Kerrisdale Capital is short shares of Tattooed Chef Inc (NASDAQ:TTCF).

Q3 2020 hedge fund letters, conferences and more

Tattooed Chef Inc (TTCF): Recent SPAC Acquisition is Already Past its Sell-By Date

We are short shares of Tattooed Chef, a $1.2bn packaged-food company that trades at about 7.5x 2020 revenues despite extreme customer concentration and flagging retail sales. Having recently gone public through acquisition by Forum Merger II Corporation, a special purpose acquisition company (SPAC), financial details regarding Tattooed Chef’s business are sparse. Investors have nonetheless bestowed a fanciful valuation on the company based on the torrid year-over-year growth rate of its namesake brand over the last few quarters, and the rosy projections made by management for 2021.

But in-depth interviews with the brand’s largest customers and a thorough analysis of scanner data from Nielsen paint an ominous picture. Tattooed Chef’s rapid revenue growth isn’t a reflection of broad-based sales growth but an artifact of the company’s relationship with a single customer – Sam’s Club, which accounts for about 70% of branded revenue. In a bid to try and “beat Costco at its own game” and foster a “treasure-hunt-type” shopper experience, Sam’s Club began stocking its frozen-food section with some Tattooed Chef prepared meals in late 2018. The initial success led to growing volumes at Sam’s in 2019 and 2020, with pandemic-driven consumer purchasing patterns greatly benefiting the frozen food category in the current year.

Though successful, Tattooed Chef’s unusual approach of launching with Sam’s Club leaves the company ill-prepared to expand elsewhere. Sam’s buyers are adamant about offering Tattooed Chef products that can only be found in club stores, which paradoxically means that successful products sold at Sam’s will be extremely difficult to leverage elsewhere. That only partly explains Tattooed Chef’s absence from the grocery channel. Another snag is that despite constant references to “innovation,” Tattooed Chef’s business with Sam’s is concentrated in just a few items, while its oft-cited relationship with Costco consists almost entirely of private label frozen vegetables. The dearth of creativity will make it impossible to displace hot brands like Caulipower or Daiya in grocers’ freezers. Finally, the relative lack of operational complexity involved in mainly selling a few SKUs to every-day low-price retailers leaves Tattooed Chef woefully unprepared for managing the intricate details of merchandising, distribution, and product assortment that are required for success in the much larger grocery channel.

