Research shows news analytics can provide an added dimension to Italian sovereign debt analysis – what can it tell us about the impact on markets of the recent crisis in the Camera?

Q4 2020 hedge fund letters, conferences and more

One area where investors are increasingly exploring the use of alternative data is in the highly news-sensitive sovereign bond market.

The Effectiveness Of News Sentiment

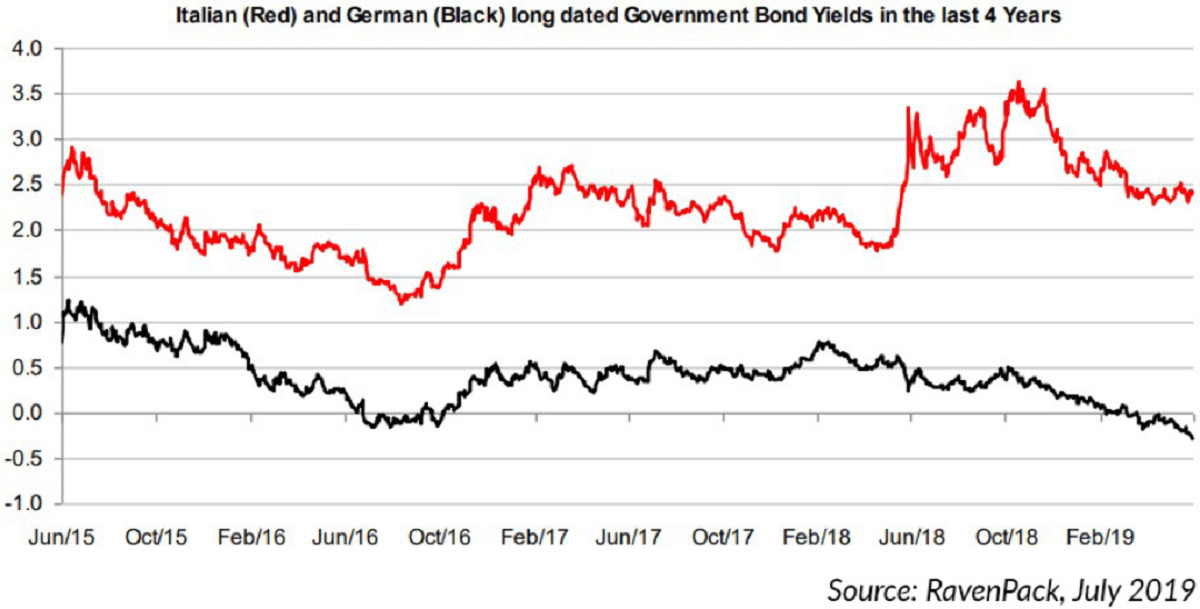

Past research has shown the effectiveness of news sentiment for forecasting sovereign bond yields - a measure of a bond’s value that takes into account changing economic conditions; yields move inversely to bond prices, and reflect inflationary expectations and default risks.

In 2019, RavenPack, a leading provider of news analytics data produced a White Paper in which its analysts compared a strategy that traded the spread between German bunds and Italian sovereign bonds (BTPs) using a news analytics model with a simple buy-and-hold strategy.

The study focused on a volatile period during the 2018 Italian general election when the country voted in a Eurosceptic coalition. The results showed that the news-based strategy outperformed the buy-and-hold one.

In that case, BTP yields rose during the crisis because of the greater risk to bond-holders associated with the election of a Eurosceptic government and Italy leaving the Eurozone.

According to experts, the two main factors driving the rise in yields were fears of the readoption of the Lira, which would overnight reduce the value of existing Euro-denominated bonds, and the risk that populist policies would result in a ballooning fiscal deficit.

