In June 1950, Walter Bahr, a 23-year-old junior high school physical education teacher from Philadelphia, led the United States soccer team to a 1-0 victory over powerhouse England in the World Cup. Walter was team captain and player-coach. England was widely acknowledged as the best team in the world.

At dinner together the night before the game, England roasted the U.S. team. Raising their glasses they confidently toasted to what they said would be a crushing 8-0 victory. But with some luck and a U.S. goal just before halftime, Bahr launched a 25-yard shot that grazed the head of a diving teammate. The win is still considered the greatest upset in World Cup history.

As a kid, all I wanted to do was to play soccer for Penn State. I’d go to every game, including the one in the photo where Coach Bahr handed the game ball to PSU goalkeeper, Dan Gallagher in the late 1970s. Coach had little interest in a local kid but my big break came in a state cup match at the old Veterans Stadium in Philadelphia. Walter attended the game. I was named MVP. I later learned he made the selection. The following Monday I got a call to come to his office. That was a good day.

I was young, self-absorbed, hitting the books, thinking about girls and competing on field. Coach would pace the sidelines wearing that Italian cap. I knew nothing of his background then. Embarrassingly, I remember a teammate telling me about the England win and I was floored – how could I not have known. I’m up to speed now.

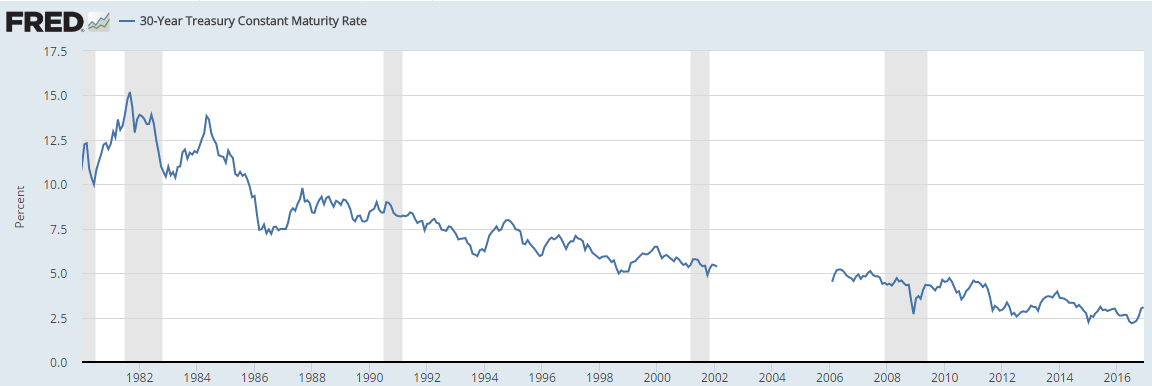

Coach made sure we focused on doing the little things right… consistently. You can imagine the farthest thing from my mind in 1981, at age 20, was what was going on in the bond market. Yet that year marked an important peak in yields. Interest rates spiked higher and the 30-year Treasury bond yield peaked that year at just over 15%.

Source: Federal Reserve Bank of St. Louis, FRED Economic Data

That was opportunity. Today we are at the polar opposite side of the secular cycle. Few were seizing that 1981 opportunity. Why? Because inflation was out of control and the thinking was rates would move even higher. Do you remember Volker’s “WIN” — whip inflation now buttons? Right.

Then, everyone was selling and should have been buying. Today, everyone is buying and should be selling. Crazy how that works. I’m pretty sure you’re fighting some of this headwind with your clients. One look at the year-to-date money flows and the winner? Bond funds and ETFs. Backwards thinking! Investment madness!

Why is this on my mind? I found myself in a soccer dream last night with Coach Bahr, wearing that odd Italian cap, pacing the sidelines. If the cap stayed on you did well, if he yanked that cap off, you soon found your rear end planted firmly on the bench. In my dream, the hat was coming off and he was rubbing his head… frustration on his face.

I’m not sure if it was my fear of being benched (maybe, as that happened more than I’d like to admit) or was it interest rates and that recent Italian Referendum “No” vote that’s been on my mind. I can see it in my mind now: Coach Bahr yanking that Italian cap off his head telling me not to miss the interest rates move and don’t be fooled by the Italian Bank head fake. Or else… bench. Something that holds true in real life. Game over…“Finito?”

OK, Coach. On it.

