IRC Section 1202 provides one of the most powerful tax benefits in the U.S. Internal Revenue Code (IRC) to entrepreneurs and investors. However, it is also one of the least recognized IRC Sections, even amongst those who stand to most benefit from its use. Section 1202 provides an exclusion from taxation to a qualified investor of up to $10 million of capital gain or 10 times the stockholder’s adjusted cost basis, whichever is greater, upon the sale of Qualified Small Business Stock (QSBS). Why has such a generous provision in the tax code gone comparatively unnoticed? A look back at recent legislative history and tax rates provides some insight.

Q3 2020 hedge fund letters, conferences and more

Section 1202 was originally enacted as part of the Budget Reconciliation Act of 1993 and meant to encourage private investment into small companies that have difficulty raising private capital. Two events in the last decade have increased its popularity. First, the tax benefits applicable to sales of Qualified Small Business Stock were made more generous in September 2010, exempting 100% of an eligible investor’s gain – up to the $10 million or 10-times basis limit. Prior to 2010, gain exclusion had been limited to 50-75% of the total eligible gain, depending on the date of the stock sale. This more generous exclusion was then made permanent in 2015. Second, the TCJA of 2017 lowered corporate income tax rates from 35% to a flat 21%, enticing more company founders to consider choosing or converting to a C-corporation for their company structure, a key requirement for stock to qualify as QSBS.

Tax Benefits of Section 1202 Exclusion

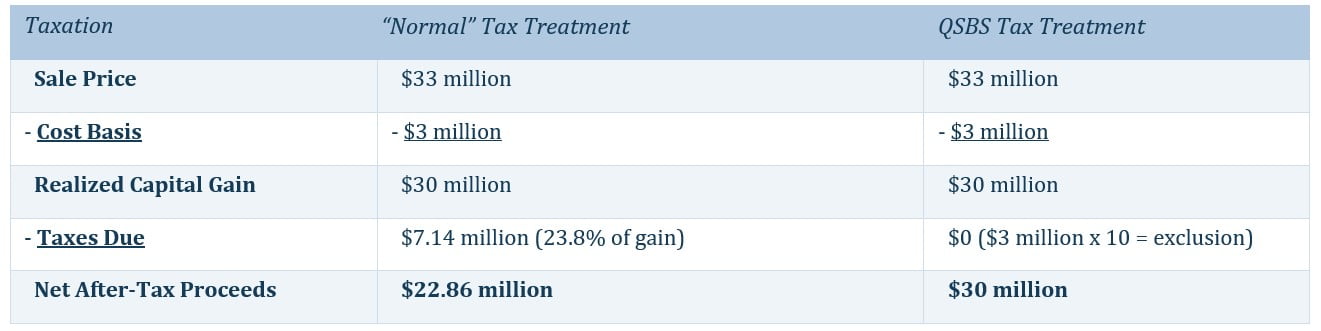

To give a concrete example of the potential value of Section 1202, consider Susan who received 1,000 shares of QSBS stock as compensation worth $3 million in 2014. In 2020, she sells all her shares for $33 million.

Under normal taxation rules, Susan would owe federal (and any state) taxes on the $30 million capital gain, paying $7.14 million in federal taxes assuming a top capital gains rate of 20%, plus the additional Net Investment Income (NII) tax of 3.8%.

Because the stock qualified as Qualified Small Business Stock, however, Susan’s capital gain can be excluded up to the greater of $10 million or ten times her cost basis of $3 million, which is $30 million in this example. As a result, Susan’s entire capital gain from the QSBS sale is excluded from taxation. See below for a summary table:

Finally, if the sale price were higher and Susan realized any capital gain above the maximum $30 million exclusion amount, that gain would be taxed at 28% under QSBS rules (but exempt from the NII tax).

