Back in the early 1970s, there was a group of companies which are referred to as “The Nifty Fifty” in the US. These were companies which were expected to grow earnings forever, by taking advantage of trends in demographics and the economy of the future decades. The stocks were often described as “one-decision”, as they were viewed as extremely stable, even over long periods of time.

Q2 2020 hedge fund letters, conferences and more

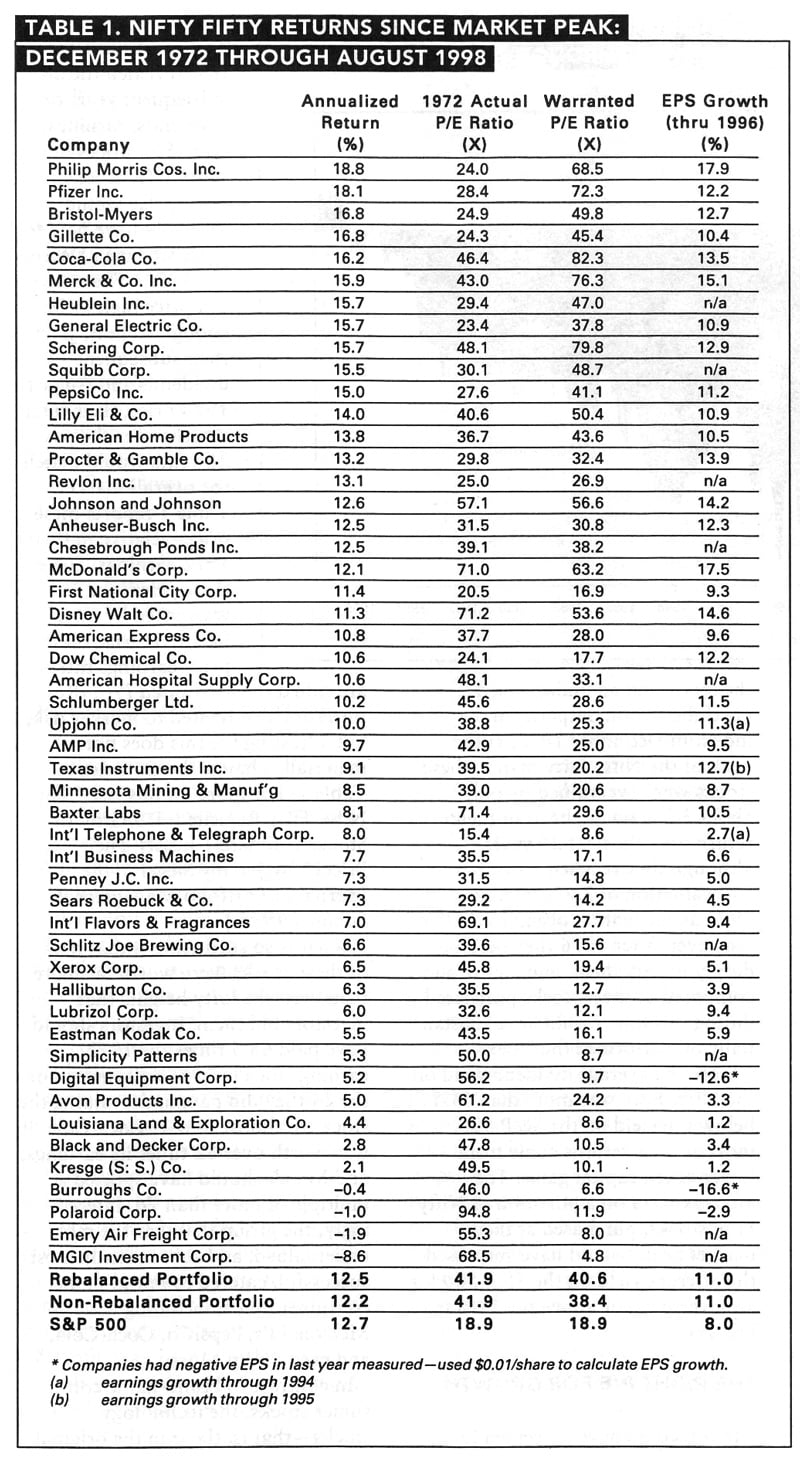

Extraordinary High P/E Ratios

The most common characteristic by the constituents were solid earnings growth for which these stocks were assigned extraordinary high price–earnings ratios.

A P/E of forty times earnings, far above the long-term market average, was common for these one-directional glamor stocks.

As a result, these companies were seen as one-directional bets which were good investment ideas at any price. The investment public was excited about these companies prospects, and wanted in at any price, without thinking about valuation.

Since buyers were willing to acquire these companies at any price, the prices moved higher. As prices moved higher, investors who bought without worrying about valuations felt vindicated and wanted to buy more without paying attention to valuation. Those who missed out wanted to buy in as well, which pushed prices even further up. By late 1972/early 1973, a lot of these Nifty Fifty companies were selling at insanely high valuations. That was because investors expected lots of future growth for these enterprises. The rest of companies in the US were more adequately valued, but were ignored by many investors, because they were not exciting enough.

By 1973 investors lost interest in the stock market, and by the bottom in 1974 lots of the Nifty-Fifty stocks were down by 70 – 80 – 90% from their highs just a couple of years earlier. Many of the companies did not deliver price increases for a while, with the majority of their returns coming from dividends in the first decade since the top. Some of these Nifty-Fifty companies ended up failing outright, while a few others ended up becoming successful beyond their original investors dreams.