Several years from now, I believe we’ll look back and see that the secular low in yields was made in July 2016. As for the Italian Banks, and the global banking system for that matter, “whatever it takes” is shifted front and center once again. Keep a close eye on the days ahead.

One last point on the recent global macro event. It’s not just the Italian banks. With $2.5 trillion in total sovereign debt outstanding, Italy is the world’s third largest sovereign debt market.

Unlike Greece, Italy matters! The Italian economy is simply too big to be saved with repeated ECB and IMF bailout packages.

Courtesy of “The Daily Shot”

The Italians don’t seem like they’re in the mood for change. Not sure they are focused on getting better. It will likely be forced upon them. It will get worse. An Italian credit event will domino through Europe and on to the rest of the global economy. What the ECB does in the short term might help but it won’t in the long term. I’m not biting on the head fake.

Below you’ll find highlights from Bill Gross’s latest letter, a few cool charts including one on inflation and some concluding commentary. Grab a coffee… I hope you find the information helpful.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- Global Debt Crisis – “Red is the New Green” by Bill Gross

- A Few Fun Charts – Well, If You Can Call Inflation Fun

- Concluding Thoughts and a Personal Note

- Trade Signals – Investor Sentiment Too Many Bulls; Zweig Bond Model Sell; HY Buy; Equity Trend Evidence Bullish (posted 12-7-2016)

Global Debt Crisis — “Red is the New Green” by Bill Gross

Bill Gross’ Monthly Investment Outlook (December 6, 2016). Here it is… fun and worth the read:

I’ve got nothing against national anthems, and I wouldn’t kneel even if I was Colin Kaepernick. I just think as a country, “America the Beautiful” might have been a better choice for ours and that in some cases, some words of “The Star Spangled Banner” don’t ring true. A few countries’ anthems are, in fact, quite pleasing to my ear. “O Canada” has a beautiful melody and words to match, although you’d probably have to be watching hockey to hear it. Our “Star Spangled Banner”? For me – not so much. I can sort of see the “rockets’ red glare”, but it’s hard to sing and quite long – especially if you’re waiting for the kickoff. But like I said, I have nothing against it, except maybe the last stanza. Not the “Home of the Brave” part. Having spent two years in Vietnam, ferrying Navy SEALs up the Mekong Delta, I witnessed a lot of bravery. Not me. I was duckin’ quicker than Bill Murray’s gopher in Caddyshack. The SEALs though. Yeah – tough guys – very brave.

I quarrel however, with the part about “Land of the Free”. Free? For almost all of us – “yes” – but for 3+ million of us? Not really. Take a look at Chart I, and be honest if your eyes don’t bug out. More than any country on Earth – in total numbers, or as a percentage of the population, Americans are incarcerated, imprisoned – freedomless. Of course there’s a legitimate explanation for many of them, but what’s the reason for the rest? Restrictive laws that went too far and tied judges’ hands: California’s “three strikes and you’re out” legislation, for one, that was approved by voters long ago but is perhaps outdated now due to the growing acceptance of marijuana. The privatization of prison management and ownership is even more damning. “Orange Is the New Black” focuses on race and classism themes, but there’s more to the show than that. I’d affirm lead character Aleida Diaz when she says, “We a for-profit prison now. We ain’t people no more. We bulk items, sardines in a can.” I spent one night in a Danish pokey 50 years ago for intoxication, and it was 18 hours too long. We owe it to 1-2 million orange clad prisoners to clean up the system and give validity to our own national anthem.

Well, solving the “Orange Is Not Free” dilemma may take time just as the solution to a global debt crisis (now seven years running) may take even longer. It helps though to understand what the plan is in order to invest accordingly. While I and others have been critical of its destructive, as opposed to constructive elements, it is the current global establishment’s (including Trump’s) overall plan, and the establishment’s emphatic “whatever it takes” monetary policies are the law of our financial markets. It pays to not fight the tiger until it becomes obvious that another plan will by necessity replace it. That time is not now, but growing populism and the increasing ineffectiveness of monetary policy suggest an eventual transition. But back to the beginning which was sometime around 2009/2010:

How policymakers plan to solve a long-term global debt crisis:

- As in Japan, the Eurozone, the U.S., and the UK, central banks bought/buy increasing amounts of government debt (QE), then rebate all interest to their Treasuries and eventually extend bond maturities. Someday they might even “forgive” the debt. Poof! It’s gone.

- Keep interest rates artificially low to raise asset prices and bail out over-indebted zombie corporations and individuals. Extend and pretend.

