Roubaix Fund Composite commentary for the fourth quarter ended December 31, 2020.

Q3 2020 hedge fund letters, conferences and more

Dear Partners,

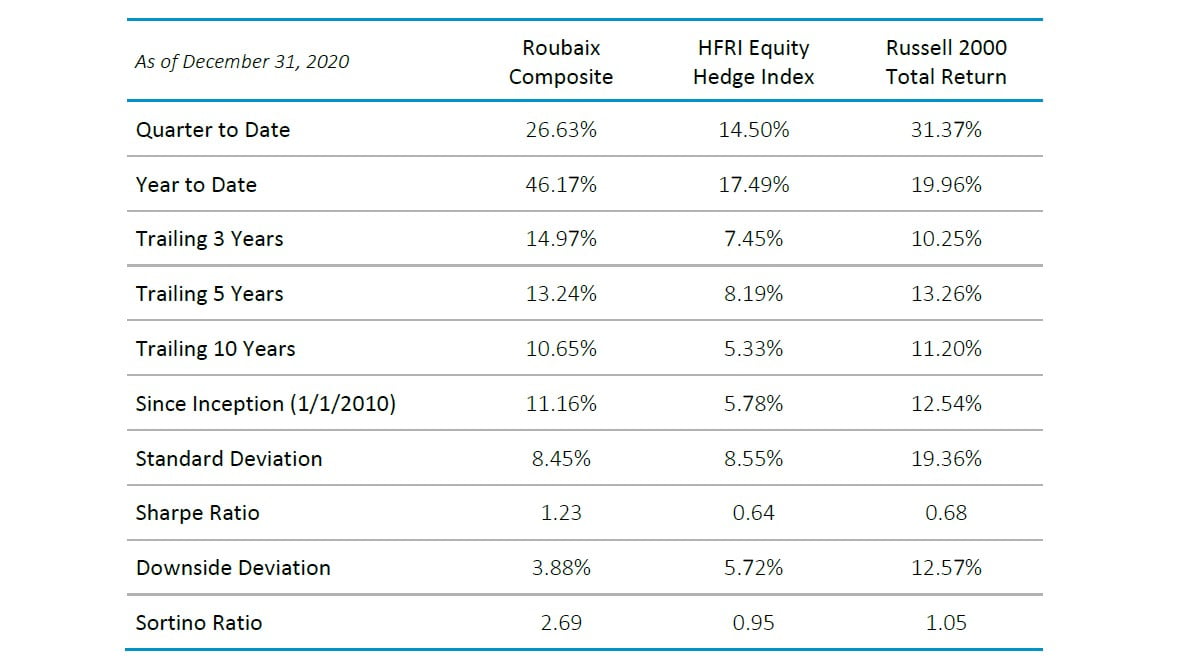

During the fourth quarter of 2020, the Roubaix Fund Composite (the “Composite”) (i) gained 26.63% on a net basis compared to a return of 14.50% for our long/short equity peer group, represented by the HFRI Equity Hedge (Total) Index (the “HFRI”)(ii) and 31.37% total return for the long-only Russell 2000 Index (the “Russell”)(ii). The end of period net exposure was 41.0% compared to a 43.5% average since inception in January 2010.

Roubaix Fund Composite gained 46.17% On A Net Basis

Full the full year in 2020 the Composite gained 46.17% on a net basis compared to a return of 17.49% for the HFRI and 19.96% for the Russell. We believe that Roubaix’s investment philosophy and process drove performance in 2020 through maintaining discipline with our price targets and stop-loss levels within a narrow focus list of ~300 stocks. The Composite was able to capitalize on both sides of the market volatility, generating substantial alpha and absolute outperformance during the Q1 market drawdown, yet still capturing a significant portion of the market rebound through the balance of the year. The Composite generated more than 45% gross alpha in 2020 relative to the Russell, with almost 25% alpha from the long book and more than 15% alpha from shorts.

