April 8, 2016

By Steve Blumenthal

“The Fed may succeed in stretching this cycle until 2017. But sooner or later it will have to grasp the nettle, and then we will discover how much monetary pain can be taken by a dollarized global economy with post-QE pathologies and total debt ratios some 36pc of GDP higher than in 2008.

So enjoy tactical rallies if you dare. But seven years into a profitless bull market is not a time for greed.”

In my view, the bet today comes down to this: you believe the Fed can hold the market up (aka “the Fed Put”), you believe politicians can accomplish structural reform and you believe that the same holds true in Europe, China and Japan. Essentially, “whatever it takes” wins. Alternatively, you believe that extremely high equity market valuations matter, excessive debt is problematic and that it is ultimately impossible for central bankers, try as they might, to repeal economic business cycles.

[drizzle]Over the last four plus years, any whiff of higher rates has put the market into a tail spin. All periods have been followed by more dovish Fed comments. For now it remains “all ‘bout that Fed.” My best guess is that it will be wage and core inflation that forces Fed’s hand. To that there are some stirrings but nothing major on the inflation front to fear just yet. But before that takes flight, keep in mind that the Fed believes interest rates should be 1½% higher today. The systematic imbalances are plenty. The tipping point may likely be higher rates.

At the beginning of every month, I like to look at the most recent month-end valuations. It gives me some sense of just how much risk is embedded in the markets and also a good feel for what the probable 10-year annualized forward returns are likely to be.

