Bonhoeffer Fund commentary for the third quarter ended October 30, 2020, providing a case study on MMA Capital Holdings Inc (NASDAQ:MMAC).

Q3 2020 hedge fund letters, conferences and more

Dear Partner,

The Bonhoeffer Fund returned 5.1% net of fees in the third quarter of 2020 compared to up 5.0% for the MSCI World ex-US, a broad-based index. Our year-to-date performance is down 15.2% net of fees, compared to the DFA International Small Cap Value Fund, which is down 15.9%. (As described in our last letter, the DFA International Small Cap Value Fund is a fund with the closest representative comparison to Bonhoeffer). As of September 30, 2020, our securities have an average earnings/free cash flow yield of 20.7% and an average EV/EBITDA of 4.0. The DFA International Small Cap Value Fund has an average earnings yield of 8.4%. The difference between the portfolio’s market valuation and my estimate of intrinsic value is still large (greater than 100%). I remain confident that the gap will close over time and continue to monitor each holding accordingly.

The US election has been a roller coaster over the past few months. Historically, for the most part, the party in charge has made changes at the edge of policy due to divided government. This looks like it is going to continue with the 2020 election result. It looks like Donald Trump has lost to Joe Biden, but his coattails were pretty short. The Republicans look to gain between seven to thirteen House seats, along with retaining the control of the Senate. The overall result, in my opinion, is better than one-party control and will result in either limited executive actions or compromise legislation and gradual versus quick change.

Bonhoeffer Fund Portfolio Overview

Bonhoeffer’s investments have not changed significantly in the last quarter. Our largest country exposures include: South Korea, Italy, South Africa, Hong Kong, United Kingdom, and Philippines. The largest industry exposures include: distribution, consumer products, telecom, and transaction processing.

Year-to-date successes have been in Korean special situations, and challenges have been in Hong Kong and South African securities. A key to the challenges has been sum-of-the-parts (SOTP) theses that have not approached fair value to date. SOTP theses are dependent upon growth and better governance to reduce the discount.

The growth in South Africa has been a challenge for our South African holdings due to the effects of COVID on the South African economy. Given the success of the COVID vaccines trials, I am optimistic about recovery in South Africa in 2021. This is an example of geographic arbitrage, described in the section below. Governance is improving in our South African holdings and, in my opinion, the current pricing more than reflects the governance situation in Hong Kong.

Since my last letter, we have added a position in an alternative asset management fund. This area is one of current interest due to low interest rates and the growth from alternative energy infrastructure build-outs around the country which will provide a nice tailwind. See the case study for details.

As discussed in the last letter, we will be reporting on holdings by special situation type (i.e., compound mispricings and public LBOs) and theme.

Compound Mispricings (61% of Portfolio; Quarterly Average Performance +18%)

These securities include the Korean preferred stocks, the nonvoting share of Buzzi, Telecom Italia, and Wilh. Wilhelmsen and some holding companies (HoldCos). The thesis for the closing of the voting, nonvoting, and holding company gap is better governance and liquidity, and corporate actions like spin-offs, sales, or holding company transactions and overall growth. Telecom Italia’s discount (in Italy) has disappeared over our holding period, but further unlocking of value is happening with a combination of its Italian telecom networks with Enel and the consolidation of the Brazilian telecom market the Telecom participates in via TIM.

Buzzi has a savings shares/ordinary share swap offer (33% discount) which is underwhelming. Unfortunately, the company can compel savings shareholders to accept this offer or a lower value based upon book value despite previous savings/ordinary offers from other Italian firms (like Exor) closer to a 5% to 10% discount. However, the long-term outlook for Buzzi is good and should be a beneficiary of any US infrastructure programs; thus continuing to hold this quality infrastructure firm makes sense. Buzzi’s management is focused on creating shareholder value in its primary markets (US/Mexico and Europe) with expanded investments in Brazil and should do well with increased infrastructure spending in the US.

The Korean preferred discounts in our portfolio are still large (20% to 37%). The trends of better governance and liquidity have reduced the discount in names like Samsung Electronics, and more preferred names trade at a premium to common shares. We sold out of a Korean HoldCo transaction in Taeyoung Engineering & Construction which provided a nice upside over the past three months.