The Effect Of The Political Crisis On Italian Sovereign Debt

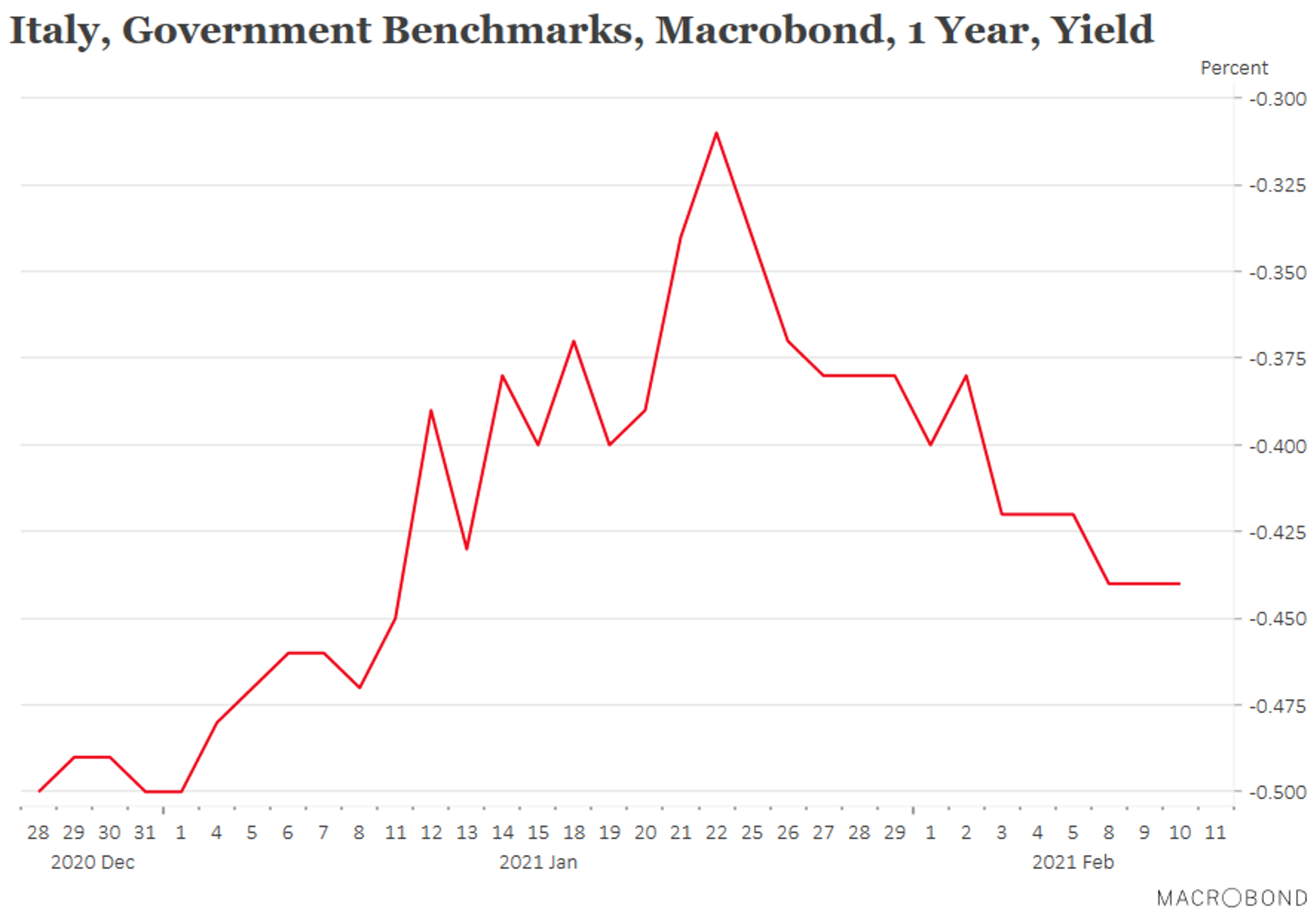

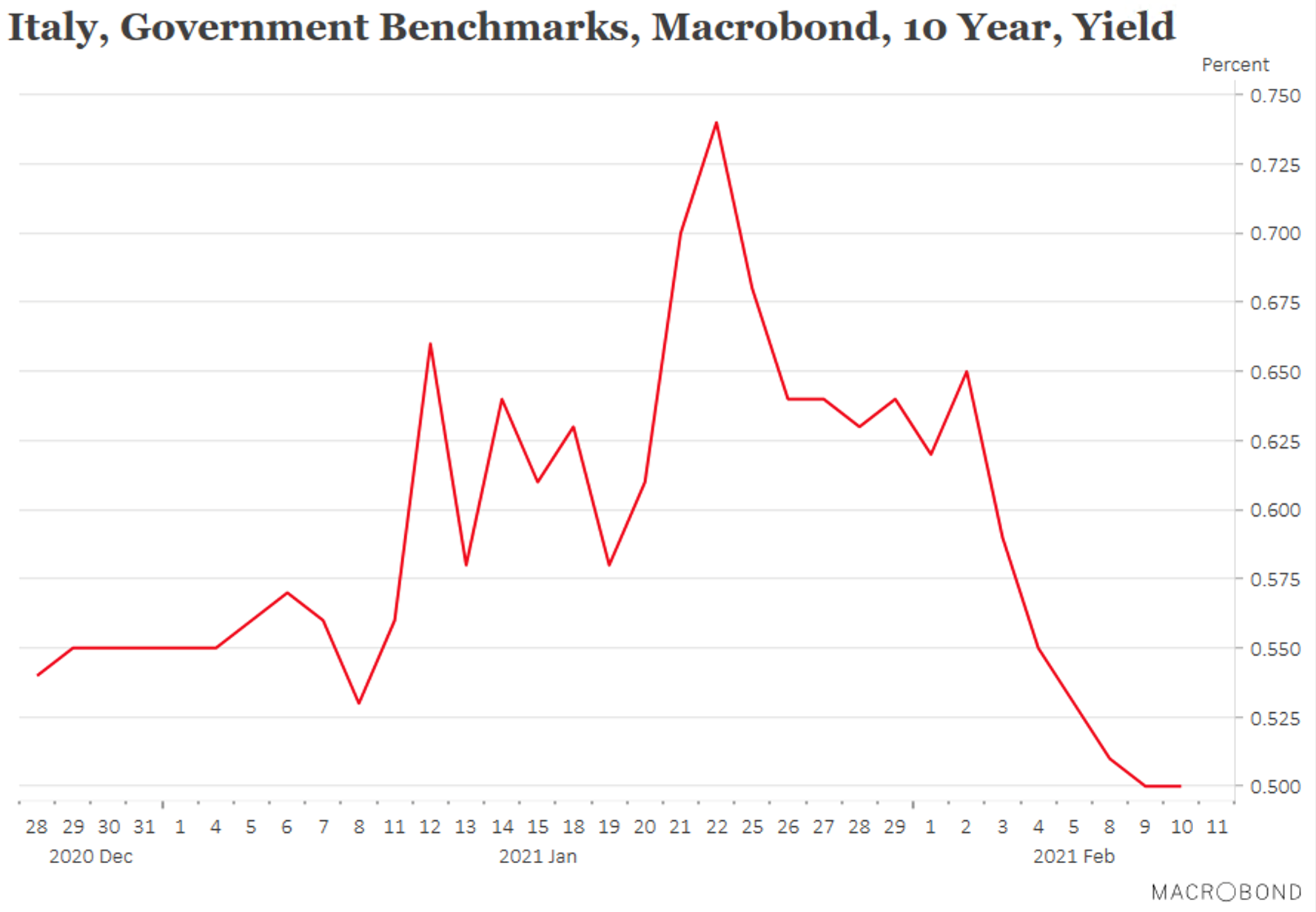

Interestingly enough, the latest political crisis in Italy, which has been playing out at the start of 2021 - in which the fragile coalition led by Guiseppe Conte unraveled because of differences in spending priorities - has had a more ambiguous effect on Italian sovereign debt.

Here, instead of BTPs just devaluing, bondholders have seen the value of their holdings fluctuate; at the start of the crisis bond prices fell (yields rose) before peaking on January 22nd shortly before Prime Minister Conte resigned. After that bond prices rose (yields fell sharply), in a ski slope down move as the crisis evolved to its final resolution stage.

The charts of Italian 1 and 10-year bond yields below clearly show this waxing and waning effect around the peak.