Corporate Requirements for Qualified Small Business Stock Treatment

Given the large tax benefit available, Congress imposed several requirements a company must meet in order to qualify as a Qualified Small Business (QSB). The key requirement is that the company must be organized as a C-corporation. S-corporations do not qualify, and pass-through entities (partnerships, LLCs) must convert to a C-corp. Though there are additional important nuances, the main corporate requirements are:

- Gross assets cannot exceed $50 million prior to or immediately after issuing stock. For the purposes of this test, assets other than cash are valued based upon their adjusted basis rather than fair market value.

- The corporation must use 80% of its assets in the active conduct of one or more “qualified trade or businesses” as defined in IRC Section 1202(e)(3). Assets for the purposes of this test are valued based upon their fair market value. Unlike #1, this requirement must be satisfied throughout the stock holding period.

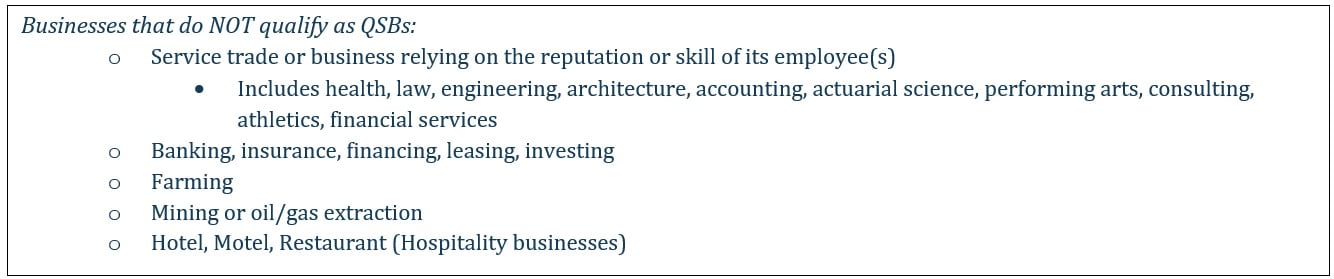

- The corporation must be a “qualified trade or business” defined as any business not specifically excluded in IRC Section 1202(e)(3) and summarized in the table below:

Investor Requirements for QSBS Treatment

In addition to the requirements above at the corporate level, there are specific investor requirements to be met as well:

- The investor must be an individual, trust, or pass-through entity. Corporate investors do not qualify.

- The stock must be acquired at original issuance as compensation or in exchange for cash or property. Acquisition through the secondary market does not qualify. Options, restricted stock units (RSUs), and convertible debt are considered original issuance.

- The investor must hold the stock for five years or longer.

