Tax revenue is becoming a major driving force as more US states contemplate legalizing gambling. Whether you’ve played poker or bet on sports, your winnings could be taxable. And with tax season around the corner, knowing how to report them is key.

To help you navigate the requirements, this guide will define gambling winnings tax and help you understand your responsibilities. We’ll walk you through reporting tax returns, federal and state tax rates, tax relief, and more to ensure compliance with the law.

Definition of gambling winnings

Before we discuss tax on gambling winnings in the US, we must be all on the same page regarding what gambling winnings are.

According to the Internal Revenue Service (IRS), the term gambling winnings refers to the money casual gamblers have won from games of chance or wagers placed on events with uncertain outcomes.

This category includes lotteries, raffles, casino games, horse races, and sports betting, as long as they involve real monetary value. It covers earnings from both local and international gambling activities and events. The term also encompasses cash winnings and non-cash rewards, such as vehicles, vacations, and similar.

The IRS explicitly defines gambling winnings since they fall under taxable income in the United States.

Do I need to pay tax on online gambling winnings?

You need to pay taxes on online gambling winnings because US law doesn’t differentiate them from traditional gambling winnings.

The IRS sees winnings from all real-money gambling activities as a form of revenue, which is taxable by law. Therefore, rewards from online gambling aren’t exempt, whether they’re from US or offshore gaming sites. To stay compliant, you must report them on your federal tax return as gambling income.

If not, the IRS may suspect you’ve underreported your earnings, which could result in penalties and interest. Depending on whether the service interprets the underpayment as negligence or fraud, you may be subject to fines of 20%–75% of the unpaid amount, plus the interest on unpaid taxes and penalties of 7%.

How much of my gambling winnings is taxable?

The total amount of gambling income is taxable. However, you cannot deduct the cost of your initial wagers directly from your winnings when reporting them.

For example, if you’ve won $530 from a slot game with a $30 bet, your taxable income won’t be $500 — it will remain $530. Namely, the IRS does not allow you to “tally” winnings and losses in your tax form.

You must report the full amount you’ve won or the reward’s fair market value (FMV) at the time of winning (if you’ve acquired a non-cash item).

Note: The FMV reflects the price the item would command in an open market transaction.

Gambling winnings tax rates

The default tax rate on gambling winnings is 24% for lottery, sweepstakes, and wagering pool prizes of $5,000 or more, as well as other gambling winnings at least 300 times the original bet amount. The only exceptions are winnings of non-resident aliens, which are taxed at 30%.

Remember, this is only the federal tax rate. You might also face state taxes on gambling winnings, depending on your place of residence. For example, Texas and Florida don’t tax gambling winnings, while Pennsylvania and North Carolina impose a gambling winnings tax rate of 3.07% and 4.5%, respectively.

Remember that you can also become liable to a backup withholding tax if you don’t provide a valid Social Security Number (SSN) or Taxpayer Identification Number (TIN) or if the IRS flags you for having a history of underreporting your income. This tax rate is also 24% for cash rewards, but can reach 31.58% for non-cash rewards.

Note: If you’re subject to regular gambling withholding, you won’t be liable for backup withholding.

Can I claim tax relief on gambling losses?

While you can’t deduct the cost of your wager from your gambling winnings tax, you can write off your losses. However, the cost of wagers (i.e., the amount you gamble) can be used as a deduction for tax purposes — but only as part of itemized deductions on your tax return.

That is, however, only if you’re a resident who complies with specific rules regarding the structure and amount of your deductions.

You must itemize your deductions

To claim losses, you should itemize your deductions on Schedule A of your federal tax return. You must keep detailed records of your gambling winnings and losses throughout the year. Your records should include the following:

- • Type of gambling activities you engaged in (specific games)

- • Date and place (name and address) where you played

- • People you played with

- • Amounts won and lost

You should also save the wagering tickets, receipts from the gambling facility (including travel and accommodation expenses), and canceled checks and credit card statements.

