Excerpted with permission of the publisher, Columbia University Press, from One Up by Joost van Dreunen. Used by arrangement with the Publisher. All rights reserved.

Q2 2020 hedge fund letters, conferences and more

10 Next-Gen Revenue Models

In the near future, we’ll have games that don’t depend on any platform. - Hideo Kojima, creator of Metal Gear series

Now that video games are a mainstream form of entertainment, the underlying economics that drive this industry have shifted. Geographic boundaries and homogeneity of its audience no longer restrict game companies. We may ask: does this newfound status and broader cultural visibility enable revenue models that previously were unsustainable?

So far, we identified two distinct eras in the games business. Starting with selling boxed titles through retail and tying software sales closely to the hardware cycle of consoles, interactive entertainment has been a product-based business since its inception. The production of physical goods that are distributed and sold through stores characterizes this period. Consumers paid a single, one-time fee in exchange for access to content, which, as we saw, sits at the very foundation of the razor-blade model of hardware manufacturers. The need for content curation and quality assuance facilitates both overall growth and the emergence of entry barriers for creative firms. This, in turn, allowed a small group of highly successful industry participants to dominate the most lucrative categories. Electronic Arts’ strategy to simultaneously corner the market for sports licenses and establish a global sales force resulted in it claiming a dominant industry position for years.1 Across the board, legacy publishers took on the capital risk associated with the production and marketing of blockbuster releases.

Success in this model consequently was expressed as the total number of units sold. By leveraging control over the value chain, publishers maximized their ability to sell as many copies as possible at the highest possible price.

With the advent of the internet began a second era: the digitalization of video games. In the aftermath of the dotcom bust, game makers quickly established themselves among the de facto suppliers of valued, novel content in an expanding digital universe. As incumbents wrestled with the poor economics of digital distribution, which allowed them to capture only accretive revenue, a new generation of companies emerged focused on attracting mainstream audiences through lightweight gameplay, accessible distribution, and novel revenue models. Firms like Nexon, Riot Games, and King Digital benefited from formulating innovative business strategies and came to characterize the digital industry. They popularized a games-as-a-service revenue model in which the measure of success consisted of the average earnings per user. This evolution triggered enormous growth and transformed the industry into a mainstream leisure activity that now caters to a global audience. The lowering of entry barriers resulted in many small developer outfits connecting with users directly and facilitated an artist-led model that previously had been unsustainable.

The industry’s progression has not stopped there. With two billion people actively playing games across mobile, console, and PC devices, publishers and platform holders now are exploring two prospects for what may soon become the next relevant source of income: indirect revenue (i.e., advertising) and recurring revenue (i.e., subscriptions).

Advertising

Unlike firms in every other entertainment category, game companies have been largely unwilling and unsuccessful in generating indirect revenue. At best, the effort to connect advertisers to their audiences is nascent. We can explain this in part by the broadly accepted perspective among creatives that money corrupts the art of making games. The tension between creativity and commerce has been prevalent throughout this book but perhaps nowhere as pronounced as in the context of ad-sponsored games. Product-based titles historically spent years in development before a publisher had a chance to promote it to consumers. In this scenario, anticipated revenue became a priority only in the lead-up to its release. By and large, creatives were not concerned about the financial outcome of their efforts until a title was fully developed. This allowed them a financial vacuum in which they honed their craft in pursuit of the best possible experience. Having to insert a monetary component into the design process introduces a new constraint on the overall creative endeavor. Zynga is an example of this. Its early success resulted from constantly measuring how well specific items performed in its virtual store. By relentlessly analyzing what worked and what did not, Zynga managed to optimize its development effort accordingly. Data, of course, were geared toward maximizing the amount of money that people spent on the game. In response, many held Zynga in low regard, arguing that instead of publishing true creative experiences, it merely designed its content to funnel players through a never-ending monetization loop. This approach deviates strongly from the traditional emphasis on creativity and delivering immersive experiences.

In entertainment, games have long existed on the fringes and have presented an odd business to media executives. It has been a long-held belief that advertising and video games do not mix. Ad revenue historically has played only a marginal role in interactive entertainment, despite a much greater prominence everywhere else. When online connectivity facilitated building a network that enabled dynamically integrating ads into games, the time for in-game advertising seemingly arrived. Microsoft found out exactly how incompatible games and advertising were when it acquired an in-game ad network called Massive in 2006. The software giant’s rationale at the time provides valuable insight into a failed business model innovation.

