Third Point Founder And CEO Dan Loeb writes a letter to The Walt Disney Company’s CEO, showing his appreciationg for the company’s DTC business.

Q2 2020 hedge fund letters, conferences and more

Mr. Robert A. Chapek

Chief Executive Officer

The Walt Disney Company

Burbank, CA

Dear Mr. Chapek:

As major shareholders of The Walt Disney Company, we write to express our appreciation for your increased focus on the company’s direct-to-consumer (“DTC”) business. We strongly support your decision to direct marquee content like Hamilton and Mulan into the DTC channel, and look forward to hearing more about your “accelerated push” into this model at Disney’s upcoming Investor Day. Ahead of this event, we thought you would be interested in our views about the DTC business that we believe could meaningfully accelerate growth for the company and value creation for shareholders.1

The Walt Disney Company's Transition

Since its founding, Disney has been defined by its creativity, bold vision, and prescient grasp of the future of entertainment. We share the view that Disney is embarking on one of the most important transitions in its history: shifting distribution of the world’s most iconic entertainment brands from the box office to the home. Disney+ has made admirable early progress. Before launching Disney+, management demonstrated laudable vision by rolling out a multi-billion-dollar investment plan that exchanged near-term earnings for long-term value creation, and the market rewarded the company for doing so. Just twelve months later, Disney has built one of the largest streaming platforms in theworld, already within the original 5-year Disney+ subscriber target range of 60-90 million.

To further capitalize on this transformational opportunity, we believe the company should permanently suspend its $3 billion annual dividend and redirect this capital entirely into content production and acquisition for The Walt Disney Company’s DTC businesses, centered around Disney+. By reallocating a dividend of a few dollars per share, Disney could more than double its Disney+ original content budget. These incremental dollars would, based on our analysis, generate returns that are multiples of the stock’s current dividend yield by driving high life-time-value (“LTV”) subscribers to your DTC platform. Even at the current ~5% monthly churn level and $6.99 monthly price point, the gross LTV of a Disney+ customer is well north of $100. Consider Hamilton, which analysts speculate drove an incremental 2 million subscribers onto Disney+, and thereby created hundreds of millions of dollars in value for Disney shareholders. These are substantial returns when compared to the mere $75 million it cost Disney to acquire rights to the film. We are fully confident that scaling that $75 million to several incremental billions and focusing that spend on Disney’s iconic in-house brands like Marvel, Star Wars, Pixar, and Disney Animation as well as selected acquisitions would drive even greater subscriber growth for Disney+, and subsequent value creation for Disney’s shareholders.

Beyond bringing additional subscribers onto the platform, increased velocity of dedicated content production will deliver several knock-on benefits spread across your existing base including elevated engagement, lower churn, and increased pricing power. To put this in perspective, improving Disney+ churn to Netflix’s industry-leading ~2% domestic churn levels would more than double gross subscriber LTV. When combined with driving pricing to Netflix’s current $13 domestic average monthly price, gross LTV would quadruple to nearly $500 per subscriber. Together, the ability to drive subscriber growth, reduce churn, and increase pricing present the opportunity to create tens of billions of dollars in incremental value for Disney shareholders in short order, and hundreds of billions once the platform reaches larger scale. We appreciate that this math is illustrative and fails to consider several costs of running the Disney+ service (into which you have better insight than we do). However, there is no arguing against the $1,200 per subscriber valuation the market currently ascribes to Netflix. It is even harder to argue against the step change in returns Disney could generate by accelerating content spend (measured in multiples) compared to paying that same capital to shareholders in the form of a dividend (measured in a low single-digit percentage).

Accelerating DTC Content Spend

Of equal importance, meaningfully accelerating DTC content spend will further broaden the divide between The Walt Disney Company and its traditional media peers - AT&T’s WarnerMedia, Discovery, ViacomCBS, Comcast’s NBCUniversal and Fox – none of which have the financial capabilities to execute such a bold plan. A more aggressive content roadmap will distinguish Disney as the only traditional US media company able to thrive in a world beyond the box office and the cable TV ecosystem, alongside digital-first businesses like Netflix and Amazon.

We also believe that collapsing all of Disney’s DTC services into the Disney+ application will simplify the product and be a meaningful enhancement to Disney’s offerings. Given that Disney+’s subscriber base is already meaningfully larger than any of your other DTC services, we believe Disney would benefit from a single customer acquisition vehicle led by Disney+. We understand that each of your DTC services – Hulu, ESPN+, and the upcoming Star offering – serve different demographics and may have various value propositions, but these challenges can be easily circumvented through tiered and bundled product offerings at various price points. Importantly, all product offerings should lead with the company’s marquee Disney product and brand.