Note: If you choose to itemize your deductions, you won’t be able to claim the Standard Deduction for your filing status, even if it comes up to more than the total of your itemized deductions. You must also itemize deductions for other expenses, or you will lose your right to claim tax relief on gambling losses.

You must mind the amount of your deductions

You can’t deduct more than the gambling winnings you report as taxable income. The IRS allows you to offset your winnings only up to the amount you’ve won.

For instance, if you’ve gambled $6,000 to win $4,000, your deduction is limited to $4,000 at most. You cannot add the remaining $2,000 to reduce other taxable income or carry it over to future years.

Note: Some states, like Connecticut, Illinois, Indiana, New York, and Minnesota, limit or even prohibit gambling loss deductions on state tax returns. But don’t worry; it only applies at the state level. You can still deduct losses on your federal return even if you live in one of these states.

How to disclose gambling tax returns

You should disclose your cash and non-cash value gambling rewards as “other income” on Schedule 1 on Form 1040, Form 1040-SR if you’re 65 or older, or Form 1040-NR if you’re a non-resident alien. All three are standard IRS documents individual taxpayers use to file annual income tax returns.

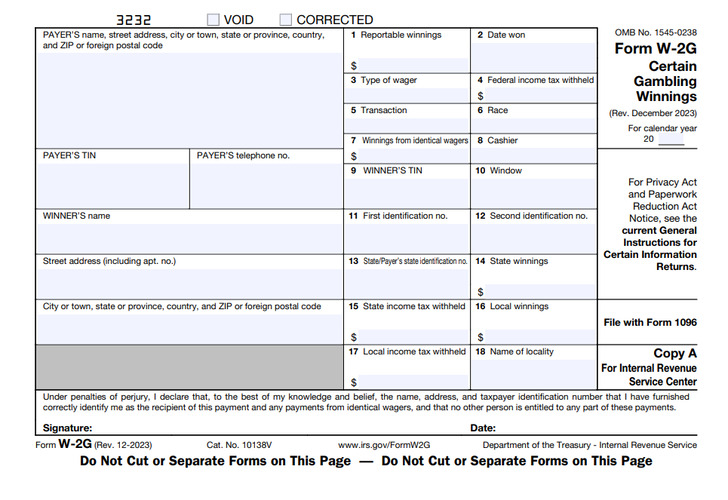

You can work out the payable amounts yourself or use a gambling winnings tax calculator. Form W-2G may assist with the reporting — it’s essentially a confirmation that the gambling establishment has withheld the income tax from the amount you won. It also shows the amount you must report on your tax return, which should be included when filing.

The gambling winnings tax form W2-G is usually issued by the casino or gambling institution at which you’ve won:

- • $5,000 or more in live and online poker tournaments.

- • $1,500 or more at keno.

- • $1,200 or more at bingo or on a slot machine.

- • $600 or more on horse races (if your winnings amount to 300 times your wager or more).

However, even if you don’t receive the document, the IRS still expects you to report all gambling income on Form 1040.

For instance, casinos don’t send W-2Gs for winnings from table games like blackjack, roulette, baccarat, or craps because there’s no way of knowing how much money you initially brought to the table.

Moreover, you won’t receive this form if you’ve won a substantial amount playing the best online casino games on a site that’s not licensed in the US. Still, any money you walk away with is taxable and must be reported to the IRS.

Note: Form W-2G reports your gambling income with a flat 24% federal tax withholding rate. It might also include an extra backup withholding tax, as discussed above.

Tax on gambling winnings — key considerations

To file your gambling winnings tax return correctly, keep these details in mind.

Gambling income is taxed at a flat rate, for the most part

Unlike regular income, which faces progressively higher tax rates the more you earn, gambling winnings are taxed at a flat 24% on the federal level.However, some states apply a progressive tax rate to gambling winnings. For example, New York levies rates range from 4% to 10.9%, while New Jersey rates vary from 1.4% to 10.75%. Stay informed about local regulations to manage your finances more effectively.

