Staphyl Capital letter to investors for the month of October, 2019.

Friends and Fellow Investors:

For October 2019 the fund was down 8.6% net of all fees and expenses. By way of comparison, the S&P 500 was up 2.2% while the Russell 2000 was up 2.6%. Year-to-date 2019 the fund is up 6.4% while the S&P 500 is up 23.2% and the Russell 2000 is up 17.2%. Since inception on June 1, 2011 the fund is up 74.9% net while the S&P 500 is up 169.3% and the Russell 2000 is up 107.0%. Since inception the fund has compounded at 6.9% net annually vs 12.5% for the S&P 500 and 9.0% for the Russell 2000. (The S&P and Russell performances are based on their “Total Returns” indices which include reinvested dividends. The fund’s performance results are approximate; investors will receive exact figures from the outside administrator within a week or two. Please note that individual partners’ returns will vary in accordance with their high-water marks.)

Q3 2019 hedge fund letters, conferences and more

The fund got absolutely schmeissed this month primarily due to our short position in Tesla (much more on that below). Also, this month, I removed our index shorts on the S&P 500 and Russell 2000 (via short positions in SPY and IWM respectively) when SPY set its second new all-time high this week, despite the fact that I’ve never seen a greater disconnect between deteriorating economic fundamentals and a stock market that supposedly depends on them.

In 2007 (while working on Wall Street before opening this fund) I sensed the economy was about to tank as the housing bubble burst and positioned the bulk of my personal accounts short the S&P 500, and thus was up in 2008 when stocks crashed. Sensing the same thing last fall (a tanking economy, albeit not to the degree of 2008’s, combined with egregiously high stock valuations), I took out the same playbook but—undoubtedly due to the resumption of Fed and ECB money-printing—it clearly isn’t working.

The short-lived era of net “quantitative tightening” among the big three central banks (the Fed, ECB and BOJ) is over. The Fed’s balance sheet contraction stopped in August and >$60 billion/month of Treasury buying resumed in September (allegedly only to meet short-term liquidity needs—a nonsensical “explanation” for debt monetization that enables Washington’s profligate spending), while the ECB resumed €20 billion/month in QE and the BOJ continues printing.

I’m now wondering if stocks might be sensing significant looming inflation due to the lack of government fiscal discipline that’s creating trillion-dollar deficits that are likely to worsen as both Democrats and Republicans spend us into oblivion. In such an environment stocks can climb (or at least tread water) in nominal terms, and as short positions are priced “nominally” one wouldn’t want to be broadly short in such a situation. (Despite closing out our index shorts, I’ve maintained our array of individual stock shorts, many of which [excluding Tesla] are working despite the rising market, perhaps because they’re among the worst public companies in America—far worse, on a relative basis, than those broad indexes.)

Following Powell’s news conference in which he basically said “The Fed won’t raise rates unless inflation gets seriously out of control” I shorted the long-term U.S. Treasury bond ETF (TLT), because as our federal budget deficit escalates (it’s now around $1 trillion a year), I think “the market” may raise rates because of the Fed’s reticence to do so. The net cost of carry on this position is only around 1% a year, and when I see the money-printing craziness beginning all over again I consider that to be cheaply bought peace of mind. If you’re unfamiliar with the topic, read up on the insanity misleadingly called Modern Monetary Theory, because it’s happening right now.