- Talk about “normalization” to maintain as steep a yield curve as possible to help financial institutions with long-term liabilities, but normalize very, very slowly using financial repression.

- Liberalize accounting rules to make some potentially “bankrupt” insurance companies and pension funds appear solvent. Puerto Rico, anyone?

- Downgrade or never mention the low interest rate burden on household savers. Suggest it is a problem that eventually will be resolved by the “market”.

- Begin to emphasize “fiscal” as opposed to “monetary” policy, but never mention Keynes or significant increases in government deficit spending. Use the buzzwords of “infrastructure” spending and “lower taxes”. Everyone wants those potholes fixed, don’t they? Everyone wants lower taxes too!

- Promote capitalism – even though government controlled, near zero percent interest rates distort markets and ultimately corrupt capitalism as we once understood it. Reintroduce Laffer Curve logic to significantly lower corporate taxes. Foster hope. Discourage acknowledgement of abysmal productivity trends which are a critical test of an economic system’s effectiveness.

- If you are a policymaker or politician, plan to eventually retire from the Fed/Congress/Executive Wing and claim it’ll be up to the Millennials now. If you are an active as opposed to passive investment manager, fight the developing trend of low fee ETFs and index funds. But expect to retire with a nest egg.

That’s the plan dear reader, and President-elect Trump’s policies fit neatly into numbers 6, 7 and 8. There’s no doubt that many aspects of Trump’s agenda are good for stocks and bad for bonds near term – tax cuts, deregulation, fiscal stimulus, etc. But longer term, investors must consider the negatives of Trump’s anti-globalization ideas which may restrict trade and negatively affect corporate profits. In addition, the strong dollar weighs heavily on globalized corporations, especially tech stocks. Unconstrained strategies should increase cash and cash alternatives (such as high probability equity buy-out proposals). Bond durations and risk assets should be below benchmark targets.

On TV, “Orange Is the New Black” yet, in the markets, “Red” (in some cases) may be the new “Green” when applied to future investment returns. Be careful – stay out of jail.

Source: Janus Capital Group

A Few Fun Charts – Well, If You Can Call Inflation Fun

Chart 1 – Number of Days Before the Start of 5%, 10% and 20% Corrections

Here is how you read this chart:

- The top section shows the history of the S&P 500 Index from 1928 to present.

- The next three sections show the number of days prior to the start of a 5%, 10% and 20% correction. Think of this as a study of history. It is normal to get corrections in the markets.

- You’ll see that it has been 116 days without a 5% correction. The average number of days since 1928 was 50 days before a 5% correction occurred. In secular bull periods the average number of days was 84. In secular bear periods the average number of days was 31.

- You’ll see that it has been 210 days without a 10% correction. The average number of days since 1928 was 167 days before a 10% correction occurred. In secular bull periods the average number of days was 331. In secular bear periods the average number of days was 91.

- You’ll see that it has been 1955 days without a 20% correction. The average number of days since 1928 was 635 days before a 20% correction occurred. In secular bull periods the average number of days was 1105. In secular bear periods the average number of days was 486.

Source: Ned Davis Research

The current case of 1955 days without a 20% correction is more than three times the average of 635 days (1-3-1928 to 12-8-2016).

To this record number of days, join me and say, “Thank you, Misters Fed, BOJ and ECB.”

As you’ll see in the Trade Signals section, the equity market trend evidence remains bullish. To date, we have not witnessed a euphoric-like top but the last few weeks do feel really good. To which we are long and I’m happy. Keep front of mind that valuations are high and thus risk is high.

