Third Point letter to investors for the first quarter ended March 31, 2020, discussing their structured credit portfolio.

Q1 2020 hedge fund letters, conferences and more

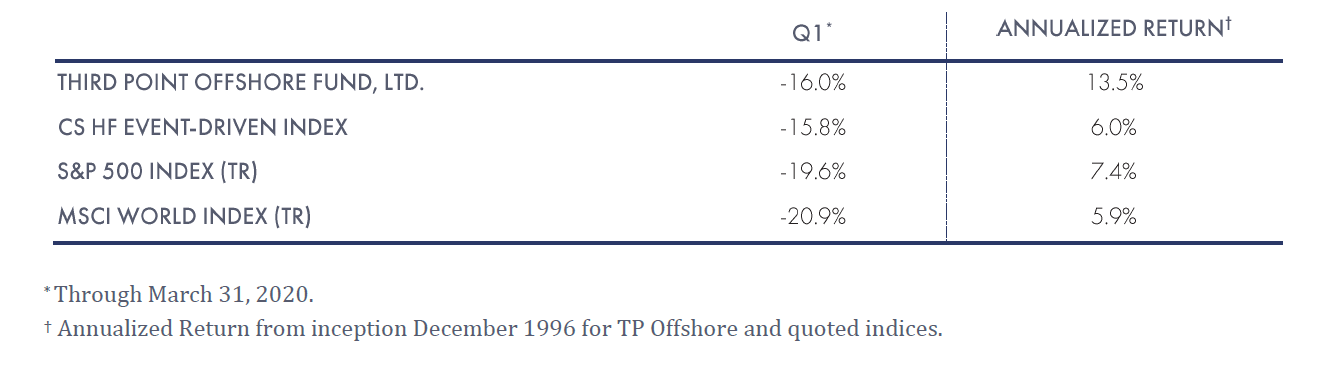

Third Point’s flagship Offshore Fund lost 16% in the First Quarter of 2020 during a period of unparalleled market turmoil. In this letter, we set forth what drove these disappointing losses, the significant shifts we have made to our asset mix, and our framework to invest in the current environment.

The COVID-19 pandemic is the worst global crisis we have faced, and the destructive impact is staggering both in terms of the loss of lives and livelihoods. We are grateful to the first responders and essential workers who are holding society together, particularly in our home, New York, which has been exceptionally hard hit.

Coming into this crisis, we were constructive on markets and the individual positions in our portfolio. We did not ascribe adequate probability to a full-blown global pandemic in our scenario analysis around COVID-19 nor to its blunt but necessary cure: a total economic shutdown in much of the world. When the pandemic exploded, our portfolio was thus susceptible to the sharp market decline for four key reasons: 1) equity exposures were at a beta-adjusted 65% net; 2) 45% of our long exposure was to non-US equities, which sold off more than the US; 3) we had a concentrated, high-conviction portfolio where the top 20 positions represented roughly 85% of NAV; 4) and, we had almost 10% of exposure in aerospace, airline, and auto-related names that substantially underperformed markets and caused over one-third of our losses in Q1.

With this positioning as our baseline, we reduced equity exposures by ~15% shortly after the sell-off began, primarily by adding hedges, to re-allocate capital to fresh credit situations we saw as asymmetric from a risk/reward perspective. We invested $2.2 billion in structured and corporate credit securities in mid-March, essentially doubling exposure. The modest losses we realized to rotate capital from equities to credit were nearly made whole within the month. We maintained most long equity positions, re-underwritten for a coronavirus scenario, and initiated several new equity positions in companies likely to benefit from changes in behavior as a result of widespread quarantines.

These shifts transformed asset allocation across our portfolio and have meaningfully changed the risk/reward profile of the fund. At the beginning of March, the book had exposure allocations of 70% net equity (65% beta-adjusted), 9% corporate and sovereign credit, 15% structured credit, and 10% other. By April 1, the portfolio was 58% net equity (48% beta-adjusted), 20% corporate and sovereign credit, 27% structured credit, and 12% other.

Stunning announcements of fiscal and monetary interventions and rescue financings have driven a sharp rebound in equity markets over the past few weeks. At the time we made most of our credit trades, neither the Fed nor Treasury had announced actions to combat the economic freefall; fear and capitulation in credit markets were at an apex. We believed at that time that given the extreme uncertainty, credit provided more asymmetric returns.