Outperformance was driven by the breadth of our investment process. For the year, the long book delivered a 52% gross total return across 180 stocks. The largest contributor added 325 basis points, while 28 stocks contributed more than 100 basis points. The short book also excelled in 2020 on a broad level. Similarly, no single short added more than 160 basis points, while 27 stocks contributed more than 50 basis points.

Economy & Markets

The health crisis from SARS-CoV-2 / COVID-19 has been a generational event that will find its place in history. Fortunately, pandemics do not happen often. The world has certainly struggled with diseases, but incidences have been geographically isolated since the Spanish Flu in 1918. A modern pandemic brought with it the challenge of globalization, which enabled the virus to spread rapidly worldwide. What was also historic was the response by governments to shut down entire economies to reduce mobility and human interaction. The ‘Great Lockdown’ cut activity in many industries to previously unimaginable levels, and thereby caused the most dramatic fall in real GDP since The Great Depression.1

The devastating impact of the virus and the shutdowns was not lost on policy makers. Central banks reacted almost immediately. The lessons from The Great Depression shaped the response to the Great Financial Crisis of 2008, and that toolkit was deployed again in 2020. Interest rates were cut to zero and large-scale quantitative easing was layered upon it. The Fed also adjusted its long-term policy framework to target average inflation over the cycle and emphasize the labor market. In other words, the Fed expects to be slower than ever to tighten policy during the next expansion.2 This has clear implications for the shape of the pending recovery as the economy will, in effect, be allowed to overheat. Augmenting this monetary response was an enormous fiscal policy response. To their credit, U.S. law makers moved quickly and with confidence to approve trillions in fiscal spending. Combined, these policy actions were the largest in US history, dwarfing the response to the Great Financial Crisis. On a global basis, “governments allocated a stunning $10 trillion for economic stimulus in just two months. That was triple what they spent during the entire 2008-2009 financial crisis.”3

Markets reacted quickly and emphatically to all phases of this crisis. In the first quarter, the globalization of the outbreak and ensuing stay at home orders issued by national, state and local governments drove the fastest bear market in U.S. history. However, the policy responses from central banks and fiscal authorities were also swift and powerful, ensuring that capital markets functioned normally. From there the rapid pace of vaccine development combined with a slower spread of the virus allowed markets to rebound at the fastest rate in history.

The Composite was able to capitalize on the opportunities the markets provided. Our consistent philosophy and disciplined process simplified the decision sets as the market initially collapsed in Q1 and then recovered. Our research centers on ~300 long and short focus list ideas that we deem to be the best and worst investment stories in our market cap range. We then track and analyze each of these stories in our research management system to assess when the individual securities present themselves as superior investments based on our assessment of the company fundamentals, the market, the economic backdrop, and our evaluation of the risk-reward profile at a given stock price. The extreme price volatility throughout the year presented a consistent pool of attractive opportunities to deploy capital to incremental long and short investments.

As 2020 got underway, we anticipated the health crisis and lockdowns that began in China and spread throughout Asia and then to the West would have a devastating impact on global equity markets. We used that judgement to increase the quality of our longs by consolidating our positions into focus list stocks that we believed were poised to best withstand any temporary headwinds from the emerging health crisis. Likewise, we were more aggressive on the short side through the addition of incremental focus list stocks that we felt had the most risk to worsening economic conditions. Thus, when the Russell 2000 Total Return Index plunged to its low on March 18, 2020 with a YTD loss of more than 40%, the Composite declined less than 5% on a gross basis despite carrying ~43% average daily net exposure over this period. This was due to a combination of the long book significantly outperforming the declining market while the short book plunged more than 50%.4

Amidst the market volatility we maintained discipline with our investment process and closed out of many of our short positions that reached our bear case price targets. As the massive global policy response took shape, we believed the worst-case scenario for the market became less likely. We were also optimistic on the scientific front that therapies and vaccines would be identified and developed at a rapid pace due to the known structure of the virus, technological progress, cooperation, and global scientific leadership. Thus, we repositioned the portfolio for an eventual economic recovery by mid-April, once again largely utilizing our existing research on core focus list positions while considering the macro implications of a recession ending and an expansion beginning.