Initially, Massive’s business model showed great promise. By adding a few lines to a game’s source code, it was able to insert ads into the experience through the internet with the intent of becoming the intermediary between the two company types. In return, it would take a slice of the revenue. Massive’s CEO Mitch Davis quipped that its solution added “$1–2” to a company’s bottom line per unit sold.2 As we saw earlier, development had started to become more complex and costlier. The interest for in-game ads surfaced between 2004 and 2006, around the same time the industry started to introduce games at a considerably higher average selling price to offset the investment in developing titles for the new hardware generation (see figure 3.3). Adding a few bucks for each copy improved the risk profile and profitability.3

Massive raised a total of $8 million in funding. Advertisers were excited and spent an estimated $414 million annually on media buys in video games at the time. Despite a slow adoption rate among publishers for whom this was new and unfamiliar territory, Massive succeeded in establishing a network that included several notable early adopters like Atari, Codemasters, Eidos, Funcom, Konami, Sony Online Entertainment, THQ, Ubisoft, and 2K Sports.4 This initial success was enough to convince Microsoft of the long-term benefits, and it promptly acquired Massive in 2006 for an estimated $200 million.

It is not immediately obvious why Microsoft, which is mostly known for its enterprise software, would buy an in-game ad company. There were no clear synergies. More broadly, however, its relevance had started to suffer as competitors like Google managed to build billion-dollar businesses on the internet. Consequently, an important part of Microsoft’s rationale had to do with its insecurity around losing online audiences to a new generation of tech firms. It was not alone in this, and the purchase coincided with a broader industry trend of big media conglomerates looking to “get into gaming” through acquisition. That same year saw a string of similar merger and acquisition activity: Viacom spent $102 million buying XFire, an online social network around video games; NewsCorp bought IGN Entertainment for $650 million; and Google acquired Adscape, an ad firm that specialized in integrating in-game advertising. Other competitors at the time included IGA Worldwide, Double Fusion, Extent Technologies, Navigate, Engage, and Greystripe, all of which fixated on the idea that the time for a marriage between interactive amusement and advertising had come.

Another aspect of Microsoft’s rationale originated from its broader strategy to increase the use value of its device for consumers by positioning the Xbox at the center of the living room. Microsoft held a formidable portfolio of development studios that included Bungie, Carbonated Games, Ensemble, FASA Interactive, Lionhead, Rare, Turn 10, and Wingnut Interactive. Integrating the ad network in all of these studios meant it would control access to their aggregated audience. As we read in chapter 6, Microsoft also started adding a string of services to its platform in the hope of pushing competitors out of the living room and becoming the primary device used by consumers to access content. Part of Microsoft’s reasoning was to sell ads against this aggregated audience.

But this move was not to be, and in 2010, Microsoft shut down Massive. In its enthusiasm, the software giant critically overlooked several things. For one, game developers had never before considered advertising as a relevant revenue stream, and they had no interest in sitting through a meeting with an ad platform to hear about the merits of their offering. To creatives, the idea of adding a bit of third-party code to a game they had spent years developing was blasphemy. According to one executive: “The account manager would work with the publisher after which the integration fell to the developers. Generally, this happened toward the end of the production of title, leaving us with little resources. Devs would come back to us saying they couldn’t do it because they were out of memory.” Technical and operational limitations forced Microsoft to dispatch last-minute client support, which made the effort cumbersome and largely unprofitable.

Massive’s executive team also critically lacked the necessary experience. Although many of them had held positions at large media firms and consultancies, few had any games industry credentials. As a result, their entry point into creative firms generally was through the corporate teams at game publishers. Executives reasoned that in-game advertising added realism to the experience. According to Kevin Johnson, Microsoft’s co-president of Platforms and Services (and who would later become the CEO of Starbucks), a racing title like Tokyo Race Driver 3 “is obviously a great place to advertise car insurance like Progressive. What you get a sense for is the ability to drive better consumer excitement, because they get more realism. You can drive rich, immersive advertising.”5 This approach, according to Johnson, made consumers “happier.” But that, too, turned out to be a horrible misconception. Players, in fact, were upset that their games suddenly showed ads. In this context, ads were new and invasive without offering any benefit to the player. In a similar vein, intellectual property holders were uninterested in having their properties sit alongside commercial messages, especially if they had no control over the type of ad. To them, this could only lower the value of their carefully cultivated franchises.