While we applaud much of the government’s action to “do whatever it takes” to provide a safety net to individuals and businesses affected by necessary social distancing and stay-at-home policies, we are dismayed by the Fed’s April 9 announcement that it will take the unprecedented step of purchasing high-yield bonds including “fallen angels” and ETFs. In our view, this does nothing to support an economic recovery but will simply prop up asset prices in the short-term and perhaps offer a reprieve to market participants who profited handsomely for years by using excessive debt to give the illusion of high returns and Sharpe ratios in risky strategies. In a free market, it is rightly the role of the many thousands of market participants to price credit risk. This holds issuers accountable through the robust restructuring process we have in place in America when companies are not able to meet their obligations.

The socializing of this risk is fraught with moral hazard on several fronts. Leveraged buyout players along with various leverage junkies including CLO, BDC, and Mortgage and other REIT issuers are offered a temporary reprieve, slowing the necessary steps these companies should take to restructure their operations and rationalize their capital structures. Responsible allocators are disintermediated from the process of providing liquidity based on thoughtful assessments of risk and thus allowing for the free market to assign the true cost of capital. We hope the Fed will realize that market interventions of this kind serve no long-term benefit and that they should limit their involvement in corporate debt markets generally, and particularly in high yield and mortgage securities. We also hope that when the US Government is left holding non-performing securities, it will observe rule of law as codified in securities law and the US Bankruptcy Code to provide for a market-based solution for restructuring debt and the reallocation of value from equity holders to creditors. Our memories of the handling of the Chrysler and GM bankruptcies where the government subordinated senior creditor rights to politically favored junior classes is still fresh. Meanwhile, after a decade, the GSEs still operate in a quagmire of receivership despite the government receiving its bailout funds and interest some time ago. The United States capital markets system is the most robust in the world and it is important that the government set policies that do not diminish market participants’ trust if the goal is to maintain market access and the lowest cost of capital for issuers.

One of the things that has distinguished our returns over the past 25 years is our ability to quickly respond to massive market turns and act rather than retreating. Our best years have been marked by taking advantage of the roughly once a decade credit cycles in which we have participated. Being positioned with flexibility, liquidity, and a broad toolkit should once again serve us well in a tumultuous period. Decades of decision-making have taught us that during chaotic periods there is never a clear roadmap and over the past month, we have drawn on our experiences in emerging from previous crises to develop a framework to navigate this challenging period and position the portfolio to capitalize on the opportunities emerging from it.

Q1 Performance And Opportunities

Activism

During Q1, the activist portfolio performed better than the market, down 18% on the long side with additional ballast from the hedges on each name, which in aggregate fell 22%. Ex-US names Prudential plc, EssilorLuxottica SA, and Sony Corporation struggled, while Nestlé SA, Campbell Soup Company, and Baxter International outperformed.

Our newest position, Prudential plc, lost 27% during the quarter, contributing 170 basis points to losses after accounting for financial sector hedges. Nothing about the price plunge since we announced our stake has materially changed our outlook for the company or its value potential and we added modestly to our stake near the lows. While we believed initially that the spread of coronavirus would have limited impact on the long-term earnings power of the company’s Asian business and might even drive increased sales and awareness of health and life insurance in the region, we underestimated how concerned markets would be about the ability of Prudential plc’s US subsidiary, Jackson National, to manage through both a sharp market decline and plunging interest rates. Jackson National is a great annuity franchise with significant value but despite this, shares currently imply a negative value for the business in excess of $20B, leading us to believe that Prudential is the most significantly undervalued security in our portfolio. This unfortunate market inefficiency has only made our case for separating Jackson stronger.

In the past few weeks, we have begun a constructive dialogue with management and the Board. Based on these conversations and the company’s recent public statements, we believe that they are considering all options to create more value for Prudential plc, including a full separation of Jackson National. While we appreciate the inherent complexity of such a transaction and the nature of the market environment, we believe that it is imperative that management work with urgency toward our shared goal of improved operations, optimized capital allocation, and creation of long-term value for all shareholders.

Last quarter, EssilorLuxottica faced a one-two punch of temporary eyewear store closures and a large manufacturing base in Italy, which was especially hard hit by COVID-19. We believe EssilorLuxottica is one of the best integrated consumer franchises in the world and expect that when the two companies are fully merged and its promise of manufacturing and retailing both lenses and frames is realized, it should be the dominant global eyewear business. This will be even more likely when its boardroom issues are resolved. When economic activity returns to some semblance of normalcy, sales should prove to be resilient given the significant exposure to non-discretionary vision correction products. We expect significant share gains given the company’s unique consumer proposition (frames plus lenses) and superior financial strength relative to its fragmented competitor base. Finally, we think the turmoil will create a greater sense of urgency within the organization to capture the promised synergies between the two businesses. The sharp sell-off gave us the opportunity to make some modest purchases near the lows, reflecting our confidence in EssilorLuxottica’s recovery.

While not immune from the current economic environment, Sony is in a strong financial position to weather the storm with a net cash balance sheet and large equity investments that could be easily monetized (~20% of market cap). Although some of Sony’s more cyclical businesses will likely face headwinds in 2020 (most notably Electronics and Semiconductors), Sony’s Gaming business is currently experiencing accelerating growth trends driven by the “stay at home” economy. Sony remains one of the cheapest large cap tech stocks in the world with market-leading positions in several growing end markets, trading at <6x LTM EBITDA and ~7x our estimate of 2020 EBITDA. Our view on intrinsic value of 11k yen per share is unchanged as few of Sony’s businesses are likely to feel long-term impacts from COVID-19.

Losses in Prudential plc, EssilorLuxottica, and Sony were balanced by better performance in three of our other large activist positions. Baxter, our largest holding, was down only 2.6% in Q1 as the company delivered solid 2019 performance ahead of expectations and resolved the accounting issues that arose last Fall. Its outlook in the coronavirus environment remains steady because Baxter manufactures critical medical equipment used in Intensive Care Units such as the Spectrum IQ Infusion System, IV solutions, the PrisMax and Prismaflex blood purification systems to treat acute kidney injury, and injectable drugs used in ICUs and across hospitals. Nestlé was down just 5% on the back of strong food sales. CEO Mark Schneider continued executing on his promised buyback program through the lows, showing his conviction about the company’s prospects in a recession scenario, which we share. Campbell Soup also benefitted from pantry stocking and excellent leadership by CEO Mark Clouse, who has transformed the company in just over a year. Today, we believe the company is in excellent hands with a sound path for long-term growth and, as we reorient the portfolio towards credit, we have exited CPB with an annualized return of 23% (vs the S&P 500’s -1.1% over the same period).

Fundamental and Event Portfolio

The fundamental and event equity book fell 28%, largely as a result of our sizable positions in aerospace names including United Technologies, Raytheon, Airbus, and Air Canada, and losses in IAA. Put simply, we got aerospace wrong and were not hedged adequately to protect against coronavirus-driven losses. United Technologies was especially hard hit in March because it was going through a three-way split up and held by event driven funds which were subject to forced selling. While we gain some comfort that half of Raytheon Technologies’ business is in the more stable defense sector and earnings will recover with both an eventual rebound in aerospace spending and scaling of the company’s GTF jet program, we expect the next few quarters to be especially challenging and so we modestly reduced the position.

Another investment that was hard hit during the quarter is IAA, a company that auctions damaged vehicles on behalf of insurance companies. IAA was spun out of KAR Auction Services in June 2019. We like the industry’s duopoly structure, pricing power, and high returns and are also excited about the opportunity for IAA to invest in the business, drive growth, and improve margins as an independent company. Management recently disclosed a strong profit improvement plan which targets a 30% increase in EBITDA over the next three years, excluding contributions from core business growth. As a result of COVID-19, traffic congestion, miles driven, and accident frequency are seeing dramatic one-off declines but we expect a recovery as the economy reopens and cheap gas and pent-up demand help get the consumer back on the road. The auto salvage industry has been resilient during past economic downturns and has grown revenue at a 10% CAGR over the last 20 years.

Credit/Privates/Other Performance

Losses were felt beyond equities across all asset classes in March. Our structured credit portfolio defended relatively well, falling less than 5% during the month amidst a violent sell off in March that drove some RMBS prices to 2010 levels. These modest losses point to the benefit of not using credit lines and margin to acquire structured credit, which both mitigated our downside and enabled us to act decisively when forced selling occurred. Corporate credit detracted modestly for the quarter as spreads blew out and we had some mark-to-market write downs in Pacific Gas & Electric and a small write-off of a long-held energy name. Lastly, our third-party valuation firm completed its routine quarterly pricing of our portfolio of private securities and we took a 10% write-down, which contributed approximately 1.4% of losses for the quarter. Having had several favorable monetization events that reduced our private company exposure to below 10% of total assets, we were optimistic about several sales or other liquidity exits in 2020-2021. Each of these private positions have the liquidity to weather upcoming economic weakness and should be able to access public markets or effectuate sales once economies and capital markets reopen.