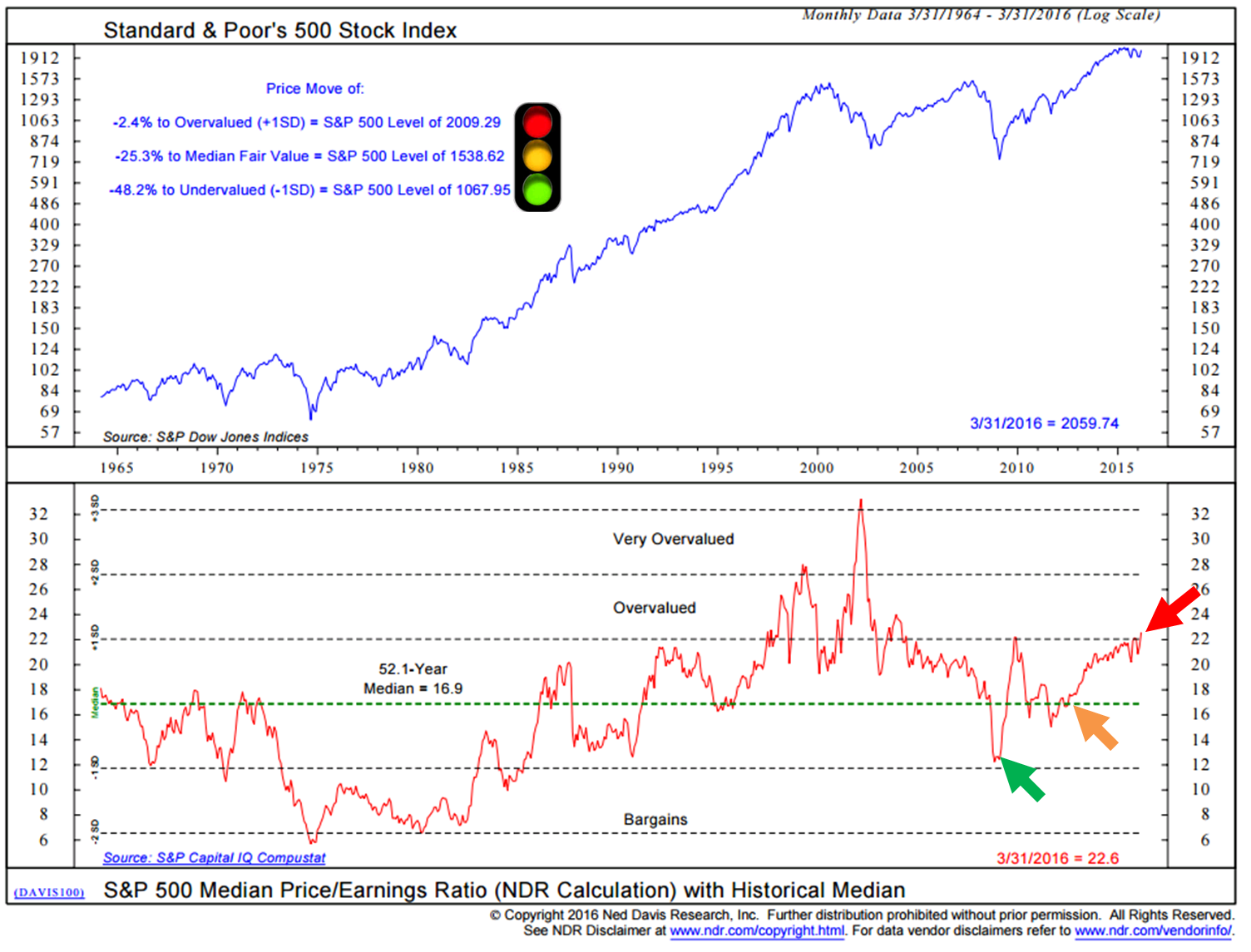

I mentioned in last week’s piece that the valuation numbers would likely come in higher and boy, did they! Median price-to-earnings ratio (my favorite measure) came in at 22.6. We sit at a higher level than the market peak in 2007.

For now, we collectively bow our heads to the Fed – and the ECB, JCB and CCB. But, as is taught in the world’s top business schools, valuations do matter. They are a powerful and reliable determinant of long-term investment returns.

Warren Buffett is famous for saying his family loves hamburgers and when they are expensive to buy, they weep, but when they are inexpensive to buy, they sing the Hallelujah Chorus. What he is saying is that investors should think about the market the same way. You’ll find his favorite valuation measure below. Hint: “PPB” pretty pricey burgers.

So this week, let’s look at valuation’s measures, take a sober look at margin debt and I share a short and fun clip that explains the Panama Papers. I think you’ll love it.

Also, as a quick aside, I was interviewed by Gregg Greenberg on TheStreet.com this week. I talked about gold and I shared what we are seeing in our tactical work (to view the short interview, click on the picture).

Ok, grab a coffee and let’s take a look at current valuations and margin debt.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- Valuations – A Powerful and Reliable Determinant of Long-Term Investment Returns

- Margin Debt – This Indicator Suggests Caution

- The Panama Papers

- Trade Signals – Steady as She Goes

Valuations – A Powerful and Reliable Determinant of Long-Term Investment Returns

Let’s start with median price-to-earnings ratios (P/E) and then take a quick run through of several other valuation measurements.

I like median P/E because it is based on the actual reported earnings of the S&P 500 constituents and it tends to remove special accounting maneuvers. By process, the outliers (those companies that show crazy-expensive P/Es and crazy-cheap P/Es) are eliminated. Think of it this way, the median is the P/E that is in the middle of all the reported outcomes.

As I showed in last week’s post (here), we can look at each month’s median P/E throughout history and see what it was on any given month and what the annualized returns were 10 years later. So simply, I believe median P/E can give us a real good sense for how well we’ll do over the coming 10 years. Sing hallelujah or weep?

Over the last 52.1 years, the median P/E for the S&P 500 Index was 16.9. So at 22.6, the S&P 500 index is currently 25.3% above its median fair value. Today, based on this measure, fair value for the S&P 500 Index is at 1538.62. I wouldn’t be surprised to see a correction that takes us to that level. Then, we can buy more burgers and sing.

What I also like about the following chart is that it shows overvalued levels and undervalued levels. Now the market could certainly overshoot both on the upside and on the downside, but what I like is it gives me a good sense of risk and reward.

Note the traffic sign I copied onto the chart (upper left) – red light, yellow light and green light. The market is overvalued at 2009.29 (red light). Note too that it ended March above that number closing the month at 2059.74. The market is fairly valued at 1538.62 (yellow light) and extremely inexpensively priced at 1067.95 (green light).

We want to be in a position to buy all we can when the light turns green. That won’t happen if we don’t know when to play offense and when to play defense. During high valuation corrections, aggressive investors will get run over on the way to that opportunity, leaving themselves few resources to buy the burgers when the buying gets good.

Median P/E:

Source: Ned Davis Research (NDR) (with stop sign and arrows added)