We understand that a more aggressive investment strategy may pressure short-term earnings on the path to creating long-term value. Lest there be reservation about making such a trade-off and any potential shareholder concerns, we highlight an observation from Warren Buffet: “companies get the shareholders they deserve.” The Walt Disney Company deserves growth-minded, long-term oriented investors, and we believe that a strategy centered around using Disney’s many resources to drive growth in the DTC business will further attract them. With Disney’s superior tentpole franchises and production capabilities, we believe that the company can exceed the subscriber base of the industry leader, Netflix, in just a few years. But time is of the essence and the company should consider significant additional investments in content both through production and acquisitions here and abroad.

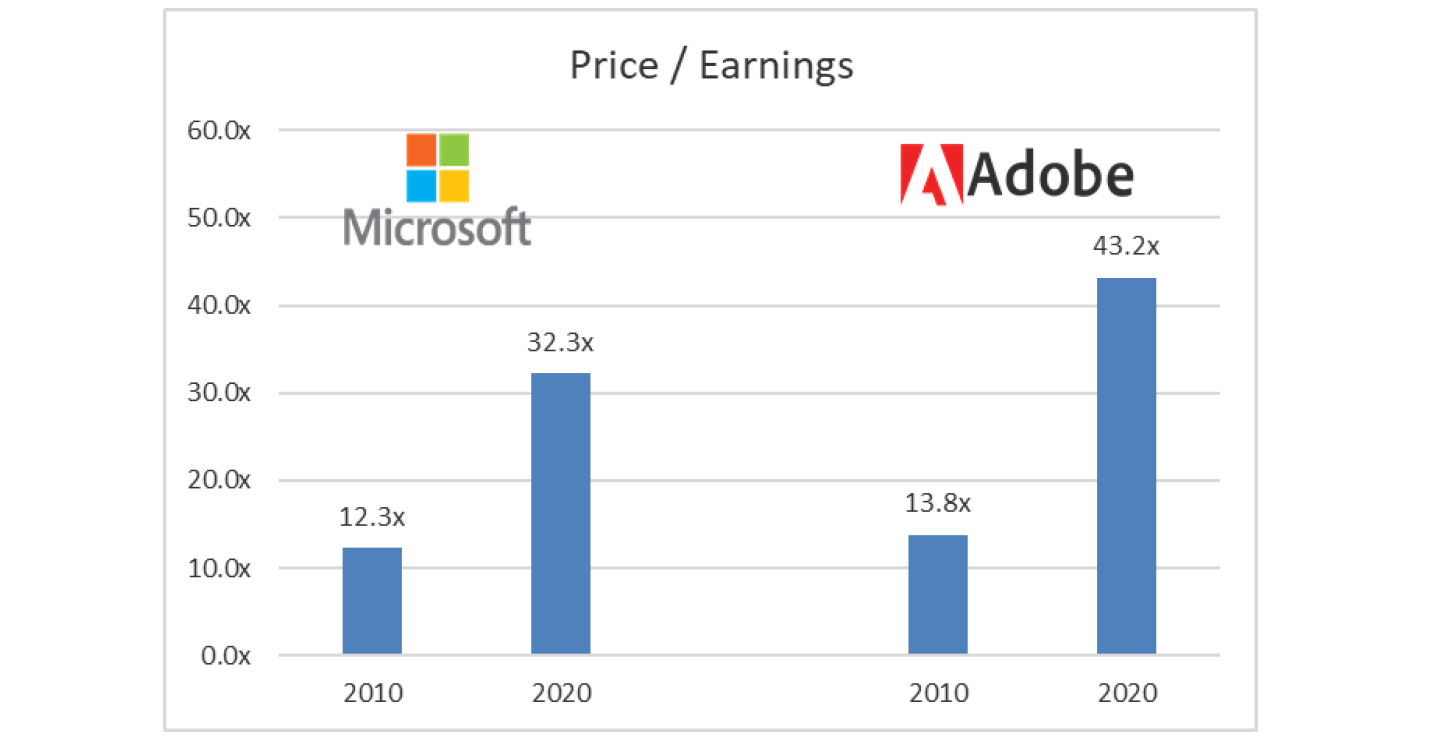

As experienced public market investors, we have observed numerous precedents of successful non-linear business model transitions that paid off handsomely for shareholders. Among such business transformations, Adobe and Microsoft stand out as particularly relevant examples of companies which, in order to optimize their distribution models, had to forgo lucrative upfront license revenues in exchange for monthly subscriptions. Investors have learned that while these strategic shifts may depress near-term earnings, their patience will be rewarded with businesses many multiples the size of what they once were. Furthermore, the stocks were rewarded with significantly higher multiples reflecting the superior quality of their new recurring, subscription revenue streams (a significant improvement over their historic lumpy transactional model). Both companies’ shares have appreciated significantly since these transitions began.