Recent Portfolio Changes: A Shift to Credit

Last month reminded us of the value of having nimble asset allocation capabilities. A short window – roughly a week – opened to buy high grade corporate credit at the widest spreads since the GFC in 2009. We took corporate credit exposures from 9% to 20%, primarily in investment grade securities, which have outperformed high yield securities coming off the bottom. In structured credit, we nearly doubled exposure in March as forced selling created compelling opportunities in RMBS and consumer-linked securities.

Corporate Credit

In the first stage of a credit crisis, we typically see selling concentrated in high-quality names driven by forced selling due to leverage or redemptions. These are the most liquid parts of the market where it is easiest to raise cash, often with a smaller impact than trying to sell names that face actual fundamental impairment. In March, this familiar dynamic created a unique opportunity to purchase liquid assets from investment grade issuers that will be impacted by a recession but should be relatively insulated from the business shutdown. Our general template for evaluating these bonds is to assume that spreads recover to historically normal levels over the next 12–18 months as financial conditions stabilize. Many of our investment grade bonds have rallied sharply off the bottom and while there is still an attractive spread tightening trade we are now focused on other parts of the market.

As mentioned above, the Fed launched an unexpected program last week to include “fallen angels” and limited purchases of high yield ETFs in its coronavirus combat efforts. This program will impact the market in two important ways: 1) it expanded the universe of “haves” (corporates with potential Fed backing) to include future fallen angels. This will reduce the potential market impact from the enormous wave of fallen angel downgrades that are likely to occur over the next six months but it does not mean companies will not be downgraded or that they will not require absorption by the high yield market; 2) it will also marginally reduce the cost of capital for high yield issuers since having a new buyer of high yield ETFs should provide some market support but this should not be overstated – ETFs in aggregate represent a tiny fraction of the high yield market and purchases are further limited to 20% of eligible ETFs.

We believe that these initiatives may marginally support the market – albeit at a high moral hazard cost – but they will do little to stop the destructive forces unfolding in real world. The next wave of selling will be in lower quality bonds as fundamental credit concerns emerge with the sharp economic contraction, and redemptions and deleveraging continue. It is hard to imagine that the Fed will move to directly support high yield issuers; even in this environment, it would be politically unpalatable to bail out leveraged buyout (aka “Private Equity”) sponsors.

Credit cycles have become shorter in the past three decades and our structural advantage is an ability to quickly allocate capital to avoid being shut out. While the markets have been temporarily assuaged by the Fed’s eased liquidity, lowered capital costs for the upper tier of the US credit universe, and trillions in spending coming into the system, we would be foolish to ignore the fact that the global economy has ground to a halt. We believe the real world faces enormous challenges that are orders of magnitude greater than those faced in the GFC, where the consumer was the weak link. We entered this crisis with a much higher level of corporate leverage, slow growth, challenging DM demographics, and a polarized body politic. A massive slice of the economy has become “shadow banked” by private lenders who may see thousands of their credits move into workout in the next month. For these reasons, we believe opportunities in corporate credit will be plentiful in the next few years.

Structured Credit

Structured credit markets were first slow to respond to the pandemic. However, following a persistent equity selloff and increasing pressure on levered buyers, these markets repriced dramatically in March. In under three weeks, we saw a price decline in structured credit that took over nine months to achieve during the GFC.

The initial opportunity in March was driven by forced selling from leveraged entities like REITs and mutual funds who came under significant liquidity pressure from investor redemptions and margin calls. Some mutual funds were selling bonds bought six weeks earlier at par down 40-50 points to raise cash. Of the 40+ REITS with portfolios of mortgage and consumer-backed securities that are 5-10x levered, five asked for forbearance in March. Two REITs sold their entire non-agency legacy RMBS portfolio on an exclusive basis and Third Point was one of the first investors involved. We focused our efforts in March on opportunities in RMBS and consumer ABS because, unlike in previous market cycles, the US consumer entered this crisis with far less leveraged household balance sheets and more equity in their homes.

