McIntyre Partnerships commentary for the second quarter ended June 30, 2019.

Dear Partners,

The following letter is in our standard format with an update to positions, returns, and a write up on a new investment, Trinity Place Holdings (TPHS). However, subsequent to quarter end, the fund has significantly increased our investment in Chemours (CC), a stock which I have spoken about frequently. At present, the stock is quite volatile, and our results will be volatile as well. Given the significance of our CC investment, I plan to update investors again on my reasoning in a subsequent letter and presentation.

Q2 hedge fund letters, conference, scoops etc

McIntyre Partnerships Monthly Net Returns (1)

Performance Review - Q2 2019

Through Q2, McIntyre Partnerships returned approx. 7% gross and 7% net. This compares to S&P 500 and S&P 600 returns including dividends of 19% and 15%, respectively.

During the quarter, the fund gave up our strong Q1 performance as several large cyclical bets reversed, in particular CC and GTX. CC was also attacked by a short seller, who claimed the company could face insolvency due to its legacy legal liabilities. As I have taken an even larger investment in CC, I obviously strongly disagree with the short case and will be detailing my reasoning in a subsequent note.

In Q2, SMTA contributed ~300-400bps while FBHS and GTX contributed ~100-200bps, while CC lost ~750bps and LILAK and uranium lost ~100-200bps. YTD, FBHS and LILAK have contributed ~400-600bps while SMTA, GTX, and CBS contributed ~200-300bps. On the losing side, PTSB, CC and uranium have lost ~100-200bps each.

Portfolio Review - Exposures and Concentration

At quarter end, our exposures are ~135% long, ~35% short, and ~100% net. Our five largest positions were 87% gross exposure and our ten largest were 124%. However, SMTA is now a risk arbitrage investment where we expect the majority of the capital to be returned via cash dividend by year end. Excluding SMTA, our net exposure falls to ~80%.

Our five largest positions are CC, GTX, SMTA, uranium, and LILAK.

Portfolio Review - New Positions

During the quarter, the fund added a new position in Trinity Place Holdings (TPHS). We view the position as a relatively safe, albeit illiquid, investment where we stand to lose little if wrong and roughly double our investment if proven right. Further, we believe the majority of the investment will be realized in the next 12-18 months.

Please see our TPHS write up at the end of the letter.

As always, please feel free to contact me with any questions.

Sincerely,

Chris McIntyre

Appendix – Trinity Place Holdings (TPHS)

“Sometimes a Photo Is Worth a Thousand Words”

Elevator Pitch Thesis: If Building B is worth as much as Building A, we double our money

Thesis

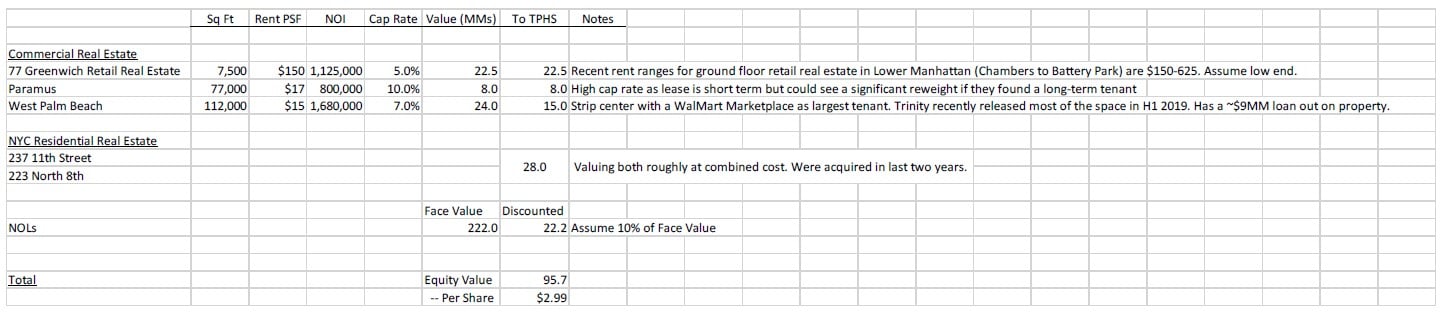

Trinity Place Holdings Inc (NYSEAMERICAN:TPHS) is a relatively simple “workout”-esque security. The ~$4 stock has ~$2.50-$3.00 in easily valued investments and one large other bet: a new build residential construction in lower Manhattan called 77 Greenwich that we believe will yield $3-$5+ in value by year end 2021, yielding a sum of the part (SOTP) of $5.50-$8.00, a 40-105% return in two years.

The critical variable in Trinity Place Holdings’s NAV is what average sales per square foot (PSF) 77 Greenwich ultimately achieves. Our $3-$5+ estimate corresponds to a $2,000-$2,500 PSF sales price, which we believe is adequately conservative versus recent comparable sales in the area. Construction of 77 Greenwich is already over 50% finished with completion scheduled for the second half of 2020. Marketing and sales commenced in Spring 2019 and are scheduled for completion in 2021. As the initial units are sold, we believe there is a possibility the market will see the relevant PSF marks for the asset and could reweight shares in advance of completion. We believe TPHS shares are an opportunity where we stand to lose little, if any, if our thesis is incorrect and stand to make a great deal if 77 Greenwich is sold inline with our projections. Further, we believe management will be good stewards of capital with the proceeds from 77 Greenwich. Management and the board are large shareholders who plan to pursue buybacks, dividends, or purchases of other stable NYC residential real estate.