A final reason Massive failed was that, ultimately, it competed directly with its acquirer Microsoft. On top of a botched integration process that crippled Massive’s ability to grow, the parent company insisted on facilitating in-game ads, in particular for the studios and titles it already owned. Worse, big publishers like Electronic Arts started running in-game ad networks inside key franchises like FIFA, for which ads conceivably would be perceived as contextually relevant. This proved fatal to Massive’s momentum, and Microsoft shut down the division.

Despite all of this activity and investment, advertising income never grew large enough to become relevant. Simultaneously the market had started to move away from display ads to search-based ads, which further exacerbated Massive’s circumstance. Observing the failure of even a large multinational like Microsoft, we may ask: Why would advertising as a revenue stream for game companies work now?

To establish a reliable two-sided model that allows publishers to efficiently connect brands to their audience, the industry needs a broad and diverse consumer base. As discussed in chapter 4, that is now the case. This need is a first reason why ads now take on a more meaningful role. Like broadcast television, radio, newspapers, and magazines, video games attract billions, which positions this business to claim a piece of the billions of dollars spent each year by advertisers. Globally, advertisers spend around $650 billion on media and entertainment. In the United States, the second-largest market after China, television generates $70 billion a year in ad sales, compared with $15 billion for print media, and $14 billion for radio. As these audiences continue to age and decline in size as people move to new technologies to consume content and those that remain tend to skew older, advertisers have started to turn to gaming. On paper, this makes sense: gamers are tech savvy, highly engaged, and early adopters, which makes this consumer group valuable to advertisers.

Second, the more recently emerged generation of game makers takes a different approach to indirect revenue. Unlike legacy publishers to whom this represents only a modest revenue stream in comparison to the income generated from their top franchises, newcomers are open to the idea of accepting money from advertisers. In their view, the relationship between ad-based revenue and a creative agenda is less tenuous and central to their economics. Rather than imposing, they argue, it frees them from revenue obligations and having to aggressively monetize their players.

Following the tremendous success of Pokémon GO in the summer of 2016, Niantic CEO John Hanke went on to explain that ad revenue was beneficial and allowed his studio to focus on its creative pursuits. According to Hanke, advertising presented a viable alternative monetization strategy because integrating microtransactions “exerts a lot of pressure on game design that can lead to games that are not very much fun to play even if they make a lot of money.”6 Instead of aggressively monetizing through microtransactions, Hanke reasoned, it was more intuitive to drive traffic to specific real-world locations and charge retailers for it.

This proved to be remarkably successful. During the height of its popularity, the firm struck deals with several notable retail chains, including McDonalds and GameStop. In Japan, Pokémon GO featured fifteen hundred McDonalds’ restaurants as poke-gyms and successfully increased foot traffic at those locations. In the United States, GameStop had a similar arrangement and saw a spike in the number of people visiting its stores. As a result, it managed to upsell visitors on battery packs and data plans.

According to Niantic, the initial ad campaigns had been so successful that it was only the beginning as a growing number of companies and brands contacted the firm for comparable campaigns.

