Logica Capital commentary for the month ended September 2020, titled, “The New Cannot Be Born”, in which they discusses calculating the beta of a straddle.

Q2 2020 hedge fund letters, conferences and more

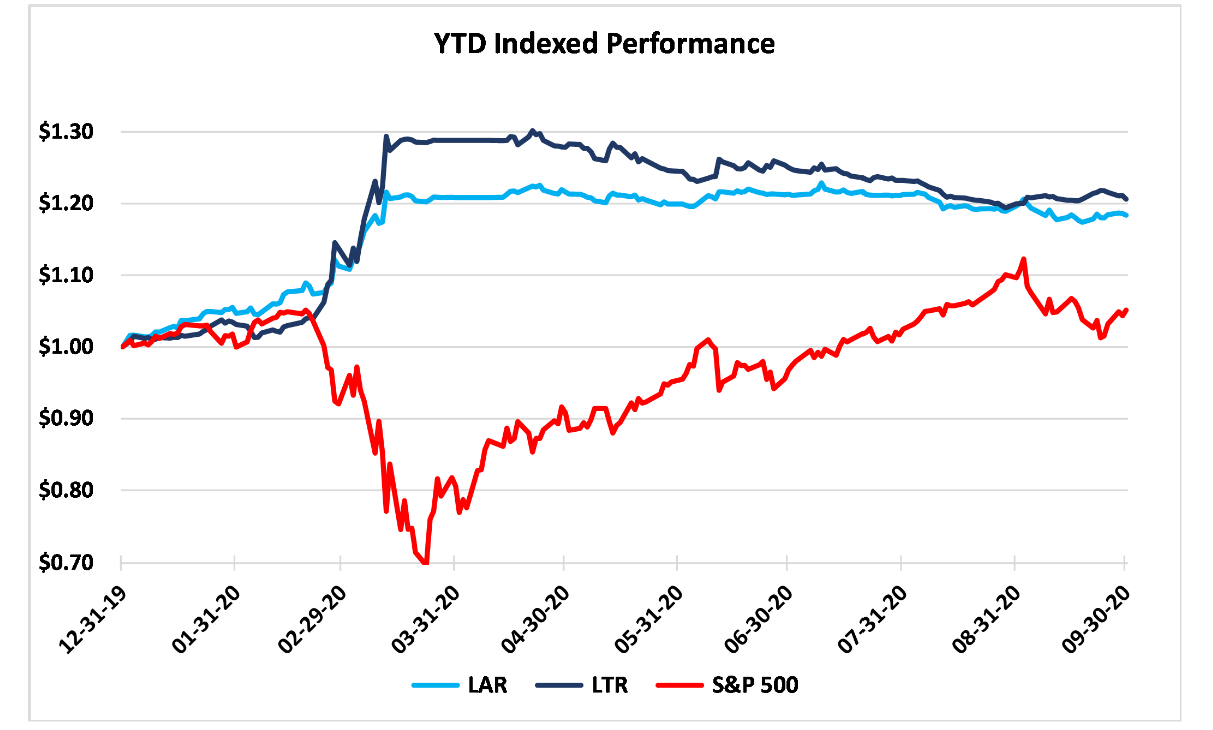

Logica Absolute Return - Up/Down Convexity - No Correlation

Logica Tail Risk - Max Downside Convexity - Negative Correlation

September 2020 Performance*

Logica Absolute Return -1.08%

Logica Tail Risk +0.67%

S&P 500 -4.13%

VIX -0.04 pts

Year To Date Performance*

Logica Absolute Return +18.4%

Logica Tail Risk +20.7%

S&P 500 -4.1%

*Returns are Gross of fees to illustrate strategy performance.

Logica Absolute Return Fund, LP returned -1.19% (net) for September 2020

“Try not to get worried, try not to turn on to

Problems that upset you, oh

Don't you know

Everything's alright, yes, everything's fine”

Andrew Lloyd Webber, 1971

A Different Kind of Loss

After a nearly 7% gain in August, markets were whipsawed by a reversal of many of the dynamics we discussed in our piece “Let’s Talk About Skew, Baby” and fell 4% even as the VIX remained unchanged. A simple model of what “should” have happened to VIX in such a market decline illustrates the extreme nature of the divergence:

This move, while frustrating, is much less concerning than the “caught offsides” dynamic of August. The unique characteristics of the market in August and September, with a “call gamma” induced squeeze upwards that subsequently unwound, has now largely played out, replaced by the dynamics of election uncertainty. If we breakdown the performance of the Absolute Return fund (LAR) for September versus the very positive experience in January to March 2020, the “only” difference was the responsiveness of S&P puts which suffered in September due to the lack of volatility (VIX) response and no real contribution from the macro overlay (EXX) strategy. Rates failed to contribute (more on this later) and, unlike January-March, gold was a no show. Graphing each of the components of LAR against the S&P, we can see that the driver of the difference in relative return was this deterioration in S&P put “beta” and the limited contribution from the macro overlay. We do not believe this is a permanent shift in the market; rather, it highlights that there is simply no fear at this juncture. The bid for protection is notably absent. This is highlighted by the positive performance of our Logica Tail Risk (LTR) strategy, which has roughly 2x the put load of LAR (relative to upcapture) and delivered results consistent with our model.

“I know what you're thinking: ‘Did he fire six shots or only five?’ Well, to tell you the truth, in all this excitement, I've kinda lost track myself. But being this is a .44 Magnum, the most powerful handgun in the world, and would blow your head clean off, you've got to ask yourself one question: 'Do I feel lucky?' Well, do you, punk?”

Clint Eastwood, 1971

The Decline In "Beta" Of A Straddle: Darkest Before the Storm

The decline in “beta” of a straddle is a fairly common occurrence. Calculating the beta of a straddle as the percent change in price of the straddle relative to the percent change in the S&P 500, we see that the average beta is roughly -2.9x. To our clients, this clearly defines the dynamics of the “non-recourse leverage” we refer to on a regular basis (the most you can lose is the premium paid) and it’s this negative coefficient that generates the hedging characteristics associated with a straddle as volatility expands in a down move driving straddle pricing higher.

However, at least four times in the past three years we have seen the beta turn modestly positive as either volatility rose as the S&P rose (call driven straddle performance) or volatility fell as the S&P fell. As the below chart illustrates, these often occur directly ahead of major S&P negative events. However, this condition in July 2020 gave way to a vicious rally in select single names as we described in “Let’s Talk About Skew, Baby”. Although we are not fans of direct historical comparison, this behavior looks suspiciously like Q4-2018 where a false signal with little volatility response (due to excessive use of Iron Condor option strategies) gave way to a steep correction as Boomers took the first of their 401K and IRA required minimum distributions. With flows into funds deteriorating, we will be watching these developments closely. As Dirty Harry might say, “Do you feel lucky?”

“The crisis consists precisely in the fact that the old is dying and the new cannot be born; in this interregnum a great variety of morbid symptoms appear.” - Antonio Gramsci, ~1930

De-Rating

The lack of contribution from the macro overlay (rates, gold and USD) is an increasingly well known phenomenon in markets and one that was discussed extensively in the Grant Williams’ Endgame podcast. The challenge largely sits at the foot of rates. With global risk-free rates now at record lows and offering much less diversification via negative correlation with equities than they did over the last decade, the value of this exposure for the goal of protection continues to decline.

This is a significant issue and can be illustrated in a variety of ways. The first approach is to decompose term premium to evaluate whether a premium is being charged for duration (due to funds being locked up at a fixed rate for a longer period of time) or whether premium is being paid for duration (as longer duration provides a hedge to lower future interest rates and/or portfolio protection). Structurally, in the US, we saw these term premiums turn negative in 2014 for 2 year rates (the peak of Jefferies’ David Zervos “Blues and Spoos”) and negative for 10s in Q4-2018 as Jerome Powell discovered that balance sheet reduction and rate hikes were slightly more interesting than watching paint dry.

This shift to paying for the benefits of duration is notable and makes perfect sense in the context of a “Fed Put”. If the Fed is going to protect balanced portfolios of bonds and equities by cutting rates whenever equities fall (or credit spreads widen which is functionally the same) then a bid for duration must emerge as the market begins to value this “put”. With this shift, we have entered truly novel territory. The Volcker regime of structurally high rates and a focus on inflation fighting finally died in Q4-2018 as it became consensus that the Fed would likely never be fighting inflation again. However, in the spring of 2020 another substantive break in the relationship occurred as bonds, particularly in Europe, failed to protect portfolios. The beta deteriorated sharply (became less negative) even as correlations remained stable. In fact, we are now having regular discussions with current and potential clients about the need to protect portfolios now that bonds have been found wanting. If bond yields shift negative, then not only will the efficacy of the hedge be in question, but the bonds themselves will offer negative yields creating a negative carry. In other words, bonds literally become puts (minus the guaranteed gamma!).