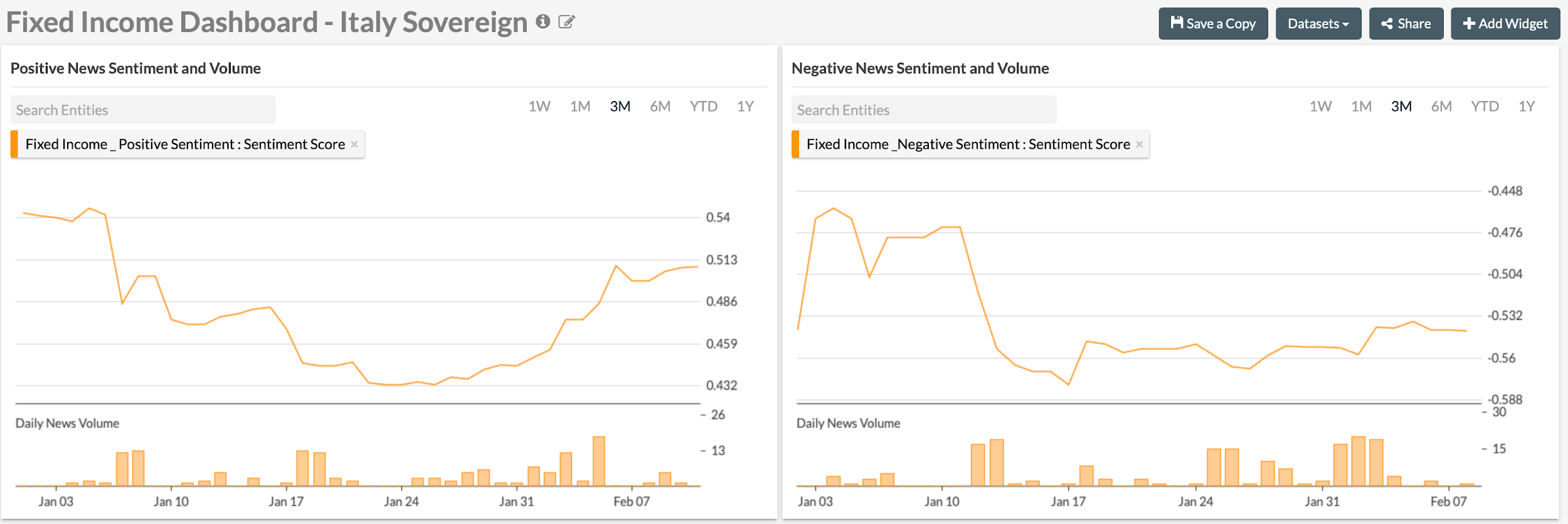

The surprisingly positive reception by bond markets to Prime Minister Conte’s resignation on January 26 is also reflected in RavenPack news sentiment for Italian fixed income, represented in the two charts below, taken from our news analytics platform.

News sentiment for Italian sovereign bonds is shown divided into two charts: positive and negative - something academic research has found useful when building predictive fixed income models - with the two different modes being more or less significant during different business cycle phases.

At the same time as bond yields pivoted around the 22nd of January positive FI news sentiment bottomed and also changed direction. It then rose, and rose sharply, tracking the fall in yields. Negative sentiment, meanwhile, remained relatively flat and then became less and less negative as time went on, as can be seen on the chart on the right.

Markets Digested The News Of Conte’s Resignation

During the last days of January, both sentiment and BTPs steadily recovered as markets digested the news of Conte’s resignation. One possible interpretation for the recovery is that markets took the resignation as the culmination point in the escalation in political instability of the prior period, and the beginning of the path towards resolution - but there may have been other factors at play too, as we shall see below.

What is clear, is that the key factor at play at the start of February when sentiment accelerated higher and bond yields lower, was the entrance on stage of a new character in the drama. This happened when, into the vacuum left by Conte’s coalition, stepped a towering figure of international finance in the form of Mario Draghi a.k.a “Super Mario”, the former head of the European Central Bank (ECB), the man who did “whatever it takes” to save the Euro.

The rapid improvement in both bond markets and sentiment at this time clearly reflected investors confidence in ‘Super Mario’s’ credentials.

It also partly explains why bonds reacted in the opposite way in the 2021 crisis to that of 2018 - Draghi represents the antithesis of the Eurosceptic government that won the 2018 elections. There is no-one less likely to take Italy out of the Euro than the man who vowed to save the Euro.

Draghi was invited to the Quirinal Palace by President Matarella on Wednesday February 3 and asked to form a new government. On the following day Draghi officially accepted the offer. Since then he has secured the support of a broad-based bi-partisan coalition of parties including the anti-establishment 5-star and Northern League. During this period, positive sentiment rose even more sharply, and yields fell with equal strength.

The Draghi-Effect

When did the Draghi-effect begin? Could speculation and rumours about Draghi have influenced markets ahead of time, and might they be responsible for kicking off the trend in late January?

