Ben Strubel’s letter to investors for the month of December 2018, titled, “The US Economy Still Looks Good.”

Dear Investors,

The market frequently goes from periods of exuberance, ignoring any bad news and just focusing on the positives, to periods of anxiety, focusing only on the negatives. Right now, we are in a period where the stock market is obsessed with negatives, such as a potential trade war, a “hard” Brexit (the UK leaving the EU without a deal), a slowdown in housing in the US, a feeling that the US economic recovery has gone very long and will end soon, a fear the Federal Reserve may raise interest rates “too far.” The list could go on. I’ve written about some of these topics before. In this newsletter, I want to focus on two things – the length of the current economic recovery and my outlook for the economy.

Q3 hedge fund letters, conference, scoops etc

The US economy is like a three legged stool. (Countries that have substantial exports would have a fourth leg to their economic stool.) The economy is made up of three “legs”: consumer spending, government spending, and business investment. Each leg supports economic growth. Weakness in one area, or leg, can be balanced out by strength in another.

Consumer Spending

Consumer spending is the largest portion of the economy and makes up about 70% of economic growth. Included in this 70% number are pass-through government programs, such as Social Security, Medicare, Medicaid, CHIP, and so forth. These programs either give money directly to consumers (e.g. Social Security) or to service providers (e.g. Medicare payments to hospitals and doctors).

Right now, this area of the economy looks pretty good. Jobs have been steadily growing since the recession, and wages are starting to grow a bit as well. Additionally, Social Security is set to have one of its first inflation increases in several years. All of this means more money in the pockets of consumers.

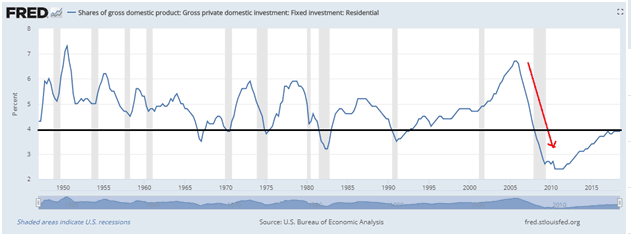

There is one area of weakness: housing. Changes to real estate tax deduction rules along with rising interest rates have slowed housing growth. It’s important to keep in mind, however, that housing now represents a much smaller part of the economy than it once did. At the height of the housing bubble, residential investment accounted for almost 7% of the economy. Today, as you can see in the graph below, it’s just below 4%.

It’s also worth noting that at today’s level, the housing market is still below previous housing cycle bottoms. (The black line on the chart is the top of today’s housing market which you can see is still below previous housing cycles.) Yes, that’s right. Housing hasn’t recovered enough to be back below the bottom of previous residential construction cycles. The weakness in housing today has much less effect on the overall economy. Given current household formation rates and the current supply of housing, we still need a lot of growth to get back to where we once were.

All in all, the consumer segment of the economy looks to be functioning fine with some minor weakness in housing as the only area of major concern.

Government Spending

Government spending (state, local, federal, and pass-through) is the next largest part of the US economy at 34%. Once we strip out pass-through payments, which are counted in consumer spending, however, state, local, and federal spending makes up about 17% of the economy. Like the consumer segment, the government segment is mostly good news. The budget cuts enacted several years ago as part of the Sequestration Agreement are gone, and government spending has risen.

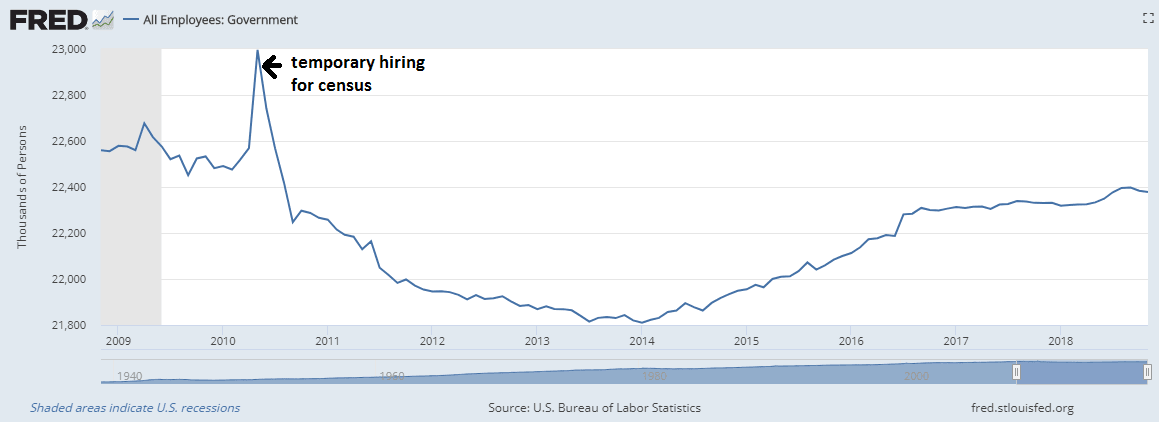

Additionally, over the last several years, government hiring is no longer acting as a drag on employment growth.

All in all, the government sector is now providing strong support to the economy.