Background

At first glance, investors may find it odd for an NYC residential development to be trading as a listed security. Virtually all NYC new build constructions are private deals, particularly at a sub-$1B size. Trinity Place Holdings’s existence owes to its odd, convoluted story. The stock was originally the old Syms and Filene’s Basement discount chain that filed for bankruptcy in 2011. After the reorganization, TPHS is the successor entity that emerged as a portfolio of real estate assets, NOLs, and one critical property – an old Syms location in the Financial District of Lower Manhattan that would eventually be redeveloped and become 77 Greenwich. Between 2015 and 2017, the company began development of 77 Greenwich and priced several rights offerings between $6-$7.50 per share as well as at-the-market offerings which sold shares with an average priced greater than $9. Through these offerings, famed investor Michael Price became TPHS’s largest shareholder with an ~21% stake.

Since the reorganization, Trinity Place Holdings has been a generally known value idea among microcap investors. We tracked the story over time but did not invest until recently. In Fall 2018, the broader equity markets declined and TPHS rolled over with them. Further, the crack in NYC real estate that began to emerge in 2017 worsened throughout 2018, drawing into question the high PSF sales targets of many NYC new developments. While the market has weakened since 77 Greenwich began planning in the mid-2010s, we believe TPHS shares are discounting a further worsening of the NYC real estate market that is unlikely to occur and have made TPHS a substantial position.

Other Assets

Before digging in to 77 Greenwich, we want to go through Trinity Place Holdings’s other assets, which establish the basis of our downside estimates. Here are our estimates:

We believe our above estimates are conservative. The NYC residential real estate was purchased in last two years into a strong NYC rental market and are located in growing areas: Williamsburg and Gowanus. The 77 Greenwich retail real estate will be street level and, while not exactly on the main corridor, will be brand new in area with a growing residential population and limited shopping. As a sanity check, according to REBNY, ground floor retail real estate in Lower Manhattan – Broadway (Battery Park - Chambers St) averaged $413 PSF in Spring 2019 with a $150-$625 PSF range while Harlem averaged $125 PSF, which compared to our estimate of $150 PSF. (https://www.rebny.com/content/rebny/en/research/retail/Spring_2019_Manhattan_Retail_Report.html) We believe there could be upside to our estimates.

Estimating the NOL is an odd endeavor as the result is reflexive. The NOL will be used to offset any gains from the 77 Greenwich project, thus if 77 Greenwich sells well, the NOL will be worth a lot, and if it sells poorly, the NOL will be worth very little. In the above NAV, we value the NOL at 10% of face value to reach a $3 per share value for the other assets. If we instead valued the NOL at close to zero, it would correspond with the low end of our $2.50-$3 other asset NAV.

77 Greenwich

Visit Website Here: https://77greenwich.com/

77 Greenwich is a new development luxury residential building located in Manhattan’s Financial District. The asset will have 90 condominiums, gym facilities, a roof top terrace with sweeping city and harbor views, and a school on the lower levels. From the company:

“77 Greenwich, a new residential condominium with a boutique approach to upscale urban living. 77 Greenwich was envisioned by a world-class team of New York-based architects and designers including FXCollaborative, the celebrated architectural firm behind acclaimed New York City residential developments including The Greenwich Lane and Circa Central Park as well as the new Statue of Liberty Museum; with interiors by Deborah Berke Partners of 432 Park.

77 Greenwich is a sculptural tower of reflective glass rising from a cast stone base. Topping out at 500’, the 42-story building features a pleated glass curtain wall façade that provides sprawling water views from each of the homes, which begin on the 15th floor located nearly 150 feet above street level, and offers a graceful juxtaposition to the heavy masonry of its historic neighbors. Designed to exacting LEED standards, the homes at 77 Greenwich are both environmentally sustainable and luxurious.”

While pretty pictures and elegant descriptions are nice, the real question is “what is it worth?” which in all honesty is a mixed bag. The bad news is that the market is definitely worse than when 77 Greenwich was originally planned. In the mid-2010s, a dearth of new construction following the Great Financial Crisis mixed with a strong NYC housing recovery to cause a surge in new development profits. Developers including Trinity began to dream of $3,000 PSF pricing, a previously unheard-of level. However, the market did what markets do and a surge of supply began construction a few years ago, which is leading to a supply glut at present. The Manhattan market has cooled significantly, with $1-$5MM homes down 10-20%, while certain high-end real estate is even worse.

The good news is that the market is not crashing like South Florida or Vegas in 2006-2009 and TPHS stock is already discounting a significantly worse outcome than we believe is likely. In particular, the lower end of our NAV corresponds with $2,000 PSF, a draconian outcome barely above construction costs, while the high end our NAV is $2,500 PSF, which we believe is inline with recent sales of similar real estate.

We believe the best comparable for 77 Greenwich is 50 West, the luxury tower right down the street in the Financial Distract featured in the photo at the beginning of this report. 50 West closed with an average selling price of roughly $2,250 PSF. However, there are a handful of critical difference between the two buildings. First, 50 West sold the first dozen or so floors of their development as condos, while 77 Greenwich sold them to the New York City school district. As the lower floors have worse views – think looking across the street into someone’s apartment versus looking across the skyline at the river – they sold for much lower prices PSF than comparable higher floors. Further, 50 West has larger floors and not all apartments have views facing the water, whereas all apartments at 77 Greenwich have at least a partial river/harbor view. In addition, we believe 77 Greenwich has a product better suited to the market. 77 Greenwich’s condos are on the smaller side but well optimized, at roughly 900 SF for a one bedroom and 1300 SF for a two bedroom. This helps to lessen the “sticker shock” when comparing to non-luxury, yet high square footage Manhattan real estate.

Putting it together, we believe our $2,000-$2,500 PSF range for 77 Greenwich is adequately conservative. Trinity began selling apartments in Spring 2019 and expects to complete construction in late 2020 with closings occurring in a similar time frame.