Subscription-Led DTC Revenue Stream

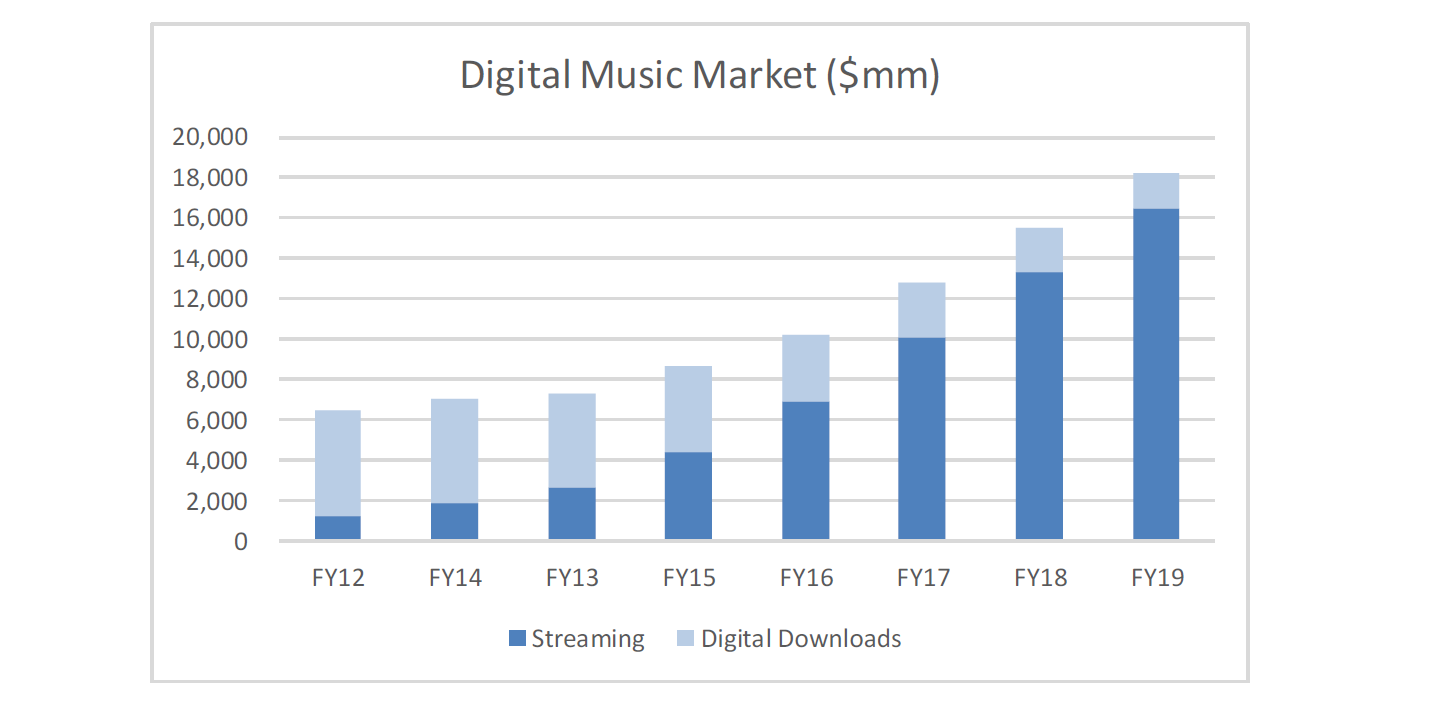

Finally, we believe Disney should maintain its focus on transitioning to a subscription-led DTC revenue stream and avoid the temptation of maximizing short-term profits through transactional VOD pricing strategies. While it may be tempting to extract short term financial profit from each marquee film and TV series that The Walt Disney Company produces, we are confident that the ‘all-you-can-eat’ approach is the best way to maximize the longer value of Disney’s content and enterprise by accelerating subscriber growth. We look to the music industry as an appropriate analogue, where Spotify and other music streaming peers have built a digital subscription industry that is multiples of the iTunes ‘a-la-carte’ model. If Spotify can accomplish this feat as a pure distribution platform in an industry where piracy is rampant, we have no doubt that your subscription DTC business, once it becomes the primary landing ground for all Disney’s content, will surpass any pay-per-film revenue stream. As shown in the software industry, we also expect this subscription revenue stream will be capitalized at much higher multiples than a transactional one. While some pundits have described the Mulan release as a “debacle” due to the $29.99 cost for a VOD download, we see this as a valuable learning experience, expect stumbles on the way to greatness, and believe this will drive a faster decision to make all content available to subscribers for a simple subscription fee.

The current 60 million Disney+, 36 million Hulu, and 9 million ESPN+ subscriber bases represent a commendable start, but nowhere near their full potential. There are currently 1.1 billion global broadband-enabled homes around the world and 4 billion mobile subscribers, across which at least 1 billion Disney fans are spread. With broadband and mobile connectivity expanding, this end market, and thus Disney’s total DTC addressable market, is growing rapidly. These fans want an easier and more affordable way to access Disney’s marquee content. We are confident that Disney can build a DTC business that will meaningfully exceed its current cable TV and box office revenue streams, but only if the company leans into this opportunity and invests more aggressively. Just this week, Regal Cinemas shuttered all its US operations and physical theaters. While we all share a certain sadness and nostalgia for this eventuality, I am sure that people felt similar emotions about horse-drawn carriages when the automobile was first introduced. Every Hollywood executive has been able to enjoy first run films in the comfort of their home theaters for years. We urge you to democratize this experience and to continue to embrace the future of home entertainment with the utmost urgency in executing the company’s digital transformation.

We look forward to continuing a constructive dialogue.

Sincerely,

Daniel S. Loeb

Founder/CEO

Third Point LLC

