Choice Equities Capital Management letter to investors for the first quarter ended March 31, 2018.

Q1 hedge fund letters, conference, scoops etc

Dear Investor:

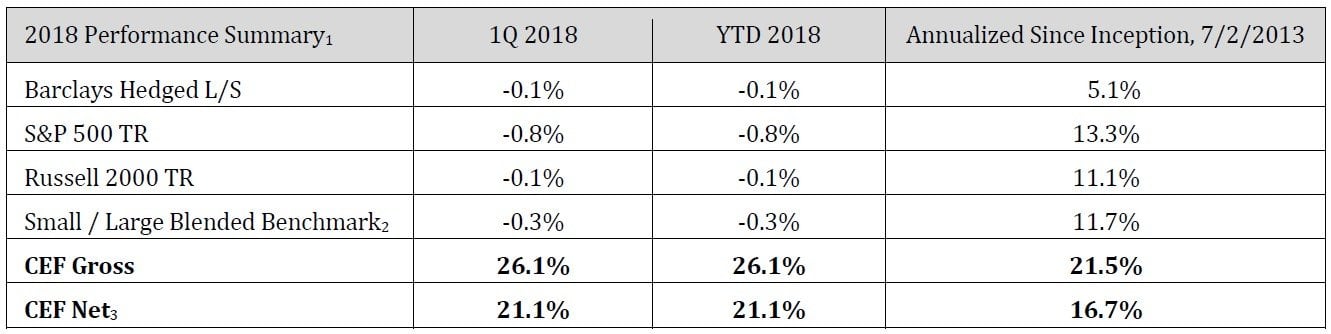

Choppy trading returned to the markets in the first quarter leaving the Russell 2000 basically unchanged at -.1% while the S&P 500 declined moderately by -.8%. Together these results put our Small / Large Blended Benchmark down -.3% for the quarter. Choice Equities Fund (CEF) was up +26.1% and +21.1% on a gross and net basis for the quarter. We are pleased to report the strong start to the year, particularly in the context of the generally flat market performance.

Executive Summary

In this letter, we will take a closer look at Bluelinx (BXC) given its outsized impact on the portfolio this quarter, and we will discuss Chipotle Mexican Grill (CMG), our most recent addition to the portfolio. We will also discuss a new small position we are closely evaluating and discuss its candidacy as a potential Choice Equities Special Opportunity Fund (CESOF). As is usual in our quarterly letters, we will close with a brief assessment of the current investment environment and market conditions.

Notable Portfolio Performance Drivers

BXC shares moved from ~$10 at the beginning of the year into the $30s during the quarter and were by far the largest driver of CEF’s positive performance. While we have already spent more than adequate time talking about deals and our affinity for distributor tie-ups in these letters before, we will have to go back to the well one more time as we highlight the cause of BXC’s performance. On the negative side, Sportman’s Warehouse (SPWM), which added +4% to fund performance in Q4, cost us just under -3% in Q1. We took some profits early in the year after shares spiked since our entry just a few months ago but were slower than we would have liked in trimming the position to a larger degree. The company is performing as expected though shares have again fallen to their level near our entry point at ~7x EPS. We exited our position in Performance Food Group with shares up ~+50% since our entry in early 2017 as the gap to our estimate of fair value closed.

On the short side, we initiated a position in an online furniture-oriented retailer at our standard short position size of 2%. Shares began to decline shortly thereafter, and the position contributed ~+50 basis points to fund performance for the quarter. We remind our investors short activity is unlikely to be a meaningful area of intentional focus in the near term. We believe most money is typically made on the long side. However, when we see a situation like this one where valuation appears to become completely divorced from the fundamentals of the business, we will participate. In this case, the company had consistently traded near a valuation of ~.2x sales for the last four years until it announced new endeavors in far afield areas of blockchain applications like bitcoin. Shares quintupled last fall as the company’s valuation exploded to ~1x sales, even as the company’s core operations continued to struggle. With the dust settling on the bitcoin mania in part driven by increasing actions of regulators, we established a position.

Portfolio Activity

BXC – A brief review of our investment in Bluelinx should prove helpful in understanding its recent performance. When we initially invested in BXC, we were buying shares of the company at about thirty cents to the dollar of our estimate of net asset value. While this sounds like an obvious bargain, it surely did not look this way to everyone - or perhaps more accurately - to the small sub-segment of investors even willing to look. Because of old marks on the company’s real estate, GAAP financials did not capture the current asset value accurately, so investors looking for undervalued companies using screens on typical financial metrics likely would not have noticed. For those that did look, they probably did not like what they found. A cursory look at that time would have shown a company suffering from a prior management team’s operational missteps, skinny operating margins and a company generally underachieving in a soft housing market. We dug deeper and found a recently installed top flight management team pursuing an appropriate corporate strategy intent on restoring promise to an operation that had once been the biggest building products distributor in the U.S. With significant real estate assets backstopping their mortgage and steady tailwinds from a resurgent housing market, our view was management simply needed to figure out how to turn their assets better to realize the significant value in its well-regarded distribution center network.