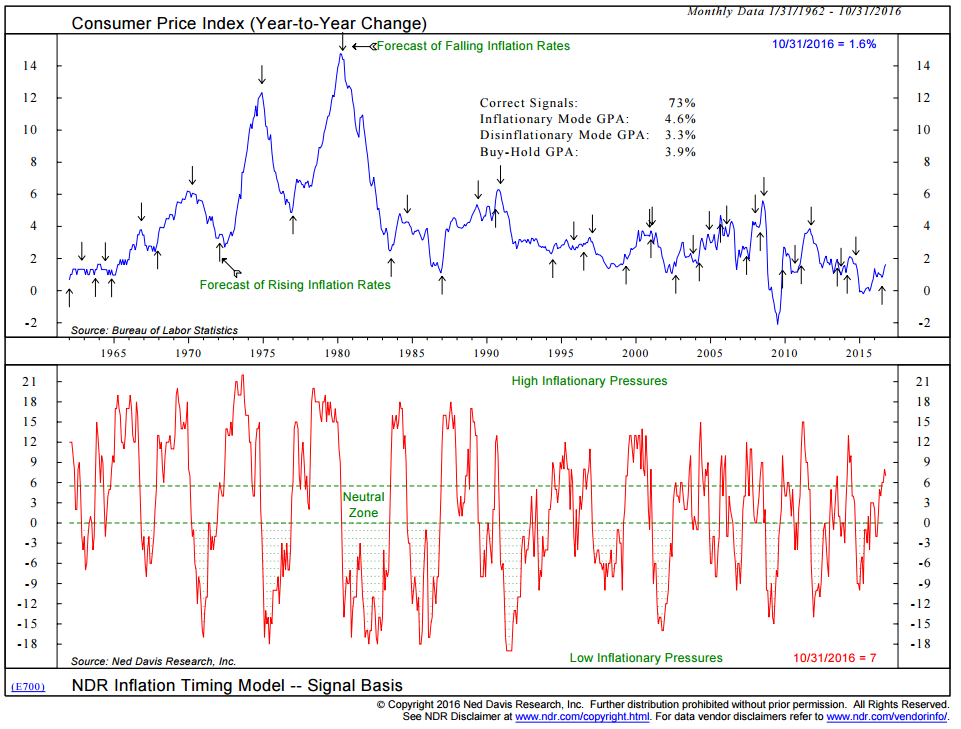

Chart 2 – Inflation

In the “we better keep an eye on inflation” camp, here is one of my favorite indicators.

Here is how you read the chart:

- The bottom section shows a “High Inflationary Pressures” zone and a “Low Inflationary Pressures” zone. Note to the far right the red line is in the High Inflationary Pressures zone.

- Also note the up arrows in 1972 and 1977. Good signals that said get out of bonds.

- Also note the down arrow in 1981 and recall the secular high in the 30-year at just over 15%. What an outstanding bond market buy signal.

- Lastly, note the recent up arrow in 2016. Will it one day look as promising a signal as that 1981 signal? Time will tell.

Source: Ned Davis Research

I’ve been hitting the bond subject hard the last few months and for good reason. I’m on record saying that the biggest bubble of all bubbles is in the bond market… here, there and everywhere.

Inflation is on the rise. That spells more trouble for the bond market. Only if you are unprepared. My two cents below.

