Stanphyl Capital commentary for the month of December 2020, discussing their porfolio holdings and that the stocks are very expensive.

Q3 2020 hedge fund letters, conferences and more

Friends and Fellow Investors:

For November 2020 the fund was up 6.2% net of all fees and expenses. By way of comparison, the S&P 500 was up 10.9% while the Russell 2000 was up 18.4%. Year-to-date 2020 the fund is down 12.7% while the S&P 500 is up 14.0% and the Russell 2000 is up 10.4%. Since inception on June 1, 2011 the fund is up 34.3% net while the S&P 500 is up 227.8% and the Russell 2000 is up 144.8%. Since inception the fund has compounded at 3.2% net annually vs 13.3% for the S&P 500 and 9.9% for the Russell 2000. (The S&P and Russell performances are based on their “Total Returns” indices which include reinvested dividends. The fund’s performance results are approximate; investors will receive exact figures from the outside administrator within a week or two. Please note that individual partners’ returns will vary in accordance with their high-water marks.)

Although we were up decently in November I found the month to be extremely disappointing, as without our short positions the fund would have been up more than twice as much. Zero Hedge recently calculated that central banks are adding liquidity at the rate of $1.2 billion every hour with a lot more to come, and fighting that (as a friend once said) is like playing poker against a guy with a chipmaking machine in his lap—whatever bet you make, he calls. Thus, until we get some PE multiple-crushing/bubble-popping inflation (likely sometime next year when enough people are vaccinated and the velocity of all the newly printed M2 can accelerate), any near-term stock market corrections (for which we’re currently well overdue) may be short-lived. Therefore, during Thanksgiving week I significantly reduced the size of our QQQ short position, and until we get the aforementioned post-vaccination inflation I’ll likely keep it reduced, as being very short (other than strategically around specific events) is currently just pissing in the wind against this monetarily rigged market.

Stocks Are Expensive

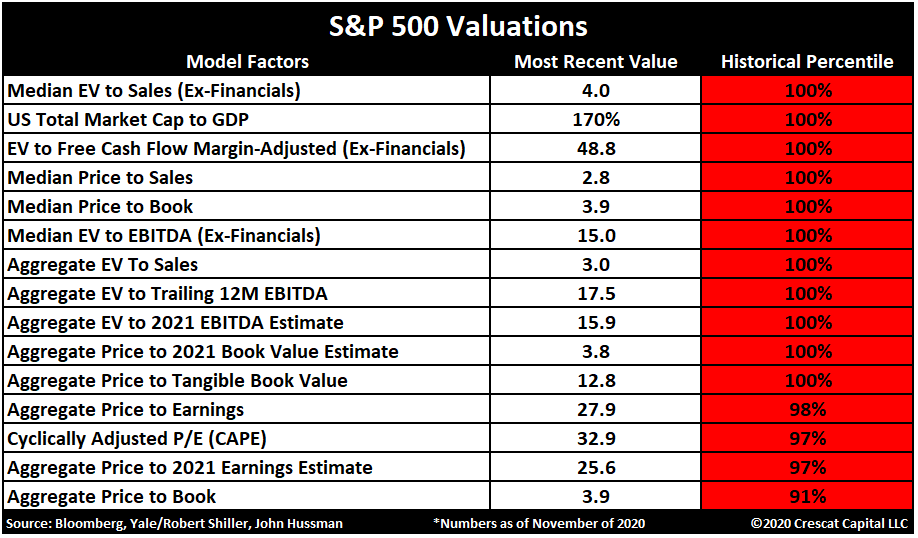

While it’s great news that we now have several COVID vaccines that work, the “forgotten news” is that - generally speaking - stocks are very expensive even based on peak (2019) earnings to which they likely won't return until at least 2022, while the S&P 500’s price-to-sales ratio is literally off-the charts:

In fact, here’s an entire table of astounding valuation data, courtesy of Twitter user @TaviCosta:

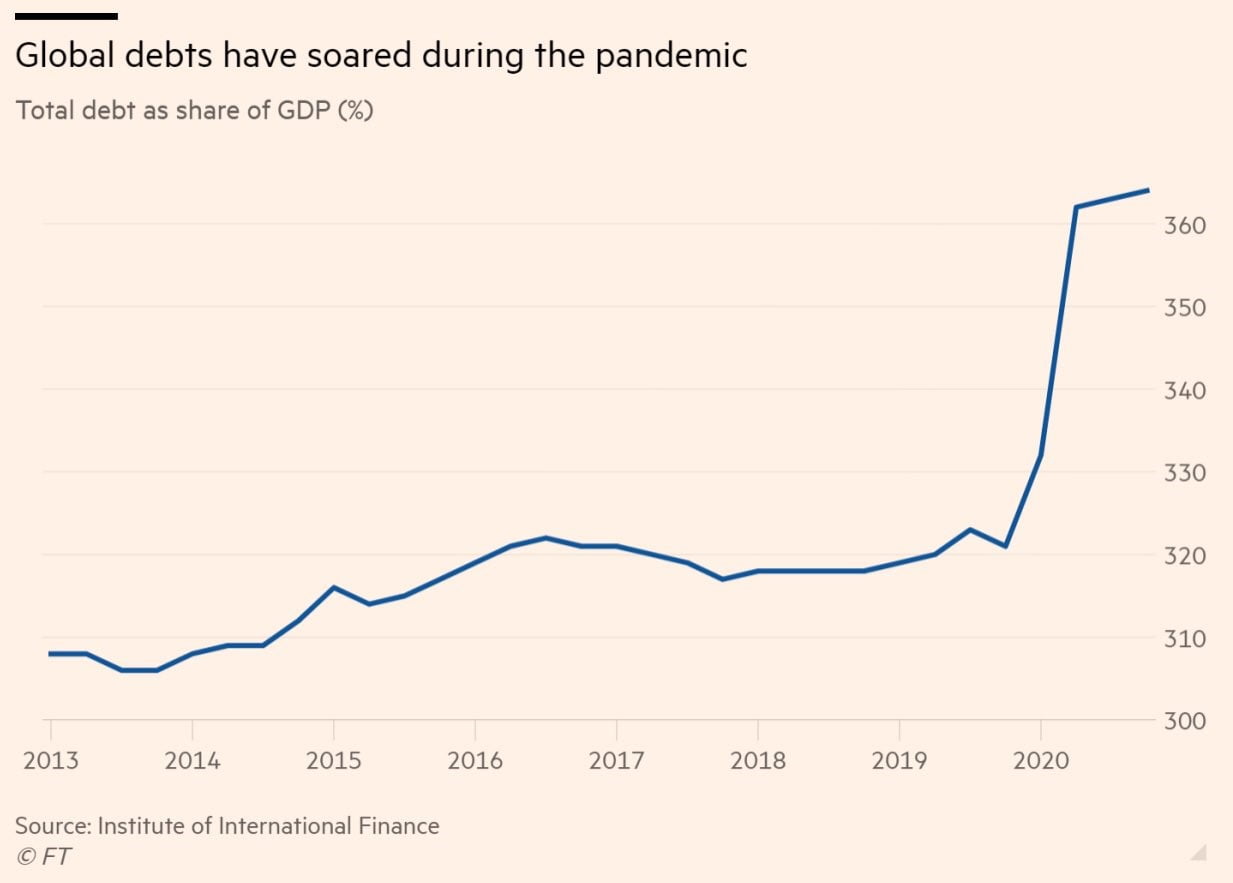

In other words, it's not as if stocks "washed out" with the economy, so how much more can they move once the economy recovers? And oh, when the economy does recover, here’s the insane amount of debt it faces:

Inflating The Central Banks

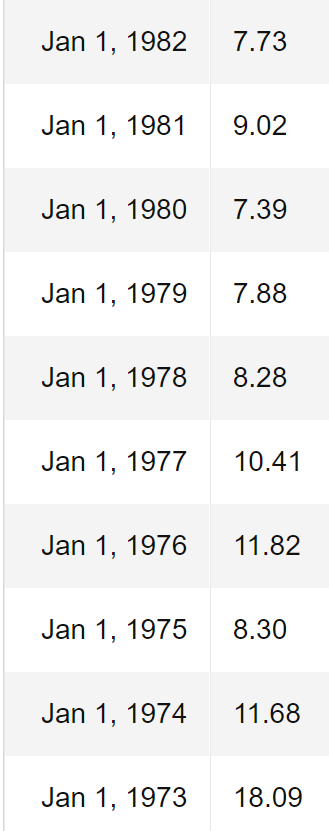

The only way that debt will be handled is by central banks inflating it away, and as governments crank up their fiscal spending that inflation will come. Thus, although while COVID currently rages markets have a “disinflationary chasm” to cross (assuming stimulus spending remains muted by a Republican Senate), eventually post-COVID deficit spending combined with the massive debt overhang will return us to an environment similar to the stagflationary 1970s; i.e., slow growth and increasing inflation, and when that happens high-flying stocks (such as the 38x TTM GAAP PE ratio NASDAQ 100 that we’re short via QQQ) and the 41x TTM GAAP PE ratio S&P 500 will suffer massive PE multiple compression and gold (which we’re long) should do extremely well. Have a look at what happened to S&P 500 PE ratios beginning in 1974 when inflation took off:

As I don’t expect near-term inflation to hit the double-digits of the 1970s, I don’t expect we’ll see similar single-digit index PEs, but even a cut from 38x to 20x would mean a massive drop in stock prices, despite inflation making the “E” nominally higher.