As the market rebound paused heading into the fall, we further adjusted the Composite to emphasize our view that the market would begin to look beyond 2020 and into the years ahead. The market is a discounting mechanism, and we believe that the pandemic, and its impact upon the economy, will prove to be temporary. We also embrace the view that Wall St. is generally better off than Main St. because public companies, even the smaller ones in which we invest, are still relatively large businesses. They typically have access to capital, flexibility to reduce costs, and find ways to maintain profitability in a downturn. In doing so, such companies can improve efficiency and set the stage for accelerated growth and profit recovery as the economy normalizes. The long book shifted towards a post-pandemic economic recovery scenario and the short book returned to focus list stocks with long-term secular pressures that benefited from a temporary increase in demand during the pandemic.

The Largest Long Contributors

The largest contributor to fourth quarter long performance was Codexis (CDXS), a truly unique investment story. The company engineers enzymes that enhance productivity of the manufacturing processes of major industries including pharmaceutical, food and other companies. The high-performance enzymes identified by Codexis enable higher levels of production, which in turn drives profits for customers. The story does not stop here. Codexis’ proprietary platform, Code Evolver, has also demonstrated early success in identifying proteins to develop novel protein and gene therapies. This adds another layer of upside optionality to the company and has validation from partnerships with Nestle and Takeda. In these instances, the company earns milestone driven incentives and royalty payments. We see Codexis’ API business generating increasing scale at the same time the pipeline around licenses and royalties has never been larger, and as a result we maintain our position.

The next largest long contributor was WESCO International (WCC). This company caught our attention due to the highly unusual circumstances that transpired. WCC was in the process of merging with peer Anixter International when private equity investors attempted to buy WCC and then the combined company. The facts were clear that there was significant value. WCC prevailed and was able to finalize the merger and avoid being acquired. However, timing added a wrinkle to the story. The deal closed not long before the pandemic struck and caused meaningful concern about the availability of capital. After the merger, WCC had significant leverage and at that time there was also uncertainty about the stability of their end markets. As our views evolved and as the U.S. Fed stabilized capital markets, we saw opportunities in companies that had meaningful levels of self-help, and we thought the balance sheet risk was less than the market believed. To date, this has been accurate and even the end markets for WCC proved to be resilient during the pandemic. While sharp appreciation has led us to reduce the size of our position in WCC, we anticipate outsized earnings growth in the years ahead from cost savings and an economic recovery.

The Largest Long Detractor

The largest detractor in the long portfolio during the fourth quarter was Repro Med Systems (KRMD). We originally invested in KRMD due to their pump system that delivers drugs subcutaneously. This method of delivery is well suited for certain therapies and it can be done in the convenience of a patient’s home, replacing a visit to a doctor’s office. As a result, the patient has a better experience, and the healthcare system saves costs by avoiding the charges that come with office visits. We see more convenient and lower cost delivery of healthcare as a trend that will be accelerated by the pressures caused by the pandemic. Unfortunately for KRMD, their main product’s production is tied to the collection of blood plasma. As the pandemic kept people at home, supply became constrained. This put pressure on KRMD’s business, and their pipeline was not far enough along to provide an offset. We exited our position in the stock but continue to monitor it and other companies that benefit from this powerful trend to make healthcare delivery more efficient.

The Best Performing Short Positions

The best performing short position in the fourth quarter was Luminex (LMNX), a medical device and diagnostics company that recently lost a large contract, faces increasing competition, and executed questionable M&A in the past. Our premise in shorting the stock in Q3 was that too many diagnostic testing stocks appreciated as beneficiaries from COVID-19. We believed LMNX was capitalizing revenue and profits that were not likely to persist past 2021 as the pandemic waned from vaccine rollouts. If that proved to be the case, investors would quickly shift their attention back to mounting competitive pressures and difficult comparisons in future periods. Our short thesis played out in a relatively short amount of time and we closed the position.