Public LBOs (26% of Portfolio; Quarterly Average Performance -9%)

This includes our broadcast TV franchises, leasing and roll-on/roll-off (RORO) shipping, and our natural gas pipeline firms. One trend in these levered firms is the increasing spread between bond yields and the firms’ free cash flow yield. An example is Gray Television, whose FCF yield is 32% at September 30, 2020, from 19% at year-end, while its debt yield has increased to 4.5% from 3% with the bond/equity FCF spread increasing from 16% to 28%. What is unusual today is that the bond yields have returned to 4.5%, but the free cash flow yield has remained unchanged. Gray has taken advantage of this mispricing by buying back almost 5% of its shares during the first nine months of the year. Management has done the same, buying a large amount of stock in the low $20s.

Today there is a changing media landscape including an ocean of content looking for viewers. Gray provides a curated mix of local news and weather, as well as content over various over-the-air and cable channels. The number of channels will increase with the introduction of ATSC 3.0 which provides broadcast-quality television directly to mobile phones and devices. ATSC 3.0 channels will be provided to each local broadcast television license holder such as Gray.

Gray Television has been the beneficiary of the current election showdown in the Senate. Georgia is going to be a key state in this showdown and Gray is dominant in five of Georgia’s seven largest markets which should add a boost to Q4 earnings as election advertising has high incremental profit margins.

Our natural gas pipelines continue to have large debt/DCF yields. Growth prospects are good with natural gas prices rising (supporting producer profitability), the US and the world demand increasing with economies coming out of the COVID shut-downs, and the continued low oil prices reducing the drilling demand for oil, much of which has large amounts of almost-free associated natural gas.

Distribution Theme (33% of Portfolio; Quarterly Performance -2%)

This includes our holdings of car and branded capital equipment dealerships, online shopping, and capital equipment leasing firms. One of the main kay performance indicators (KPIs) for dealerships and shopping is velocity, as described below. We own some of the highest velocity dealerships in markets around the world. There have been challenges in some markets hit by COVID, like South Africa, however, there should be recovery once a vaccine is approved and distributed.

Telecom/Transaction Processing Theme (30% of Portfolio; Quarterly Performance +3%)

This includes our transaction processing and telecom firms. Despite continued expected performance, these firms have lagged in the rebound. The increasing use of transaction processing in our firms’ markets and the roll-out of 5G will provide growth opportunities. Given that most of these firms are holding companies and have multiple components of value (including real estate), the timeline for realization may be longer than for other firms.

Consumer Product Theme (18% of Portfolio; Quarterly Performance +8%)

This includes our holdings of food, consumer product, tire, and beverage firms. The defensive nature of these firms has led to better-than-average performance. We are in the process of accepting a take-out offer for a beverage firm we own that is being bought by another beverage firm we own.

Real Estate/Construction Theme (26% of Portfolio; Quarterly Performance +18%)

This includes our holdings of real estate, residential construction, and cement firms. One holding area is Hong Kong/China real estate which has been rocked by both the coronavirus and the actions of the Chinese Communist Party in Hong Kong. In my opinion, the pricing of our real estate holdings includes both a recession in Hong Kong and a communist takeover of Hong Kong. The current cement and construction holdings should do well as the world recovers from COVID shutdowns and governments start infrastructure programs.

Velocity

One important feature of firm cash flow growth is velocity. Velocity is how fast a firm is generating revenue from customers or a group of customers. Velocity can be measured by specific working capital item such as inventory turns for a retailer or distributor, a recurring revenue rate for a software or service provider, or increasing transactions for a marketplace or transaction processor. Velocity is a key driver of return on assets, as velocity times profit margin equals return on assets. Velocity is multiplicative to margins in creating return on equity versus linear changes associated with higher margins and leverage.

