Traditionally used by hedge funds to drive alpha-generating strategies, news analytics data also has applications for assessing financial market risks, as the deep-dive into the research below shows.

Q1 2021 hedge fund letters, conferences and more

Before ordering in the Moet it’s always a good idea to make sure your back is covered, and as every professional money manager knows, an accurate assessment of the potential downside to any given position is an integral part of the job, especially in the current regulatory climate.

The investment game is a bit like poker; to be good you don’t just need to know the odds but you also need to be able to read the opponent’s hand - not just so you can win but also so you can know when to cut your losses; and to do this successfully players employ all the information at their disposal.

As such, we thought it would be useful to look at whether news analytics data - a type of alt data generated by scanning thousands of news articles online - can help portfolio managers get a better picture of the downside risks to their positions.

Obviously, the news has a highly reflexive relationship with asset prices; driving, and in turn being driven by them; and this would suggest this type of data could be of great value, but to what extent and in what ways can it be useful?

To help us answer these questions, RavenPack’s data science team wrote a white paper on the subject, which we have summarized below.

We hope it provides an assessment of the downside risks, if any, of not incorporating this type of data into your decision-making.

No Reward Without Risk

Volatility is a double-edged sword. When positive it can be a gold mine for traders; when negative a Balrog chasm in Moria. Without it, traders can’t turn a profit, but along for the ride comes a healthy dose of liability. How then, if at all, can news sentiment help investors get on the right side of this tricky customer?

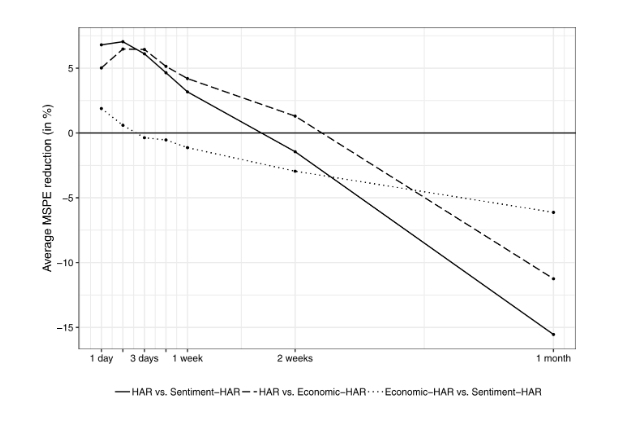

Most but not all volatility is caused by the news so it seems to be an area ripe for the use of news analytics. Research by Audrino et al proves the efficacy of news as a forewarner of intraday volatility after results showed news sentiment produced a lower forecasting error than economic data.

The chart below shows the reduction in error rates versus other models (HAR etc.). The sentiment-enhanced model is represented by the most granular dotted line.

Retail traders are more jittery according to Research by Ballinari et al who wanted to investigate whether the amount of volatility caused by news depended on who was reading it. His conclusions were that the higher the percentage of retail investors responding to a particular news story - when compared to institutional investors - the higher the volatility.

What sort of news causes long-term volatility? The question was the subject of a study by Ho et al which concluded that company-level news produced lengthier periods of volatility compared to macro-economic news; and negative news played out for longer than positive news.

Domino Effects

Scaling the peaks of the market engenders risks, not just for individual stocks but also for all those companies linked to the stock whether by supply chain or other means. What part can news analytics play in identifying and assessing the risks inherent in these relationships?

The news can be used to map company interrelationships. News analytics platforms such as RavenPack’s can count co-mentions of companies in the news together, and then these can be used to map relevance, as illustrated in research by Balash et al. In network diagrams the nodes represent individual companies and the thickness of the connections the degree of reflexivity (measured by co-mention volume) between them.

The advantage of using a news-based approach is that it can capture hidden relationships. Often companies are reluctant, or otherwise not required, to divulge their business relationships, whereas journalists tend to dig up hidden interconnections whether arising from deals, litigations or changes in the supply chain.

Running With the Pack

To properly analyse risk it is also necessary to assess the extent to which companies diverge individually from broader market trends. Think how the wind might impact all sailboats in a similar way but that each vessel will also react in its own idiosyncratic style. The degree of a stock’s individual divergence is known as beta, or ‘systematic risk’.

Research by Dang et al has shown that news sentiment is a key determinant in the extent to which company returns and liquidity move in concert or not with the broader market. His conclusion was that, “The comovement between firm-level and market-level sentiment is one of the underlying sources of related return and liquidity co-movement.”