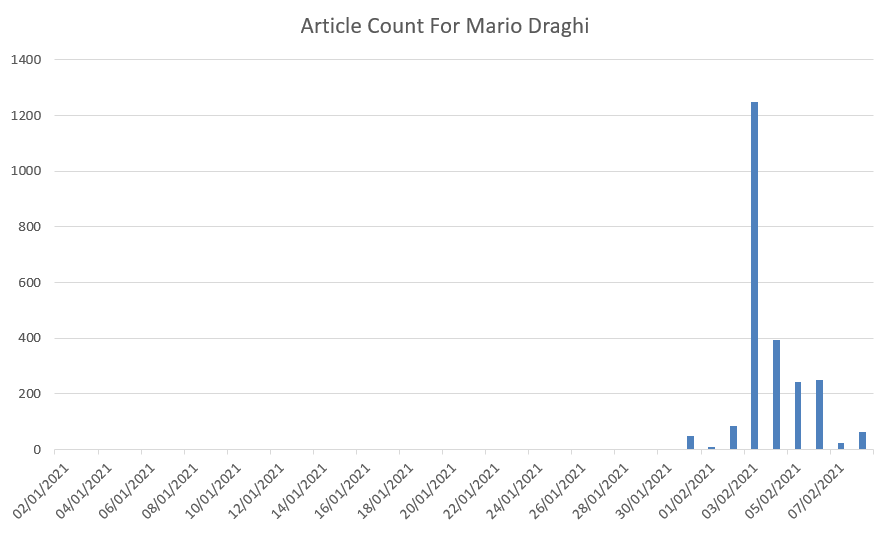

We can use RavenPack news analytics to check out this hypothesis by creating a dataset that counts the number of articles mentioning Draghi per day.

If we were to find a flurry of articles in late January containing speculation and rumours of Draghi’s appointment we might conclude that this was a factor.

Conducting such a count proves revealing. Between January 1 2021 and January 31 there are only 2 articles about Mario Draghi.

The first was published on January 5 and the second on January 26. After that there were none until January 31 when the number suddenly jumped to 48 as speculation of his succession became more widespread. The number then jumped to 1247 on February 3 when he was courted by Mattarella. This is shown in the chart below. Note that the two mentions prior to the start of the main surge don’t show up very clearly because of the scale.

Draghi Being Conte’s Successor

The question is, did either of the two articles on the 5th and 26th contain speculation or rumours about Draghi being considered as a candidate that might suggest this was a factor?

One of the powerful features of the RavenPack platform is that it allows users to drill down to an individual article level so it is possible to check what these two articles prior to the main surge were about.

Interestingly, what we find is that both the article on the 5th and the 26th contained speculation that Draghi might be next in line for the premiership.

The article on the 5th, in a publication called Euractiv, bore the headline “Mario Draghi to replace Conte? Virus-hit Italy gripped by political crisis”, and contains the following line about Draghi: “Former European Central Bank president Mario Draghi is often mentioned as a possible saviour for the country, but he has shown no appetite for a political career, at least in public.”

The article on the 26th, on a website called Veteran’s Today, also contained speculation about Draghi being Conte’s successor. It bears the headline “Italy: PM Conte Resigned. New Government with former ECB President Mario Draghi?”. The story contains a paragraph in which Silvio Berlusconi appears to endorse Draghi as a possible leader, and a revealing photo of the two, that seems to evidence the point.

“While Silvio Berlusconi, Forza Italia center-right wing party’s leader, did not even wait for the formalization of his resignation to open the doors to a government of national unity that already has the flavor of a great partnership with the Democratic Party in view of a “technical” candidate like Mario Draghi, former European Central Bank president.”

The contents of the two articles prior to the main surge in speculation about Draghi on January 31 - when the story really ‘broke’ for the international media - suggest rumours were already circulating prior to his official appointment. Whilst this does not explain the surge in yields prior to the January 22 market top, the reporting of Berlusconi’s vocal support on the 26th suggests rumours at that time were gaining traction, and that this may have been a contributing factor in the relatively strong performance of Italian sovereign bonds during the last week of January.

It was during this short period that there was a vacuum and no successor, a situation which might normally be expected to cause a deterioration in the bond market, however, one might speculate that a contributing factor to its improvement, may have been the shadow cast by Draghi waiting in the wings!