In today’s interconnected world, having a reliable international payment provider that offers a safe payment gateway is no longer a luxury but a necessity for businesses looking to expand their global footprint. A payment gateway is a service that your business needs to accept electronic payments from your customers smoothly and securely wherever they may be.

Payment service providers are the backbone of global commerce, enabling quick and efficient transactions across borders. In this guide, we selected and reviewed the best payment gateways for getting paid internationally to help you find the one that suits the size of your business, the location and payment preferences of your customers. Read on to see our picks.

Top international payment service providers, at a glance

Here are our picks to of the top payment platforms to seamlessly collect payments from around the world:

- Revolut: The UK-based fintech company, founded in 2015, offers a range of payment acceptance options, including card payments, online payments, and in-person payments through card readers. It has a big focus on consumer-oriented features.

- Wallester: The Estonia-based company was founded in 2016. It focuses on the gig economy. It offers a free plan with limited features and paid plans with varying fee structures.

- Airwallex: The fintech company, founded in 2015 in Melbourne, Australia, is now based in Singapore. It’s known for providing financial services and software as a service (SaaS) to businesses. Its focus on cross-border transactions and online payments makes it suitable for businesses with international clients.

- Western Union: Founded in 1851 in Denver, Colorado, Western Union’s business services segment provides payment and foreign exchange services, mainly cross-border and cross-currency transactions for small and medium-sized businesses.

- Clover: The Sunnyvale, California-based fintech is known for its ease of use and the customer loyalty features that are part of its system, such as promotion sharing and up-selling.

- Stripe: With no monthly charge, the San Francisco and Dublin-based fintech is known for its multifunctionality. It has strong global payments support, helping businesses expand into other markets, and innovative currency conversion features.

- Square: The San Francisco-based fintech was an early mover in mobile payments and point of sale transactions for merchants. It was launched in 2009 and is known for its universe of business-friendly apps. It’s free to use but its credit card transaction fees are relatively high.

- OFX: The Sydney-based provider was founded in 1998 as a worldwide payment and foreign exchange servicer for consumer, corporate and internet retailers. It’s expanding its cross-border payment capabilities after purchasing multicurrency account and expense management software provider Paytron last year.

- Wise: The London-based company, founded in 2011, specializes in international money transfers and provides other financial services. In addition to money transfers, Wise offers services such as multi-currency accounts, debit cards, and international business payments.

- PayPal: This US company allows you to make and receive international payments to and from more than 110 countries. It now accepts payments from US users in US dollars converted from PayPal USD (PYUSD), a US dollar-denominated cryptocurrency.

An in-depth look at today’s best payment gateways

Let’s take a more detailed look at each of these platforms and what makes them worth checking out.

1. Revolut: Best low-cost payment platform for small businesses

Revolut is a fintech company that offers a range of financial services, including international money transfers, currency exchange, and banking. While it started as a consumer-focused platform, delivering a prepaid card and app-only overseas payment service, it has expanded to offering tailored tools for businesses, including payments, savings and other investment products.

Revolut has about 9 million customers in the UK and more than 45 million globally. Its business should expand now, when after three years of wrangling, it managed to secure a banking license in the UK. It already had a banking license in the EU from authorities in Lithuania.

Furthermore, its business account offers access to three physical and 200 virtual cards. Your first plastic card is complimentary, and any others you order will incur a delivery fee.

Depending on your plan, you may also be able to order a limited number of complementary metal cards. It has a mobile app that allows you to manage business banking and the business account will sync with third-party accounting tools such as QuickBooks and Sage. Revolut allows users to hold multiple currencies in one account and spend abroad without hefty fees, making it a good choice for travelers and international businesses.

Pros

- User-friendly app

- A big range of features, including crypto trading and budgeting tools

- Low fees and competitive exchange rates

Cons

- Limited customer support

- Subscription fees once you go past the basic account

- Limited deposit protection

2. Wallester: Top payment gateway for secure transfers

Wallester offers a suite of financial tools designed to streamline operations and boost efficiency for small businesses, including business-branded VISA pre-paid and debit cards, and expense management tools that can be customized.

