Eschler Recovery Fund commentary for the first quarter ended March 31, 2020.

Q1 2020 hedge fund letters, conferences and more

Dear Partners,

Eschler Recovery Fund fell 24.7% in Q1 2020, net of fees and expenses, as global equity markets abruptly priced in a sharp recession catalysed by measures to contain a metastasizing health crisis. At quarter-end, the S&P 500 had fallen by 20% (recovering somewhat from -33.9% peak-to-trough) and the Russell 2000 by 30.6%. Small-cap value indices more representative of the Fund’s universe, such as the Russell 2000 Value Index, fell by over 35%. The median US stock (Value Line Geometric Index) fell 35.8%.

To be sure, we are in unchartered territory. Billions of people are currently quarantined at home. Tens of trillions of dollars of wealth has evaporated in the space of two months. As a result, economies are now collapsing. Not least, the constant barrage of depressing media reports has market participants scared of much worse to come. If economic activity remains on hold for another 6-12 months, they will probably be right. In which case, the “cure” will have been far worse than the disease ever could have been. But based on the historical data I am evaluating (see outlook section), if things start to normalise within several months, abetted by unprecedented stimulus, this bear market could be over relatively soon. I have capitalized on the recent rampant uncertainty – and the discounted pricing it has spawned – by investing a cash position worth 30% of net assets. While in no way wishing to downplay the health tragedy unfolding around the world, based on the bottom up valuations in the portfolio I feel upbeat about the Fund’s long-term prospects.

At the time of writing this letter (7 April) the Q2 return is +6%.

Irrespective of the disappointing Q1 result, a key question I would ask if our roles were reversed is: How did you build defences into your portfolio to protect against a change in market regime? After all, signs of excess were evident for some time. The answer is that structuring the Fund for a change in market regime was, and continues to be, a core element of the strategy. My objective has been to construct a portfolio with low gross exposure comprised of primarily cyclical deep value stocks, with a recent emphasis on precious metals, and cash in the absence of high conviction ideas. The strategy goal remains to capture long-term mispricing in individual securities by harnessing volatility spawned by market and industry cycles. Seen in that light, it is periods like the one we have just experienced that provide fuel for future returns.

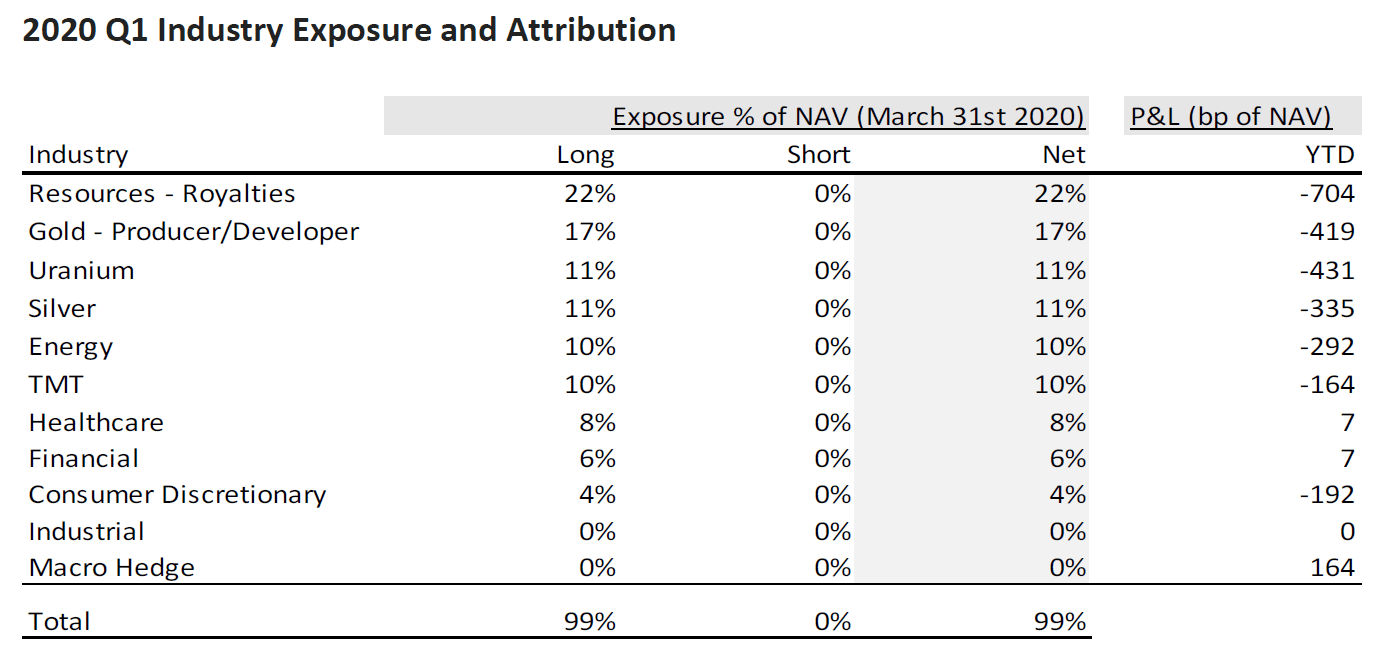

Eschler Recovery Fund Q1 2020: The Good, the Bad and the Ugly

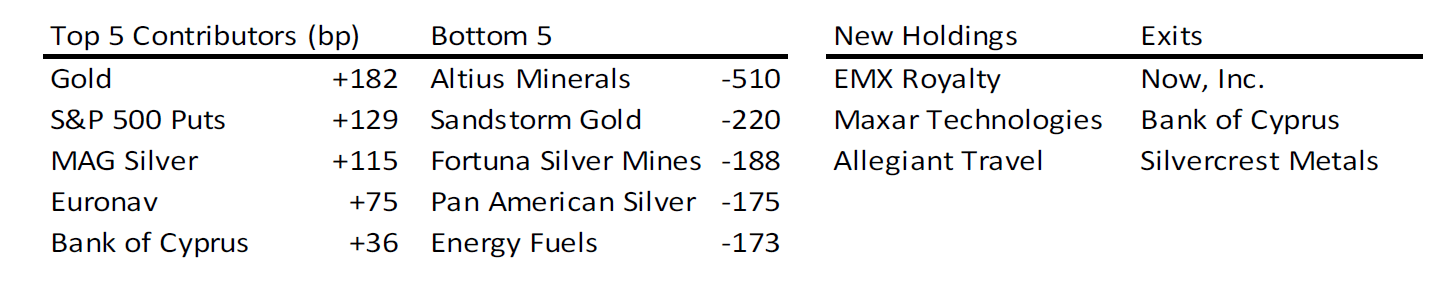

During January I reduced exposure, exiting Now, Inc, the Australian bank shorts, Silvercrest Metals and Bank of Cyprus. By the beginning of February cash balances had reached 30% and I was long gold and S&P 500 puts. Fortunately, the Fund had no exposure to banks and little exposure to oil & gas or consumer-facing businesses. Near the lows I was able to buy back some deeply discounted precious metals positions and establish several new holdings. This is the good news.

The bad news is that the Fund’s uranium and base metal holdings were hit hard. The uranium book fell 30% and the Fund’s largest holding, base metals royalty company Altius Minerals, fell 40%. In addition, new holdings purchased in early March detracted 3%. I also covered hedges way too early.

Worse, precious metals shares suffered an ugly 50% peak-to-trough fall driven by margin calls from mid-February to mid-March, ending the quarter down about 33% (but up 27% off the lows). With gold now above $1700/oz and diesel prices cut in half, the fundamentals of these businesses are favourable and the shares are due a major catch up—more below.

Current Positioning

I believe the greatest opportunities to generate strong returns are in smaller businesses run by entrepreneurial managements. The Fund’s core exposure is to small- and mid cap cyclical growth businesses in industries recovering from deep bear markets, including precious metals, uranium and energy, as well as several deep value special situations. The median market capitalization of the Fund’s top 20 holdings is $890 million.

Precious metals equities represent by far the largest exposure at 45% of net assets targeted at royalty companies, small-cap producers and developers. Gold and gold stocks remain firmly in a bull market. Drivers of gold include negative real interest rates, a rising US budget deficit, equity market turmoil and a falling US Dollar. All but the latter are a feature of today’s market and a falling US Dollar cannot be ruled out as record fiscal stimulus comes on-stream in America. Precious metals equities have greatly lagged gold recently, having been caught up in technical liquidation during March. Silver equities, in particular, were a victim of intense silver futures liquidation—despite physical silver in the form of coins and bars selling out around the world.

In the first days of April gold and silver have taken off. The whole complex presents a tremendous opportunity in my view. It is important to note that gold can also do well during deflation. One reason is that commodity input costs fall, amplifying margins. From October 1929 through July 1932, while commodity prices fell 30% and the Dow Jones fell 89%, gold rose and Homestake Mining, the largest gold stock of the era, doubled.

One short-term issue holding back the Fund’s precious metals holdings is the temporary closure of mines in many producing countries due to Covid-19. As a result, despite the benefit of lower energy prices, Q2 costs on a per ounce basis could be disappointing as production volumes will be depressed. Royalties and streams will also be impacted. I believe the market will mostly look through this and I have thus made no changes as a result.