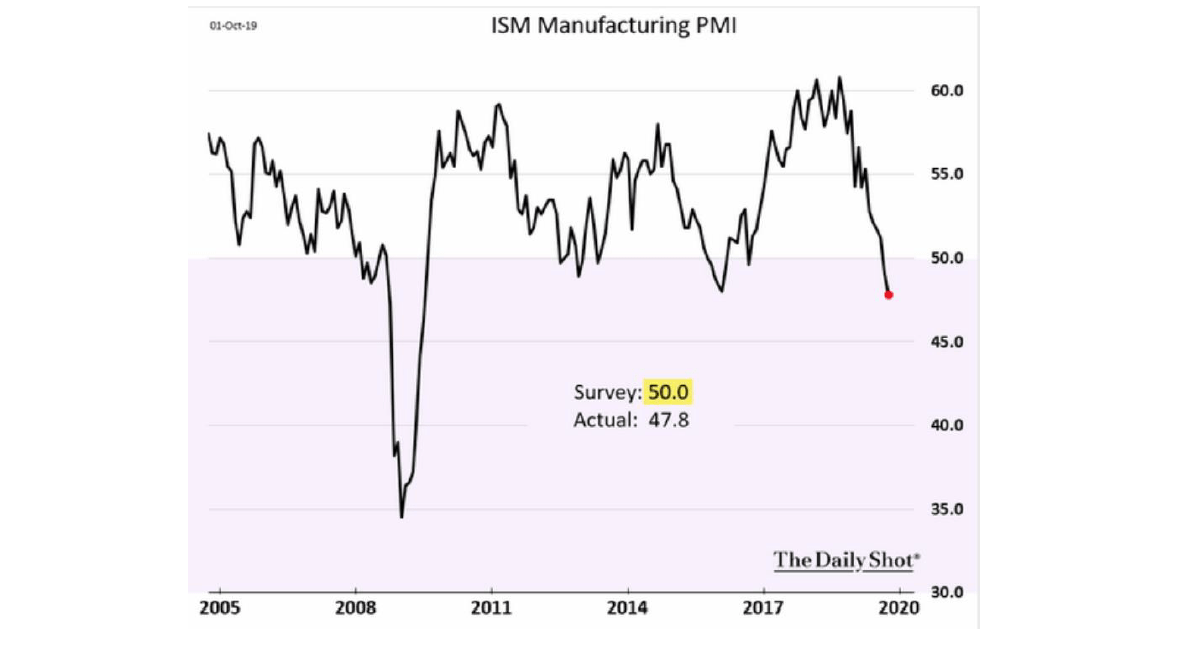

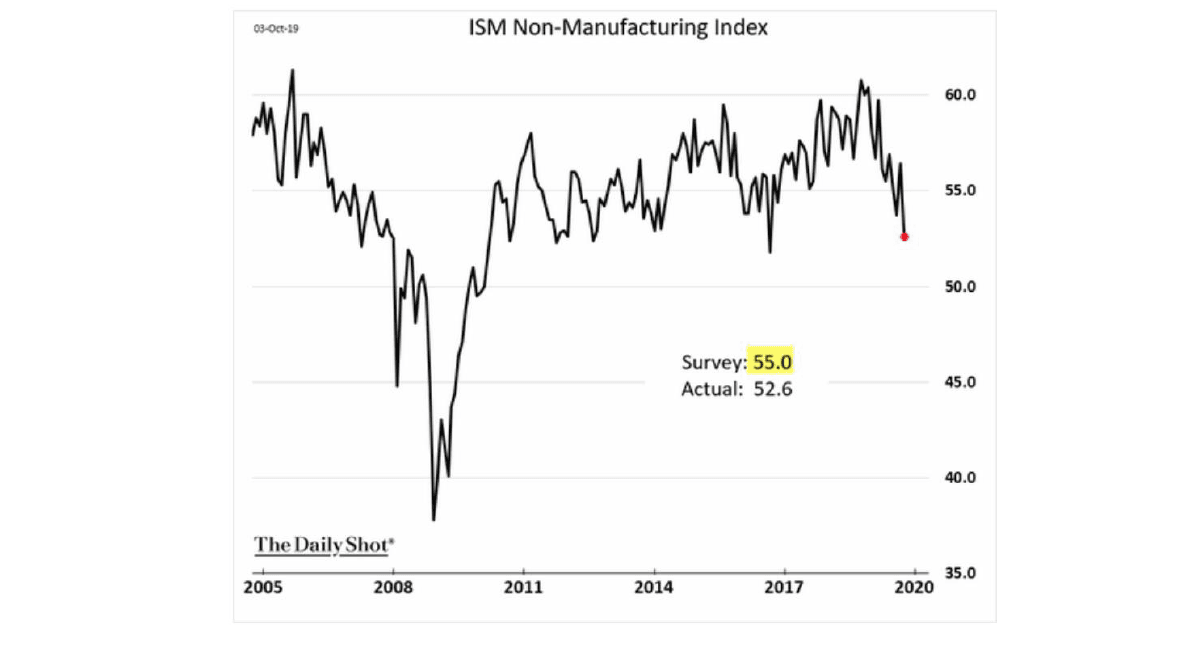

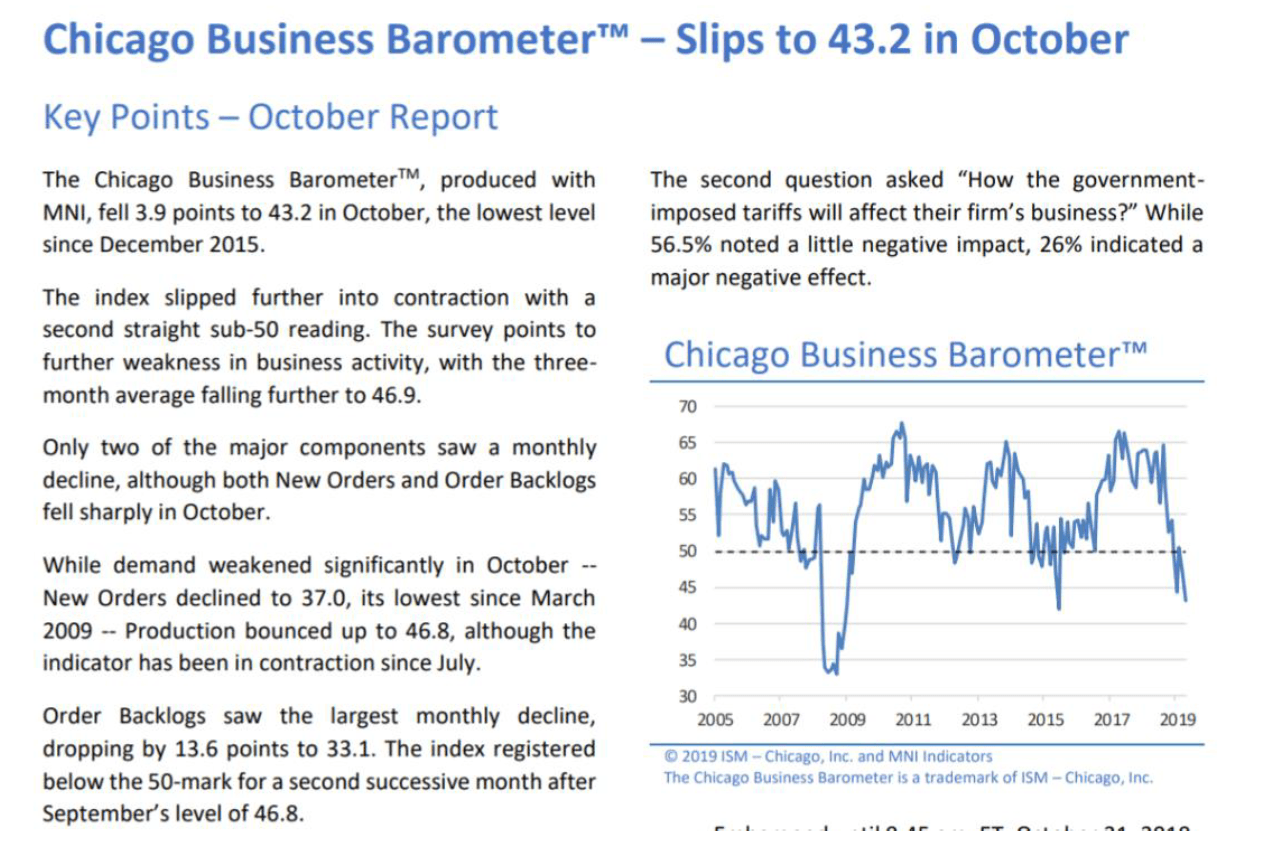

Meanwhile, if you’re wondering why I’m so economically bearish (and thus now expecting to see a return of 1970s-style “stagflation”), here are some of the reasons why…

