What You Will Learn

- The problems with EBITDA as your go to solution

- The problems EBITDA causes with over-valuation

- Buffett, Munger and Klarman’s thoughts and explanations on EBITDA

What Adjustments to Reported Earnings Do You Make?

Here's what Buffett and Munger had to say about EBITDA in the 2003 shareholder meeting.

[When goodwill was required to be amortized,] we ignored amortization of goodwill and told our owners to ignore it, even though it was in GAAP [Generally Accepted Accounting Principles]. We felt that it was arbitrary.We thought crazy pension assumptions caused people to record phantom earnings. So, we're willing to tell you when we think there's data that is more useful than GAAP earnings.

Not thinking of depreciation as an expense is crazy. I can think of a few businesses where one could ignore depreciation charges, but not many. Even with our gas pipelines, depreciation is real — you have to maintain them and eventually they become worthless (though this may be 100 years).

It [depreciation] is reverse float — you lay out money before you get cash. Any management that doesn't regards depreciation as an expense is living in a dream world, but they're encouraged to do so by bankers. Many times, this comes close to a flim flam game.

People want to send me books with EBITDA and I say fine, as long as you pay cap ex. There are very few businesses that can spend a lot less than depreciation and maintain the health of the business.

This is nonsense. It couldn't be worse. But a whole generation of investors have been taught this. It's not a non-cash expense — it's a cash expense but you spend it first. It's a delayed recording of a cash expense.

We at Berkshire are going to spend more this year on cap ex than we depreciate.

[CM: I think that, every time you saw the word EBITDA [earnings], you should substitute the word “bullshit” earnings.]- Source: What adjustments to reported earnings do you make?

Buffett's Thoughts on EBITDA?

A year before that in 2002, it was pretty much the same when it came to EBITDA.

It amazes me how widespread the use of EBITDA has become. People try to dress up financial statements with it.

We won't buy into companies where someone's talking about EBITDA. If you look at all companies, and split them into companies that use EBITDA as a metric and those that don't, I suspect you'll find a lot more fraud in the former group. Look at companies like Wal-Mart, GE and Microsoft — they'll never use EBITDA in their annual report.

People who use EBITDA are either trying to con you or they're conning themselves. Telecoms, for example, spend every dime that's coming in. Interest and taxes are real costs.

Seth Klarman on EBITDA from his Book Margin of Safety

Below is an excerpt from Seth Klarman's Margin of Safety, with a discussion about the value of EBITDA as a measure of earnings.

A Flawed Definition of Cash Flow, EBITDA, Leads to Overvaluation

Investors in public companies have historically evaluated them on reported earnings. By contrast, private buyers of entire companies have valued them on free cash flow.

In the latter half of the 1980's, entire businesses were bought and sold almost as readily as securities, and it was not unreasonable for investors in securities to start thinking more like buyers and sellers of entire businesses.

There is, of course, nothing wrong with re-examining an old analytical tool for continued validity or with replacing one that has become outmoded.

Thus, in a radical departure from the historical norm, many stock and junk-bond buyers in the latter half of the 1980's replaced earnings with cash flow as the analytical measure of value.

In their haste to analyze free cash flow, investors in the 1980's‘ sought a simple calculation, a single number that would quantify a company‘s cash-generating ability. The cash-flow calculation the great majority of investors settled upon was EBITDA (earnings before interest, taxes, depreciation and amortization).

Virtually all analyses of highly leveraged firms relied on EBITDA as a principal determinant of value, sometimes as the only determinant.

Even non-leveraged firms came to be analyzed in this way since virtually every company in the late 1980's was deemed a potential takeover candidate.

Unfortunately EBITDA was analytically flawed and resulted in the chronic overvaluation of businesses.

How should cash flow be measured?

Before the junk-bond era investors looked at two components: after-tax earnings, that is, the profit of a business; plus depreciation and amortization minus capital expenditures, that is, the net investment or disinvestment in the fixed assets of a business.