By centralizing expense management, Wallester helps owners maintain tight control over their finances. Its virtual and physical cards provide flexibility for both in-person and online transactions, while robust reporting features offer valuable insights into spending habits. The company has strong security protocols, alerting business owners to irregular asset movements. When you go beyond the basic plan, the price jumps quickly, along with increased features.

Wallester’s integration capabilities allow seamless connection with existing accounting software, saving time and reducing errors. This centralized platform can significantly enhance financial oversight, enabling business owners to make data-driven decisions and identify potential cost-saving opportunities.

Ultimately, Wallester’s user-friendly interface and comprehensive features make it a valuable asset for any small business seeking to optimize its financial management. Wallester platforms are usually made to accommodate business growth, allowing for increased transaction volumes and user management.

Pros

- Good security protections

- Fixed foreign exchange fees

- Transparent costs

Cons

- Clunky desktop interface

- High transaction fees

3. Airwallex: Solid payment processor to grow a business

Airwallex is used by more than 100,000 businesses internationally. It aims to be a one-stop financial solution for businesses operating in multiple markets. It helps businesses make international transfers at interbank rates to more than 150 countries, while accepting more than 160 local payment methods, including Klarna, Apple Pay, Google Pay, Visa, and Mastercard. One of its key features is its Multi-Currency Wallet, which holds up to 23 currencies, making global sales easier.

Airwallex differentiates itself by providing a suite of solutions, including payments, currency exchange, virtual and physical cards, and embedded finance capabilities. This holistic approach allows businesses to manage their financial operations more efficiently and effectively on a global scale.

The company has been active in forming partnerships to improve its payment systems. It just paired with Canadian B2B company Float, which will use Airwallex’s Bill Pay product for bank transfers, EFT, wire and ACH payments as part of its business finance platform. Some of Airwallex’s other recent partnerships include a deal with WooCommerce, an open-source ecommerce platform for WordPress, to enable its merchants to accept crossborder payments using global cards, Google Pay, Apple Pay and other local payment methods. It also paired with Singapore-based health technology company Jebhealth and Visa to introduce payment cards for corporate health and employee benefits.

Pros

- One-stop service to manage global payments and finances

- Good web interface and software tools

Cons

- Needs better transparency on fees

- Below-average customer service

4. Western Union: Best online payment services company for an international presence

Businesses of all sizes can send and receive international payments around the clock with Western Union Business Solutions. WUBS provides risk management services while allowing businesses to make payments and receive payments almost anywhere in the world. The stability and high recognition factor of Western Union make it a strong choice for many businesses, despite higher fees in some cases.

Western Union can enable a business to send or receive payments across more than 200 countries and in more than 130 currencies. It’s known for consumer-to-consumer money transfers, but offers global payroll services to businesses, in addition to a platform to send and receive payments in various currencies.

It is particularly useful in cash-based businesses, such as restaurants or retail stores. Its offices are ubiquitous internationally, and its platform to send and receive payments can streamline transactions. It also has a free international platform, WU Edge, where you can find business partners, make global payments and manage international transfers, as well as a streamlined platform, Online FX, which allows businesses to send outgoing payments and transfers from a mobile phone or computer, 24/7.

Western Union offers the potential for partnership programs for financial institutions, retailers, and other businesses. This can involve providing money transfer services under the partner’s brand or integrating Western Union’s technology into existing platforms.

Pros

- Well-recognized international name

- Dependable customer service

- Good platform for recurring payments

Cons

- Only bank-to-bank transfers

- No domestic payments to and from same country

- Limited deposit protection

5. Clover: Customizable payment gateway for business

Clover is owned by payments and financial technology provider Fitserv. It’s primarily known as a point-of-sale system for small businesses to take payments in person. Moreover, Clover works well with third-party apps such as QuickBooks,Time Clock, Yelp and other processes, allowing you to improve its functionality.