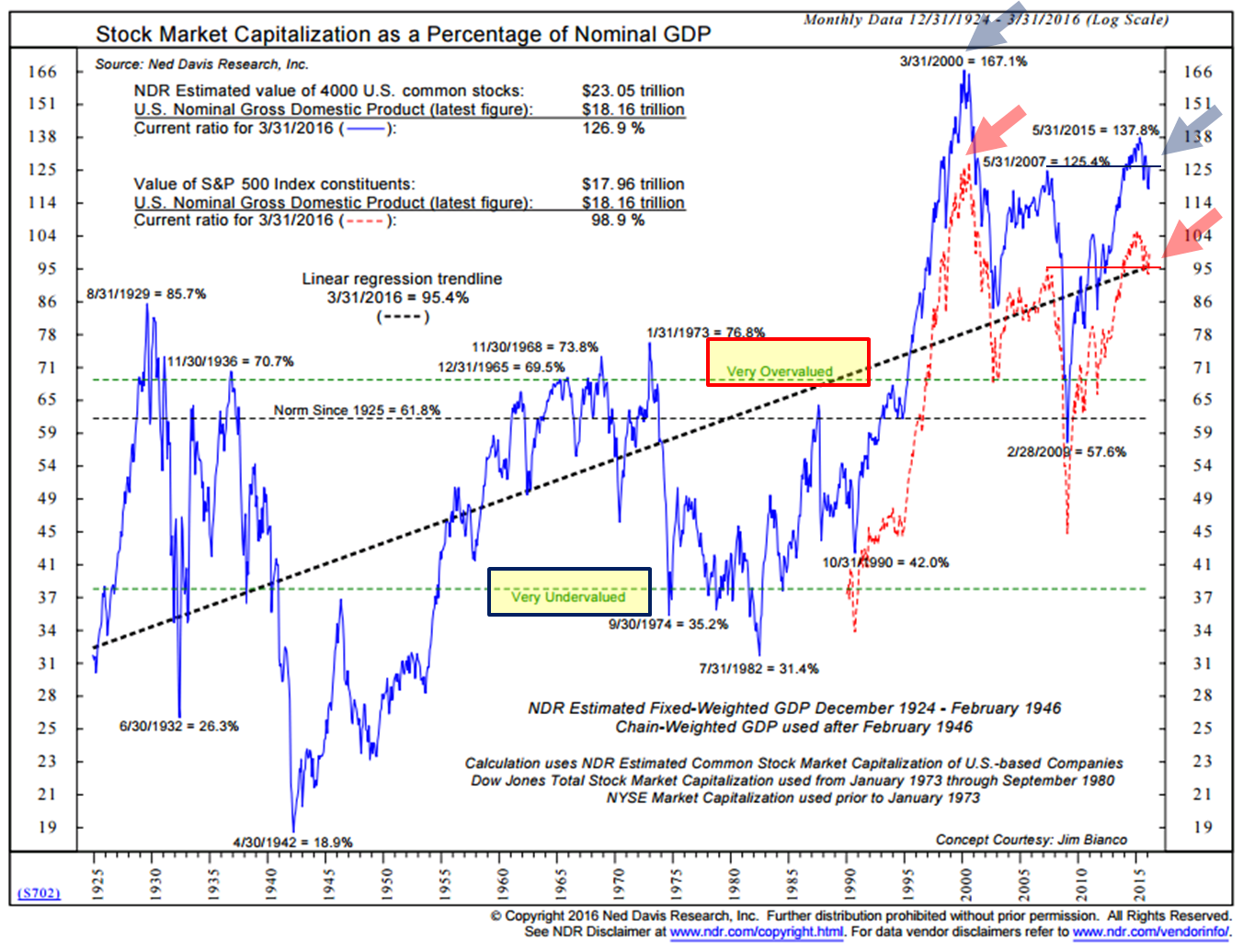

Warren Buffett’s favorite (as he stated in a 2001 Fortune Magazine article) valuation measure is Total Stock Market Capitalization as a Percent of GDP.

Here is how you read the next chart: The yellow highlighted areas show the levels above which or below which the market is “very overvalued” or “very undervalued.” The light blue arrows show the estimated value of 4,000 stocks (as calculated by NDR) in 2000 and 2016. The light red arrows show the value of the S&P 500 stocks in 2000 and 2016.

Several takeaways:

- both markets peaked in 2016 at higher levels than were made at the markets’ high in 2007

- 2000 was an outlier in my view (unprecedented valuations)

- both the 4,000 stocks and the S&P 500 are well into the “very overvalued” zone

- better buying opportunity will be found between 50 and 60 (vertical right side of chart)

The analyst/portfolio manager, John Hussman, charts the information as follows: using the total capitalization of the S&P 500 Index, according to his research, expect a mere 2% annualized returns over the next 10-12 years.

Source: Weekly Market Comment, “Run-Of-The-Mill Outcomes vs. Worst-Case Scenarios,” John P. Hussman, Ph.D.

Now that I’ve totally depressed you, let’s take a look at a few additional valuation metrics.

Prices-to-Sales – Higher than 2007 and any other time with the exception of the end of the greatest bull market that ended in March 2000.

Next is a look at Price-to-Operating Earnings. Note that the average value since 1926 puts the S&P 500 level at 1448.35. Overvalued based on data back to 1926 puts the S&P 500 level at 1830.56.

