In this class, we completed our discussion of real options, starting with an analysis of why financial flexibility can be viewed as an option, and how to value it. We then turned our attention to distressed equity, and why stock in a highly levered, money losing firm can become an option, and why it matters for investors. We ended the class by looking at the sad history of value destruction in acquisitions, and set up the discussion for why.

Slides: http://www.stern.nyu.edu/

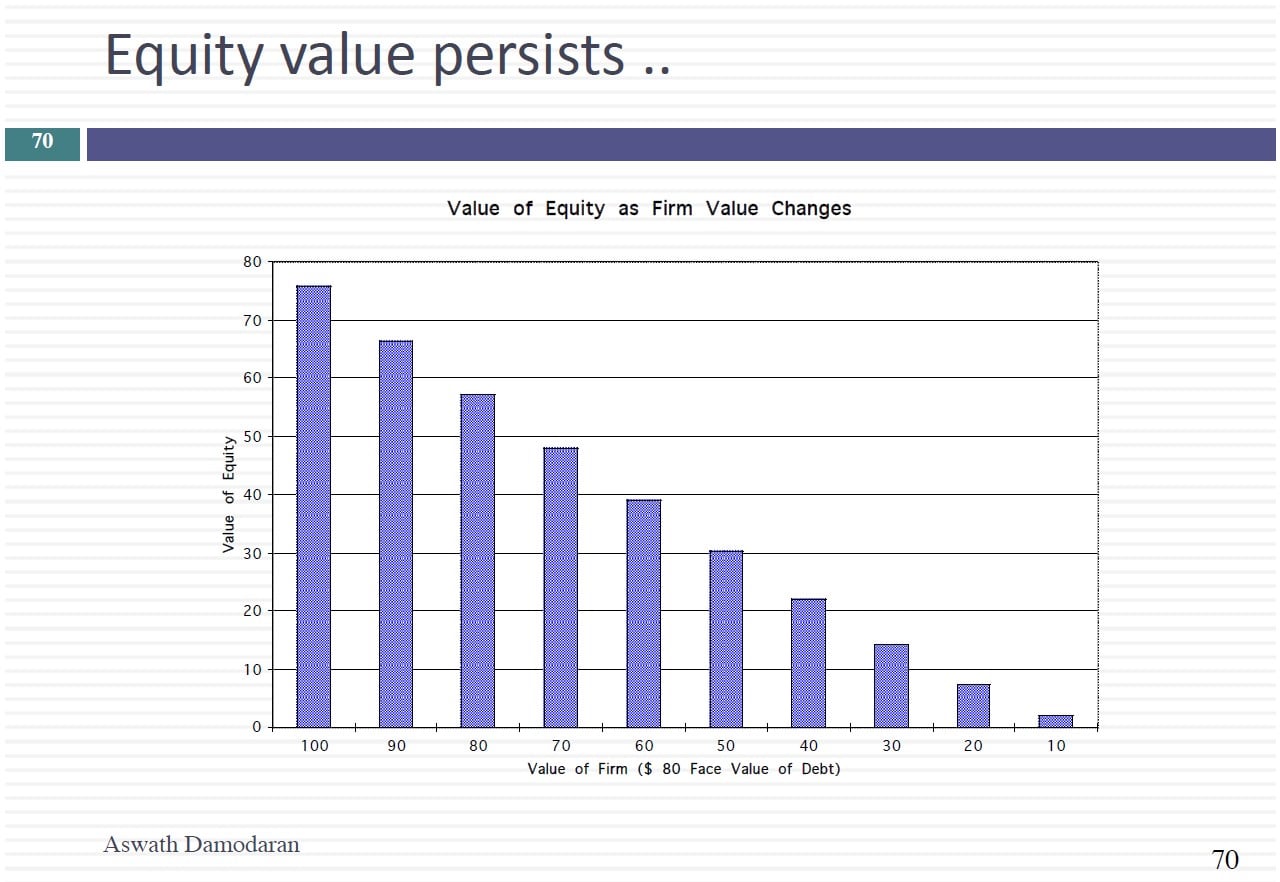

Session 23: Financial Flexibility & Distressed Equity

Q1 hedge fund letters, conference, scoops etc

Transcript

So I'm going to show you two companies and let her out for the case of argument assume that the numbers are OK.

I value two companies one is Royal Dutch and the other's Petrobras. Let's assume they have the same value. But here's where they're different let's assume Royal Dutch gets a bulk of its value from developed reserves and Petrobras gets a bulk of its value from undeveloped reserves. The value today is the same. And let's say today's oil price is sixty dollars about and today you valued both companies correctly. The price per barrel of oil is sixty dollars. Tomorrow. Let's say you wake up to a Middle East crisis which is almost always around the corner. So let's say you wake up to a crisis and oil prices jump from 60 to 100 dollars a barrel. So let me ask the a question what would happen to these two companies. First this is good news or bad news if you're an investor in these companies it's good news the price will go up. Will it go up about the same for both. The value is the same for both companies before. Will it go up roughly the same.

Which company do you think is going to go up more and why this one is that increased price will make all oil more valuable because you have an option you get a time premium and now that you've had a jump in the price that time premium might be greater. But they both go on. But let's make this more interesting. Let's say the day after the Middle East crisis goes away. Don't ask me how that happens and the price goes back down to sixty dollars about we're back to a status quo right. Two days ago the price was 60. Now we're back to 60. Will the two companies revert back to the values they had before the crisis or has anything changed. Lou you say you want to try. Which will be about more Royal Dutch you think would be what more. You think Petrobras will be what more. We wanted to do a show of hands I in a 50 50 shot right. Or will they both. How many things will be what the same IV drug prices back to 60s was what it was two days ago.

How many think nothing has changed and you should be at the same value nobody. OK. How many think Roy that should be worth more OK.

The rest I will you. I won't even ask you to embarrass us. Pretty sure it's a tie. No idea. It's true the price of oil hasn't changed right. But what did the two days do. Remember that when we talk about the volatility in oil prices it's always forward looking. It's not a historical volatility that you price things aren't. What did the two days teach you that oil prices can be very volatile. You wake up two days later you're now going to say you know what those Petrobras reserves are out of the money but in the day they can go to being in the money because that's what we saw yesterday. What I'm trying to say is when you value oil companies. It's not just the level of the oil price that drives the value to volatility what can kill an oil companies what happened in the 1980s. You know what happened in the 1980s oil prices went low and they stayed low. They were boring boring low is the worst possible scenario for an oil company exciting law you can live with exciting highs dream time but boring low kills both the undeveloped and the develop reserves because the value of the optionality goes away. I'm going to do one final piece to this and this has very little to do with these reserves but I want to talk a little bit about how you can use option pricing to deal with some interesting twist that can be thrown at you.

Let's assume that Petrobras auctions off these undeveloped reserves. Right. So you're the potential buyer. Let's say you are Exxon Mobil. But they had a condition. They had a condition that you can get the value of all the oil under the ground up to one hundred and fifty dollar oil price and above the 150 100 percent of whatever you make goes back to the government because the Brazilian government says this is our oil. We don't want to just give it away. So what have I introduced. I've introduced the optionality but I put a cap on how much money you can make because the oil price goes above one hundred and fifty yolk your profits are capped. Is there a way I can use option pricing to bring in the effect. Of this cap. See what I have. I have an option but now I put a cap on how much money can make. So if I draw the payoff diagram and look a little bit like this right. Basically to look like a court and for for a while it looks this like any other. But then you and you get to 150 it flattens out again. So what would I need to do. I'd first value a call with a strike price of 60. That would my traditional option. Then I'd value a call with a strike price of 150 y 150 that's where the cap is. My option value would then be the difference between those two. This is actually a general technique that's useful whenever you have caps and floor so let's you have a management compensation contract where you're entitled to 10 percent of the profits on this.