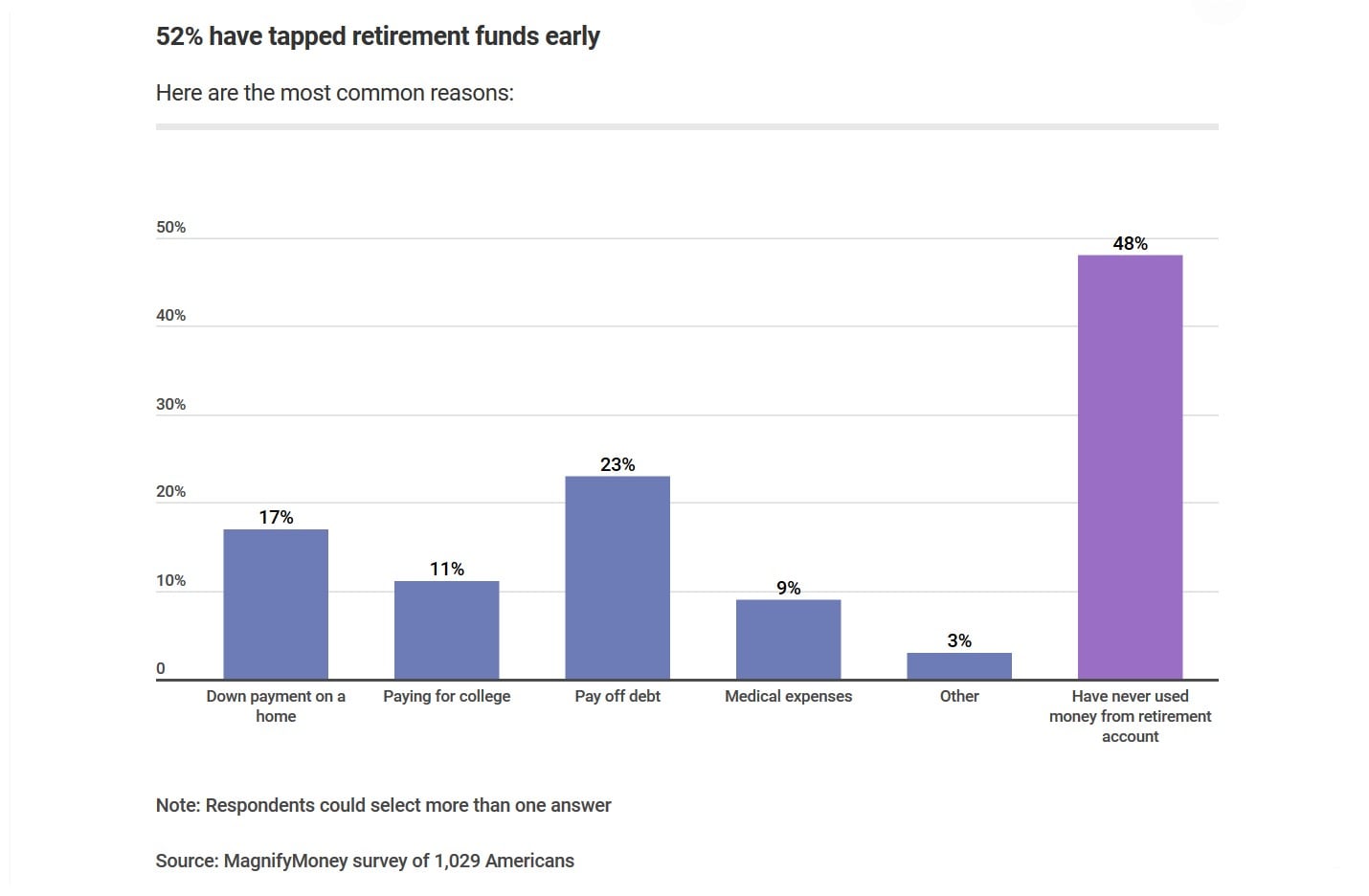

The two main reasons respondents cited for withdrawing money from their retirement savings are as American as apple pie: home ownership and personal debt. According to the survey, 23% of those making an early withdrawal did so to help pay down non-medical debt, while 17% needed the money for a down payment on a home.

Although the housing market appears to be cooling off compared to just a few years ago, a down payment on a home still requires a significant chunk of change — experts recommend a down payment equaling 20% of the total mortgage to optimize your mortgage payments.

Q2 hedge fund letters, conference, scoops etc

Personal debt, from credit cards to student loans, remains a fixture of everyday economic reality for millions of Americans. In other words, the stressors that cause workers to raid their retirement funds don’t look like they will decrease appreciably in the foreseeable future.

Which Americans are withdrawing money the most?

Breaking down the demographics, older savers are less likely to withdraw money from their retirement fund than younger savers. 54% of millennial savers say they’ve taken an early withdrawal from a retirement savings account, compared with 50% of Gen Xers and 43% of baby boomers. This stands to reason considering that many millennials have now entered the stage of life where they are getting mortgages, starting families and taking on bigger financial obligations while also being decades away from the traditional retirement age. Millennials are also more likely to say that raiding your retirement fund is justified under certain circumstances, as seen in the chart below:

Just one of many bad retirement savings habits

Tapping into retirement funds — whether an employer-sponsored 401(k) or a traditional IRA — before the appropriate age almost always comes with a financial penalty in the form of additional taxes and fees. What is more, you’re diminishing the principle that fuels the compound interest you need to meet your retirement savings goals.

Unfortunately, the survey reveals early withdrawals are just one of the many bad habits Americans engage in when it comes to retirement savings. This list of less-than-ideal practices includes:

- 35% of Americans are not currently saving for retirement. Of those who are, 37% started saving at age 30 or above, and 12% started saving when they were older than 40.

- 60% of Americans do not know exactly how much they have saved for retirement. Just 40% know the exact amount, while 45% have a rough idea and 15% have no clue.

- Nearly 1 in 5 Americans don’t contribute enough to their employer-sponsored retirement account to get the maximum company match. Maximizing a company match is one of your best ways to maximize your retirement savings. Among those with an employer-sponsored retirement savings plan, just 17% of respondents contribute 10% or more of their take-home pay. Almost 5% contribute nothing at all, and nearly 6% are unclear about how much they contribute.

Approximately 42% of respondents have made the mistake of withdrawing their entire balance from an employer-sponsored retirement plan when changing jobs without rolling it over – and nearly 15% have done so more than once. A little more than 47% of millennials admit to this faux pas.

The most damning finding of all is that 27% of those surveyed have never thought about how much they’ll need in retirement. And while “ignorance is bliss” may hold true when it comes to some things in life, this expression should not apply to your retirement plans.

Methodology

MagnifyMoney by LendingTree commissioned Qualtrics to conduct an online survey of 1,029 Americans, with the sample base proportioned to represent the general population. The survey was fielded June 24-27, 2019.

Generations are defined as:

- Millennials are ages 22-37

- Generation Xers are ages 38-53

- Baby boomers are ages 54-72