Dear fellow investors,

Jessie Livermore was one of the greatest investors of all time. In the book, Reminiscences of a Stock Operator, Livermore explained that the single activity that made him the most money was, “sitting on my hands.” In other words, the willingness to leave your portfolio of companies in place longer than your competitors was one thing which made him rich. This tells us much about where the tortoise can find investment opportunities today.

1. Asset allocation is in disarray

Source: The Wall Street Journal

Q3 hedge fund letters, conference, scoops etc

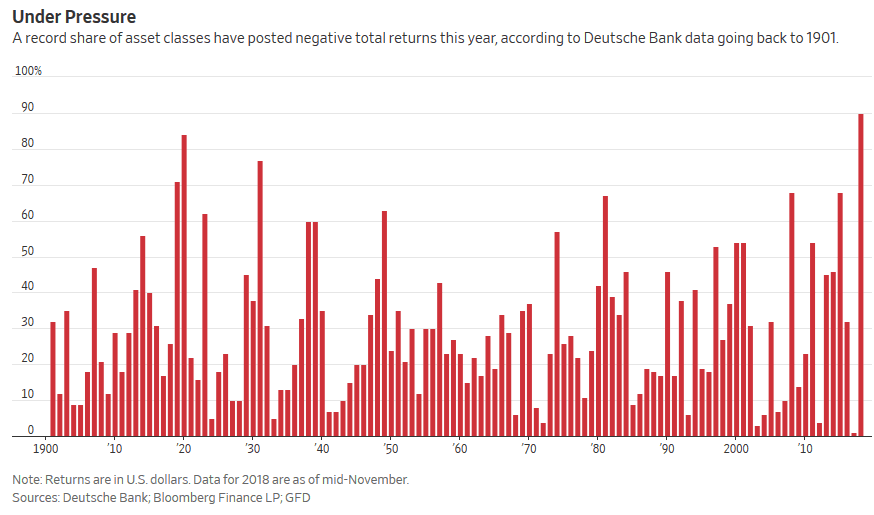

Through mid-November of this year, the largest number of asset classes had negative returns. In other words, almost nothing has worked in asset allocation this year and frankly, not too many stock sectors besides FAANG stocks have worked for the last five years in the U.S.1 The hares have run way out ahead of almost every asset class regardless of any tortoise-like qualities they might have had. The momentum people were racing out front in 2008 and 2011 by being in love with China, emerging markets, oil, industrial commodities and farm commodities. Those hares are like Joe DiMaggio in the song, Mrs. Robinson, “Where have you gone?”

This harkens us back to 2012, when we wrote a piece called, “Stock Pickers: Somebody I Used to Know!” Back then, David Swenson from Yale’s endowment, Jeremy Grantham from GMO and other early asset allocation adopters were at the pinnacle of their success. Most of the largest endowments are reorganizing around a different approach, because of dismal lookback returns since then. When investors get concentrated in one sector of investing, whether it be tech stocks, oil stocks, gold and commodities, it is usually a good time to spread your bets and add to the sectors which are the most out of favor. We are not asset allocators outside of large-cap U.S., but asset allocation is probably a tortoise and due for a comeback.

2. Value is screaming for dollars

Source: Fundstrat, August 29, 2018.

If this isn’t the easiest mean reversion trade since 2000, we’d like someone to show us the one which is better. The sector, U.S. large value, is the most out of favor in relation to large growth as it has been since 2000 and that was the biggest extreme of my 38 years in the investment business. We believe growth is an over-cooked goose and by three years from now, nobody will want to eat goose. Nothing mimics the hare from the fable better than investor enthusiasm for something new and pioneering. The problem for the “new and pioneering” is once everyone buys into it, it is part of a financial euphoria episode. John Kenneth Galbraith would say, “Circle the Wagons.”

3. Don’t chase rabbits

While attempting to get to their investment goals quickly, we see many investors make mistakes similar to the rabbits. If you want to see this playing out in real time, consider housing. We read the news, we listen to the shows, and what they’re telling us defies the moral of the story.