In early 2018, management validated that view in spades. In our Q4 letter, we noted their largest shareholder had exited in a sloppily priced secondary that priced at $7, an ~30% discount from recent trading levels. This was a meaningful decline which we participated in. But our comprehensive understanding of the situation allowed us to quickly recognize the situation for what it was: the uncommon and highly sought-after occurrence of lower prices on good news. Eyeing a business likely to do over $2 per share of earnings in 2018 with the company intent on soon unlocking more of the value present in their real estate, we added to our position.

As the calendar turned to 2018, a string of positive developments unfolded, and shares responded in kind. But before we jump into the events, we think it will also prove useful to remind our readers of a key reason we like these distribution companies so much: there are real synergies to be had in certain corporate tie-ups. While there are many ways a distributor can differentiate itself (service, scale, culture, etc), their assets are frequently quite homogenous. After all, at its most basic level, distributor operations simply consist of moving other companies’ manufactured products to end customers through a supply chain network, and for the most part, product is product and buildings are buildings. As a result, acquiring companies can realize synergies from capturing new customers, improving terms of product sourcing and eliminating redundant supply chain costs. These attributes create the potential for deals to create significant value.

Returning to the events of the quarter, the company announced sale lease-backs on their four largest distribution center properties a few weeks into 2018 in a transaction that generated $110M of proceeds. This refinancing allowed the company to pay off its remaining mortgage in its entirety leaving in place only a revolver for working capital as its remaining debt. Shares spiked into the mid-teens on the lowered leverage profile. At this point, our position size had grown through appreciation, but we maintained the outsized position given the attractive valuation and increasing attention the company was garnering in the investment community.

And something about their approach in the sale leaseback transaction struck us as a bit curious. Why did the company go the big bang route? Their mortgage schedule only called for principal payments of $55M in 2018. They could have accommodated this payment in myriad other ways. But this approach seemed to provide the greatest flexibility in managing the other 34 remaining properties in their distribution network going forward. Why would they want to preserve maximum flexibility across their remaining footprint? Was something bigger brewing?

In early March, we found out what the company was up to when Bluelinx announced its acquisition of its larger peer Cedar Creek. The deal is quite impressive in that its highly synergistic nature allows for it to achieve the rare combination of being both massively accretive, while simultaneously deleveraging. The map is the key. The distribution networks of the two companies are practically right on top of each other, meaning the combined entity will have many duplicative supply chain costs it can eliminate. Once the company adds the $60M of Cedar Creek LTM EBITDA to its $44M of LTM EBITDA and achieves the $50M of targeted synergies, the newly combined company will have a lower leverage profile and approach an earnings run rate in excess of $8 per share. Investors approved of the deal and sent shares into the $30s. Insiders subsequently followed suit with multiple buys acknowledging approval of their own. At this point, we took some profits and have reduced the position size to a still meaningful but more normal level. The outlook and valuation of 5x near term earnings power remains compelling, and we look forward to continuing to participate as shareholders in the newly combined company’s outsized opportunity.

We will close our discussion here with one final update. A year ago in the 1Q 2017 letter, I commented on having the pleasure to squeeze my way into attendance of a Best Ideas dinner in New York. While it was clear at the time our operation would have finished dead last in the category of assets under management, I am quite pleased to report that as a result of BXC’s strong performance we came out on top in the category you care about most. We would like to extend a sincere thank you to our hosts for the invitation and look forward to continuing to build on the relationships we developed there.

CMG – Our newest investment is a little larger than many of our typical holdings, but in this case, its large size and well-regarded brand is a significant component of the investment case. Chipotle, as you have probably heard, has had a rough couple of years. The troubles started in July 2015 when five customers fell sick with E. Coli that was traceable to a Chipotle location in Seattle, WA. Five other episodes followed by December which spanned multiple states and added salmonella and norovirus to the list of contracted illnesses. Then, in July 2017 after the company finally seemed to have these issues behind it, an employee sick with norovirus transmitted their illness to another 80 customers in Sterling, VA. The culpability for the food safety issues rests entirely on the company, and the incidents are a big deal, especially considering the pride with which the company touted its wholesome, locally-sourced ingredients and differentiated supply chain. Responsibility for the recent norovirus episode also falls on the company, though unlike the other events, it does not carry the same gravity of implications around a permanently impaired supply chain sourcing process. Whatever the causes, the series of troubling events led consumers to abandon the pioneering fast-casual burrito chain, and the once high-flying shares that had been driven by best in class unit economics, strong new store growth and coveted same-store sales growth were subsequently cut into a third.