Some additional data points (in summary): Also “extremely overvalued” are the following: price-to-GAAP earnings, Shiller P/E, price-to-forward earnings, price-to-sales, price-to-book and even dividend yield. There are a few valuation bright spots, but they are not on my personal radar – “Extremely undervalued”: net repurchase yield, net payout yield and free cash flow to enterprise value.

Finally, on the valuation front, I’m often asked about forward P/E. I just don’t like it because the estimates are just that – they are based on Wall Street’s earnings estimates and those estimates are almost always revised lower. Thirty-plus years in the business and all I can say is it may help Wall Street sell stocks, but it is not reliable and what you’ll see next is that what may look cheap is really not cheap.

Forward P/E and history:

- Forward P/E, as of April 6, 2016, is estimated at 15.9

- 15.9 might look like a better number than median P/E of 22.9 but that is not correct

- Forward P/E should be compared to the forward P/E numbers from other points in time. Likewise, median P/E should only be compared to historical median P/E.

- In the next chart, you can see the forward P/E (green dot, upper right) is higher than it was at the market peak in 2007. Then it peaked at 15 times earnings.

- Also note: forward P/E reached 22 in March 2000 (frankly, I doubt we’ll see that extreme overvaluation again… at least in my lifetime. But hey, I could be wrong. It’s a bad bet – I just don’t like the odds).

- Finally, take a look at the percentage gains and losses over the last 20 years.

High prices and declining profit margins (declining earnings) do not mix well for investors.

As you can see in the yellow highlighted section at the upper left of the next chart, the economy does not do as well when profit margins are declining. In this way, think of equities as an important leading indicator.

Summing up the current state: Part of the problem is that corporate earnings peaked in the second quarter of 2015. Another part is that debt financed equity buybacks have helped drive equity market prices higher.

Lower earnings and higher prices mean we get a higher P/E ratio – or expensive hamburgers!

As a quick side note, historically, recession typically starts five to seven quarters after the peak. Keep that one top of your mind, though there is no sign of a U.S. recession right now. Let’s look at several “recession watch” indicators next week.