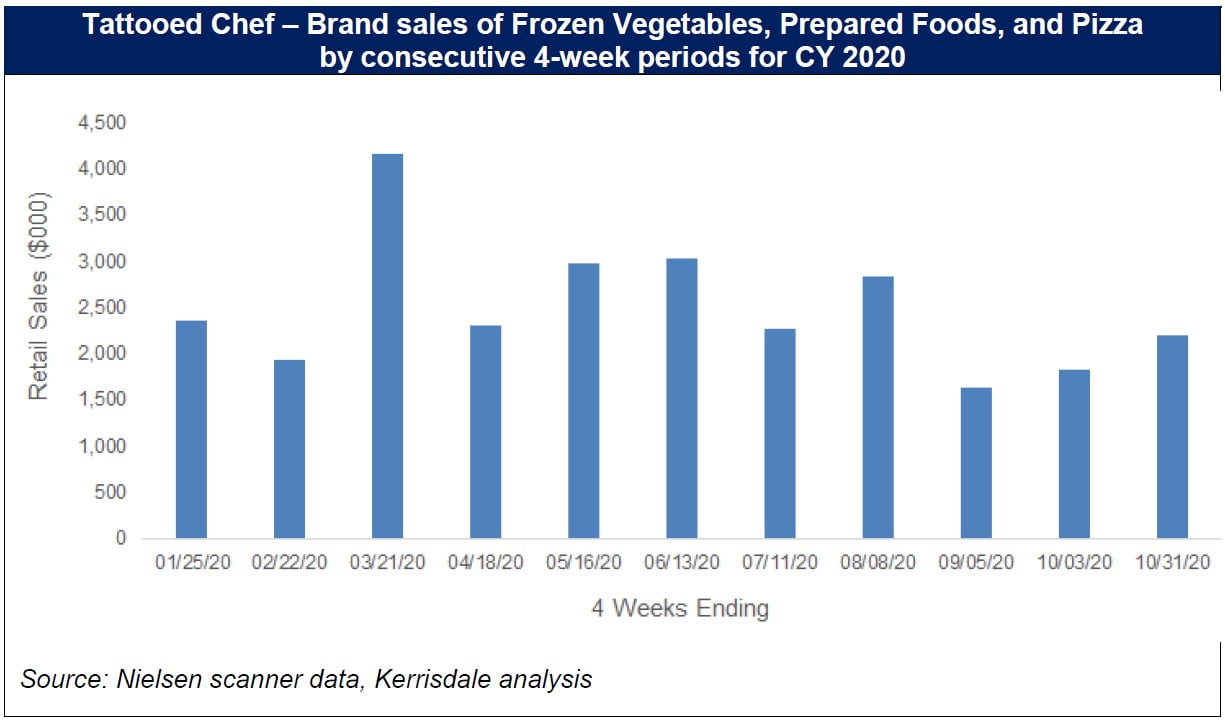

More worrying than an inability to expand into the grocery channel is recent scanner data that shows that across its customer base, over two thirds of which is comprised of Sam’s, the Tattooed Chef brand has dramatically underperformed comparable frozen food brands in recent months. While frozen food categories have begun their typical post-summer sales acceleration, Tattooed Chef’s sales at retail have just experienced their worst 3-month period since last December. That’s not exactly the mark of a “disruptive” and rapidly growing upstart that’s portrayed in the company’s investor presentation. Worse yet, breadth of the brand’s sales has narrowed considerably in recent months, concentrating primarily in just a handful of frozen prepared meal products and losing almost all momentum in frozen mixed vegetables.

Going public through a SPAC acquisition has allowed Tattooed Chef to avoid the kind of scrutiny that might reveal customer concentration risk far more serious than suggested by the company’s disclosures. It’s also allowed for a pandemic-driven paroxysm of consumer frozen food purchases at one retailer to be portrayed as sustainable sales momentum. But the reality cannot be hidden for long: Tattooed Chef’s frozen food sales are melting, and investors will be left holding the bag.

I. Investment Highlights

Retail sales of the Tattooed Chef brand have already stalled, suggesting a weak brand that is already suffering from consumer fatigue. Investor excitement around Tattooed Chef is centered around its eponymous branded products, which comprise about 55% of the company’s year-to-date revenues and are almost entirely responsible for the 90% year-to-date revenue growth rate. The brand’s products include “plant-based” frozen prepared meals such as cauliflower macaroni and cheese, cauliflower pizza, and acai bowls, as well as frozen vegetables like riced cauliflower and zucchini/squash spirals.

The narrative that has developed around the brand is that Tattooed Chef products are a chic and modern “plant-based” take on stodgy frozen prepared foods and vegetable mixes, which puts the brand in a great position to gain market share against legacy brands like Birds Eye, Green Giant, and Stouffer’s. A more extreme version of the narrative is that the “highly disruptive lifestyle brand” (CEO Sam Galletti’s description on the recent earnings call) belongs in the same category as rapidly growing “plant-based” versions of traditional proteins such as oat milk and Beyond Burgers. To date, it’s been difficult to evaluate the Tattooed Chef brand because the only information available to investors has come in the form of sparse disclosures in the company’s merger proxy, one presentation that management gave (and repeated since) when the acquisition was announced this past June, and its recent vague earnings release. Both the presentation and the recent earnings call also included tantalizing revenue growth guidance of ~75% for the 2020 calendar year and 50% for 2021.

Retail scanner data from Nielsen, which includes the brand’s sales at Sam’s Club, suggests an entirely different narrative than the one of a “disruptive” frozen vegetable juggernaut. While it’s true that the brand’s 2020 sales far exceeded those of 2019, the momentum has slowed considerably in recent months, with sequential sales performance dramatically underperforming industry sales patterns in comparable frozen food categories. The chart above tells a story that’s less about an upstart brand rapidly gaining share from dull competitors, and more about a brand that was flashy enough to get consumers to try it, but just not good enough to create permanent customers. While almost every frozen food brand saw retail sales decline from the panic-driven retail buying fueled by the pandemic in March, it’s almost impossible to find a brand where sales declined in the last 3 months from the typical July trough, let alone as significantly as they did for Tattooed Chef.

As we detail in the report that follows, Tattooed Chef’s branded retail sales trajectory over the course of 2020 has been markedly weaker than that of emerging brands that have demonstrably taken off with consumers. Even legacy brands with comparable products, such as Morningstar Farms, have found renewed pandemic-driven interest from consumers and have exhibited a much stronger sales cadence. By contrast, Tattooed Chef has gained traction only sporadically with 2-3 seasonal prepared food items sold at Sam’s Club, while failing to innovate beyond those products or make any headway in the frozen vegetables category. The result has been significant overall deceleration of sales at retail that will inevitably affect revenues in coming quarters.

In fact, this seems to have been unintentionally alluded to in Tattooed Chef’s most recent investor presentation, which projects that 52% of the company’s 2020 revenue will consist of branded products and the rest will come from private label sales. But branded sales accounted for about 56% of revenue over the first three quarters of the current fiscal year, so the annual projection contemplates an approximate 30% sequential branded revenue decline in the fourth quarter, which should theoretically be the seasonally strongest quarter of the year. It’s just another indication of the brand’s weakness, even as management has talked up 2021 revenue guidance and increased distribution.

Tattooed Chef’s customer concentration risk is much more than meets the eye. The most recent merger proxy filed by the company shows that in the 6 months ending this past June 30th, its two largest customers accounted for 39% and 32% of revenues, respectively. Based on the company’s investor presentation disclosures, as well as discussions with frozen food buyers at Sam’s Club and Costco, Sam’s is the top customer and expects to account for 35-40% of the company’s total projected 2020 revenues of $148 million. But that actually understates the concentrated nature of Tattooed Chef’s sales.