The food safety issues are neither trivial nor without precedent. The company simply must figure out how to deliver fresh food that tastes good safely and consistently. But as we look through history to draw informed conclusions about potential outcomes, we see that consumers tend to forgive and forget, especially if the product is valued. McDonald’s, Burger King and Taco Bell have all had their issues. Events at Jack-in-the-Box were the most unfortunate, sickening 732 and ultimately killing four. We do not attempt to make light of any of these tragic events. But in this case, it is useful to note the West Coast burger chain managed to put their food safety issues behind them and was still subsequently able to double their store base. As for the evaluation of Chipotle’s product, in what must be either one of the more ironic legal outcomes in recent memory or simply a new low for our judicial system, one of the people who sued the company due to illness, actually settled for coupons for free food – from Chipotle! It is unclear if this anecdote says more about our country’s legal system or Chipotle’s brand, but at a minimum, it seems to support the notion the product is valued.

Since the food issues cropped up, Chipotle has taken significant steps to ensure the safety of its food. And they look to have made good progress on this score as the supply chain issues have not resurfaced since 2015. They have done other things as well. They have rolled out a new app to enable mobile ordering. And they have implemented second make lines which will allow them to serve more customers, particularly ones that order via the app. These are steps in the right direction and will improve throughput. But throughput is not the problem. The problem is many of their customers left and have not come back. As a result, traffic counts have been steadily declining ever since the first food safety episode in 2015.

The company has made some efforts to win back their customers. They tried some promotions and have had some moderate success in a loyalty program offering. But relative to other concepts, it appears the company is only scratching the surface of what is possible from a marketing and outreach perspective. Why is this? Corporate culture may provide some explanation. When Chipotle burst onto the scene as a category killer in the fast-casual restaurant space over a decade ago, its brand was thriving. The company eschewed the typical corporate marketing strategies and instead opted for a grass roots marketing campaign that was largely done by word of mouth. The company’s fast and delicious “food with integrity” simply spoke for itself. As a result, in terms of marketing, it simply was not in the company’s DNA, and if anything, they became known more for their lack of it than anything else.

But it is time for a change. And we think incoming CEO Brian Niccol will be that agent for change. His playbook, developed in turning around what was once thought of as a completely lifeless Taco Bell concept with a blend of snappy marketing, menu innovation and social media outreach, looks to be the right one. If Chipotle can get bring its customers back, profits will follow. Shares do not look statistically cheap on most current financial metrics. But most financial metrics do not account for the brand value which continues to endure as a standout in the fast-casual restaurant space. Should improved marketing efforts position the company to capitalize on their franchise value and approach operating margins of the pre-food crisis levels, shares at current levels will prove to have been a bargain and could turn into a compounding machine. Fortunately, we do not need this scenario to unfold for a successful investment as even modest success in this area will likely produce a highly satisfactory result. We began legging into our position a week after Mr. Niccol’s appointment and will adjust the position size as we continue to evaluate risk and return.

CESOF – We believe we have identified a company that may be a good fit for a CESOF. It is an obscure company and one that is even a little small for us. Upside is not difficult to imagine, but our position size in the fund will be limited due to the lack of liquidity in shares’ daily trading volumes. In the case of a successful investment, the investment could add several percentage points to CEF performance. In a CESOF, which will be wholly comprised of this single position and carry differing risk, reward and liquidity considerations, we have the opportunity to do much better.

In the event the CESOF is a green light, we will attempt to raise a finite pool of capital that will maximize the potential returns of the investment. Existing CEF investors will have first right of refusal to fill the potential desired asset level while prospective investors will have the opportunity in the event the fund is not oversubscribed. We are closely evaluating the company and look forward to updating you on these efforts.

Shorts/Hedges/ETFs – In addition to the single short position introduced this quarter, we hold a few small short positions in four ETFs and some residual cash from the recent sales of BXC in the portfolio. The short ETF positions act as hedges and allow us to lower our overall market exposure while maintaining the ability to participate as owners in companies we believe offer attractive risk / reward characteristics.

2018 OUTLOOK – We have no meaningful changes to report in our broader investment views from our outlook just a few months ago. The placid markets of 2017 appear to be a thing of the past as investors begin to view those conditions for the anomaly they were. The economy looks strong and confidence is surging. The market appears to be digesting last year’s gains as well as the emergence of a few new narratives like rising rates, inflation and posturing in the global battle for preferred terms of trade. Our focus as always is on earnings which are quite strong and coming in at a growth rate of over +20% for Q1. We are enthused about recent additions to the portfolio and continue to believe our prospects are more exciting than what can be found in the broader market itself.

Conclusion

As always, we are happy to discuss any portfolio holdings or our investment outlook with you at any time. Please reach out to us at any time. In closing, we are honored and privileged to have the responsibility you have entrusted in us in managing your capital, and we look forward to continuing our relationship further into the future.

Best regards,

Mitchell Scott, CFA

Portfolio Manager

Choice Equities Capital Management