During the quarter I established a new holding in EMX Royalty, a cash-rich, shareholderoriented small-cap royalty business. Led by geologist David Cole, EMX has assembled a remarkable portfolio of mineral rights around the world, buttressed by producing gold royalties in Nevada. This year and next, EMX will begin to monetize key royalties in Serbia and Turkey. The team has a strong track record and I am thrilled to partner with them.

Uranium equities remain a core holding at 11% of net assets. Temporary mine closures in Kazakhstan, Namibia and Saskatchewan could shave another 5-10% off uranium mined supply this year, further stretching what has become a gigantic supply deficit. It has been a long road but, as stated in previous letters, I believe higher uranium pricing is inevitable and having a position in the industry ahead of its recovery crucial.

The market crash provided an opportunity to deploy Fund capital into several non-resource ideas as well, two of which I would like to highlight.

I invested a half-position (3%) in Allegiant Travel, an ultra-low-cost US domestic airline focused on monopoly leisure routes with the best margins in the business and an upgraded fleet of Airbus aircraft. The company has no corporate or long-haul international exposure, does not hedge fuel, has low fixed costs and can rapidly adjust capacity to demand. Senior management has implemented 50% salary reductions, company-wide cost initiatives and a freeze in investments to free up cash to weather the lockdown. The CEO draws no salary and owns 17% of the business. As the US economy recovers, Allegiant’s earnings power and historical multiples should combine to produce a much higher share price.

Maxar Technologies is a Leader in geospatial imagery and analytics and satellite manufacturing. The core imagery business enjoys recurring, recession-proof cash flow derived from contracts with governments around the world. The company is in the process of deploying a new constellation of high-resolution satellites with the potential to lower risk and improve economics. New management has de-risked the balance sheet and will use growing free cash flow from 2021 to further pay down debt. At 5x EV/EBITDA the shares offer excellent risk-reward.

Outlook

In recent years quantitative easing (QE) and stock-based compensation encouraged excess borrowing in the pursuit of share buybacks. This came at the expense of growth capex. Monetary and fiscal policy alternated as sources of stimulus and money velocity slowed. The stock market boomed but productivity and GDP growth lagged. As a result stocks with rapid, consistent growth became very valuable. The most successful drifted toward the top of the S&P 500, where they remain.

Unlike during the past decade, today’s policy response is coordinated, and that means everything. Not only is the Fed, the lender of last resort, backstopping market liquidity but money is being put directly into citizens hands. Initially this direct fiscal infusion will merely offset lost income and a higher savings rate. Over time, though, this massive, doublebarrelled stimulus has the potential to usher in a cycle of faster nominal economic growth.

Faster growth, combined with more constrained access to credit in the short-term, might make corporate capex spending look more attractive. If growth becomes less scarce, why pay up for it? Low-valuation stocks would boom.

This hypothesis above, if directionally correct, would take time to play out. Where to in the shorter term? Consider that the median US stock as represented by the equally-weighted Value Line Composite, has now been cut in half in the 2+ years since January 2018. The stock market had been discounting a slowdown in growth for some time. After the recent collapse, recession is now the consensus base case. Is this when the bear market ends?

The prevailing level of interest rates remains a critical variable in valuing stocks. One useful recent study¹ of the 1968-2020 period looks at the influence of valuation on forward market returns as represented by the Value Line Composite index, when the BAA corporate bond yield was 5% or less. This Value Line index captures the market level as defined by the median stock; comprises 1700 stocks; and uses a stable blend of trailing and forward sixmonth EPS to calculate its price/earnings (P/E) ratio. Whenever the P/E ratio fell below 13.5x (it fell below 13x in late March 2020), the market bottomed 100% of the time since 1968.

Which group of stocks tends to perform best in a market recovery? Unsurprisingly, it is the smallest, cheapest stocks, ideally with high asset turnover and low risk of bankruptcy, that post the strongest returns. The best empirical evidence for this was laid out in a recent study by Verdad². Verdad looked at asset class returns following eight economic crises since 1974 starting three months after high yield spreads rose above 6.5% (the BofA US High Yield Index OAS Spread is currently 9.4%). Small value stocks, as defined by a value composite of the cheapest decile using an average of EV/EBITDA, P/B, P/E and FCF Yield, returned on average ~40% over 12 months and ~70% over 24 months.

So empirical evidence derived from large historical datasets implies opportunity amidst crisis. Is this time different? If not, Fund returns will improve, perhaps dramatically. If, on other hand, the above hypothesis is wrong and the global economy continues to deflate, I would expect the large holding in precious metals to provide ballast to the portfolio.

Theron de Ris

Portfolio Manager

7 April 2020