The second best short in the quarter was Hibbett Sports (HIBB), a sporting goods retailer. Many businesses were able to benefit from the spending shifts caused by the pandemic. For example, online retailers, companies that sell into the home improvement markets and grocery stores all saw varying degrees of improvement. We did not see HIBB as a clear beneficiary as they have historically underinvested in their online business. However, they managed to post very strong results during their third quarter from leisure spending trends and the stock reacted favorably. We shorted the strength of this rally and continue hold our position as we do not see HIBB as a longer-term winner in its markets.

The Largest Short Detractor

The largest detractor in the short portfolio during the fourth quarter was Diebold Nixdorf (DBD). The company’s primary business is selling automated teller machines to banks. We view the cash ecosystem as a structural share loser and several companies in this ecosystem are on our short focus list. While electronic payments continue to consistently take share, and while there was some concern about using paper money during the health crisis, DBD was able to post reasonable results. The stock has carried a low valuation as many stocks do when they have secular pressure. This low valuation allowed the stock to rally alongside the market in Q4 and we exited on our risk discipline. We will continue to monitor this stock and others in this ecosystem for opportunities to re-short when the risk-reward in more favorable.

Outlook

Markets finished strong in 2020, creating something of a hurdle for 2021. Valuations have expanded and the magnitude and pace of gains, combined with bullish investor sentiment, are reasons to remain balanced as the year gets underway. Low interest rates may also pose a risk to asset prices if they were to migrate back towards historical norms, or even pre-pandemic levels. By in large, our outlook remains constructive. Monetary policy is extraordinarily accommodative, as it has been for some time. Fiscal policy has also been historic in its magnitude. These have contributed to keeping consumers and the economy healthy. In fact, the U.S. consumer by some measures (savings rate, household net worth) is in the best position in decades, which is remarkable in and of itself, let alone when emerging from a recession. Retail spending fully recovered at a pace much greater than the last crisis. This was due in part to stimulus checks and enhanced unemployment benefits, as well as the consumers shifting spend areas that were either unaffected by the pandemic or that benefited from it.

The consumer strength is remarkable, especially considering the record surge in unemployment during the pandemic. Consumers found ways to both save and spend during this downturn even when spending on travel and leisure has remained largely unavailable. The pandemic continues to be a formidable foe and cases are again accelerating to the upside. Viruses mutate and it appears a new strain that is more transmissible5 that became dominant in the UK has now spread to other geographies. There is also another strain from South Africa that may be more elusive to the immune system’s antibody response.6 Situations like these present a refreshed headwind in early 2021, especially as countries reopen schools following the holiday break and as general fatigue of dealing with the virus grows.

There are also market based reasons for a degree of caution. IPOs are running at rates not seen since the 2000 tech bubble. Special purpose acquisition vehicles (SPACs) – where capital is raised for the purpose of doing an unknown acquisition – have been raising significant funds, and the underlying securities have posted rapid gains.7 Similarly, any equities related to the trend in electric vehicles and green energy have also seen exponential advances. While we do see reasons for enthusiasm in some of these areas, the appreciation has been relentless and may be a sign of excess in the market. To this point, the participation of retail investors in the U.S. stock market reached a record high.8 When we combine these factors with a market near record high valuation, we continue to see value in our long/short equity approach where we can capitalize on certain potential areas of weakness as this cycle progresses.