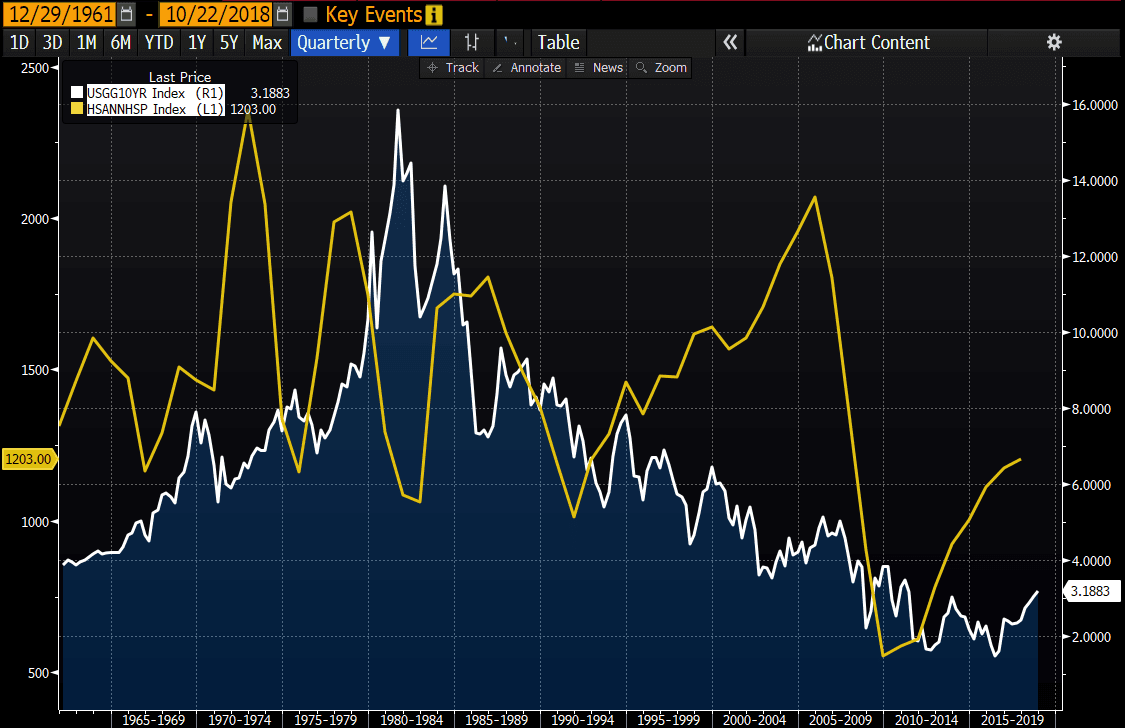

At Smead Capital Management, our tortoise shell is strong, and we rarely forget the thesis. The chart below shows U.S. housing starts in yellow and ten-year Treasury Bond interest rates in white. The U.S. population in 1960 was around 175 million and today it is somewhere around 325 million. There is no correlation between interest rates and home building. There is a correlation between household formation, child bearing and home building. Adjusted for population, today’s home building statistics are off the charts low!

Source: Bloomberg. Data for the period 12/29/1961 – 10/22/2018.

In 2012, we bought shares of Bank of America (BAC), JPMorgan Chase (JPM) and NVR Inc. (NVR) to get at what we thought would be a 15-year recovery in housing in the U.S. The largest banks owned millions of foreclosed homes and would benefit greatly from a rebound in those home prices. NVR was (and still is) the fifth largest, and by far the most profitable of the nation’s publicly-traded home builders. The common shares of these three companies have soared in value over the last six years but have run into a very normal correction in the last twelve months. Corrections like these in a secular recovery like this are designed to shake all the hares out of these stocks and has hurt momentum investors who were late to the party.

The media is pounding on this correction like it is the end of housing life as we know it, rather than as a normal part of a long-term, secularly-favorable trend. Many people who live in the most expensive housing markets are like spoiled children, if it’s not going well for them, they don’t want it to go well for anybody else. Someone once said, “don’t get into a public fight with someone who has an unlimited supply of ink.” We relish how lonely it is today to be a housing bull and an investment tortoise, because we like to say, Only the Lonely Can Play!

4. Be greedy when others are fearful and fearful when others are greedy!

The tortoise is famous for owning stocks with low price-to-earnings ratios and patiently waiting for them to come back into favor. Maximum pessimism was what John Templeton always looked for. Can traditional retailing get any more out of favor? Target (TGT) and Nordstrom (JWN) are superior merchandisers and have as loyal a clientele as anyone on the planet. Whenever the Millennials (and every generation before them) get over themselves (usually when they have kids), we believe they will start to get package fatigue and disingenuous company fatigue. They will also recognize that we all need something to do.

Television is being greatly underestimated as well. When somebody actually regulates the internet, the experts could find that TV is much more engaging and is much stickier for advertising than the ads are online. Someone who can only afford $30 per month for TV viewing IS A LOUSY PERSON TO ADVERTISE TO ANYWAY! We have spent so much time the last ten years wallowing in the post-financial crisis/80-million single twenty-something year-old world, we can’t even think straight. Television is the domain of affluent 30-45-year-old families with two to four kids. Like Willie Sutton said about banks, “that is where the money is!”

5. It is time in the market, not market timing, that matters

Our decades of experience in the U.S. stock market have shown us there are two phases in stocks. There is the phase where you wait patiently to get rewarded by owning stocks. There is the second phase where you patiently hold on while you get rewarded for owning stocks. Unless I’ve missed something, the two requirements of each phase are ownership and patience. How did this ever get confused?

You might notice that the stock market has been range-bound in 2018. Every time markets get range-bound, technical analysis suddenly becomes extremely popular. It is all you see on the stock market channels. Let me tell everyone a secret. A great company whose stock price falls forty percent is likely going to provide much more in returns the next ten years than if it hadn’t declined in price. In every other facet of commerce, lower prices are considered a good thing. When stocks fall sharply, and professionals get nervous, the urge is to try to predict short-term swings. We call it embarrassment defense. What a stock price does in the short run doesn’t matter in ten years. How well the underlying company does and how attractively you bought that tortoise determines the long-run returns.

Like the tortoise, we will keep moving toward our portfolio return goals using our eight criteria for stock selection. We will resist the frantic pace of hare-bound investors who try to shorten the holding periods through momentum investing or technical analysis. Lastly, we will stick to our discipline in both phases of the stock market.

Warm regards,

William Smead

1FAANG stocks include Facebook (FB), Apple (AAPL), Amazon (AMZN), Netflix (NFLX) and Google parent Alphabet (GOOGL).

The information contained in this missive represents Smead Capital Management's opinions and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2018 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.