Common Real-Life Issues for QSBS Investors

Holding Period

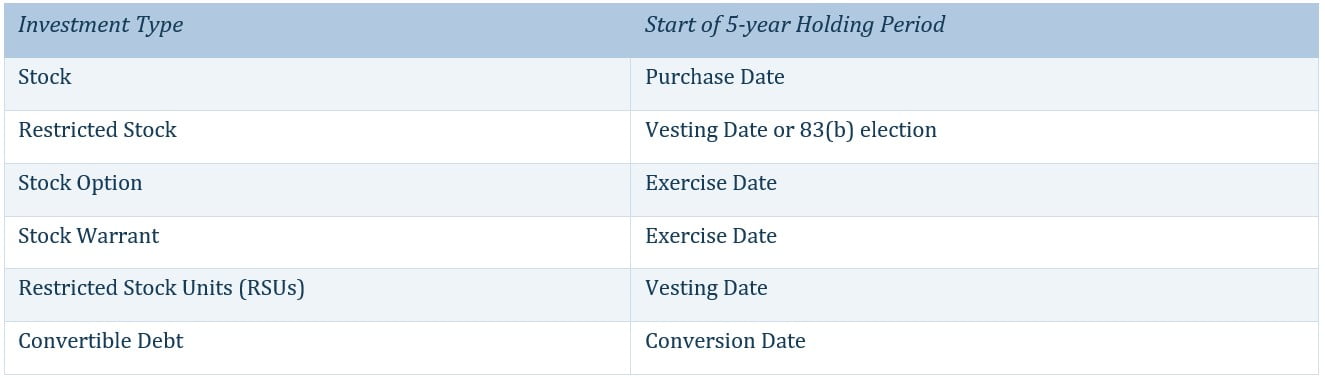

A common question that arises and can cause significant confusion pertains to when the holding period for an investor of Qualified Small Business Stock begins. While straightforward for normal stock purchases (the purchase date is the beginning of the holding period), shares acquired via other methods require close attention. The table below summarizes the holding period “trigger” for restricted stock, options, warrants, Restricted Stock Units (RSUs), and convertible debt.

Consider John who received restricted stock as compensation from his QSB eligible company in 2011. It has a cliff vesting schedule that vests 100% after four years. Because John did not make an 83(b) election within 30 days of the grant date for his restricted stock, his holding period for QSB purposes only starts upon receipt of the fully vested shares four years later in 2015! For company founders and early employees, making an early 83(b) election can be very important in the right circumstances and beneficial for QSBS purposes.

Acquisition by a Non-QSB Company

Suppose you have held QSBS stock for four years, shy of the 5-year holding period, and your company is acquired by a public company that does not qualify as a QSB, and your shares are converted to shares in the new public company. Is all for naught? The good news is that your shares can still qualify for the QSBS exclusion, but only to the extent of your gain at time of the acquisition.

Continuing the previous example, John’s company is acquired by a non-QSB eligible public company in 2019 (4 years after his restricted stock vested in 2015). The shares are worth $5 per share at the time of acquisition. John holds the stock an additional year and sells the public company’s shares for $10 per share. John’s gain on the sale qualifies for the QSB exemption, but only up to the $5 per share value at the acquisition date. John owes capital gains taxes for any gain above the $5 acquisition price.

Redemptions of QSB Stock

If applicable, be very cautious in allowing redemptions of Qualified Small Business Stock to existing shareholders (or their relatives). Doing so runs the risk of disqualifying the entire stock issue that was not redeemed. Section 1202 contains provisions disqualifying the stock if a) greater than 5% of the company stock is redeemed within one year of issuance, before or after and/or if b) greater than de minimis redemptions are made within two years of issuance, before or after. There are exemptions for termination of an employee, death, divorce, and disability, but tread carefully.

Pass Through Entities (VC & PE Investors)

QSBS tax benefits are available to investors holding QSBS via pass-through entities. IRC Section 1202(g) explicitly allows this so long as the original corporate and investor-level requirements are met. The pass-through entity must hold the stock for at least five years, and the underlying stock must meet the corporate requirements discussed previously for the entire holding period. Individual investors must also have been a partner/member of the pass-through at the time the QSBS was acquired and through the stock sale.

Qualified Team and Documentation

This post is not meant to be an exhaustive list of requirements, and the Qualified Small Business Stock provisions can seem overwhelming. The most important items are working with a knowledgeable team, including a financial advisor, accountant, and lawyer experienced in this area. Good advice here is well worth the cost. In addition, securing proper documentation is critical, especially when multiple rounds of financing are involved. This is easier said than done, but another reason to rely on a competent team you trust.

Article By Kevin Brady, CFP®

Wealthspire Advisors LLC is a registered investment adviser and subsidiary company of NFP Corp.

This information should not be construed as a recommendation, offer to sell, or solicitation of an offer to buy a particular security or investment strategy. The commentary provided is for informational purposes only and should not be relied upon for accounting, legal, or tax advice. While the information is deemed reliable, Wealthspire Advisors cannot guarantee its accuracy, completeness, or suitability for any purpose, and makes no warranties with regard to the results to be obtained from its use. © 2021 Wealthspire Advisors

Certified Financial Planner Board of Standards, Inc. owns the certification marks CFP®, Certified Financial Planner™ and federally registered CFP (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.