Professional gamblers are not taxed in the same way as casual players

Those who play regularly and rely on gambling winnings as their primary income are considered professional gamblers. The IRS treats their winnings as regular income and requires them to report it on Schedule C (Form 1040), like self-employed individuals.Their gambling winnings are subject to federal, state, and self-employment income taxes. It also implies that they can’t deduct gambling losses like casual players but may be able to write them off as business expenses, for example, travel for tournaments or internet costs for online competitions.

Gambling income doesn’t need to be taxed at once

Casinos, lotteries, and other gambling providers may pay your winnings as a lump sum or in installments. Some will let you pick between the two, while others will make that choice for you. Either way, how you’re taxed will depend on how the payment is issued.A lump sum payment will be taxed immediately at federal and state levels. An annuity payment spreads the tax liability across multiple years, which aligns with how you receive the installments. Make sure you factor these findings into your budgeting to avoid falling behind on your payments.

Online gambling winnings in cryptocurrencies are taxable

All online gambling winnings are taxable, whether in fiat money or cryptocurrency. Crypto winnings, similar to non-cash rewards, are taxed based on their USD value at the time you’ve received them. If you exchange them for USD down the line, they also incur capital gains taxes. This is a levy on your profit, reported on Form 8949, that the IRS imposes on all investors.The capital gains tax amount will depend on the change in value of your crypto coins since you received them. Keep records of their fair market value at the time of receipt and any fees paid to acquire it. Try to time your exchange to minimize your tax liability.

Gambling income could affect your Social Security benefits

Like investment profits, interest, and dividends, gambling winnings fall under unearned income. They don’t affect Social Security retirement benefits because they only consider earned income. However, the Supplemental Security Income (SSI) is an entirely different story.SSI is a needs-based program, which means any additional earnings, including gambling winnings, count. Depending on the total amount you’ve received, it could reduce your payments or even lead to disqualification.

How much does the US government make from online gambling taxes?

According to the American Gaming Association’s research, US online gambling revenue in 2023 reached $6.2 billion across the six states where it was legal at the time. That same market generated $1.61 billion in tax revenue.

There’s no denying that these numbers are fantastic, but what’s even more striking is how close they are to sports betting tax revenue, which brought in only half a billion more despite being legal in 23 additional states.

Based on the data, researchers estimate that local governments could collect up to $15 billion in combined tax revenue annually if all 44 jurisdictions legalized some form of iGaming. It’s just a shame that the real-world outlook isn’t as promising as the statistics.

Besides Rhode Island, which became the seventh state to legalize online casinos, few others have made successful moves in this direction. States like Maryland, New York, and Illinois all recently saw online casino-friendly bills fail.

This stance isn’t surprising, as online gambling has always been a tough sell in the US due to cultural and political resistance. However, the fact that lawmakers keep trying shows there is at least some interest.

Conclusion

The US imposes federal and state taxes on gambling rewards, but that shouldn’t make winning at a casino any less exciting. You can make the process much easier with our tips and a good gambling winnings tax calculator.

Make sure you report all gambling income, whether you’ve won it online or in person, in fiat or cryptocurrency. Try to keep thorough records of your bets, wins, and losses, and ensure your deductions are itemized and within the allowed limits. And don’t be afraid to seek professional legal advice if you’re unsure or lost.

A little organization is all you need to stay compliant and avoid legal issues and penalties.

FAQ

What does the IRS consider gambling winnings?

How much tax do you pay on gambling winnings?

Will I get audited if I don’t report gambling winnings?

Is claiming gambling losses on taxes worth it?

References

– About Schedule A (Form 1040) (Internal Revenue Service)

– About Form 1040-SR, US Tax Return for Seniors (Internal Revenue Service)

– About Schedule C (Form 1040) (Internal Revenue Service)

– About Form 8949, Sales and Other Dispositions of Capital Assets (Internal Revenue Service)

– Instructions for Forms W-2G and 5754 (Internal Revenue Service)

– Supplemental Security Income (SSI) (Congressional Research Service)

– 2023 Commercial Gaming Revenue Reaches $66.5B (American Gaming Association)

– US iGaming State Tax Revenue Potential (Light & Wonder)