While we are thrilled to be having these conversations, the unfortunate reality is that nothing can take the place of bonds in this role. At Logica, we would conservatively estimate the capacity for our strategy is in the $2-5 billion range (heady growth from these levels). Bonds are measured in the trillions. At a beta of 0.15x, average for post GFC ex-Taper Tantrum, bonds could be used effectively to “hedge” equity risk without taking on excessive duration risk. However, if that beta has deteriorated as sharply as it appears to have, markets are faced with the unappealing risk that such protection is no longer available. Faced with this lack of protection, investors have three choices – find alternate hedges, reduce risk and accept lower return, or soldier on in the hopes of achieving returns despite the increased risk. With many institutional investors facing a mandate to deliver returns versus liabilities, we fear the answer may be the third.

This is certainly supported by the continued increase in multiples. In August, the forward P/E for the median company in the S&P 500 hit a record high. September’s retreat barely registers.

The relationship between available hedges via bonds and valuation is an intriguing one. While it is far from conclusive, there is evidence that supports this conclusion. Effectively, when bonds and equities have negative correlation, they become complementary assets and demand for each rises leading to higher valuations. When the correlations shift positive, they become substitutes and aggregate demand falls leading to lower valuations. Under this model, the level of rates matters much less than the direction. The data is intriguing when presented graphically.

With an activist Fed supporting the most negative correlations in history, it becomes an interesting question whether the Ides of March 2020 foretell the end to a chapter. At Logica, we have begun to aggressively research alternatives to a simple rate exposure in our macro overlay and have found some promising solutions that we look forward to deploying in the coming months. While it is unlikely that the solutions offer the simplicity and scale of risk-free bonds, we are excited to explore this interesting plot twist.

Business Update - Logica Absolute Return Offhsore Fund

Logica is targeting launch of the offshore version of the Logica Absolute Return Fund on November 1st. If you are an offshore eligible investor currently in our onshore vehicle, please reach out if you have interest in transferring. If you are a new investor interested in our offshore vehicle, please contact Steven Greenblatt for more information.

New Hire of Chief Compliance Officer

We are also excited to welcome Jeff Press as our new Chief Compliance Officer. Jeff joins us as part of a broader engagement with Compliance Risk Concepts as an outsourced compliance solution. Jeff is a Senior Regulatory Compliance Professional at CRC, with over 25 years of deep and varied expertise in Compliance, Risk and Operations programs from build out, to gap analysis, to lights on optimization and maturity. With expert knowledge of the practical application of financial services regulatory implementation and best practices, he formulates and executes a strategic vision that effectively demonstrates proper controls supporting business initiatives while helping to protect the enterprise from legal and regulatory risk. Jeff has broad industry experience in Operations, Risk, Compliance, Exams/Audit, and Governance from his time as a former CCO of large and small BDs and RIAs and has participated in the forensic compliance analysis at two high profile RIAs under SEC Receivership.

Logica Strategy Details

Note: We have comprehensive statistics and metrics available for our strategies, but only include a select few to highlight what we believe is our most valuable contribution to any larger portfolio.

- If you would like to learn more about our strategies, please reach out to Steven Greenblatt.

- If you would like to speak with Wayne or Mike on their views on Hedge Funds/Investing/Trading and trends they see shaping the industry, please contact Steven Greenblatt at [email protected] or 424-652-9520.

Follow Wayne on Twitter @WayneHimelsein

Follow Michael on Twitter @ProfPlum99

Logica Absolute Return

2015-2019 stats & grid, reconstitution of live sub-strategies

2005 to present growth of $1000 chart, simulation

Jan 2020 live with partner capital

Logica Tail Risk

2015-2019 stats & grid, reconstitution of live sub-strategies

2005 to present growth of $1000 chart, simulation

Jan 2020 live with partner capital

Endnotes

- “Navigating Constraints: The Evolution of Federal Reserve Monetary Policy 1935-1959” https://www.dallasfed.org/-/media/documents/institute/wpapers/2014/0205.pdf

- “When Did the FOMC Begin Targeting the Federal Funds Rate? What the Verbatim Transcripts Tell Us”, https://www.jstor.org/stable/4123043?seq=1

- Robert Shiller Online Data, https://www.axios.com/statistics-crisis-coronavirus-unemployment-ad4d88ad-65f9-474f-920f-a056d147c076.html

- Yardeni Research, Oct 7, 2020 https://www.yardeni.com/pub/stockmktperatio.pdf

- Grant Williams, https://podcasts.apple.com/us/podcast/the-end-game-ep-3-mike-green/id1508585135?i=1000483139066

See the full letter here.