An illustration of velocity can be seen in auto dealerships. If a dealer can sell more automobiles (i.e., turn the inventory) faster than competitors in a market, then they can either offer lower prices resulting in even more unit sales or have the same sale price with higher units sold per year. The result, either way, is higher return on assets. Velocity also becomes a key metric in measuring how fast cars can be matched to customers resulting in a transaction. Stepping back from the transaction itself, metrics like net promoter score (NPS) can be used to measure intentions, but ultimately the close rate of intentions to transaction is the relevant key performance indicator. Inventory turns combine both intentions and actions into one KPI. The inventory turn rate is related to customer happiness, as happiness can provide evidence of the ultimate network effect amongst customers. Velocity can also be a measure of customer happiness. Increasing velocity, acceleration (increasing inventory turns, recurring revenue rates, or transaction velocity) can be a measure of increasing happiness and a signal of a network effect amongst customers. Sarah Tavel has a nice set of articles on Medium that describe happiness in marketplaces and how to measure and enhance it for both buyers and sellers in marketplaces.1 She mentions NPS as another metric used to gauge customer happiness, but its focus is intention, not actions. Actions, she posits, are measured by recurring revenues from existing customers. In the case of retailers/distributors, this translates into inventory turns.

Relative velocity to peers can be used to measure the moat or relative customer satisfaction on a consistent measurement basis. If we look at Cambria Automotive in the UK car dealer market, for example, its inventory turns were 5.8x in 2019, versus 6.0x in 2016. Cambria comps Vertu Motors and Lookers had turns of 4.3x to 4.8x over the 2016 to 2019 period. Cambria has a 1.1 to 1.5x inventory turn advantage over its comps. In addition, Cambria has margin advantage of 50 to 60 bps in margins over Vertu and Lookers. Cambia’s market position advantage is reflected in relative margins and inventory turns. This advantage provides Cambria with a moated advantage over Vertu and Lookers. One automobile dealer whose focus is on inventory turns as a KPI is China MeiDong (20x turns). This firm has one of the highest returns on equity (mid-20s to mid-30s) of car dealerships worldwide. If we look at our South African dealership, Combined Motor Holdings, it has about a 5x turn advantage over Motus and about an 80-bps-lower margin which creates a 6% to 10% advantage in return on equity.

We use velocity and long-term changes in velocity to assess the growth potential for our portfolio holdings. As an example, in our case study, MMAC reports the loan customer retention rate of 81% and a seven-month average remaining term. So, over a year, new loans are originated 1.4 times. The ability to generate new loans from existing customers reduces customer acquisition costs and increases the lifetime value of a customer. In the niche that MMAC occupies, the size of the market reduces the competition. MMAC’s competition is primarily small banks which, in most cases, have higher efficiency ratios and funds which have lower efficiency ratios but limited access to underwriting expertise.

Velocity also has scale advantages, as the amount of fixed operating costs (sales and marketing, facilities, and customer support) can be spread across more sales per year. This is similar to local economies of scale advantages that local distributors have. Higher velocity combined with fixed costs creates velocity-based economies of scale.

Geographic Arbitrage

Another tool that can be used in international portfolios is geographic arbitrage. This is a situation where an event and subsequent actions (like the COVID-19 epidemic and the associated lockdowns) begin in one geography and then spread around the world. COVID-19 struck China first, then spread to Europe, then to the US and to the emerging markets. We can look at automobile dealers to see how a COVID recovery may play out in Europe and emerging markets by taking a look at China and the US.

The high-inventory-turn firm China MeiDong (described above), located in mainland China, is an example of a firm that was directly affected by the COVID shutdowns in late 2019 and 2020 in China and the subsequent re-openings. Since the decline in the spring, China MeiDong’s share price has increased 140% above the pre-COVID levels. The high-inventory-turn auto retailers in the US are at pre-COVID levels, while the high-inventory-turn UK dealers are down by about 30%, down 35% in South Africa, and down 45% in Greece. If the recovery seen in China and the US spreads to the rest of the world, then we should see recovery in the lagging European and emerging markets firms’ stock prices.

Efficiency in Financial Services

As velocity is a measure of efficiency in distribution, costs measured by the efficiency ratio is a measure of efficiency for financial services companies. The efficiency ratio—noninterest expense divided by net interest income plus fees—measures the expenses investors pay to have access to an interest-generating asset. If the asset is levered, then the net interest margin (NIM)—asset return plus fee income less the borrowing cost—represents the return to the investor before costs. Good underwriting provides large net interest margin, as the asset returns are asset yields less expected losses.

MMAC’s solar loans have above-average NIMs and better-than-average underwriting, with no losses since 2015. MMAC’s relatively high efficiency ratio reduces the returns of these above-average NIMs. However, the net return to shareholders returns are better than most other spread-based businesses like banks and other BDCs and can further increase as the efficiency ratio is driven down.