Portfolio Holdings

Here then are the fund’s current positions, beginning with the longs; please note that we may add to or reduce position sizes as stocks approach or recede from our target prices…

Aviat Networks

We continue to own Aviat Networks, Inc. (ticker: AVNW), a designer and manufacturer of point-to-point microwave systems for telecom companies, which has recently been a very big winner for us. (We booked some of those profits on the way up.) In November Aviat reported a fantastic Q1 for FY 2021, with revenue up 13.1% vs. the year-ago quarter and both earnings and EBITDA up hugely, with management guiding to meaningful growth on both the top and bottom lines for all of FY 2021 (which began in July). 10x $20 million in adjusted EBITDA (the midpoint of this year’s guidance) + $36 million in net cash + a $30 million valuation on over $600 million in domestic & international NOL carryforwards would make AVNW a $48 stock. Alternatively, last January the company’s board (controlled by activist investor Warren Lichtenstein) appointed the current CEO and the accompanying press release made it quite clear (based on his experience) that he was brought in to dress up Aviat and get it sold. Aviat’s closest pure-play competitor Ceragon (CRNT) sells at an EV of approximately 0.75x revenue. If we assume $250 million in annual revenue (the midpoint of guidance) for Aviat, $36 million of net cash and a heavily discounted (due to change in control limitations) $10 million valuation on the NOLs, we get an acquisition valuation of 0.75 x $250 million = $188 million + $36 million net cash + $10 million for the NOLs = $234 million divided by 5.5 million shares = $42.50/share. A 20% “control premium” on that would put the price at $51.

Data I/O Corporation

We continue to own Data I/O Corporation (DAIO), a manufacturer of semiconductor programming devices, which in October reported a solid Q3 2020, with revenue of $5.9 million, up 55% (!) from the cyclically low year-ago quarter and 25% (!) sequentially, with a 55% gross margin, a GAAP loss of less than $200,000 excluding a one-time Chinese dividend withholding tax and a foreign currency transaction loss, and $13 million in cash with no debt. This company is a great play on the increasing electronic content in cars—particularly hybrids and EVs—and a great buy-out target. An EV of 2x $30 million in average annual revenue would put the stock at around $8.70/share.

Evolving Systems

We continue to own Evolving Systems, Inc. (EVOL), a small telecom services marketing company that in November reported an excellent Q3, with revenue up 8% sequentially and almost 11% year-over-year. This is a 68% gross margin software company that at an EV of 2x $27 million in run-rate revenue would sell for over $4.50/share. Alternatively, EVOL now generates around $2 million/year in free cash flow and would make a great buy for a strategic acquirer, as $1 million/year in savings from eliminating the cost of being a standalone public company would raise FCF to around $3 million/year. Thus, at an acquisition price of 15x post-merger FCF, a buyer would be paying around $4/share on an EV basis.

Communications Systems

We continue to own Communications Systems, Inc. (ticker: JCS), an IOT (“Internet of Things”) and internet connectivity & services company, which in October reported Q3 revenue up a very nice 26% from COVID-affected Q2, albeit still down 11% from Q3 2019 (a quarter that was juiced by an extremely large one-time contract). Impressively, JCS shifted from recent large losses to a slight net profit, while gross margin was a very decent 43%. With $21 million of cash and no debt, an enterprise value of 1x run-rate revenue for JCS would value it at over $7/share; the only reason I don’t own more is that management is acquisition-minded, which I read as “potentially blowing a beautiful balance sheet on something stupid.”

As central banks increase their money-printing to ever higher levels in order to fund multi-trillion-dollar annual deficits, we continue to hold a substantial long position in the gold ETF (GLD) and a much smaller position in the silver ETF (SLV); the likelihood of post-COVID negative real interest rates for years to come adds a substantial tailwind to these positions, while silver is also a major component in the solar cells the Biden administration is expected to heavily subsidize.

Amtech Systems

In November I sold our position in Amtech Systems, Inc. (ASYS) when it reported a lousy FY 2020 Q4 and disappointing guidance.