To understand why, it’s worth remembering that the company’s extravagant 7.5x sales valuation anticipates the rapid growth of branded sales. Adjusting for the much less exciting 45% of revenues coming from the private label business year-to-date, the branded business trades at closer to 13x 2020 projected sales. Sam’s Club accounts for 35-40% of total sales, or about 70% of these valuable branded sales.

Our discussions with Sam’s frozen food buyers and our analysis of Nielsen’s scanner data suggest a further element of concentration that poses a risk to Tattooed Chef’s investors: the overwhelming majority – we estimate over 75% – of the Sam’s Club business consists of just 4 products –cauliflower pizza, cauliflower burgers, cauliflower macaroni and cheese, and a seasoned corn bowl. The story at Costco, which accounts for about a third of the company’s total sales, is slightly different but also underscores the company’s concentration risk. Most of the Costco business is private label, but on the branded side, Costco stocks just 2 SKUs, including a slightly modified version of the corn bowl sold at Sam’s.1

Almost the entire value of Tattooed Chef rests on the moderate success the brand has had selling just a few different items to mostly one customer that belongs to one relatively narrow sales channel – club stores. It makes little sense to expect that performance to presage large-scale success in the vastly different grocery channel.

Tattooed Chef’s customer concentration reflects the limitations that impede its expansion into the grocery channel and will also make that expansion even more challenging. The layers of concentration risk – few products, few customers, one sales channel – are a feature, not a bug, of Tattooed Chef’s façade of commercial success. Prior to launching the Tattooed Chef brand, Ittella, as the company was known prior to last year, had a small business selling primarily large bags of Ittella-branded frozen riced cauliflower to both Sam’s and Costco. Those relationships were instrumental in getting the branded Tattooed Chef line in front of the frozen food buyers at the clubs, both of which were willing – to varying degrees – to give the new brand a try in their stores.

The club sales channel is characterized by large stores selling very few SKUs in large quantities and sizes, and at low but generally stable prices. In other words, from the standpoint of the vendor, it’s a relatively simple business because there’s no need for creative product assortments, detailed merchandising plans, or complicated distribution logistics. A new vendor just needs one or two products to which the consumer takes and the sales will follow. Still, the club channel is the last place branded food companies will try and penetrate – the customers are brutally cost-conscious and they want just one or two products, specially designed so that the consumer can’t find it at supermarkets, and at the risk that if the product bombs, a new one has to be designed (or the club store relationship severed). Given Ittella’s already existing relationship with Sam’s and Costco, though, it made perfect sense for Tattooed Chef to start there.

But aside from the fact that both channels sell packaged food, there’s not much in common between the club business and the grocery/supermarket business, and Tattooed Chef has none of the attributes needed to enter the latter. While the company’s investor presentation mentions “innovation” 13 times and boasts of 39 branded SKUs sold over the course of 2020, even management had to admit in the most recent earnings call that only 15 SKUs were sold through the club channel, while 13 SKUs generated enough sales at retail to make it past the low bar required to be included in retail scanner data.. The product count is closer to 8 after adjusting for small differences that technically necessitate another SKU, and the business at Sam’s and Costco can be attributed almost entirely to 4-5 items. That’s a far cry from 39. And it’s not for lack of trying – many of those 39 have been attempted, including at Sam’s, and simply didn’t catch on. Putting new products on a shelf isn’t innovation. Successfully selling those products is but Tattooed Chef hasn’t been able to do that, and it won’t be possible to enter the grocery channel without it.

Worse yet, discussions with Sam’s buyers reveal that Sam’s has made it clear to Tattooed Chef that it strongly prefers that the attempt to penetrate the grocery channel be driven by frozen vegetable mixes rather than the higher-margin prepared foods that have sold well at Sam’s. Unsurprisingly, Sam’s has no desire to compete with supermarkets on a narrow set of successful products that Sam’s itself was responsible for seeding. The impetus to keep its largest customer happy by testing any potentially successful product at Sam’s, and the consequent inability to leverage that successful product at a larger scale, will be a lasting and damaging legacy of the initial success that Tattooed Chef attained through the club channel.

Finally, it’s quite apparent that Tattooed Chef’s executive team isn’t really aware of the merchandising competence necessary to build branded relationships with grocers. Merchandising means targeted price reduction programs, seasonal promotions, shelf placement consulting, and other subtle elements of selling packaged foods through grocers that are entirely absent from the club store relationships. As one large packaged foods distributor told us, “selling to an EDLP [every-day-low-price] customer doesn’t prepare you for selling into Kroger’s or Whole Foods…Tattooed Chef’s announcement that they’ll sell frozen enchilada bowls direct to consumer shows that they’re amateurs…they have no idea what they’re doing.” Neither do their shareholders.

Read the full article here.