Conclusion

As always, if you would like to discuss any of the philosophies or investments in deeper detail, then please do not hesitate to reach out. Until next quarter, thank you for your confidence in our work and have a safe and restful remainder of the fall and a blessed 2020 holiday season.

Warm Regards,

Keith D. Smith, CFA

CASE STUDY: MMA Capital (MMAC)

MMA Capital (MMAC) is an alternative asset fund. Historically, MMAC was an asset manager so the transition to an alternative asset fund has created an interesting investment opportunity. MMA Capital is managed by Hunt Investment Management, LLC (HIM), an experienced originator and asset manager in the renewable energy lending sector. Since 2015, HIM has originated over 190 loans for 760 renewable projects in 24 US states and territories. MMAC has investments in renewable energy (primarily solar projects) bridge financing and legacy investments in affordable housing debt and real estate debt and equity. MMA Capital is selling the legacy portfolio investments to fund new renewable energy bridge financing investments. The renewable energy bridge financing is provided to renewable power developers between the pre-construction and operations phases of renewable power projects. About 67% of the portfolio is for construction financing while 33% is for pre-construction financing for design and land purchases. In the operations phase of a renewable power project, lower long-term financing can be obtained due to the long-term power purchase agreements with creditworthy electric utilities. These loans facilitate the current disruption taking place in the energy generation business with solar displacing coal for power generation.

