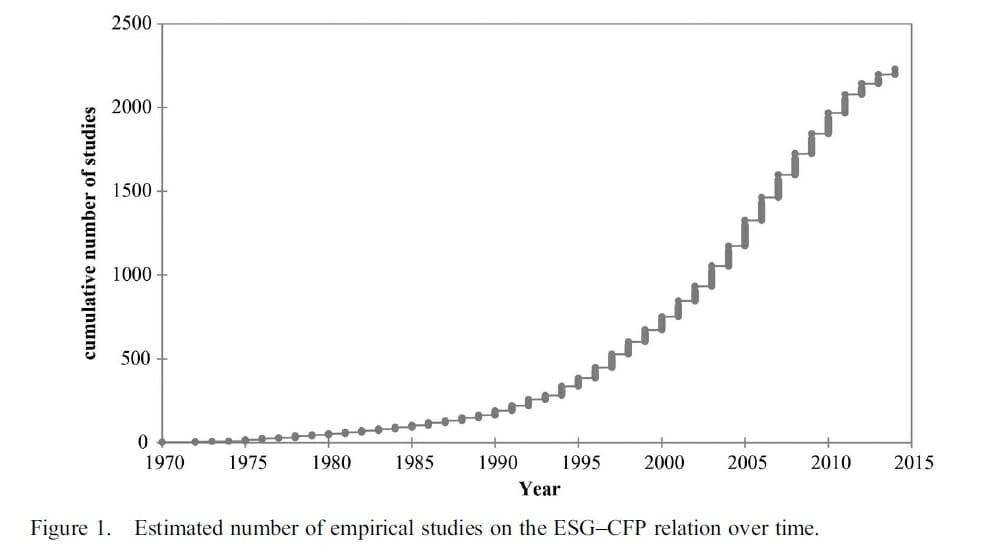

Yet, all these first-level review studies provide an incomplete picture. This study is the first effort to provide aggregated evidence based on more than 2000 empirical studies that have been released since the 1970s (see Figure 1).

We chose a two-step research method to analyze existing review and primary studies. First, we include findings from so-called vote-count studies. Vote-count studies count the number of studies with significant positive, negative, and nonsignificant results and “votes” the category with the highest share as winner (Light and Smith 1971).

These studies provide interesting insights, but are less sophisticated from a methodological point of view. The shortcomings are well documented in the literature.1 Second, we aggregate the findings of econometric review studies – so-called meta-analyses – to derive a second-order meta-analysis.

In total, 60 review studies – both vote-count studies and meta-analyses – with a gross number of 3718 underlying studies on the empiric relation between ESG criteria and CFP provide the starting point for our second-level review study.

When adjusted for overlaps, this figure reduces to a net number of more than 2200 unique studies. This still represents a dataset, which is 35 times larger than the average of analyzed primary studies in prior review studies.

In this study, we explain both systematic methods of summarizing extant research and present a research symbiosis of votecount studies and meta-analyses in the spirit of a best-evidence synthesis (Slavin 1986).

See full PDF here.