Light At The End Of The Tunnel

While the health crisis has renewed vigor in the near term, there is a light at the end of the tunnel. Clearly more and more people have been infected, and that will provide a degree of natural immunity. According to one respected expert, nearly a third of the U.S. population will have been infected by the virus by the end of January.9 Despite these harrowing realities, the nexus of technological advances and decades of scientific progress, global cooperation, and a singular focus on finding a solution to the pandemic has delivered vaccines that are highly efficacious, and in record time.10 Also encouraging, immunity to the coronavirus appears likely to last quite some time after either infection or vaccination.11 While early distribution has not been smooth, vaccine supply improves by the day as production grows and more vaccine trials complete successfully. Barring unforeseen circumstances, this should drive an increasing degree of community immunity by mid-year and progress towards normalcy.12

The U.S. political landscape also appears to be settled. With a surprising finish in the Georgia Senate runoff, Democrats possess a narrow congressional majority that will likely allow them to set an agenda. This will reinforce fiscal spending and an emphasis on the worker at some expense to the employer. This is a trend that has been in place for some time internationally and was emphasized by the Fed’s change to its monetary policy framework. Spending on certain areas that are reasonably bipartisan, such as infrastructure and clean energy, could help offset some of the pressure on jobs that have been, and will continue to be, dislocated by benefits of technological progress and automation. On the other hand, taxes are likely to rise and there may be more upside risk to inflation and treasury yields, which will present a multi-faceted challenge to capital markets in future periods, again underscoring the potential benefits of a long/short equity strategy focused on fundamental stock picking.

The Composite has positioned for a return to normalcy. This is reflected on the long side in equities that should demonstrate significant growth and enhanced profitability as the economy recovers. As discussed, we see an unusually strong consumer coming out of this recession due to the increased saving rate, record high household net worth and now rising wages. Companies like GoPro (GPRO) and Kura Sushi (KRUS) should benefit from the consumer rebound, but also have their own unique drivers of value over the next 2+ years. In the case of GPRO, the company launched its newest action camera, the GoPro9, under the umbrella of a new business model. The company offers a discount on the camera when customers purchase a subscription agreement that comes with additional services and benefits. The uptake of the subscription has been strong to date and offers the company a line of sight to a higher margin and more predictable revenue stream. The stock’s low double digit earnings multiple remains undemanding. We have seen this type of transformation play out in numerous situations in software, hardware and even retail companies such as RH. We see GPRO following suit and expect a return to travel later this year to be another reason for consumers to buy a new camera as they head back out on vacation.

Kura Sushi

In the case of Kura Sushi, the company is one of the newest restaurant concepts in the U.S. market. With just under 30 stores in 2020, the opportunity for growth is vast to a targeted long-term goal of ~300 locations. The product offering is quality food at an affordable price, something that always resonates with consumers. The experience is unique due to the highly automated food ordering, delivery, and a ‘gamified’ plate return system that all operate on automated conveyor belts. In addition to entertainment value, it enables high throughput with minimal staff. This operating model makes the business more readily scalable nationally as it is less dependent on labor. With rents for many attractive locations in decline due to the pandemic, the concept has a good chance to secure good locations at favorable prices. Even at its modest size, Kura has shown the ability to deliver excellent margins. We expect the end of 2021 and the following year to be a breakout for the company, and the modest valuation versus high growth benchmarks provides a roadmap for solid returns for the stock.

Raven Industries

While we see the unleashing of pent up consumer demand driving certain businesses in 2021, we also see good opportunities in the industrial complex where is potential to find companies with a combination of cyclical, thematic and company specific drivers. One example is Raven Industries (RAVN), an agriculture equipment company that has invested heavily in automation, a consistent theme in our long portfolio. With the economy recovering and corn prices rising recently, the cyclical outlook has also improved. In the medium and long run, using technology to improve productivity is critically important. RAVN’s products allow equipment to be run around the clock with fewer employees. We see RAVN compounding value both in 2021 and in the years ahead.