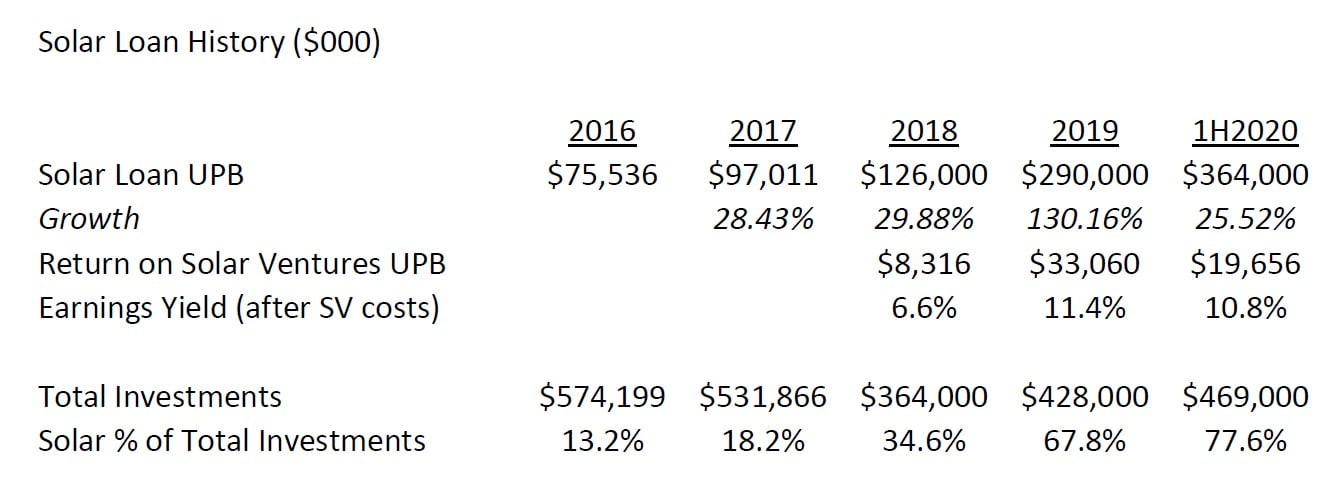

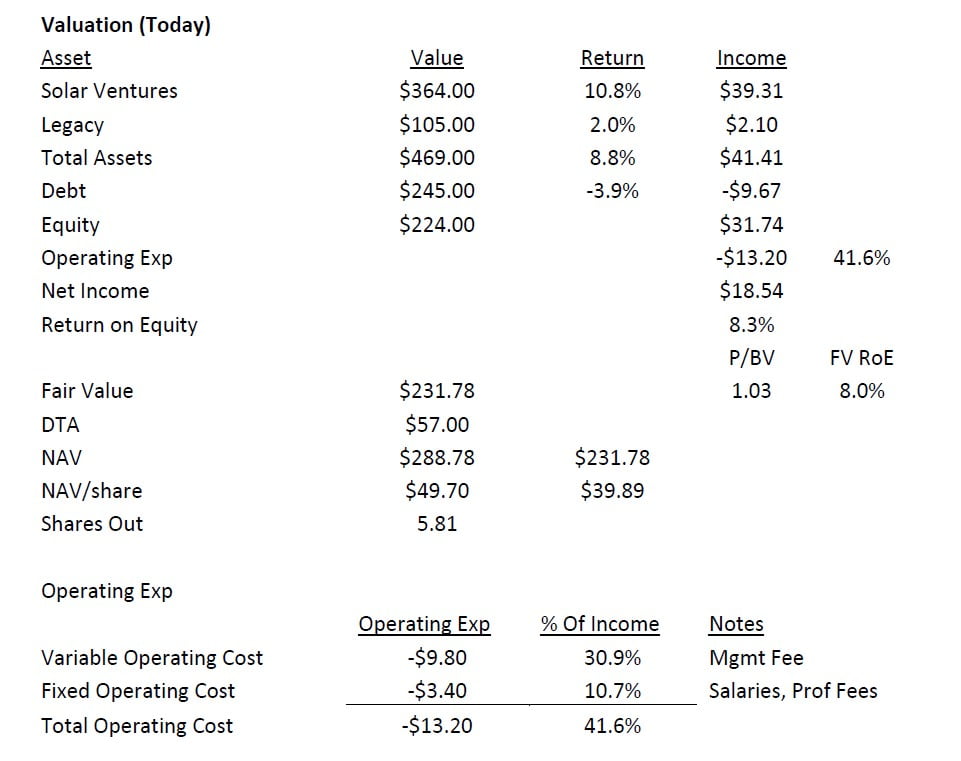

Currently 78% of the portfolio is in solar ventures while 22% is legacy (affordable housing debt and real estate debt and equity). The solar investments are via joint ventures with Fundamental Investors (an investment fund). MMA Capital has an approximately 50% interest in the renewable power loan pools. The solar loans have principal balances of $5 to $20 million, have coupon rates of 7% to 14%, and an average remaining maturity of seven months. The current portfolio has 60 loans with an average loan to value of 50%, an average interest rate of 9.5%, and the fund generates 1% to 3% origination fees. The loans are primarily first-lien loans on the projects. As of June 30, 2020, the funded balance is $758.8 million ($364.4 million MMAC share) with an unfunded balance of $427.5 million ($214.9 million MMAC share). The solar investments have $110 million of debt at the MMAC level and $364 million of equity. MMA Capital has an 81% recurring revenue rate from existing customers. The current pipeline is about $800 million out of $2 billion opportunities reviewed annually. Historically, solar ventures have originated $540 million of loans over the past year and $2.8 billion since inception. MMA Capital directly sources loans with no reliance on brokers. Loans have been underwritten to 10% to 15% annual returns. Actual returns have been 16.7% for all loans originated to date. The current trailing 12-month returns on the portfolio have been 11.8%. The current net interest margin in the solar portfolio is 4.9% (6.9% if fully invested in solar ventures) with an average financing rate for MMA Capital of 3.9%. This margin combination with an efficiency ratio of 41.6% results in a return on equity of 8.3% (11.1% if fully invested in solar ventures).

The solar asset management firm (formerly owned by MMAC) was sold to Hunt in 2018 for $57 million. Hunt had a $365 million asset value in 2018, so the price paid was 15.7% of assets under management (AUM). The proceeds were used by MMA Capital to invest in more solar loans. Hunt is paid a management fee (2.0% of equity and 20% above 7% increase in equity book value) and reimbursements of about 3.5% of equity or 1.9% of assets as of Q2 2020. Current operating expenses as a percentage of net interest income (efficiency ratio) is about 41.6%. If you include the pro-rata operating expenses of solar ventures of $2.4 million per year, then the adjusted efficiency ratio is 45.7%. The efficiency ratio will decline as the portfolio grows and the fixed non-management fee operating expenses stay constant. As a result of the asset management sale, some investors sold MMAC, as they wanted to invest in an asset management firm, not an alternative asset fund.