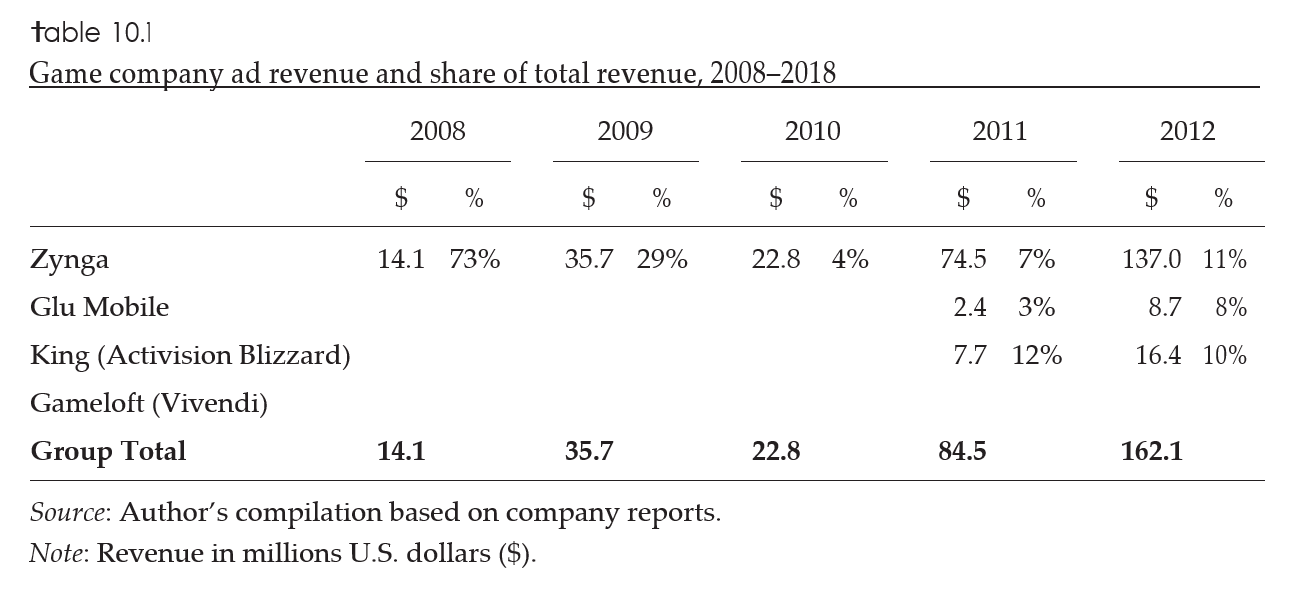

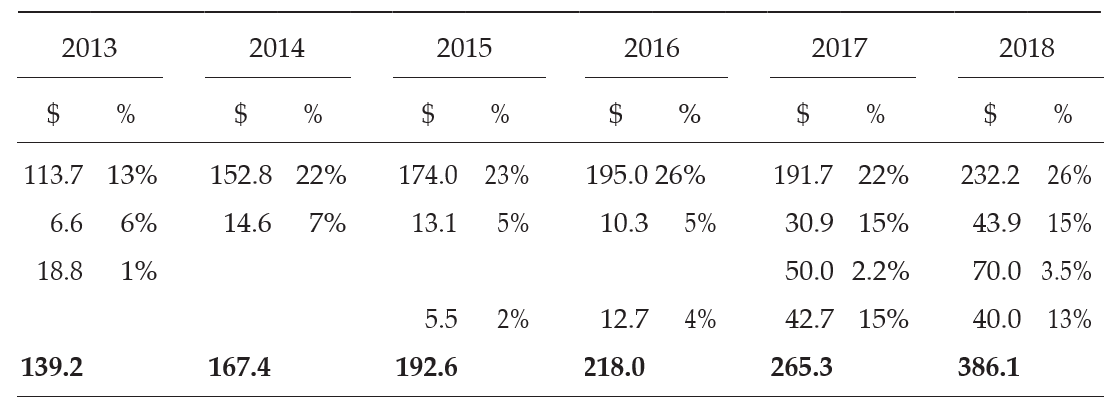

Another mobile giant had also come to appreciate the opportunity of ad revenue, despite having walked a different path. At the height of its success in 2013, King Digital had initially sent an email to its advertising partners that explained why it would no longer rely on them for income. According to the email, the firm’s commitment to providing “an uninterrupted entertainment experience” meant it was going to remove all advertising components from its games.7 This was not surprising as the success of its titles like Candy Crush meant that advertising income represented only around 1 percent of total earnings (see table 10.1). Nevertheless, as an organization with deep roots in both social network–based and mobile gaming, both of which are characterized by their ad-heavy nature, this was a shock to many. King’s success meant that it did not need to rely on indirect income and could monetize its audience directly through microtransactions.

This proved to be only a temporary abstinence. Following its acquisition by Activision Blizzard, King saw its momentum decline and came under pressure to make its earnings goals. It had suffered a disastrous initial public offering and had to confront the general slowdown in its business as competitors swept in and audiences moved on. Increased competition also put pressure on King’s ability to draw revenue from its existing player base. King readopted the model. Its monthly active user count had declined, but King still reached such a massive player base that it was well worth it to embrace advertising again in 2017.