It isn’t really designed much for international business, though. While Clover offers online ordering, its e-commerce features are not as extensive as other platforms. That said, where it shines is its ability to tailor to specific business needs. Whether you need inventory management, employee scheduling, or customer loyalty programs, Clover can be configured to meet your requirements.

Clover’s app market provides a wide range of business tools to help in marketing, finance and other operations.

To sum up, if you need to make or receive international payments, the best choice on Clover is its Multi-Currency Payment Acceptance account, which uses dynamic currency conversion in all major credit and debit cards. Clover’s transaction fees vary depending on which plan a business subscribes to, with the more expensive plans offering businesses lower transaction fees.

Pros

- Competitive price for POS

- Good customer service

Cons

- Many promotions require long-term contracts

- Some popular accounting integrations only available through third-party apps

6. Stripe: Solid choice for international e-commerce

Stripe has become a favorite of e-commerce companies, due to the ability to customize its solutions for business and its adaptability to a large number of currencies. The payment platform was founded in 2010 by John and Patrick Colllison and has become popular, particularly with small businesses. Another advantage is that it t delivers a good array of merchant services, from reporting tools, fast payouts and fraud prevention services.

Its Radar platform utilizes Stripe’s reach of the 197 countries its processes payments in. The provider claims that even if a credit card may be new to your business, there’s a 91% chance the Stripe network has seen the card before. Stripe uses its partnerships with Visa, Mastercard, American Express, and leading banks to obtain data such as TC40s, SAFE reports, and early dispute notifications to help identify fraudulent charges before they’re disputed.

Stripe has been busy building its business through acquisitions. It just purchased Lemon Squeezy, a merchant of record that calculates and pays global sales tax for digital products, handling legal processing and fees across the globe. It mainly serves Software as a Service and software businesses. In March, Stripe acquired the four-person team of Supaglue. That company, formerly known as Supergrain, specialized in open-source developer platforms for user-facing integrations.

Pros

- Good advanced development tools for online checkouts

- Transparent, flat-rate pricing

- Handles a wide range of currencies

Cons

- Not easily customizable for small businesses

- Difficult integration with other payment platforms

7. Square: Payment provider beefs up security protection

Square is known for its point-of-sale (POS) options. It has a small card reader that can be used by a cell phone, all the way to a large register with double touchscreens. The payment service provider is good for international transactions because it facilitates the ability for a business to accept payments nearly anywhere in the world. It features a pay-as-you-go-model of 2.9% + $0.30 per transaction, with no monthly fees or currency conversion fees for merchants.

One of Stripe’s advantages is that the company’s low starting costs make it a good choice for startup businesses or smaller businesses. Its plans start out at $0 for monthly fees, including a Square Reader for Magstripes. Additionally, we think that for merchants whose transactions vary quite a bit from month to month, it can be a good fit, because you only pay processing charges for what you earn.

However, the downside to Square is it doesn’t accept as many credit cards for payment as some other payment platforms. Square does allow users to set up an e-commerce website for free without knowing any code. If you pay an additional $12 a month, you can add a custom domain. If you already have a website, you can use Square’s Online Checkout to take payments. It gets high grades for fraud protection, providing alerts on suspicious transactions through algorithmic automation and human observation.

Pros

- Easy setup with no additional costs

- Great for in-person sales

Cons

- Limited credit cards to take paments

- Limited customer service

8. OFX: Specialized payment provider for companies looking to save

From importing goods to paying overseas suppliers or employees, managing foreign exchange can be complex and costly. This is where OFX can shine. OFX often positions itself as a more specialized solution for businesses, emphasizing personalized service and tailored solutions. It offers online seller accounts specifically for businesses selling on marketplaces and is a member of Amazon’s Payment Services Provider Program.

While it doesn’t have all of the business apps that some other platforms do, OFX specializes in streamlining international money transfers and providing competitive exchange rates. By leveraging that expertise, businesses can significantly reduce the costs associated with cross-border payments. Their platform is designed to be user-friendly, allowing businesses to easily manage their foreign exchange needs from a single dashboard.