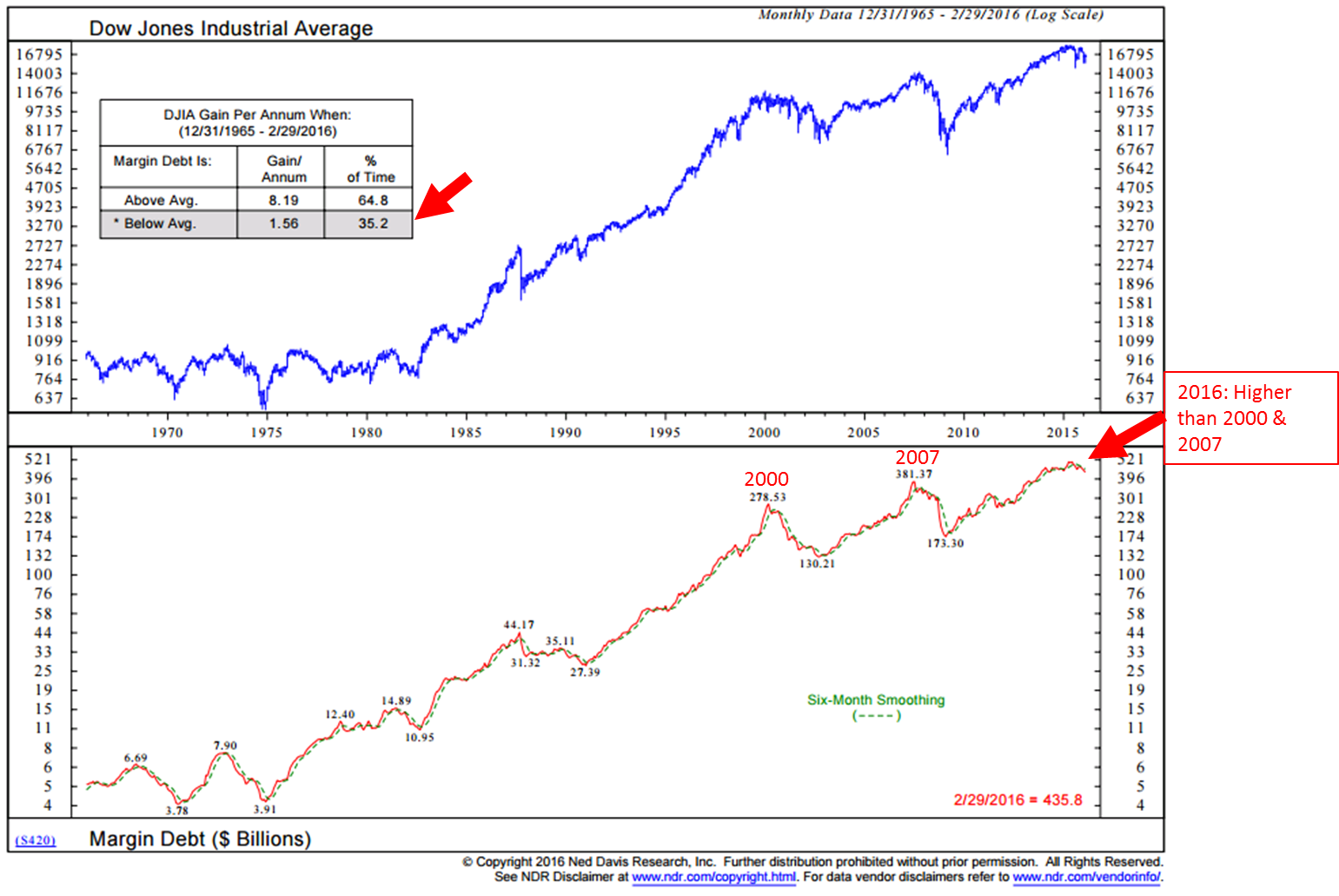

One last area that causes me concern is the high level of margin debt. I don’t know if it is from individuals borrowing from their stock brokerage accounts similar to how they used home equity lines of credit at the peak of the housing bubble or if they are aggressively invested in stocks but high margin debt – high any debt can be problematic.

When you combine overvalued markets with declining profit margins, high margin debt and questionable liquidity, markets have the tendency to unwind quickly. Declines trigger margins calls and in many cases this causes forced selling to meet those calls. Forced selling may trigger additional margin calls, which triggers more forced selling. More sellers than buyers… other buyers step out of the way and thus waterfall-like declines occur.

Hedge that equity exposure.

Margin Debt – This Indicator Suggests a Bear Market is Now Underway and It’s Likely to be a Painful One

MARCH 31, 2016 by JESSE FELDER

“NYSE margin debt fell again during the month of February. After the selloff in stocks that kicked off 2016, this should come as no surprise. Investors are usually forced to reduce leveraged bets during these sorts of episodes in the stock market. In fact, this forced selling can actually exacerbate the volatility. And because margin debt is only now beginning to come down from record highs, surpassing those seen at the 2000 and 2007 peak, this should be of concern to most equity investors.

To fully appreciate this risk, I prefer to look at margin debt relative to overall economic activity. When leveraged financial speculation becomes large relative to the economy, it’s usually a sign investors have become far too greedy. As Warren Buffett would say, this is usually a good time to become more fearful, or conservative towards the stock market.

Not only did margin debt recently hit nominal record-highs, it hit new record-highs in relation to GDP, as well. In other words, over the past several decades, investors have never become so greedy as they did recently. And yes, this includes the dotcom bubble.

One reason I prefer this measure is that it has a fairly high negative correlation with forward three-year returns in the stock market. When investors become too greedy, returns over the subsequent three years are poor and vice versa. As of the end of February, the latest forecast implied by this measure is for a loss of about 35% over the next three years.

While this measure is pretty good at forecasting three-year returns, that doesn’t help much for investors concerned with the next year or so. In this regard, it may be helpful to observe the trend of margin debt. Where is the nominal level of margin debt relative to its 12-month moving average or simply its level from one year ago? Historically, when these indicators turn negative from such lofty levels, a bear market, as defined by at least a 20% drawdown, is already underway. Right now, both of these measures are, in fact, negative.

So margin debt right now is sending a very clear signal that investors have recently become very greedy. This suggests returns over the next several years should be very poor. Finally, the trend in margin debt also suggests that a new bear market is likely underway. If history is to rhyme that means a decline of at least 20% in the S&P 500 is very likely to occur sometime soon. And, because of the sheer size of the potential forced supply that could come to market in this sort of environment, that could easily be just the beginning.”

Source article

Here is another look at margin debt – higher than 2000 and 2007 and below six-month smoothed moving average: Specifically, take note of the comparative levels of margin debt in the lower section in next chart.

It is when it starts to roll over that we should stand up and take note (and it’s rolling over – red arrow).

The Panama Papers

I thought this tweet was great:

I retweeted this next article from Ambrose Evans-Pritchard earlier this week. He has a masterful way of explaining things. See Panama bombshell spells demise of shadow finance, and privacy.

You can follow me on twitter here.

[/drizzle]