MMA Capital is the largest competitor in the market of banks and specialty finance funds. Many solar lenders will not provide lending before commercial operations, so MMAC is one of the few financing sources pre-operations. The market growth is based upon the increased amount of installed solar capacity over time. According to the Solar Energy Industries Association (SEIA) and Wood Mackenzie, over the next five years, the amount of installed solar capacity is expected to double (15% annual growth) which will create many more lending opportunities for MMA Capital as the solar energy infrastructure is built out across the US.

Since solar loans represent 78% of total assets and are the future of the business today, the history of the solar loans is shown below:

Historically, MMA Capital has not had enough capital to meet the 50% loan share agreement it has with Fundamental Investors.

The legacy assets include: debt and equity in a mixed-use town center development in Spanish Fort, Alabama; a land development project in Winchester, Virginia; a tax-exempt affordable housing bond for a property in Atlanta, Georgia; and interests in South African housing (a REIT and a housing fund).

Renewable Lending Business

The renewable lending business competitors include financers of solar projects from development to operations. MMA Capital focuses on the pre-construction and construction phases of solar projects. The competitors include large banks and bonds for operational solar projects, and smaller banks and funds for development and construction loans.

Other comparable firms include private debt providers (BDCs) and real estate loan providers (construction bridge loans). See Appendix A.

Downside Protection

The downside protection is the asset value of MMA Capital. The value of MMAC is driven by the cash flow of MMAC’s assets (solar ventures and legacy assets) less interest payments for its debt. MMA Capital has debt of $245 million or 51% of equity book value. None of the 132 solar loans that have been repaid since inception (2015) have incurred a principal loss.

Financial leverage can be measured by the debt/enterprise ratio. MMA Capital debt/enterprise ratio is higher than the low cost comparable firms (see Appendix A), but MMA Capital’s portfolio has better credit metrics than the low cost comparable firms (see Benchmarking in Appendix A) and the stock, in my opinion, is undervalued.

COVID has been a test of the resilience of MMA Capital. The impact thus far has been (1) an impairment on the Spanish Fort, Alabama development, (2) no incremental losses in the solar loan portfolio, (3) the origination levels for the solar loan portfolio have been flat year-on-year, and (4) lower interest rates have increased the fair value of the solar portfolio.

Management and Incentives

MMA Capital is managed by HIM. The asset management agreement pays HIM 2% of equity per year (1.5% on assets) and an incentive fee of 20% above a 7% increase in book value per year. The current efficiency ratio is 41% of net interest income, typical for an alternative asset management fund. Once MMA Capital is fully invested in solar loans, the efficiency ratio will decline to 39.2%. HIM and MMAC management hold about 15% of MMAC’s equity.

Valuation

MMA Capital is valued based upon the income its assets can generate capitalized by a normalized capitalization rate. MMA Capital is comprised of solar assets that are currently generating 10.8% and legacy assets that are generating a 2% return. The cost of the debt has to be subtracted from the income generated by the assets resulting in net interest income. Finally, the operating costs of management fees, salaries, and professional fees are subtracted from net interest income resulting in net investment income (NII). The efficiency ratio is 41.6% which is at the high end of the low-cost alternative asset funds. The current return on equity is 8.3%. One way to value MMA Capital is to estimate a normalized return on equity from comparable funds (see Appendix A). Given MMAC’s low loss ratio, the normalized return on equity should be on the low end of the comparable firm range of 6.8% to 11.9%. The resulting normalized return on equity is 8.0%. Therefore, using the normalized return on equity results in a price-to-book value of 1.03 (8.3%/8.0%). Applying this to MMA Capital’s equity of $224 million results in a low-end value of $231.8 million or $39.89 per share. If you add the deferred tax assets associated with the net operating loss carryforward of $57 million, then the resulting high-end value is $288.8 million or $49.70 per share.