OFX has a strong international reach, as it allows transfers in more than 55 currencies and to more than 190 countries, with no limits on how much or how often money can be sent. It may not be the best for small businesses, though, as it has a $1,000 transfer minimum and a relatively high markup on exchange rates. It also allows only bank transfers, instead of allowing transfers by bank draft, cash or credit card.

Pros

- User-friendly app

- Good for companies with remote workers

Cons

- Limited customer support

- Fee of $11 if you transfer less than $10,000

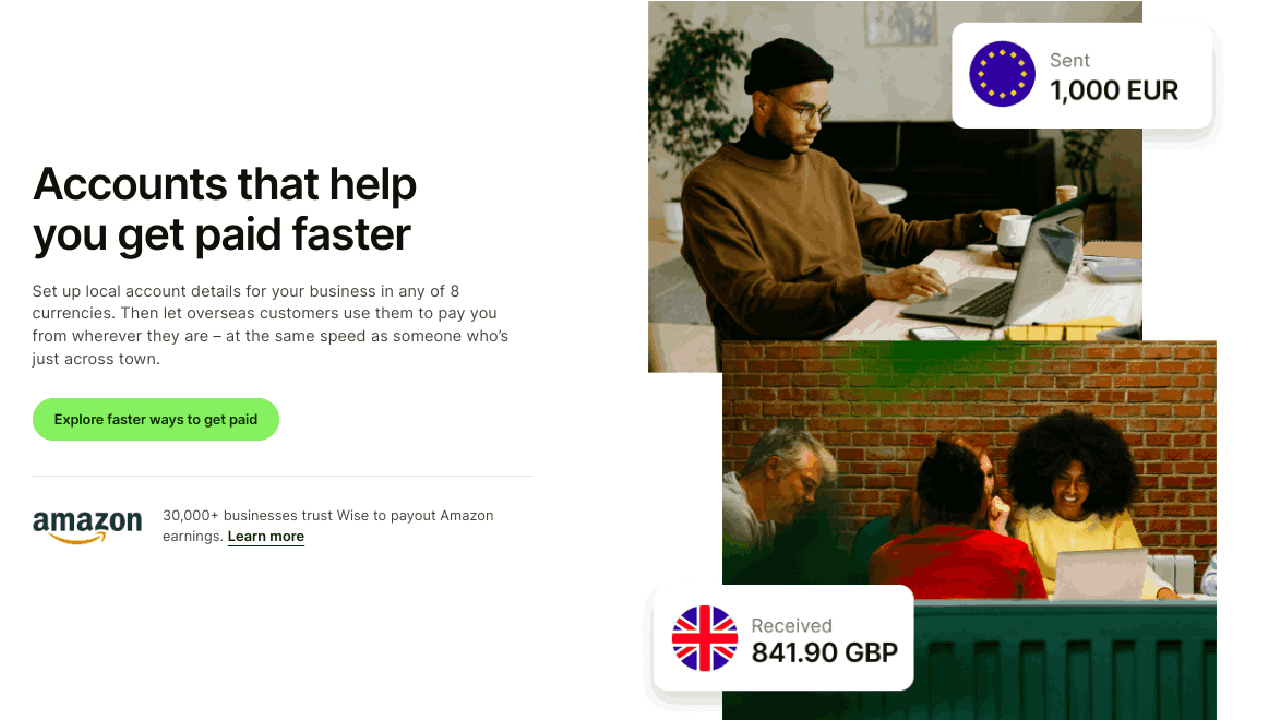

9. Wise: Payment platform prides itself on fast, dependable service

Wise works with more than 85 different payment platforms and the big advantage for the service is its speed, with 62% of end-to-end payments arriving within 20 seconds. Once you sign up with Wise, you can hold more than 40 different currencies in your account, enabling you to convert them at the mid-market exchange rate.

Wise accounts come with localized bank account numbers across multiple jurisdictions. It is a good platform for businesses that do frequent transactions in more than one country and a good alternative to having multiple foreign bank accounts.