You, of course, may disagree with how the government spends money. That’s fine. All we are saying here is that spending more money and hiring more employees adds to GDP. It may be worthwhile projects or not. For example, hiring 100 people to paint Donald Trump’s portrait every day will add to GDP. However, it’s not very worthwhile. On the other hand, building a new highway or airport will also add to GDP while providing additional economic value. We all have our own opinions on what programs count as “portrait paintings” and what are worthwhile projects like infrastructure.

Business Investment

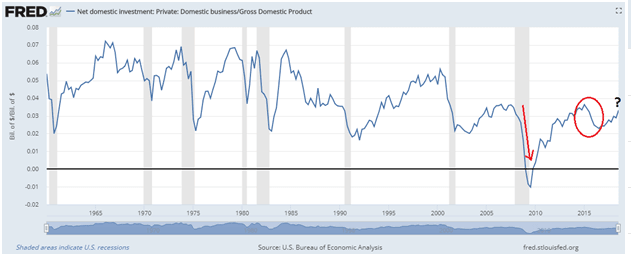

The final leg of the economy is business investment spending. This accounts for around 18% of the economy. This is the one area of the economy that is (and will likely continue) to slow. In the chart below, you can see the big drop in investment during the great recession (the red arrow). There was another dip around 2015 (the red circle) when oil prices dropped and energy companies severely cut spending.

With the recovery in business investment since the energy price recovery, it’s likely that falling oil prices will again curtail at least some spending. Also, the threat of tariffs will likely keep companies from aggressively expanding. If you aren’t sure what your costs for importing or exporting will be, then it is hard to decide where and when to open new facilities.

The good news is that a potential slowdown in business investment is easily managed by an economy where the other two legs of the stool are strong enough to hold extra weight.

When Will We Get a Recession?

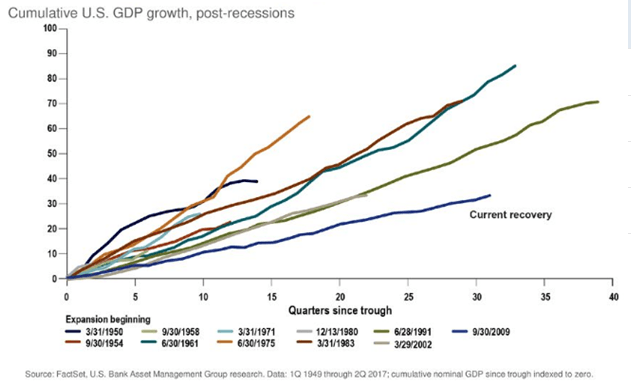

One of the stranger ideas is that economic recoveries have some sort of “sell by” expiration date. Currently, many people (market pundits, economists, etc.) seem to be deciding that the current economic expansion has gone on long enough and we are “due” for a recession soon. While it is true that the current recovery is one of the longest on record, it’s also one of the weakest. The chart below shows GDP growth after a recession.

If you are a firm believer in business cycles, then why wouldn’t our recovery peak when growth has reached a cumulative peak close to other recoveries?

I currently believe the best way to look at things is just to examine each piece of the US economy. We’ll get a recession when none of the legs of the stool are strong enough to hold it up. Right now, it looks like we have one leg (government spending) in great shape, another (consumer spending) in good shape, and a third leg (business investment) that’s a bit wobbly. Growth may slow but not enough to cause a recession or a huge stock market drop. We may have pockets of turbulence in the market like we have now, but once some of the recession and trade worries fade things should return to normal.

About Our Portfolios

The Capital Appreciation Fund and the Dividend Fund are innovative, investor friendly alternative to traditional actively managed mutual funds called a Spoke Fund ®. We can also customize portfolios for clients seeking less risk and volatility by including allocations to other asset classes such as bonds and real estate.

Spoke Funds are significantly less expensive and more transparent than a large majority of mutual funds. Both portfolios are managed for the long term using value investing principles. Fees for both portfolios are 1.25% of assets annually. That figure includes both our management fee and all trading costs. We try to minimize turnover and taxes as well in both funds.

Investor accounts are held in your name (we never take investor money) at FOLIOfn or Interactive Brokers*.

For more information visit our website.

*Some older accounts may be custodied at TradePMR.

Disclaimer

Historical results are not indicative of future performance. Positive returns are not guaranteed. Individual results will vary depending on market conditions and investing may cause capital loss.

The performance data presented prior to 2011:

- Represents a composite of all discretionary equity investments in accounts that have been open for at least one year. Any accounts open for less than one year are excluded from the composite performance shown. From time to time clients have made special requests that SIM hold securities in their account that are not included in SIMs recommended equity portfolio, those investments are excluded from the composite results shown.

- Performance is calculated using a holding period return formula.

- Reflect the deduction of a management fee of 1% of assets per year.

- Reflect the reinvestment of capital gains and dividends.

Performance data presented for 2011 and after:

- Represents the performance of the model portfolio that client accounts are linked too.

- Reflect the deduction of management fees of 1% of assets per year.

- Reflect the reinvestment of capital gains and dividends.

The S&P 500, used for comparison purposes may have a significantly different volatility than the portfolios used for the presentation of SIM’s composite returns.

The publication of this performance data is in no way a solicitation or offer to sell securities or investment advisory services.