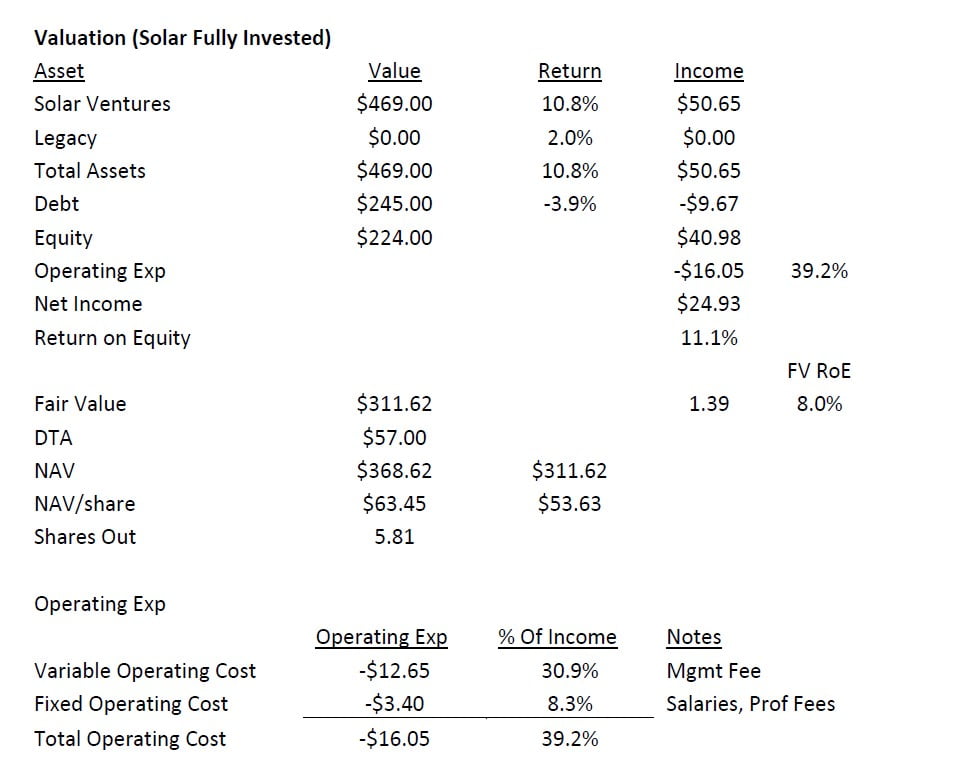

Currently, MMA Capital’s plan is to further replace legacy assets with more solar loans. If the remaining legacy assets are replaced by solar loans, then the income from investments will increase from $41.4 million currently to $50.7 million (see table below).

The cost of the debt has to be subtracted from the income generated by the assets resulting in net interest income of $41.0 million. Finally, the operating costs of management fees, salaries, and professional fees are subtracted from net interest income resulting in NII of $24.9 million. The efficiency ratio is 39.2% (assuming no salary savings) which is on the high end of the range compared to other alternative asset funds at the high end of the low-cost alternative asset funds. The expected return on equity is 11.1%.

Using the normalized return on equity of 8% (derived above) results in a price-to-book value of 1.39 (11.1%/8.0%). Applying this to MMA Capital’s equity of $224 million results in a low-end value of $311.62 million or $53.63 per share. If you add the deferred tax assets associated with the net operating loss carryforward of $57 million. then the resulting high-end value is $368.62 million or $63.45 per share.

Comparables/Benchmarking

In the table in Appendix A are the low-cost BDC and real estate loan funds firms engaged in the asset-backed lending. MMA Capital has a lower NII multiple of 5.9 (w full solar investment) than the comparables’ range of 8.4 to 15.1x and average of 10.7x.

MMA Capital has one of the lowest total loss/year ratios versus the comparables and 100% of the loans are first lien secured loans. While the expense ratio of 41.6%/39.2% is above average for the low-cost comparable firms, it has some downside as overhead is reduced.

Risks

The primary risks are:

- lower than expected return on solar investments;

- a dependence on functional renewable energy financing market; and

- a lack of new investment opportunities (including solar if subsidies are reduced).

Potential Upside/Catalyst

The primary potential catalysts are:

- higher return on solar investments as lending standards reduce competition; and

- other high-return renewable investment opportunities.

Timeline/Investment Horizon

The short-term target is $45.00 per share, which is almost 80% above today’s stock price. If the replacement of legacy assets with solar assets thesis plays out over the next five years, then a value of $58.00 could be realized. This is an 18% IRR over the next five years.