The company said it processes more than £9 billion in international money transfers every month. It handles more than 40 currencies and can send payment to more than 160 countries. In fiscal 2024, it grew active customers by 29% to 12.8 million, according to its earnings report.

While it doesn’t markup currency exchange fees, the downside for Wise is its fees can quickly add up. The costs for using bank transfers or multi-currency account transfers start at 0.4% of the total transfers and debit card and credit card money transfer costs range from 3% to 4%.

Pros

- Good customer service

- Works in a wide range of countries

Cons

- Transfer fees can be expensive

- Fees for holding higher value balances

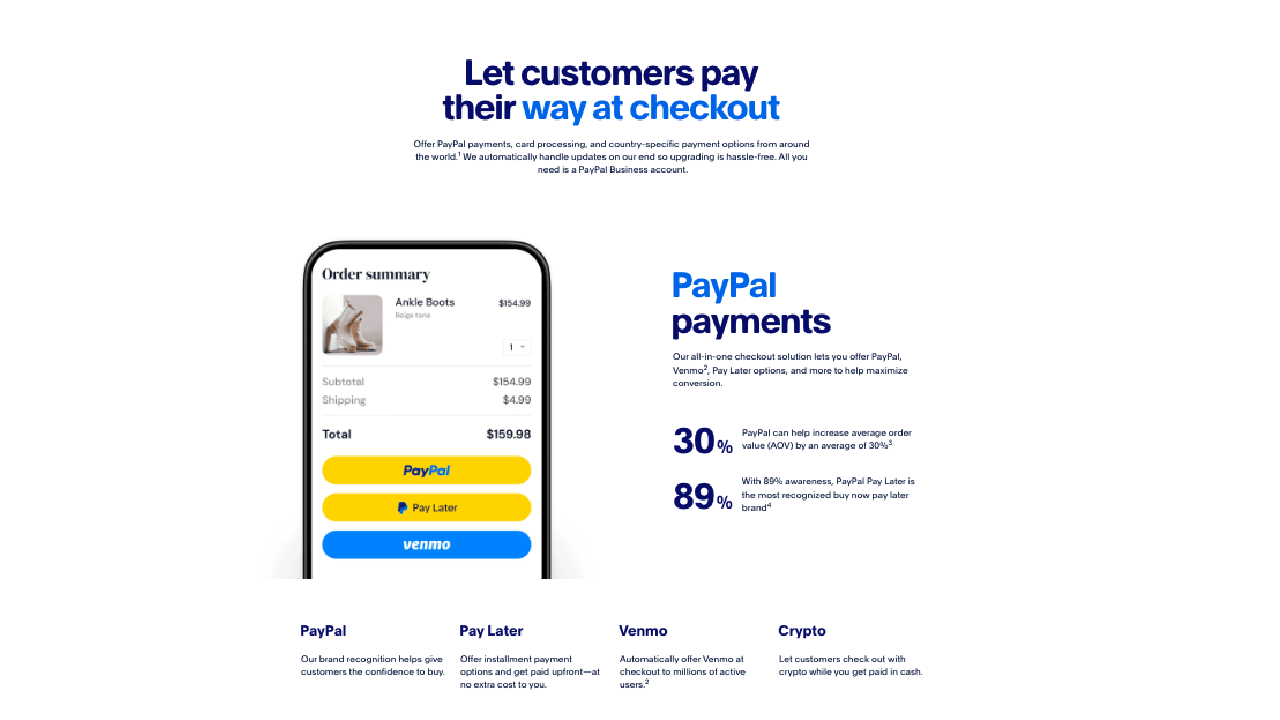

10. PayPal: Move to allow crypto payments could be a game-changer

PayPal is accepted in more than 200 countries and regions, so it already has a strong international presence. It supports multiple currencies and automatically does the conversion rate for businesses when conducting international business.

It doesn’t have a monthly fee, so that’s a big edge for small businesses. However, its transaction fees add up and are higher than some payment systems. It has been doing this a while and because of that, has above-average security features. PayPal allows you to send payments to multiple recipients at once, which is helpful for payroll or refunds.