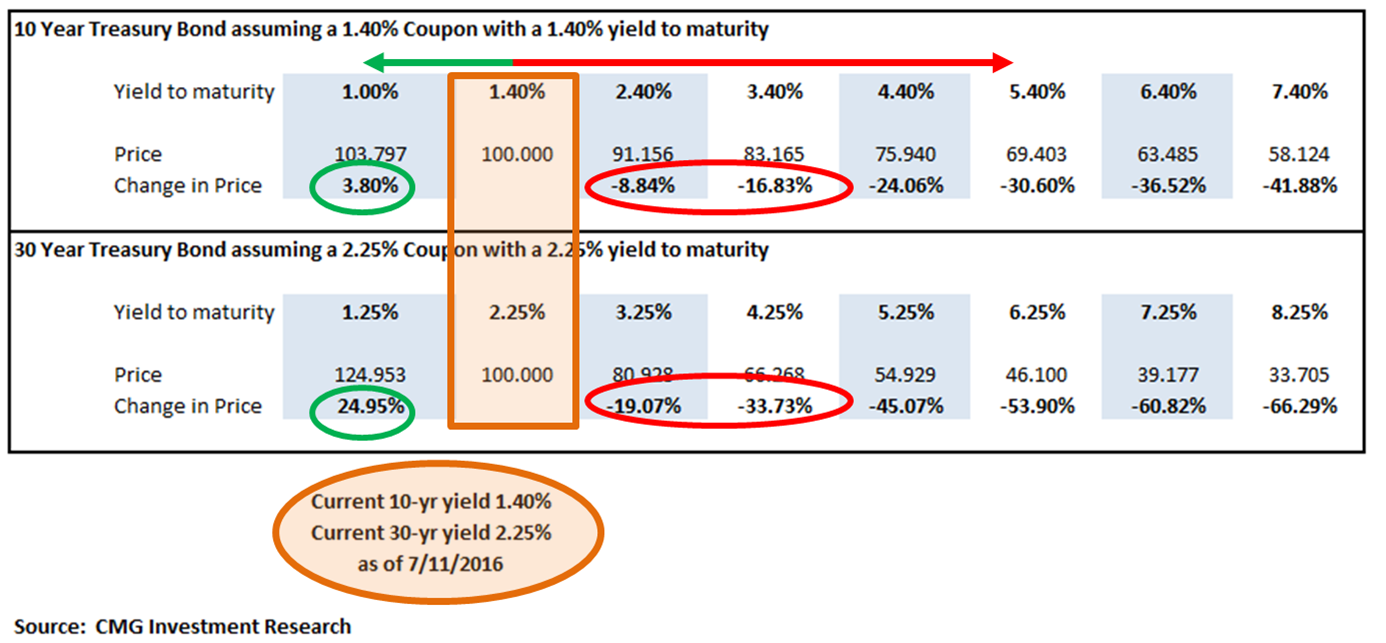

Chart 3 – Bonds Lose Value as Rates Rise

Here is how you read this chart:

- The yield on the 10-year Treasury Note as 1.40% in July 2016

- It is now 2.40%. That rise in rates equates to a -8.84% decline in value.

- Think about that a second: more than four years of yield has been wiped out in just four short months.

- If your client has 30-year maturity exposure, the loss is nearly double.

- Note what happens if rates rise another 1% from now 2.40% to 3.40%.

Investors will be opening November statements and be greeted with a degree of shock. Not all bond positions are of 10-year and 30-year durations yet it’s been messy nonetheless. I’d use bond market rallies to shift away from a buy-and-hold mentality (unless you are laddered and short-term in your overall exposure). We are at the opposite end of the secular cycle that began in 1981. I do think you can do better.

My two cents is not to bail on the asset class but to diversify to a handful of fixed income trading strategies and tactical ETFs. Here is a link to information on our CMG Tactical Fixed Income Index – performance data through November. There are a handful of tactical bond ETFs that have done a good job over the recent period. I show a few in Trade Signals below.

Trade Signals – Investor Sentiment Too Many Bulls; Zweig Bond Model Sell; HY Buy; Equity Trend Evidence Bullish (posted 12-7-2016)

S&P 500 Index — 2,212 (12-7-16)

The U.S. equity market trend evidence remains bullish. Investor sentiment has reached a bullish extreme. Such readings are short-term bearish for the equity markets and suggest a pull-back that would test the recent breakout to new highs.

The CMG Managed High Yield Bond Program is in a buy signal and the CMG Tactical Fixed Income Index is long “JNK” and “CWB”. The Zweig Bond Model remains in a sell, favoring “BIL”.

You’ll find the charts and data by clicking the link below.

Posted each Wednesday, Trade Signals looks at several of my favorite stock, investor sentiment and bond market indicators. It is my weekly risk management dashboard, designed to keep me better in sync with the major technical trends. I hope you find the information helpful in your work.

Click here for the most recent Trade Signals blog.

Concluding Thought and Personal Note

Alan Greenspan was in the press this week. Do you remember his “Irrational Exuberance” call in the mid-1990s? I sure do but his call was early. The euphoria that followed in the late 1990s, as everyone jumped aboard the tech train, may go unmatched.

I remember his “there is no bubble in the housing market” call and later admitting that he missed it and no one saw it coming. Except we and many others did. But he’s sharp and a few comments made this week caught my eye (from the article):

The 90-year-old Mr. Greenspan, who remains active at his company Greenspan Associates LLC, declined to comment specifically about the Fed or politics.

While he isn’t as worried about stocks today as he was in the mid-1990s, he is far more concerned about the bond market and the recent sharp rise in interest rates. “The key is not the S&P 500. It’s the 10-year note and 30-year bond that matter,” he said. “The only thing which is way out of line is the price/earnings ratio in the bond market. And that is not an insignificant factor.”

He is also concerned that the economy could be headed for a period of stagflation—rising prices coinciding with weak growth. “The odds are better than 50/50,” Mr. Greenspan said. “At this stage, that’s what I worry about.”

But Mr. Greenspan maintains the hands-off attitude he has expressed in the wake of the housing collapse. “Once a bubble emerges, it is difficult to do anything to stop it that won’t have a major negative impact on the economy,” he said. “The best thing to do is to let it run its course and address the consequences when they occur.”

Stay around in this business long enough and there are a few events that just get replayed in your mind. In 1987, I was in Maui on a Merrill Lynch award trip when the market crashed. Talk about irrational behavior. People were… well… crazy. I awoke to a 3:00 am Maui time call. It was my manager who proceeded to scream to get on the next plane home. No cell phones back then – just a huge three-day phone bill and much distress.