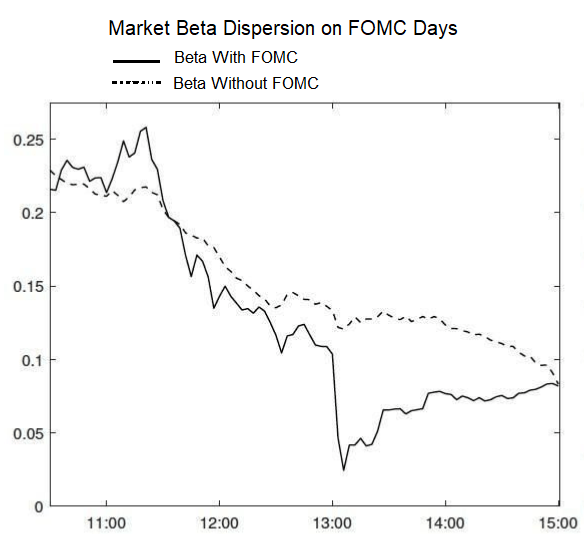

An attempt to model beta and assess systematic risk was the subject of another study using RavenPack news analytics, which made use of the platform’s entity and event detection capabilities to identify events such as earnings releases and FOMC announcements.

The news data highlighted how stock betas deviated considerably from their initial values at the time of FOMC announcements as shown in the chart below.

How news sentiment compares to other means of forecasting beta was the subject of a paper in which researchers pitted sentiment against 80 other variables for predicting systematic company risk. A horse-race between models ended with the news-based model coming out on top.

Of Bonds and Words

Though traditionally seen as a cast-iron guarantee, the reputation of bonds has suffered in recent years due to the sovereign debt crisis of 2012, suggesting methods for assessing risk remain pertinent.

A major source of volatility stems from the relative illiquidity of bond markets given the often large trade sizes. The ability to time liquidity is, therefore, crucial in avoiding adverse market movements and reducing risk.

Thankfully, news sentiment can warn of volatility to come, according to research by Jiang et al, which found there exists a negative correlation between news flow and adverse market movements.

One cause stipulated was the rebalancing of a high default level of information asymmetry between so called informed and uninformed investors during periods of high news volume - with the release of firm-level news alleviating this asymmetry.

Other research has looked at how news sentiment can be used to assess country risk in the sovereign bond market. Research by Erlwein-Sayer showed that the inclusion of variables from news enhanced the forecasting accuracy of sovereign bond risk.

The study took the sovereign bonds spreads of five European countries and showed how incorporating news sentiment from relevant entities and macro-economic topics improved the prediction of spread changes.

A further conclusion was that news sentiment was more effective in less stable compared to more stable economies.

The Credibility of Ratings

Credit ratings lost credibility after failing to alert holders to risk during the great financial crisis of 08/09. A flawed rating can lead to an inaccurate assessment of the credit-worthiness of either a company or nation. Research indicates news analytics can help in this regard, providing greater transparency and accuracy to ratings produced by the oligopoly of the ‘big three’ ratings agencies.

Research by Bonsall et al showed that companies with greater news coverage tended to benefit from more accurate ratings. Greater news coverage also led investors to better rate the credit-worthiness of institutions and had a positive feedback effect inducing ratings agencies to improve the accuracy of their ratings.

Changes to company credit ratings tend to have an impact on the volume and extent of their voluntary disclosures according to research by Basu et al, that made use of RavenPack’s detailed earnings guidance event taxonomy. The study concluded that downgrades tended to lead to more voluntary disclosures and upgrades to less.

The tendency of companies with very poor credit ratings to underperform was the subject of a paper by Gao et al. Using the Expected Default Frequency (EDF), a gauge of poor creditworthiness, to rank stocks, they found those in the lowest deciles also tended to exhibit relatively more negative news sentiment and therefore relatively lower returns, suggesting the news could provide a barometer of risk. The cause of low future stock returns was put down to investor overconfidence, in line with a behavioural approach.

ESG, Credit and the News

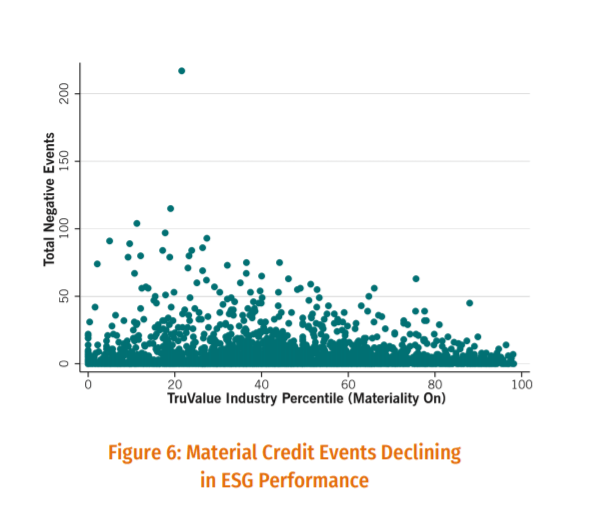

Given the high cost of fines and lawsuits, the question of whether a company’s Environmental, Social and Governance (ESG) rating impacts on its ability to pay its debts and therefore its credit-rating has also been the subject of research incorporating RavenPack news sentiment data in its methodology.

Henisz et al used RavenPack’s rich ESG event taxonomy to screen for company material credit events and then cross-referenced these to ESG scores. Their conclusion was that companies with poor ESG scores tended to experience a higher incidence of credit events.

As can be seen from the above research news analytics data provides a rich and varied number of novel approaches to assessing risk - suggesting investors might well be at risk from not taking the opportunity to invest in it!