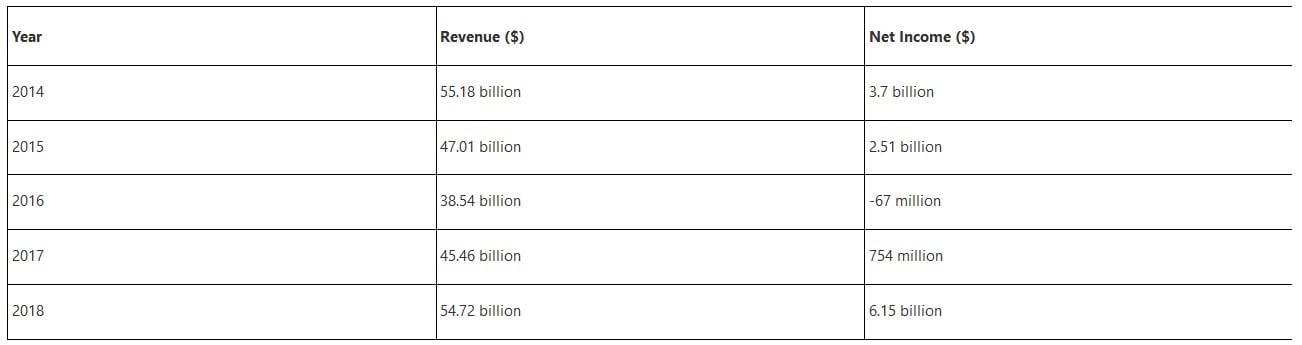

Finding a great business which is also a great stock can be a challenge, but at present I am convinced that Caterpillar Inc. (NYSE:CAT) is both, and I will outline why in the following. Most people reading this will know that Caterpillar is the biggest manufacturer of earthmoving equipment in the world, and that it is a cyclical business. This is reflected in the revenue and net income figures reported over the past five years.

Another fact reflected in the revenue and net income figures relayed above is the disparity between the revenue figures and net income figures. This disparity is down to how capital intensive Caterpillar’s business operations are. And yet, despite its cyclical nature and capital-intensive business model, Caterpillar maintain a solid financial position. With total assets of $78.73 billion against total liabilities of $63.25 billion, Caterpillar has a net worth of $15.48 billion. In tandem with cash of $7.16 billion and accounts receivable of $17.89 billion, and Caterpillar’s long-term debt of $24.24 billion is not quite as off-putting.

Q1 hedge fund letters, conference, scoops etc

Further proof of Caterpillar's sound financial position can be gleaned from its dividend record - Caterpillar has rewarded investors with consecutively rising dividends for twenty-six years, a streak which makes it a de-facto dividend aristocrat and which is impressive for a cyclical firm (especially taking the Great Recession into account). And with a payout ratio of 30.90%, that dividend can continue to be raised going forward.

Looking ahead, Caterpillar is not without risks as an investment. I have now labelled the firm cyclical twice, and that is due to its reliance on global economic growth. After all, a growing economy will have a higher appetite for earthmoving equipment and the fixed costs of manufacturing such equipment are so high that established players such as Caterpillar have little difficulty fending off competition. So long as a severe economic recession does not hit, Caterpillar's anticipated earnings-per-share growth of 5.63% over the next year and of 19.13% over the next five years appears realistic.

Recent business performance has been encouraging - the very good 2018 results outlined in the table above indicate how Caterpillar's competitive advantage facilitates its growth. And the Q1 2019 results reinforce this encouraging outlook.

However, with global issues such as the ongoing U.S./China trade war having impacts and the fact that many observers opine that we are long overdue for a recession, a cyclical stock such as Caterpillar - even with its excellent recent performance, sound fiscal position, outstanding dividend record, and strong competitive advantage - is out of favor. The fears that investors entertain in that regard are borne out by the 20.17% fall in share price that Caterpillar has seen over the past year from its 52-week high of $159.37.

These fears are not groundless, but they do seem overblown. Nevertheless, such fears do drive home the necessity of getting Caterpillar at the right price. On the evidence presented thus far, it is fair to say that Caterpillar is a great business. At this time, though, at $127.23 per share, is it a great stock?

I have revised my approach to valuation more thoroughly, and believe that the great Dave van Knapp's approach to valuation is in accord with my overall investing philosophy. He takes a four step approach, then averages the four steps to get his fair price. I find three of these four steps to be a sound means of valuing a stock, and eschew one of these - his use of Morningstar's fair price valuations - on the grounds that Morningstar use a DCF method, which I have previously repudiated. The virtue of van Knapp's approach is that at every step, the current price is kept firmly in mind to determine fair value. And as a certain well-known gentleman once opined: "price is what you pay, value is what you get."

So, the first step is to compare the current stock valuation to the average historical valuation of the market in general. The market's average historical P/E is 15, and Caterpillar's current P/E is 12.39. So we now divide current P/E by the market's historical average P/E to get a valuation ratio:

12.39 / 15 = 0.826

Next, we divide the current price by this valuation ratio:

$127.23 / 0.826 = $154.03.

So our first step gives us a fair value of $154.03. This suggests the stock is undervalued at this time, but is it? To be sure, we move on to step two.

In the second step, we compare the stock's valuation to its own five-year average valuation. As already stated, Caterpillar's current P/E is 12.39, and its five-year average P/E is 75.75. So we now divide current P/E by the five-year average P/E to garner a valuation ratio:

12.39 / 75.75 = 0.163

Next, we divide the current price by this valuation ratio:

$127.23 / 0.163 = $780.55.

This is a shockingly different result from the one that the first step yielded. One thing they both have in common, however, is that they suggest the stock is currently undervalued. However, we still have step three to go through.

In the third step, we compare the stock's current dividend yield to its five-year average yield. Caterpillar's current dividend yield is 3.24%, and its five-year average yield is 3.00%. So we now divide the five-year average yield by the current yield to garner a valuation ratio:

3.00 / 3.24 = 0.926

Next, we divide the current price by this valuation ratio:

$127.23 / 0.926 = $137.40

This is far closer to the current price than either of the previous two figures - especially the second one. Now that these steps have been completed, we need to find the average of these three figures:

154.03 + 780.55 + 137.40 / 3 = $357.33.

If we average all three figures, fair value for Caterpillar comes to $357.33. However, if we were to treat step two as an outlier, and restricted ourselves to the figures from step one and step three, we get the following:

154.03 + 137.40 / 2 = $145.72.

I personally think the latter figure is a more reasonable estimate of fair value. The former figure would indicate that Caterpillar is undervalued by 180%, which is unlikely, while the second figure suggests it is undervalued by 15%. However, both figures tell the same tale: Caterpillar is undervalued at this time, and is a worthy addition to a long-term portfolio for investors that have a high tolerance for cyclical stocks. It is this cyclical quality and its capital-intensive nature that has caused many investors to be bearish on it at this time, overlooking its superior fiscal discipline and excellent dividend record.

DISCLAIMER: The author is not a financial professional and accepts no responsibility for any investment decisions a reader makes. This article is presented for information purposes only. Furthermore, the figures cited are the product of the author's own research and may differ from those of other analysts. Always do your own due diligence when researching prospective investments.