In December 1999, my client of just a few years, Roberta, left us to move to a broker who was putting her into what she called “safe stocks.” “Safe stocks” that turned her $1 million into $500,000 in just few short years. She was just a few years away from retirement. She averaged about 14% in 1998 and 1999 but that paled in comparison to 25% for the S&P 500 and more than 50% for the tech sector. Her husband had remained a client. We gained in 2000, 2001 and 2002. She was down 50%.

Of course, subprime and the near implosion of the global financial system occurred in 2008. Most recently, it is all that money in passive equity funds/ETFs, bond funds/ETFs and a lot of money in those high dividend payers. My client Aram called me this past spring wanting to buy high dividend stocks. His neighbor was making a killing.

I was thinking about 1987. Add approximately 10 years and we came to 1998 and the Long Term Capital Management crisis. Add 10 years and the 2008 crisis hit. Add approximately 10 years and I’m starting to think. 2018 or sooner?

Keep this front of mind:

- 1998 is when Russia defaulted on its debt. There was a global liquidity crisis and Long Term Capital Management, a hedge fund, owed over $1 trillion to Wall Street banks. My friend Jim Rickards was the attorney for LTCM. He negotiated the bail out.

- In the room was Fed Chairman Alan Greenspan and Treasury Secretary Robert Rubin. Both later testified that they were just a few hours from shutting down every stock and bond exchange in the world.

- $4 billion was made available, the Wall Street banks’ balance sheets were propped up, the Fed cut rates and the storm passed.

- Lehman failed in September 2008. Morgan Stanley was just a few days away from failing. It would have spread to Goldman, Citibank, Bank of America and JPMorgan.

- However, the Fed intervened once again. They printed $4 trillion in new money and did $10 trillion of swaps with the ECB. The ECB gave the Fed trillions of euros in exchange for dollars, which they couldn’t print so they could use the dollars to bail out the European banks. The Fed was left with trillions of euros on its balance sheet.

- The Fed guaranteed every money market fund and every bank deposit in the U.S.

- In 1998, Wall Street bailed out a hedge fund. In 2008, the Fed bailed out Wall Street.

- The Fed printed almost $4 trillion to bail out the banks and lowered rates to zero percent.

- Their balance sheet currently sits at $4.5 trillion. It was $800 billion in 2008 and $2.8 trillion in 2012.

- If their balance sheet was back down to where it was in 2008 and interest rates were at 2.5% vs. ½% today, they’d be in a far healthier position to deal with the next crisis.

Source: Mises.org.

My wife would tell me to quit complaining, so I’ll hop off my horse and simply conclude by saying something just doesn’t smell right to me. Something is off. There isn’t much room for error and we are far more globally interconnected than most people might think.

For now, the good news is that the equity trend remains positive. It will be better news if you are in good shape to take advantage of the opportunities the next dislocation creates. So stay hedged, stay tactical and stay patient.

I’m really looking forward to Sunday. I’ll be visiting Brie in NYC and she’s excited because I’ll be hauling some of her excess stuff back home. I think we’ll walk around and do a little shopping. Then it’s dinner with good friends John Mauldin and Rory Riggs. Both smart forward thinkers. Some deep discussion and I’m pretty sure a few “high fives” – Rory loves to high five.

I’ll be in Denver on December 17-19 with a ski day planned for Sunday the 18th. So I’m working on getting into better shape. Susan and I are taking the kids to Lake Placid in late December and the plan is to watch the Penn State Rose Bowl game with Ohio State crazed Uncle Jim and his family. They have an amazing house in Lake George.

I’ll be in Colorado on January 8-11 and the Salt Lake City area on January 11-13. Then, the Inside ETFs 2017 Conference in Hollywood, Florida. I will be presenting on gold (which is in a confirmed down trend – I’ll share a few ideas on how to trade gold). If you are planning on attending, please let me know. I’d love to grab a coffee or better yet a good beer with you.

Coach Bahr had a few sayings that still stick with me today. The one I remember most is, “If you’re not getting better, you’re getting worse.” No matter where you are in life or what you are doing, don’t sit idle, focus on getting better. I like that.

Lift a glass with me as I send a special Italian hat tip to the great Walter Bahr. His health has been challenging for him. He should know just how very much he is admired and loved. Thank you, Coach. And here’s wishing you and your family the very best.