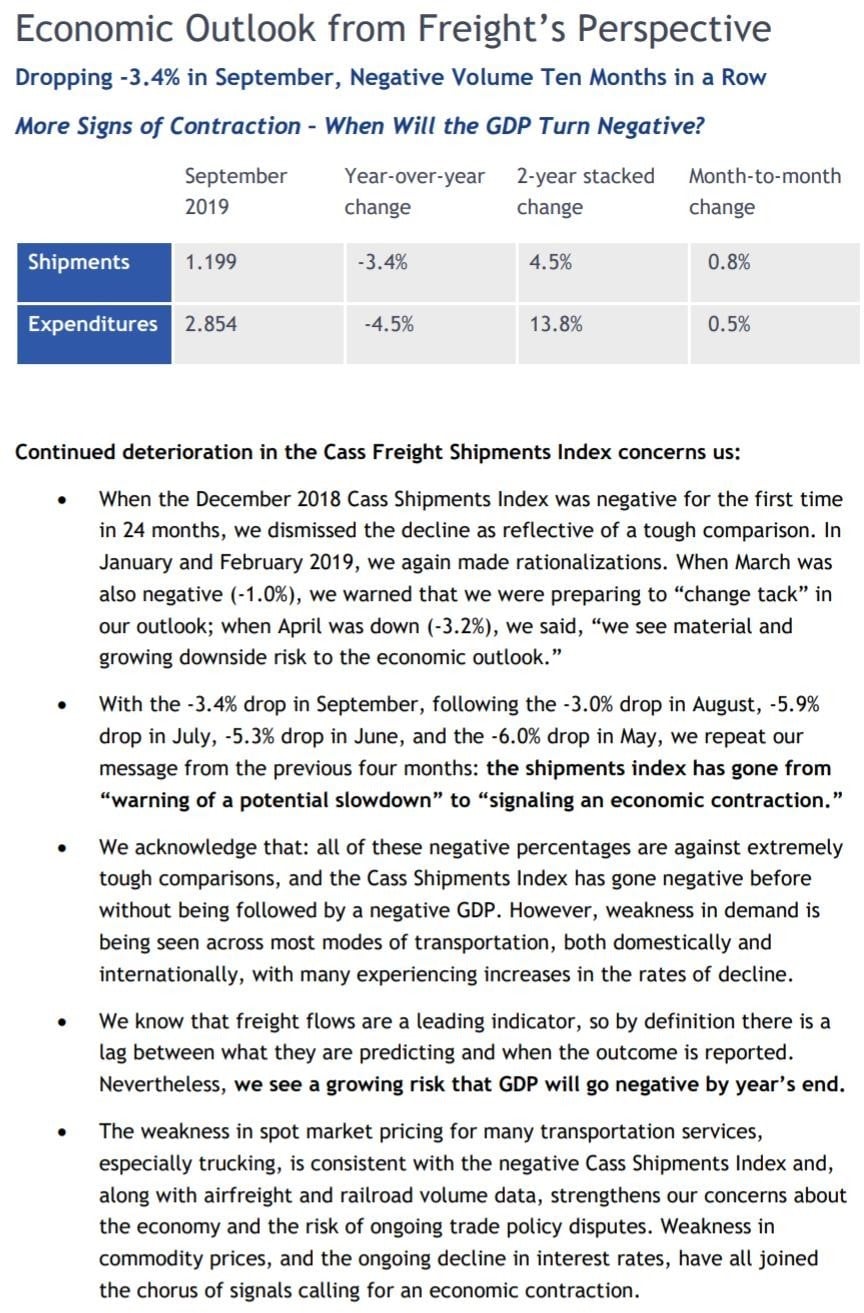

And have a look at how ugly U.S. rail traffic is.

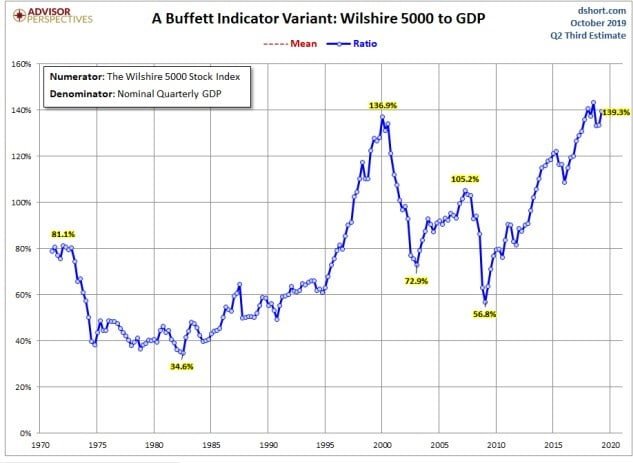

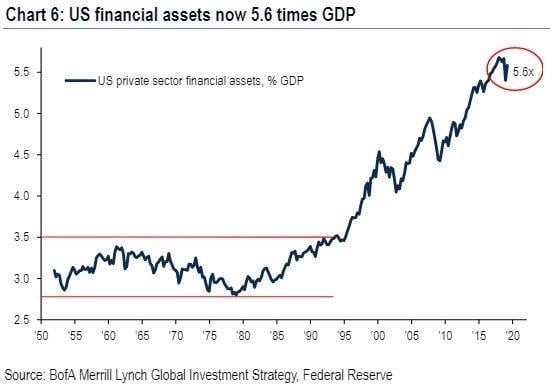

And here are a couple of metrics showing how historically expensive this market is:

And in case you’re still not convinced we’re in a giant financial bubble…

And now for our other shorts…

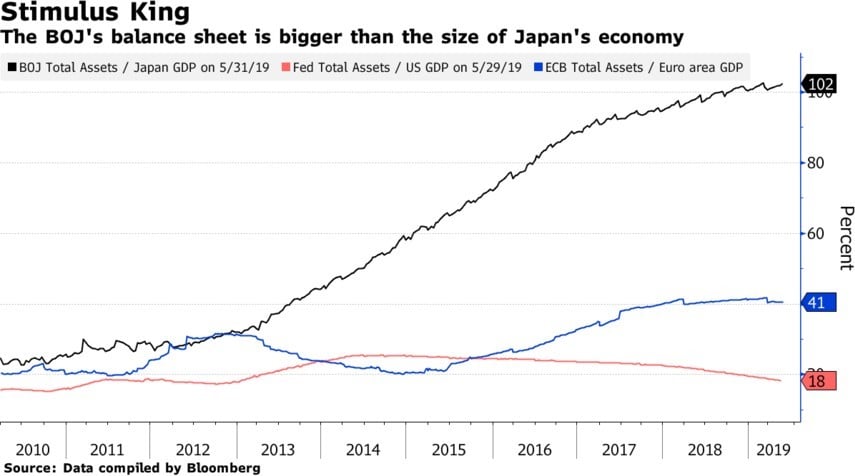

We continue (since late 2012) to hold a short position in the Japanese yen via the Proshares UltraShort Yen ETF (ticker: YCS) as Japan (despite having substantially tapered its QE) continues to print 3% of its monetary base per year after quadrupling that base since early 2013. In 2018 the BOJ bought approximately 67% of JGB issuance and in 2019 it anticipates buying 70%! In fact, the BOJ’s balance sheet is now larger than the entire Japanese economy…

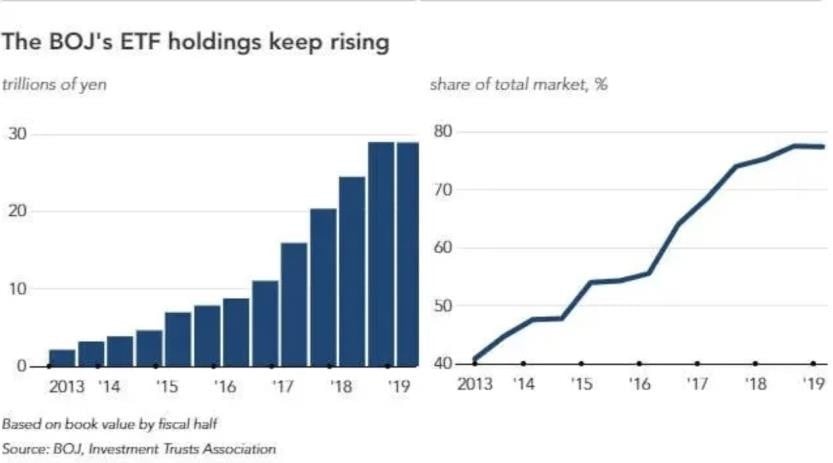

…as it owns nearly 45% of Japan’s debt and nearly 80% (!) of its ETFs:

Just the interest on Japan’s debt consumes 8.9% of its 2019 budget despite the fact that it pays a blended rate of less than 1%. What happens when Japan gets the 2% inflation it’s looking for and those rates average, say, 3%? Interest on the debt alone would consume nearly 27% of the budget and Japan would have to default! But on the way to that 3% rate the BOJ will try to cap those rates by printing increasingly larger amounts of money to buy more of that debt, thereby sending the yen into its death spiral.

When we first entered this position USD/JPY was around 79; it’s currently around 108 and long-term I think it’s headed a lot higher—ultimately back to the 250s of the 1980s or perhaps even the 300s of the ‘70s before a default and reset occur.

We continue to hold a short position in the Vanguard Total International Bond ETF (ticker: BNDX), comprised of dollar-hedged non-US investment grade debt (over 80% government) with a ridiculously low “SEC yield” of 0.42% at an average effective maturity of 10 years. With Euro area core inflation at 1% and—due to the ECB’s money-printing ultimately headed much higher—I believe this ETF is a great way to short what may be the biggest asset bubble in history. Currently the net borrow cost for BNDX less the dividends provides us with a positive rebate of around 0.5%/year and I think it’s a terrific place to sit and wait for the inevitable denouement of this insanity. And as noted earlier in this letter, we’re also now short TLT which is roughly the U.S. equivalent of BNDX, but with an average maturity of 20-30 years.

We also hold short positions in Netflix (NFLX) due to its egregious valuation within the context of terrible cash burn and increasing competition (particularly from Disney), Square (SQ) due to its egregious valuation and a stock-dumping CEO who so effusively praises (and enables) Elon Musk that I suspect he’s equally untrustworthy (and indeed in June the company fired its auditor), Carvana (CVNA) due to a laughable business model with escalating losses, a founder with a sketchy past and insiders who dump stock steadily, Wayfair (W), an egregiously bad negative-scale on-line furniture business with yet another team of insider stock-dumpers and Invitae (NVTA), a non-proprietary, money-losing genetic testing company showing negative scale.

And now for the fund’s long positions…

We continue to own Communications Systems, Inc. (ticker: JCS), an IOT (“Internet of Things”) and internet connectivity & services company, which in October reported fantastic Q3 earnings of .19/share with a 42% gross margin and $2.20/share in net cash. JCS is now making an annualized .68/share (based on the first nine months of the year) and a 14x multiple on that plus the cash would value it at almost

$12/share. The company’s multiple divisions are best explained by the slide presentation from its annual meeting and this terrific Seeking Alpha article.

We continue to own Aviat Networks, Inc. (ticker: AVNW), a designer and manufacturer of point-to-point microwave systems for telecom companies, which in September booted its perpetually overpromising/under-delivering CEO and gave the job to the COO/CFO credited with stabilizing and turning around the business. In August Aviat reported a solid FY 2019 Q4, with revenue up slightly year- over-year accompanied by a significant improvement in operating income while guiding to a very strong first half of FY 2020 (which began July 1, 2019), with income and cash flow expected to be up substantially year-over-year. Additionally, Aviat has $408 million of U.S. NOLs, $8 million of U.S. tax credit carryforwards, $212 million of foreign NOLs and $2 million of foreign tax credit carryforwards; thus its income will be tax-free for many years so GAAP EBITDA less capex essentially equals “earnings.” Valuation- wise, if we assume $14 million in FY 2020 adjusted EBITDA (first-half guidance is $7.5 million) and remove $1.7 million in stock comp and $5.3 million in capex we get $7 million in earnings multiplied by, say, 14 = approximately $98 million; if we then add in approximately $37 million of expected year-end net cash we get $135 million, and if we divide that by 5.4 million shares we get an earning-based valuation of around $25/share. Alternatively, if we look at Aviat as a buyout candidate its closest pure-play competitor, Ceragon (CRNT) sells at an EV of approximately 0.7x revenue, which for AVNW (assuming $240 million in 2020 revenue) would be 0.7 x $240 million = $168 million + $37 million expected year-end net cash = $205 million. If we value Aviat’s massive NOLs at a modest $10 million (due to change-in-control diminution in their value), the company would be worth $215 million divided by 5.4 million shares = almost $40/share. Meanwhile, here’s a great Seeking Alpha article about the company.

We continue to own Westell Technologies Inc. (WSTL), which in August replaced its CEO for the umpteenth time (and its CFO left for a larger company) after reporting an awful FY 2020 Q1, with revenue down 31% year-over-year and a drop in gross margin from 45.5% to 36.1% and negative free cash flow of around $1.2 million; about the only good news here is that the company ended the quarter with $24 million in cash and no debt. That said, we continue to own Westell because it now sells at a negative enterprise value, so on that metric it’s dirt cheap although clearly the business needs to stabilize and grow, and in a step towards “stabilization” in October the company executed a mild restructuring which will meaningfully cut the annual burn. Westell also suffers from a dual share class with voting control held by descendants of the founder, yet the company is so cheap on an EV-to-revenue basis that if management can’t start generating meaningful profits it seems primed for a strategic buyer to acquire it. Assuming 15.6 million shares, an acquisition price of just 0.6x run-rate annual revenue of $36 million would (on an EV basis) be nearly $3/share.

We continue to own the PowerShares DB Agriculture ETF (ticker: DBA), as agricultural products remain the most beaten-down sector I can find that isn’t a “buggy whip” (something on the way to obsolescence) or cyclical from a demand standpoint. Perhaps “Phase 1” of Trump’s China trade deal plus recent harsh weather in the farm belt will finally be able to move it higher.

Thanks and regards,

Mark Spiegel

{kind=link}

{kind=link}