In reality, an investor who bought a portfolio of these companies and held through thick and thin for the next 30 years did well in the end.

The Original Nifty-Fifty Stocks

While that doesn’t matter to me as much as it does to others, the portfolio of the original Nifty-Fifty companies did slightly better than the S&P 500. This is according to research from Jeremy Siegel, which you can read about here:

Valuing Growth Stocks: Revisiting the Nifty Fifty

The problem is that it took 30 years to get there. A lot of investors would have bailed out at the first sign of trouble. Even if you managed money and held these companies, your investors may have wanted out. So it is very likely that very few investors realized the excess returns.

Lessons To Be Learned

There are lots of lessons to be learned from the Nifty-Fifty companies of the 1970s.

The first lesson is to be diversified. Nobody could have known in advance which of these companies would turn out to be rockstars in terms of performance, or which would turn to ashes. Therefore, it makes sense to spread your bets accordingly. Doing so on an equally weighted basis makes sense.

The second lesson is to hold through thick or thin. If you buy a portfolio of investments, put them away and just forget about them. If you are going to be disappointed, because a company did poorly over a certain short period of time, you will never have the tenacity to hold on to any portfolio you select. It is possible that any portfolio could disappoint over any short-term period of time of five to ten years. Of course, deciding whether your portfolio is truly bad or it simply has a temporary setback is more art than science. This is similar to the Coffee Can Portfolio approach.

The third lesson is that valuation matters. Buying these securities at lower valuations would have resulted in an amazing track record. Buying these securities without worrying about valuation would have generated a great return, but a lifetime to get there. If it appears that an investment is “not working”, many investors may be quick to abandon ship. Selling is usually a mistake.

However, I did some additional digging and learned that there never was an official Nifty Fifty list of securities. It is quite possible that the securities in Jeremy Siegel’s list were not the ones investors were buying in the 1970s. Therefore, their results would have been wildly different than what Jeremy Siegel suggests. His research makes me believe that it is fine overpaying for securities, because things worked out at the end. He even goes on to show that certain overvalued securities like Altria were not overvalued enough, since they generated amazing returns over time.

I do not like where this is going, because I think that overpaying for securities teaches investors bad habits and can lead to buying companies without thinking about valuations or fundamentals. And most importantly, that can lead investors to ignoring any common sense and buying without having any margin of safety. Just because things worked out in the end, doesn’t mean that things couldn’t have gone the other way.

Overpaying For Securities

Altria could have just as easily taken the path of John’s Manville and wiped out the common shareholders in the process due to lawsuits. I think that blindly buying securities is not a good habit in the first place. Therefore, I would caution against overpaying for securities, no matter how exciting their growth prospects may seem. That’s because the future can be uncertain, and things could change for one reason or another – competition, government regulation, changes in consumer tastes and preferences, technological disruptions etc.

To reiterate the third, but most important lesson, you should not overpay for future growth. While a lot of the hot growth companies of any era are usually seen as high quality, they are frequently overvalued. However, buying an overvalued security exposes the investor to the risk of valuation shrinkage. This is where you buy a security at an inflated valuation of say 50 times earnings, and then your growth expectations materialize, but the business is now worth only 10 times earnings. After all, trees do not grow to the sky, and growth usually hits a plateau after a few years, due to competition, obsolescence and disruptions and regulations. If you buy for 50 times earnings, and earnings go up 8 times in 21 years, your stock would only go up by 60% in total.

When you overpay too much for a security, you are taking a big gamble, and you are probably speculating. No company is worth overpaying for.

I have seen this lesson everywhere I have looked. For example, Japanese stocks did very well in the 1980s, delivering double-digit mouthwatering returns. Japan was overvalued in 1980, but still delivered amazing returns to investors. When returns come easy, without looking, it would be easy to tell yourself that valuations do not matter.

Unfortunately, the stock market was selling at 100 times earnings by 1989 and a dividend yield below 0.50%. It has taken the stock market 30 years for it to sell for a more normal P/E of roughly 12 and a dividend yield of roughly 2% - 3%, while the stock market is down by 50% since then. This means that earnings per share and dividends per share have been rising gradually over the past 30 years. The reason why investors didn’t generate much in returns is due to the massive overvaluation of securities. While ignoring valuations worked in the 1980s, the law of gravity caught up with investors by 1990, and they are still paying the price many decades later.

I saw this first hand in 1999 and 2000, when stock market investing became a national sport, and companies sold at high valuations. As a result, we had the lost decade in 2000 – 2009, where stock prices went nowhere, despite increases in earnings and dividends. It took a decade for fundamentals to catch up to share prices. Since share prices are driven by investor sentiment, we went from massive exuberance in 1999/2000 and overpaying for future earnings to a massive depression in outlook for stocks and unwillingness to pay for future earnings.

My analysis of the performance of the Nasdaq 100 companies from 2000 shows that it ultimately did work out for investors. However, we should also strive for margin of safety and some humility along the way. In general, while investing in Nifty-Fifty from 1972 ultimately worked out, I still think investors should be cognizant of these factors:

Investors should always be conscious of starting valuation when placing their bets. Starting valuation matters.

Ignoring entry valuation may work for a while and the ease of making money may trick you into believe that it doesn’t matter.

When stocks go nowhere or go down from your purchase price, you may have to wait for a long time, before even breaking even.

Relevant Articles: