Where will the world’s most sophisticated investors make their bets in 2019? Natixis Investment Managers, a leading global asset manager, today released its annual institutional investor outlook, which tracks the planned actions of 500 institutional investors who collectively manage more than $16 trillion in assets for retirees, insurance companies, governments, nonprofits, pension systems and other institutions around the globe.

This annual outlook of institutional investors provides a good roadmap for investors of all sizes, and answers questions such as:

Q3 hedge fund letters, conference, scoops etc

- Will the US bull market come to an end in 2019?

- What are the biggest threats to the market in 2019?

- What are the biggest obstacles to performance? Trade, Brexit, interest rate increases?

- Which sectors provide the most opportunity?

- Where are the biggest bubbles?

- Will there be more volatility in 2019?

- To reduce the risks of a bumpy ride, are institutional investors planning to flock to the private markets more than ever before?

The report, titled “Keep Calm and Invest On,” includes institutional investors’ 2019 market outlook as well as several trends guiding their long-term investment strategy. You can download the full report at: im.natixis.com

2019 Outlook: Institutional Investors See an End to the Bull Market but Are Ready to Handle Increased Risks, Natixis Survey Finds

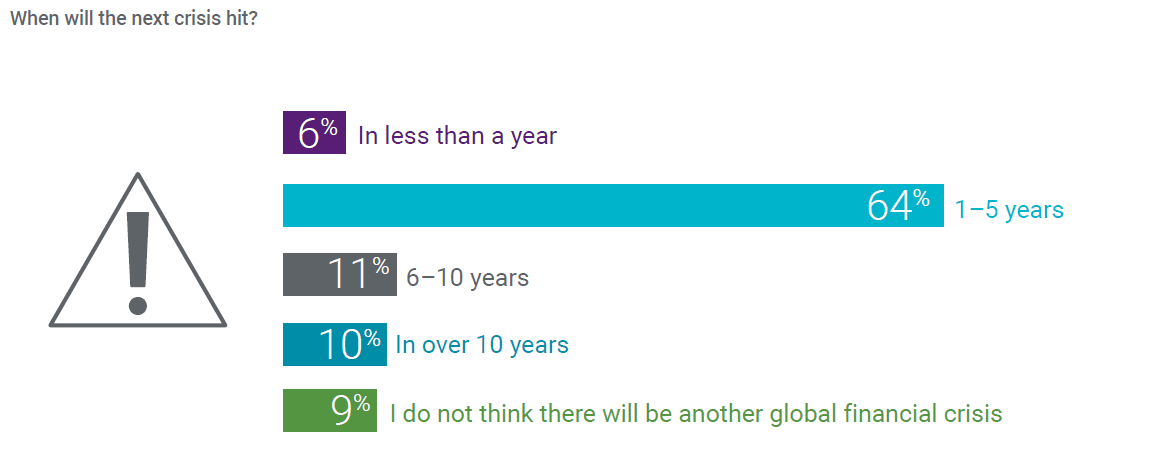

- Two-thirds of institutional investors say the US bull market will end in 2019; 70% expect another financial crisis within five years.