The availability of large amounts of nonrecourse financing changed things. Since interest expense is tax deductible, pre-tax, not after-tax earnings are available to pay interest on debt; money that would have gone to pay taxes goes instead to lenders.

A highly leveraged company thus has more available cash flow than the same business utilizing less leverage.

Notwithstanding, EBIT (earnings before interest and taxes) is not necessarily all freely available cash. If interest expense consumes all of EBIT, no income taxes are owed. If interest expense is low, however, taxes consume an appreciable portion of EBIT.

At the height of the junk-bond boom, companies could borrow an amount so great that all of EBIT (or more than all of EBIT) was frequently required for paying interest. In a less frothy lending environment companies cannot become so highly leveraged at will.

EBIT is therefore not a reasonable approximation of cash flow for them. After-tax income plus that portion of EBIT going to pay interest expense is a company‘s true cash flow derived from the ongoing income stream.

Cash flow, as mentioned, also results from the excess of depreciation and amortization expenses over capital expenditures. It is important to understand why this is so.

When a company buys a machine, it is required under generally accepted accounting principles (GAAP) to expense that machine over its useful life, a procedure known in accounting parlance as depreciation. Depreciation is a noncash expense that reduces reported profits but not cash.

Depreciation allowances contribute to cash but must eventually be used to fund capital expenditures that are necessary to replace worn-out plant and equipment.

Capital expenditures are thus a direct offset to depreciation allowance; the former is as certain a use of cash as the latter is a source. The timing may differ: a company may invest heavily in plant and equipment at one point and afterward generate depreciation allowances well in excess of current capital spending.

Whenever the plant and equipment need to be replaced, however, cash must be available. If capital spending is less than depreciation over a long period of time, a company is undergoing gradual liquidation.

Amortization of goodwill is also a noncash charge but, conversely, is more of an accounting fiction than a real business expense.

When a company is purchased for more than its tangible book value, accounting rules require the buyer to create an intangible balance sheet asset known as goodwill to make up for the difference, and then to amortize that goodwill over forty years.

Amortization of goodwill is thus a charge that does not necessarily reflect a real decline in economic value and that likely not be spent in the future to preserve the business. Charges for goodwill amortization usually do represent free cash flow.

It is not clear why investors suddenly came to accept EBITDA as a measure of corporate cash flow. EBIT did not accurately measure the cash flow from a company‘s ongoing income stream. Adding back 100% of depreciation and amortization to arrive at EBITDA rendered it even less meaningful.

Those who used EBITDA as a cash-flow proxy, for example. Either ignored capital expenditures or assumed that businesses would not make any, perhaps believing that plant and equipment do not wear out.

In fact, many leveraged takeovers of the 1980s forecast steadily rising cash flows resulting partly from anticipated sharp reductions in capital expenditures. Yet the reality is that if adequate capital expenditures are not made, a corporation is extremely unlikely to enjoy a steadily increasing cash flow and will instead almost certainly face declining results.

It is not easy to determine the required level of capital expenditures for a given business.

Businesses invest in physical plant and equipment for many reasons: to remain in business, to compete, to grow, and to diversify.

Expenditures to stay in business and to compete are absolutely necessary. Capital expenditures required for growth are important but not usually essential, while expenditures made for diversification are often not necessary at all.

Identifying the necessary expenditures requires intimate knowledge of a company, information typically available only to insiders.

Since detailed capital-spending information was not readily available to investors, perhaps they simply chose to disregard it.

Some analysts and investors adopted the view that it was not necessary to subtract capital expenditures from EBITDA because all the capital expenditures of a business could be financed externally (through lease financing, equipment trusts, nonrecourse debt, etc.).

One hundred percent of EBITDA would thus be free pre-tax cash flow available to service debt; no money would be required for reinvestment in the business. This view was flawed, of course. Leasehold improvements and parts of a machine are not typically financeable for any company.

Companies experiencing financial distress, moreover, will have limited access to external financing for any purpose. An overleveraged company that has spent its depreciation allowances on debt service may be unable to replace worn-out plant and equipment and eventually be forced into bankruptcy or liquidation.