Seemingly unlimited monetary policy and the fiscal stimulus bill helped abate some of the panic selling at the end of March, but prices for structured credit are still down 20-40% from February. Borrowing from their 2009 playbook, the Federal Reserve reintroduced the Term Asset-Backed Securities Loan Facility (“TALF”) which will serve as a funding backstop for the issuance of eligible asset backed securities (ABS) issued on or after March 23, 2020 until September 30, 2020 where primary dealers can access funding for government backed ABS and consumer ABS including student loans, auto loans, static CLOs, and secondary CMBS AAAs. In 2009, TALF took three months to implement. It is important to note that non-agency RMBS is not included and funding only applies to newly created securitizations. In the last cycle, while investment grade assets compressed over one year, opportunities to invest in sub-investment grade structured credit with equity-like returns persisted for multiple years, which provided a substantial opportunity for Third Point.

As in corporate credit, investors typically sell senior cashflow, investment-grade rated bonds first. As government stimulus programs take hold, we believe shorter duration assets will rally and we can move into longer duration securities, which we expect will be a compelling, multi-year opportunity. We are constructive on government stimulus to relieve the immediate concerns for the consumer to make payments in addition to the various payment deferral plans for the coming months. However, over the next two to three months, we will see the direct impact of the global economic shutdown with increased payment deferrals and elevated corporate defaults in these bonds. We expect this will lead to a second wave of opportunity to invest in structured credit, particularly CMBS and CLOs — although we believe that it is currently too early to wade into these markets.

Looking Ahead

As worldwide shelter in place directives have taken root, “flattening the curve” successfully is essential to prevent worst case scenarios. Recent positive news out of the most hard-hit European countries who started quarantine before the US is encouraging but we clearly still have a long way to go before returning to a semblance of normalcy. The world is in a recession and growth has plummeted. Our base case scenario is that a return to “normalcy” will be structurally difficult and complex, with the likely recovery being shaped like a Nike swoosh, as some economists have described it. Today, we believe equity markets are expecting a much sharper recovery, the high yield market prices a more moderate recovery, and the mortgage market is trading as if recovery will be slow.

As we looked for threats to the global growth paradigm over the past few years, we consistently came back to the leverage and “free” money ballooning throughout the system as the biggest risk. Over the last decade, the world has binged on buybacks, unicorns, private equity dollars, easy loans, and return-chasing in an ultra-low rate world. This bubble is popping now too, and it will be painful for many investors and asset managers as things reset.

Jonathan Haidt, the NYU professor and co-author of The Coddling of the American Mind, has said that two positives are likely to come out of this period: anti-fragility for our school age children and personal reprioritization. We can imagine a host of changed behaviors – some short lived, and others more permanent. Many speculate about fundamental shifts in the way people consume entertainment, or use Amazon for all essentials, or prefer working from home to offices, or reverse urbanization trends, just to mention a few. We also believe, and hope, that the crisis will draw increased focus on the disparities in our country, illuminated by the disproportionate way the virus has affected different income groups. Let us hope that the result is an increase in compassion and a greater implementation of public-private partnerships to ameliorate inequality in our education, criminal justice, and healthcare systems.

These are deeply unsettled times, and our portfolio is designed to look through the valley of volatility and manic market sentiment. We benefit from having the ability to look across asset classes to find the best risk reward and most asymmetric returns. The value in our strategy has always been in its opportunistic ability to toggle between asset classes, sectors, and geographies with a speed not available to bigger organizations or those without such a broad toolkit. We are pleased with how we have shifted the portfolio and we have high conviction in our activist and other equity positions over the long run. As we have highlighted, we particularly like credit where we know that our coupons will be paid, and our instruments either repaid or exchanged for an equity stake that represents the full value of our par claims.

With at least two very difficult quarters ahead of us, we will need to stay focused on opportunities sprouting on the other side of the valley while navigating painful volatility. This is not the first time we have found ourselves a bit offsides when markets suddenly implode but we have always moved quickly to find the path out, typically through credit and other event driven strategies, a blueprint we are seeing emerge again.

Team Updates

Laura Lonardi joined Third Point in 2020 with a focus on structured credit. Prior to joining Third Point, she worked as an Analyst in the Whole Loan Trade Analytics Team at Goldman Sachs. Ms. Lonardi graduated summa cum laude with a B.S. in Applied Mathematics and a B.S in Statistics from Baylor University and received an M.S. in Finance from the Massachusetts Institute of Technology.

Sincerely,

Third Point LLC