The information in this presentation is for information purposes only, and this presentation does not constitute an offer to purchase or sell any security or investment product, nor does it constitute professional or investment advice. The information in this presentation is based on publicly available information about The Walt Disney (the “Company”). Except where otherwise indicated, the information in this presentation speaks only as of the date set forth on the cover page, and no obligation is undertaken to update or correct this presentation after the date hereof. Permission to quote third party reports in this presentation has been neither sought nor obtained.

This presentation may include forward-looking statements that reflect the current views of Third Point LLC or certain of its affiliates (“Third Point”) with respect to future events. Statements that include the words “expect,” “intend,” “plan,” “believe,” “project,” “anticipate,” “will,” “may,” “would,” and similar words are often used to identify forward-looking statements. All forward-looking statements address matters that involve risks and uncertainties, many of which are beyond the control of the parties making such statements. Accordingly, there are or will be important factors that could cause actual results to differ materially from those indicated in such statements and, therefore, you should not place undue reliance on any such statements. Any forward-looking statements made in this presentation are qualified in their entirety by these cautionary statements, and there can be no assurance that the actual results or developments anticipated will be realized or, even if substantially realized, that they will have the expected consequences to, or effects on, the Company or its business, operations, or financial condition. Except to the extent required by applicable law, we undertake no obligation to update publicly or revise any forward-looking statement, whether as a result of new information, future developments, or otherwise.

Third Point currently has an economic interest in the price movement of the securities of the Company. It is possible that there will be developments in the future that cause Third Point to modify this economic interest at any time or from time to time. This may include a decision to sell all or a portion of its holdings of Company securities in open market transactions or otherwise (including via short sales), purchase additional Company securities (in open market or privately negotiated transactions or otherwise), or trade in options, puts, calls or other derivative instruments relating to such securities. Third Point also reserves the right to take any actions with respect to its investment in the Company as it may deem appropriate, including, but not limited to, communicating with the board of directors, management and other investors.

Although Third Point believes the information herein to be reliable, Third Point makes no representation or warranty, express or implied, as to the accuracy or completeness of those statements or any other written or oral communication it makes with respect to the Company and any other companies mentioned, and Third Point expressly disclaims any liability relating to those statements or communications (or any inaccuracies or omissions therein). Thus, shareholders and others should conduct their own independent investigations and analysis of those statements and communications and of the Company and any other companies to which those statements or communications may be relevant.