EBITDA may have been used as a valuation tool because no other valuation method could have justified the high takeover prices prevalent at the time.

This would be a clear case of circular reasoning.

Without the high-priced takeovers there were no upfront investment banking fees, no underwriting fees on new junk-bond issues, and no management fees on junk-bond portfolios.

This would not be the first time on Wall Street that the means were adapted to justify an end. If a historically accepted investment yardstick proves to be overly restrictive, the path of least resistance is to invent a new standard.

EBITDA Analysis Obscures the Difference between Good and Bad Businesses

EBITDA, in addition to being a flawed measure of cash flow, also masks the relative importance of the several components of corporate cash flow. Pretax earnings and deprecation allowance comprise a company's pretax cash flow; earnings are the return on the capital invested in a business, while depreciation is essentially a return of the capital invested in a business.

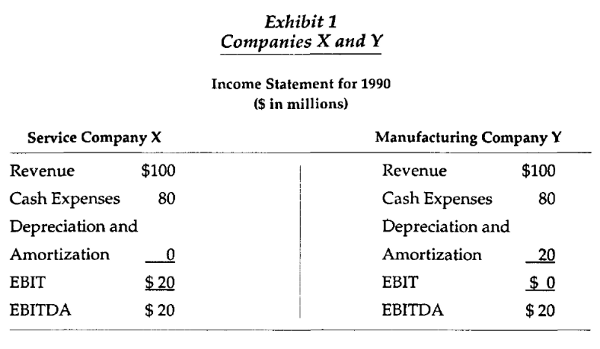

To illustrate the confusion caused by EBITDA analysis, consider the example portrayed in exhibit 1.

Investors relying on EBITDA as their only analytical tool would value these two businesses equally.

At equal prices, however, most investors would prefer to own Company X, which earns $20 million, rather than Company Y, which earns nothing. Although these businesses have identical EBITDA, they are clearly not equally valuable. Company X could be a service business that owns no depreciable assets.

Company Y could be a manufacturing business in a competitive industry. Company Y must be prepared to reinvest its depreciation allowance (or possible more, due to inflation) in order to replace its worn-out machinery. It has no free cash flow over time.

Company X, by contrast, has no capital-spending requirements and thus has substantial cumulative free cash flow over time.

Anyone who purchased Company Y on a leveraged basis would be in trouble. To the extent that any of the annual $20 million in EBITDA were used to pay cash interest expense, there would be a shortage of funds for capital spending when plant and equipment needed to be replaced.

Company Y could eventually go bankrupt, unable both to service its debt and maintain its business. Company X, by contrast, might be an attractive buyout candidate.

The shifts in investor focus from after-tax earnings to EBIT and then to EBITDA masked important differences between businesses, leading to losses for many investors.”

About the Author

The pseudonymous Hurricane Capital was Born in the 80's, lives in Sweden with a Masters of Science in Business and Economics from Stockholm University. Got interested in value investing and devotes his free time and investing. The main goal through the Hurricane Capital blog is to learn about different investing topics, investors and business cases for investment.

The pseudonymous Hurricane Capital was Born in the 80's, lives in Sweden with a Masters of Science in Business and Economics from Stockholm University. Got interested in value investing and devotes his free time and investing. The main goal through the Hurricane Capital blog is to learn about different investing topics, investors and business cases for investment.

Additional Articles I Recommend

- Changes in Working Capital and Owner Earnings – The… What You Will Learn What the "change" REALLY means in…

- The Evolution of Warren Buffett's Career from 1936 to… Take a look at how Buffett's career evolved and what…

- Why Apple Is the Best Retail Stock According to this 15… (This is a guest post. The author's views are entirely…

- My Top 10 Stock Valuation Ratios and How to Use Them (edit: this article has been updated with additional commentary, new…

- Uncovering How Buffett Interprets the Financial Statements Get insights into how Buffett would analyze financial statements.

This post was first published at old school value.

You can read the original blog post here What Buffett and Seth Klarman Say About EBITDA.