Stoneridge

Stoneridge (SRI) should also benefit from the strengthening economic outlook and the application of technology to improve efficiency. On the first point, SRI supplies components and systems into the commercial vehicle and automotive markets. Both markets are poised to improve in 2021 after varying degrees of headwinds in 2020. On the technology side, SRI’s MirrorEye product has promising applications for commercial truck owners. The product directly improves driver visibility which should reduce accidents, and thereby insurance premiums from costly insurance claims. Further, since the product replaces physical side mirrors it improves aerodynamics. This cuts fuel costs and creates another source of saving and productivity for vehicle operators. The pandemic delayed adoption in 2020, but 2021 is poised to be a breakout year for this company.

Anterix

We also maintain many long positions in companies that are not specifically tethered to the current backdrop. Instead, either the merits of the business, the development of the thesis or the strength of a trend control the expected outcome. One such position, which we have discussed in the past and remains a large position for the Composite, is Anterix (ATEX). The company owns spectrum approved for dedicated enterprise networks for critical infrastructure industries, among others. This spectrum will allow users to build fully private high speed data networks to capture the value of the internet of things, while at the same time having a higher level of secure communication and infrastructure. 13 In May 2020, company’s plan for its 900 MHz spectrum was approved by the FCC. 14 More recently in December 2020, the company announced its first commercial contract with Ameren (AEE) for a 30 year spectrum lease for a private LTE network with a further 10 year renewal option. This sets the precedent for future contracts. As the company scales with more contracts in 2021, the high margin business model will come into focus and should drive the shares. We also see the potential for the new administration to increase infrastructure spending and emphasize grid security15 as ways to drive employment and in reaction to a recent high profile government hack, respectively.16

Sequans

As was the case during 2020, we expect our returns to be driven by the breadth of our positions. While Anterix offers a unique investment that will benefit primarily from utilities creating private high speed data networks, demand for high speed data is clearly a much larger, and dare say ubiquitous, trend that will be evident in the years ahead. There are many ways to invest behind this, but in small cap equities we see Sequans (SQNS) as a particularly strong beneficiary. For years, the company has focused on developing the semiconductor technology that is uniquely suited to enabling these networks. Specifically, Sequans chips use less power and are lower cost, two basic parameters that differentiate their products from more expensive and power-hungry chip architecture that is rooted in the current PC and handset markets. The end markets Sequans is focused on are expected to grow over 40% and the company anticipates rising market share. The company’s growth this year will take profitability to break-even levels and they see a roadmap to over 20% operating margins as revenues scale over the medium term. The company’s goals would imply an earnings rate nearing $1.00 in 2023, which, if achieved, would drive the stock materially higher.

The short side of the portfolio has a balance of cyclical, thematic and company specific shorts. With the current backdrop having more of a macro influence than usual, we are expressing that in our mix of shorts. We see a large set of opportunities in companies whose stock prices have appreciated due to the temporary benefits of the health crisis. We think the premium valuations that have developed in otherwise mature areas such as consumer staples and retail offer particularly attractive short returns. We believe consumers are anxious to shift spending away from the basics and back towards areas where they have been unable to spend, namely travel and leisure.

Companies including J.M Smucker Company (SJM) and Scotts Miracle-Gro (SMG) have seen their sales accelerate to unsustainable levels that are not consistent with their mature end markets. We expect sales to slow and eventually give back some of the one-time gains caused by the unusual circumstances of 2020. Further, we question the sustainability of current peak valuations in the face of likely peak sales. We believe companies with such characteristics could face a combination of negative earnings revisions and lower valuations as the demand reality sets in this year. We also anticipate that companies that have benefited from consumers being homebound will see very challenging comparisons in 2021. No doubt, spending on home improvement and furnishing grew at unsustainable rates in 2020. Companies such as At Home Group (HOME), which was nearly insolvent at the start of the crisis, were ‘bailed out’ by booming sales. Homewares is a mature and competitive category and companies such as this should soon return to the challenging realities that were in place before the benefit of a forced spending shift.

Sykes Enterprises

We also continue to identify short opportunities driven by company specific situations. On the thematic front, we see Sykes Enterprises (SYKE) as a company that has its roots in servicing customers with labor intensive call centers. As the quality of alternatives continues to improve, the demand for SYKE’s services declines. Further, even voice level interactions are improving at exponential rates due to advances in artificial intelligence. While the company is of course adjusting its strategy to adapt, it by no means has the resources of the tech giants and software as a service companies that are making alternative solutions better and cheaper by the day. Identifying the trends that are transforming the business landscape often highlight the companies that are competitively challenged by those very same trends, and we expect this to be a continuous source of investment ideas on the short side of our portfolio.

To summarize, the outlook is constructive, albeit with risks developing. We believe that the economy is in the first stages of another economic expansion that is likely to last for years. The work from the scientific community coupled with the marvels of modern computing and analytics has allowed mankind to put the pieces in place to defeat a pandemic caused by a novel virus in approximately one year. As this becomes reality, people will again be free to return to the travel, leisure and work activities that involve personal contact. With household net worth and personal saving at or near all-time highs, consumer spending should be strong. Businesses largely navigated the recession caused by the pandemic well and are likely to generate a fresh high in earnings in 2021 and 2022. Small caps are attractive relative to the rest of the equity markets with faster earnings growth and lower valuation multiples. Within that context, we have a portfolio positioned for a return to normalcy. Further, we continue to identify and invest in numerous company specific situations that fit our investment process and offer attractive risk-reward profiles on each side of the portfolio.

We believe the most important drivers of equity value over time are the strength or weakness of a company’s business model, the advantages or challenges created by their financial structure, and the quality of the fiduciaries involved. We identify what we believe are the best long and short narratives in the small and mid cap universe of U.S. stocks and track them on a focus list. Our list is dynamic as we evaluate new companies entering our market cap range due to price changes, IPOs, spin-offs and other corporate developments. Likewise, we eliminate stocks from our focus list when the long thesis plays out and they become too large for our approach, or if the short thesis drives the stock price to a level at which it transforms into a special situation with vastly decreased liquidity and/or increased price volatility. Base, bull and bear case price targets are derived from two year forward valuation, while also considering longer term trends discounted back appropriately. We deploy capital when these differentiated narratives present themselves with a compelling risk/reward profile relative to other stocks in our portfolio.

We concentrate our efforts on smaller companies due to their inherent structural inefficiencies that drive greater price dispersion, in turn enabling higher alpha generation on both longs and shorts. The investment landscape continues its trend of consolidating investment management and advice at ever larger financial institutions. The cost benefit of increased scale has an inverse effect on the ability of investment managers to buy and sell smaller stocks when considering reasonable liquidity parameters. Further, the rapid growth in passive and quantitative investing is reducing the amount of competition from fundamentally driven active stock pickers overall. As an increasing share of daily trading volume shifts to passive from active mandates, there is even less economic benefit to sell side equity research. This in turn reduces the amount of published information, particularly in smaller stocks with lower trading volume. Importantly, we think these inefficiencies are not just persistent, but should move even more in our favor over time.

Smaller companies are likely to remain a reliable source of mispriced investment opportunities that are either overlooked or are not practical investments for larger firms. This is especially true today as the small cap Russell 2000 Index lags the large cap S&P 500 Index by ~15% YTD, and almost 30% over the past three years. We believe our structured fundamental investment process allows us to uncover such unique ideas and generate value through stock selection on both long and short investments. We tend to concentrate individual stock positions in 30-50 longs and 30-50 shorts to maximize the value of our research, and likewise do not utilize ETFs or options to hedge. Position level weights are optimized for exposure to changing fundamental factors, catalysts and risks. To manage overall portfolio risk, we avoid leverage on the long side, maintain consistent net exposure, and remain disciplined with our price targets and stop-loss levels. We believe our strategy is amongst the leaders in small cap l/s equity with a decade of compelling net returns, low volatility, and consistent capital preservation in weak markets.

Thank you for your ongoing support,

Christopher E. Hillary