Of course, only the disproportionally popular titles like Candy Crush and Pokémon GO have managed to establish meaningful revenue from advertising. We already can see, however, a rough outline of how the broader adoption of this income may play out. Across the ecosystem, we find other initiatives by large firms that push in this direction. Google’s cloud gaming solution, Stadia, offers game publishers a 30/70 revenue split in addition to a cut of ad revenue generated by video content featuring their titles. Facebook similarly is enticing publishers, hoping that gaming content will drive traffic and engagement. And Tencent used ads to offset the decline in revenue it suffered in 2018 as a result of its government shutting down the approval process for new titles to be released in China. The success it initially enjoyed as a result of the market protectionism enforced by the Chinese government has proven to be a limitation in more recent years. At the height of the success of titles like PlayerUnknown’s BattleGround (PUBG) and Fortnite, Tencent saw itself unable to monetize because of a government reorganization that, ultimately, sought to purposefully stall the approval processes before titles could be monetized in China. To make up the difference and continue its growth, Tencent triggered a reorganization that, among other efforts, united the firm’s advertising operations into a single division in order to increase ad revenue and lower its exposure to the volatility in its gaming group.8 Moreover, according to Yang Yu, the head of Tencent Cloud Gaming Solution, the firm plans to rely on in-game advertising to monetize its cloud services. The average hourly spending among Chinese consumers in 2018 was Rmb2.2 ($0.30) compared with the Rmb5 ($0.70) cost of streaming games over the internet.9 Given their dominance, vast data resources on users, and strong relationships with advertisers, these firms will notably influence the industry’s move to design around an ad-based model.

With games becoming a viewable form of entertainment, live streaming and esports continue to further strengthen the interaction between game makers and advertisers. Activision Blizzard’s success with its Overwatch League (a professional esports league) relies on its ability to persuade large advertisers to commit to long-term, league-wide sponsorship deals. In its ambition to cater to a diverse, mainstream audience, Activision Blizzard faces the still-substantial challenge of creating a clear path to market for sponsors and advertisers. In an interview, one of firm’s senior ad executives acknowledged that, “gaming is new for a lot of advertisers, (so) we’ve really tried to make it as simple as possible.” In the same breath, however, the executive repeated the exact words that previously evidenced the disconnect between the creative and commercial sides when it comes to in-game ads, claiming that they “can even improve the concept of the game.”10 Even as the technology has advanced and audiences have evolved, some of the old ideas around the relationship between games and ads persist in the minds of decision-makers. Economic pressures and the popularity of video games incentivize top companies in the industry to formulate and explore innovative revenue models. Advertising presents a credible candidate for how interactive entertainment will generate money in the future.

Subscriptions

A second revenue model that recently has started to become viable involves audiences paying a recurring fee in exchange for access to a content selection. It emulates conventional models of, for instance, cable television and print publishing. With interactive entertainment having reached mainstream status, and the contemporary challenges of a global market saturated with digital content, video game subscriptions present an emerging approach to capture value.

We can distinguish among different types of recurrent revenue models. Subscriptions around specific titles or access to a single publisher’s catalog in exchange for a monthly fee have been around for quite some time. Many failed to attract large audiences, however, until the cost of online connectivity started to come down. We already discussed World of Warcraft and how it led the charge as online role-playing took off and successfully proved that millions of players were willing to pay a monthly fee for continued access. And even before that, there were also several casual PC-based services that had accomplished something similar. In the early 2000s, casual game maker Big Fish Games, for instance, offered packages for $4.95 a month or $29.95 annually in exchange for discounted access to premium downloadable games and a range of other content features. Audiences were coming online in droves even at a time when dial-up internet was still the norm. Access to a broad inventory of casual titles that were relatively small to download quickly proved popular with consumers. In combination with a curated content strategy, which included its best-seller series Mystery Case Files, Big Fish Games managed to grow revenue from $9 million in 2005 to $100 million in 2008. It managed to do so by distinguishing itself through an abundance of available content. Key to this approach was its aggressive content acquisition strategy. For years Big Fish Games was a top-tier sponsor of casual gaming conventions in order to set up hundreds of meetings with small creatives and acquire fresh content for the Big Fish catalogue.

Next, platform holders offer content subscriptions. Most obviously, it increases their earnings potential per customer. We previously covered PlayStation Plus and Xbox Live in the discussion of strategies that allowed the console market to sustain its presence as mobile became more popular. Hardware manufacturers successfully expanded their offering (and grew revenue) by upselling their user base. In addition to improving the return on investment made by selling hardware at a loss, capturing additional value through the sale of software by charging users an additional monthly fee is quite lucrative, because there are no incremental costs of goods. This is doubly important toward the end of a hardware life cycle, when market saturation sets in. Because gaming hardware resets every several years, consumers generally are aware that a new generation of better consoles is just around the corner. Existing owners will naturally become increasingly reluctant to invest in new games for an aging platform. Offering them a low-risk monthly commitment that provides access to a host of titles they otherwise would not have tried creates additional value for both sides.

For example, Microsoft’s release of the Game Pass, a monthly subscription of curated titles, successfully reinvigorated earnings for its gaming division. When first introduced, the program received positive reviews and Xbox owners readily adopted it.