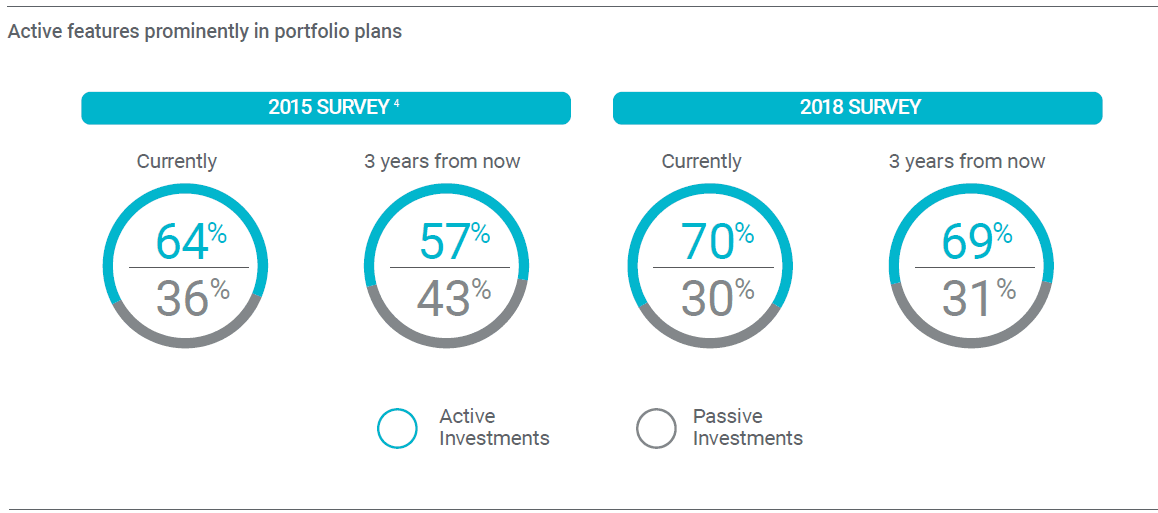

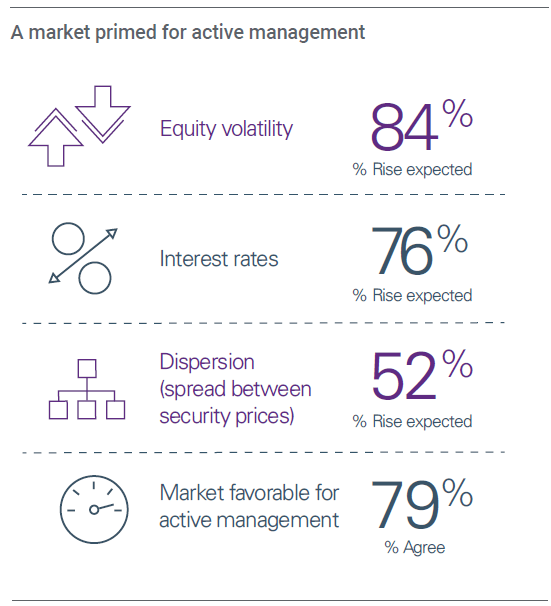

- 79% believe the current market environment favors active management, and average allocations to active strategies grew to 70%, up from 64% in 2015.

- 84% of institutions expect more volatility in the stock market and two-thirds say the bond market will be more volatile as well.

- Investors see geopolitical disruptions and trade disputes as the biggest potential threats to markets in 2019, with rising interest rates posing the greatest risk to portfolios.

- Survey identifies top trends driving long-term investment strategy for institutional investors.

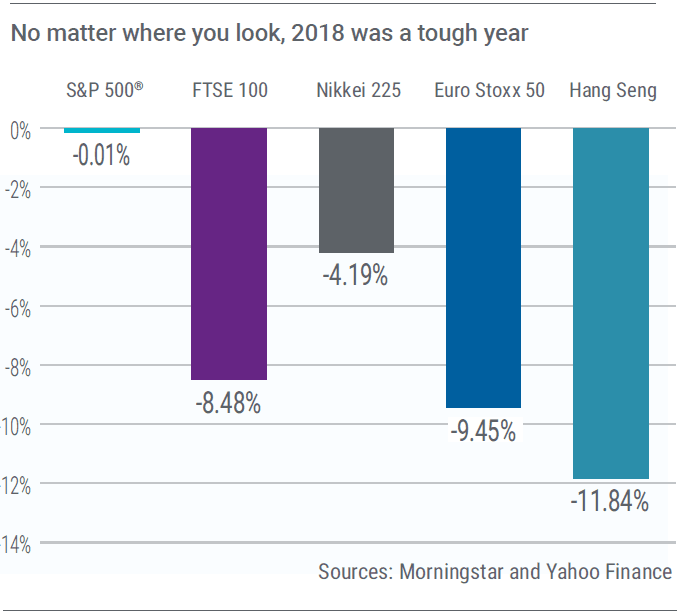

BOSTON, Dec. 5, 2018 – Nearly two-thirds (65%) of institutional investors predict that the decade-long US bull market will end in the next 12 months, bringing to a close the historic bull market that brought record-high stock prices and record-low volatility. But even as they anticipate more turbulent times, six in ten investors say they feel prepared to handle the risks in 2019, according to a new report released today by Natixis Investment Managers.

“Our research shows institutional investors are already positioned for the potential market turbulence on the horizon,” said David Giunta, CEO for the US and Canada at Natixis Investment Managers. “For these sophisticated investors, actively managed strategies and alternative investments are their tools of choice to help optimize their portfolios for the challenges ahead.”

Natixis Investment Managers’ Center for Investor Insight surveyed 500 institutional investors around the world on their market outlook and asset allocation plans for 2019. These investors manage more than $16 trillion of assets for retirees, governments, insurance companies and other institutions.

According to the findings, institutional investors anticipated today’s market challenges given the trends of the past several years. As a result, few of them plan drastic changes to return assumptions or portfolio strategy and will remain focused on active management to guide them through more volatile markets in the year ahead. Eight in ten (79%) institutional investors agree the market environment in 2019 is likely to be favorable for active portfolio management. Accordingly, investors continue to increase their allocations to active strategies while their use of passive strategies continues to decline. Current allocations are split 70% active and 30% passive, up from 64% active with 36% passive in 2015.

The study also found:

- Long-term return goals deemed achievable: Institutional investors say their organization’s current long-term target return is 6.7%, and three-quarters (77%) believe their firm’s return assumption is realistically achievable. More than half (56%) expect to keep their assumed rate of return unchanged in 2019, although 35% plan to lower it and 9% expect to raise it.

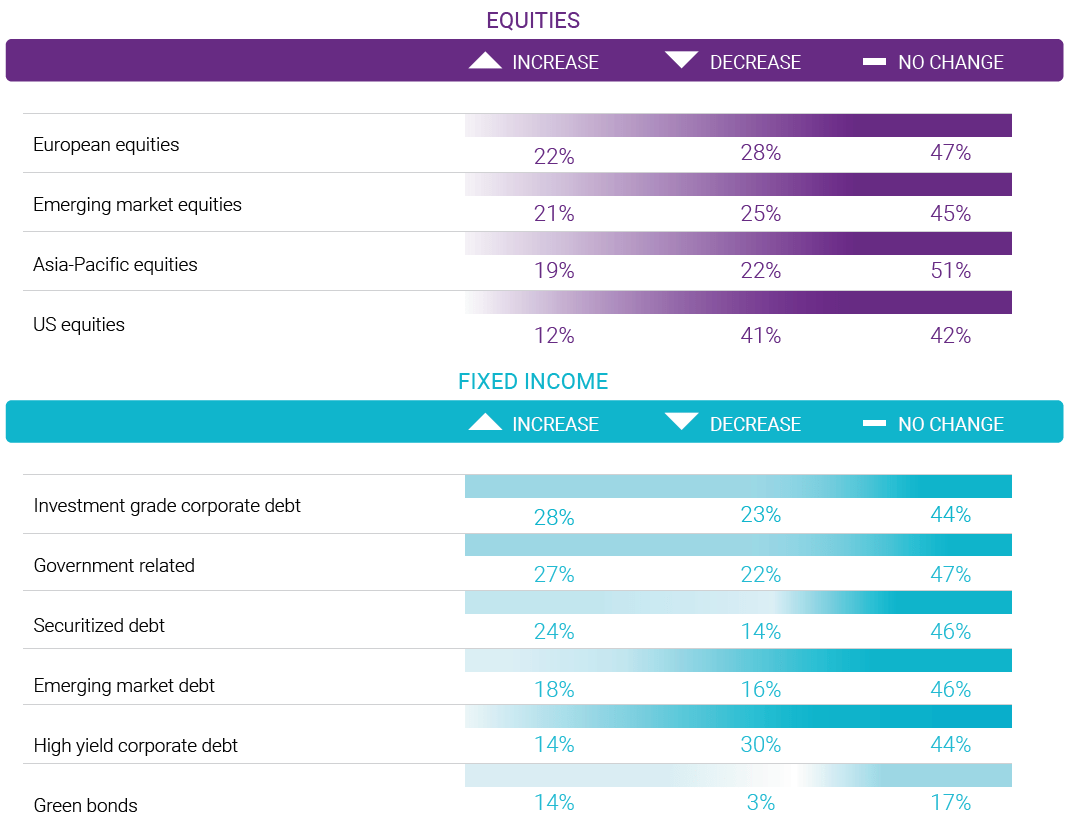

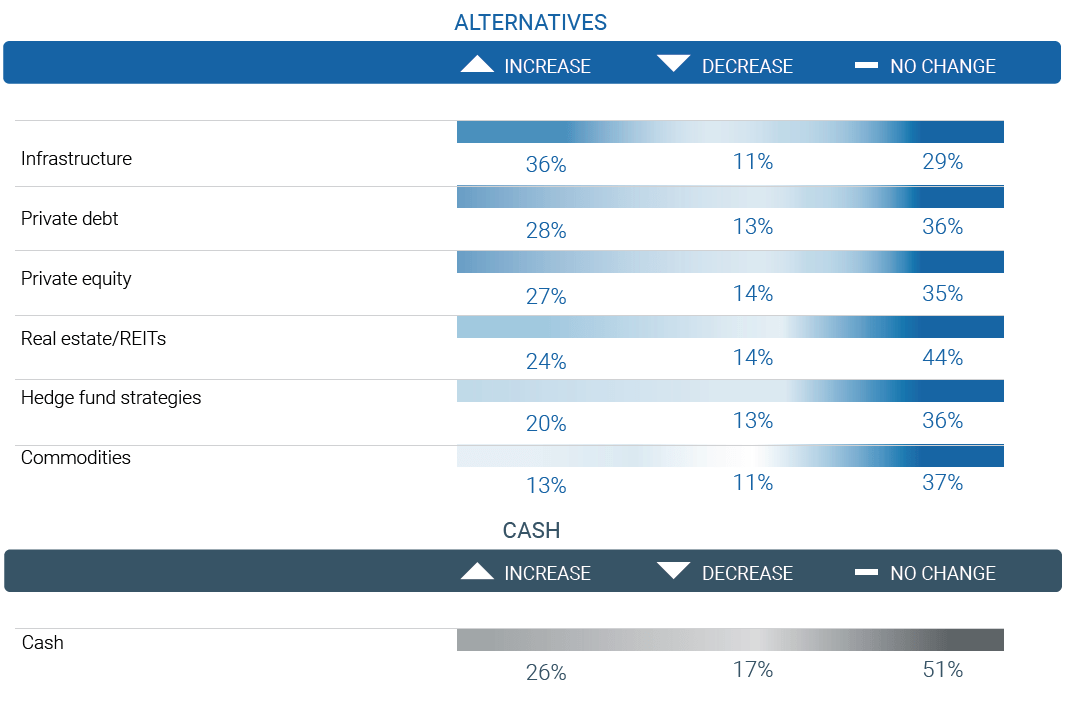

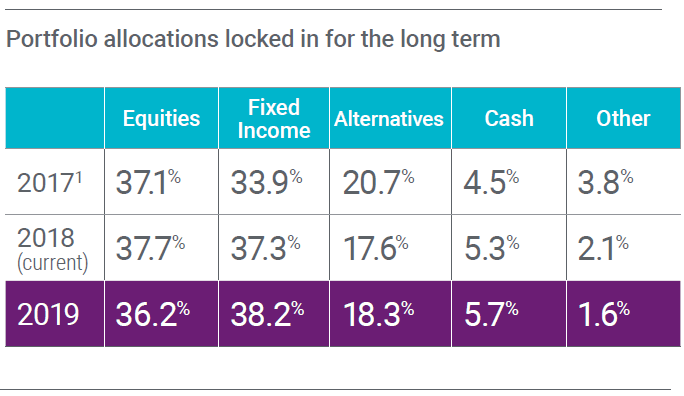

- Little changes in portfolio allocations: Despite expectations for the US bull market’s end, institutional investors foresee minimal changes to their portfolio allocations in 2019. Investors expect to reduce their equity allocations from 38% of their portfolios to 36% while increasing fixed income from 37% to 38% and cash from 5% to 6%. They expect no change in their alternatives allocation (at 18%). Among the biggest moves within classes, 41% of institutional investors expect to decrease exposure to US equities, and 36% expect to increase exposure to infrastructure.

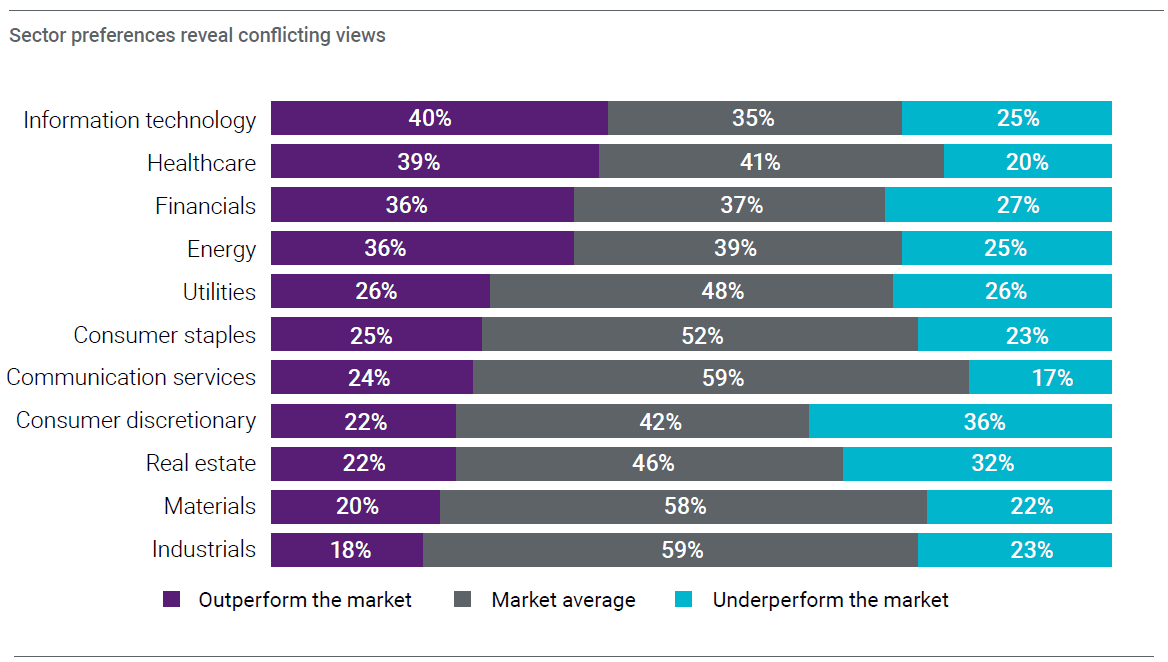

- Tech and healthcare top sector calls for 2019: Institutions have the greatest confidence in the information technology (40%), healthcare (39%), energy (36%) and financial (36%) sectors to produce above-market returns.

- Geopolitics seen as the biggest threat to performance: Three-quarters of investors (77%) see geopolitical disruptions such as North Korea and Brexit as having a negative impact on investment performance in 2019, followed by trade disputes (74%), the unwinding of quantitative easing (65%), interest rate increases (56%) and market volatility (54%).

- Rates and volatility spikes lead portfolio risks: Institutional investors most frequently point to interest rates (56%) as the biggest portfolio risk. Volatility spikes (52%) come in a close second, which is not surprising in light of recent market performance. Regulatory constraints (32%) and liquidity (32%) also are cited as part of the risk discussion.

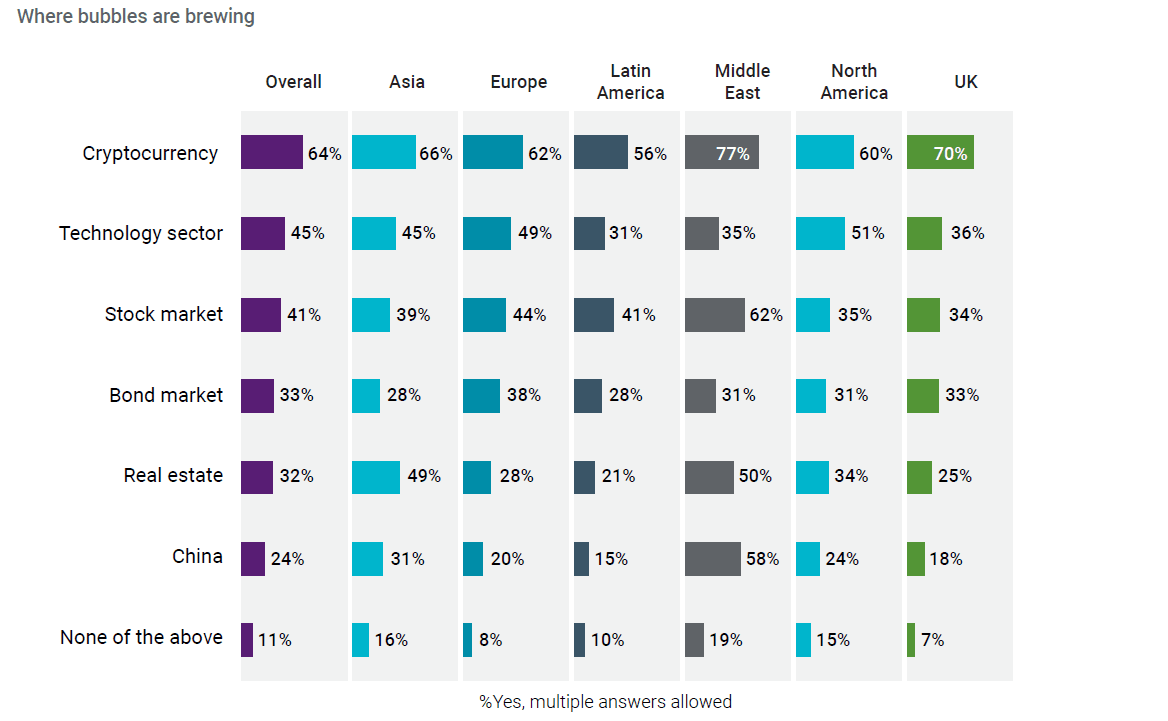

- Potential for bubbles: Seven in ten (71%) institutional investors believe their individual investor counterparts are unaware of asset bubbles, but they see the potential for such bubbles across multiple asset classes: cryptocurrency (64%), technology sector (45%), stock market (41%), bonds (33%), real estate (32%) and China (24%). Six in ten (61%) institutional investors list asset bubbles as being among the biggest threats to investment performance next year.

“Institutional investors have time horizons that average ten years or more, so while it is important for them to look at factors that will affect short-term performance, the survey results also yield critical insight into bigger issues, such as interest rates, political upheaval and the debt crisis that institutions see as driving long-term investment strategy,” said Bob Hussey, Executive Vice President of Sales Management at Natixis Investment Managers.

According to the report, institutional investors also have identified several trends that will drive their long-term investment strategy. Among them are:

- Volatility is the new reality

Institutional investors have warned for the past two years that volatility could return in earnest. Volatility topped their list of concerns for 2017,[1] and 78% predicted the stock market would be more volatile this year.[2] Looking ahead to 2019, a majority once again expects greater volatility in the stock (84%) and bond markets (70%). Institutional investors say that market-neutral liquid alternative strategies are best-suited to reduce risk.

- A transition from low yields to rising rates

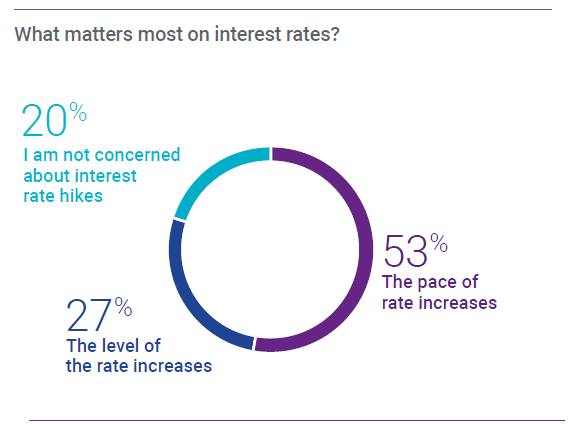

Historically low interest rates have driven post-crisis investment strategy, but the Federal Reserve has been increasing rates, and 76% of institutional investors expect rates to increase further in 2019. Institutions report they are more concerned about the pace of rate hikes (53%) than about the actual level of the increases (27%). If rates rise too fast, for example, it could result in even higher levels of volatility.

- Active management matters more

The active versus passive debate, ongoing among retail investors, is settled among their institutional counterparts. Six in ten institutional investors (61%) say active investments outperform passive investments in the long run, and 78% say they are willing to pay a higher fee for strategies that can deliver outperformance.

- The expanding role of private assets

A combination of uncertain returns and rising rates has institutional investors turning to private markets. Half (51%) say that private equity or private debt are an important part of their organization’s portfolio. Such assets provide higher returns (according to 71% of respondents) and greater diversification (according to 60%). The performance potential of private assets makes them worth the higher fees they often command, say 68% of investors.

- A new crisis is lurking

Investors are less sanguine about the longer term. Although roughly half (52%) of institutional investors believe that regulations put in place after the financial crisis have been effective at mitigating market risk, most (70%) believe that another global financial crisis will occur within the next five years.

The report, titled “Keep Calm and Invest On,” includes additional trends and concrete findings guiding institutional investors’ ongoing investment strategy. To download a copy of the full report, im.natixis.com/us/research/institutional-investor-survey-2019-outlook.

Methodology

Natixis Investment Managers surveyed 500 institutional investors, including managers of corporate and public pension funds, foundations, endowments, insurance funds and sovereign wealth funds in North America, Latin America, the United Kingdom, Continental Europe, Asia and the Middle East. Data were gathered in October and November 2018 by the research firm CoreData.

About the Natixis Center for Investor Insight

As part of the Natixis Investment Institute, the Center for Investor Insight is dedicated to the analysis and reporting of issues and trends important to investors, financial professionals, money managers, employers, governments and policymakers globally. The Center and its team of independent and affiliated researchers track major developments across the markets, economy, and investing spectrum to understand the attitudes and perceptions influencing the decisions of individual investors, financial professionals, and institutional decision makers. The Center’s annual research program began in 2010, and now offers insights into the perceptions and motivations of over 70,000 investors from 31 countries around the globe.

About Natixis Investment Managers

Natixis Investment Managers serves financial professionals with more insightful ways to construct portfolios. Powered by the expertise of 27 specialized investment managers globally, we apply Active ThinkingSM to deliver proactive solutions that help clients pursue better outcomes in all markets. Natixis ranks among the world’s largest asset management firms3 with nearly $1 trillion assets under management4 ($999.5 billion/€860.6 billion AUM).

Headquartered in Paris and Boston, Natixis Investment Managers is a subsidiary of Natixis. Listed on the Paris Stock Exchange, Natixis is a subsidiary of BPCE, the second-largest banking group in France. Natixis Investment Managers’ affiliated investment management firms and distribution and service groups include Active Index Advisors®;5 AEW; AlphaSimplex Group; Axeltis; Darius Capital Partners; DNCA Investments;6 Dorval Asset Management;7 Gateway Investment Advisers; H2O Asset Management;7 Harris Associates; Investors Mutual Limited; Loomis, Sayles & Company; Managed Portfolio Advisors®;5 McDonnell Investment Management; Mirova;8 MV Credit; Ossiam; Ostrum Asset Management; Seeyond;8 Vaughan Nelson Investment Management; Vega Investment Managers; and Natixis Private Equity Division, which includes Seventure Partners, Naxicap Partners, Alliance Entreprendre, Euro Private Equity, Caspian Private Equity;9 and Eagle Asia Partners. Not all offerings available in all jurisdictions. For additional information, please visit the company’s website at im.natixis.com | LinkedIn: linkedin.com/company/natixis-investment-managers.

Natixis Investment Managers includes all of the investment management and distribution entities affiliated with Natixis Distribution, L.P. and Natixis Investment Managers S.A.

Natixis Distribution, L.P. is a limited purpose broker-dealer and the distributor of various registered investment companies for which advisory services are provided by affiliates of Natixis Investment Managers.

3 Cerulli Quantitative Update: Global Markets 2018 ranked Natixis Investment Managers as the 16th largest asset manager in the world based on assets under management as of December 31, 2017.

4 Net asset value as of September 30, 2018. Assets under management (“AUM”), as reported, may include notional assets, assets serviced, gross assets and other types of non-regulatory AUM.

5 A division of Natixis Advisors, L.P.

6 A brand of DNCA Finance.

7 A subsidiary of Ostrum Asset Management.

8 Operated in the U.S. through Ostrum Asset Management U.S., LLC.

9 Caspian Private Equity is a joint venture between Natixis Investment Managers, L.P. and Caspian Management Holdings, LLC.

{kind=link}