By leveraging PayPal’s features and global reach, businesses can expand their customer base, streamline operations, and mitigate risks associated with international commerce.

One big edge is its funding option allows users in the US to convert the stablecoins in their linked PayPal Cryptocurrency Hub to US dollars to fund transactions to recipients in approximately 160 countries with no transaction fees.

Pros

- It can transfer and receive funds relatively quickly

- Versatile payment solutions

- Above-average security measures

Cons

- Not efficient for high-volume businesses

- High fees for currency conversions

How do these payment gateways stack up?

| Platform | Has a free plan | Transaction fees | Instant deposits | Trustpilot score |

| Revolut | Basic plan is free | Begin at 1% | Yes | 4.1 |

| Wallester | Basic plan is free | Begin at 2% | Yes | 4.4 |

| Airwallex | Has a free basic plan | Payment acceptance fee beginning at 1.30% and + £0.20 | No | 3.6 |

| Western Union | Businesses can sign up for free | Begin at $0.99 per transaction | Yes | 4.2 |

| Clover | $0 for CloverGo POS platform | Begin at 2.6% plus 10 US cents per transaction | Yes | 3.4 |

| Stripe | Free to join | Begin at 2.9% plus 30 cents per transaction, though high-volume businesses pay less | Yes | 2.3 |

| Square | Free to join | Begin at 2.6% plus 10 cents per transaction | Yes | 4.1 |

| OFX | Free to join | None | No | 4.4 |

| Wise | Free to join | None | Yes | 4.3 |

| PayPal | Free to join if you belong to PayPal | Begin at 2.9% | Yes | 1.3 |

Who needs a payment gateway?

Any business that conducts transactions with customers electronically in their home market or in different countries will require a payment gateway.

This is especially true of online retailers that need to accept various currencies and payment methods, service-based businesses that cross borders and import-exporters.

Some of the payment providers in this guide offer a broad range of services to businesses not exclusively ones related to payments and electronic transactions. These include point-of-sale services, such a accepting credit cards or mobile payments, payroll, accounting services and expense management all in one place.

Payment gateway, payment service provider, payment processor — What is the difference?

The world of international payment technologies is often confusing. The terms payment gateway and payment processor and payment provider tend to be used as synonyms. While they are related, they refer to different phases in collecting online payments.

The best way to imagine a payment gateway is that it is the checkout counter of an online merchant. The payment gateway links all the parts of the international payment ecosystem that need to work together to authorize the transaction. When a customer wants to make a payment, it transmits the encrypted payment information safely through the network.

A payment processor is the engine behind the transaction and it communicates with the customer’s and the seller’s banks to move the money between the two and complete the payment.

A payment provider, such as PayPal includes a whole payment infrastructure, which often encompasses both a payment gateway and a payment processor, and much much more.

Businesses need a payment gateway to accept online payments, and individuals don’t. There is a multitude of ways in which a person can send money to another person overseas, even just with an email address. Of course, the system of electronic payments swings into motion to safely carry out those transactions.

How to choose the right payment gateway for getting paid internationally

Depending on what kind of business you are involved in, there are multiple factors you will want to examine before signing up for a specific platform.

- Transaction fees: Compare processing fees, monthly fees, and other charges.

- Payment methods: Ensure the app supports the payment methods your customers prefer (credit cards, debit cards, digital wallets, etc.).

- Hardware compatibility: If you need physical payment terminals, check compatibility with your devices.

- Additional features: Consider if you need features like invoicing, inventory management, or employee management.

- Customer support: Evaluate the quality and availability of customer support.

Our methodology – How we ranked the top international payment gateways

One of the primary ways we ranked these payment processing providers was how expensive it was to use their service, including whether there was a monthly charge, in addition to any transaction fees.

Apart from that, we looked at the ability of each to send and receive payments from as many countries and as many currencies as possible. It was also important to analyze how intuitive each payment processor’s website was and whether its services were customizable.