Berkshire Hathaway Stocks or BRK stock, traded as BRK.A and BRK.B where 1,500 BRK.B equal one BRK.A, is undervalued when compared to the market. So in this Berkshire Hathaway stock valuation exercise we compare the actual market capitalization of Berkshire with what would be the likely market value of Berkshire Hathaway’s holdings if traded like public companies.

Q2 2020 hedge fund letters, conferences and more

When it comes to Berkshire and Warren Buffett, the key not the stock price, the performance or comparison, the key is the investment style. I believe how Buffett is investing, which is the opposite than corporate America, is a much better way to invest because it is focused long-term. There is no crazy leverage, Berkshire doesn't do crazy buybacks and there is the cash pile ready to take action when all others fail.

The funny thing is that Berkshire Hathaway is trading at a 40% discount to the market while being a better fundamental investment from all perspectives. You see how what fits your portfolio.

Berkshire Hathaway Stock Under Valuation - A Stock To Buy

Transcript

Good day fellow investors. In this video, we're going to discuss Berkshire Hathaway, its 500 billion market capitalization and compare it to the sum of parts value, which is significantly higher than what the market is valuing Berkshire now, I have recently analysed all railroad stocks, and I have done a video on that. So you can check that. And in that analysis, I said, Okay, which is another class one railroads, that's Burlington, Northern Santa Fe, that Warren Buffett purchased in 2009. And then I went to the financials to the financial statements, and two things struck me. First, the lower debt that Burlington Northern has compared to all other railroads, and that the market value of Burlington, with this free cash flow wheel, the free percent that most other railroads have, would be 200 million that would make 40% of Berkshires market capitalization, just the one railroad that makes one sixth of profits. That's unlogical. That's market irrationality.

And that's what we're going to discuss in this video by analysing all the holdings of Berkshires part by part, seeing what would be a market valuation given the average market valuations pricings and then give a sum of parts valuation of Berkshire that puts another perspective on the undervaluation. The quality that Berkshire is, by the way, disclaimer, I am long Berkshire, I love Buffett. So that might be a bias on my side. But let's start with the analysis. So this is what I have done, I have compared everything in the railroad sector. And this goes even to 2.6%. Seven now. But everage debt to cash flows are six for the listed railroads that to cash flows for Burlington, Northern Santa Fe, I first thought it was zero, but these have some debt in the structure there. So 3.5 times debt to cash flows. And if I would put it on a free percent cash flow wheel that's average for other railroad stocks, the market cap would be 198 billion on the 5.9 billion free cash flows.

Buffett And Taleb

And this is extremely significant because I was just listening to Nassim Taleb recent Bloomberg interview on make a summary and discussion on that on Friday. So please subscribe because it's very interesting. But what also was very interesting was not seems coherency in thoughts with Warren Buffett, when Nassim was a trader, the saying was take all the risks you can but make sure that you are there tomorrow. So take all the risks, but keep alive stay in business. And that's exactly what Warren Buffett is doing with his railroads. No matter what happens, given the low debt, lower that then other railroads. Buffett is pretty sure that his railroad which will survive whatever comes at it. All the other railroads are forcing buybacks, lowering their cash flows to the minimum amount and increasing that higher, higher and higher. Same, the same was done by airlines, for example. And that's something that shows really, OK, Buffett way of thinking value long term, slow and steady versus the market. And Buffett's idea is now undervalued. And that's peculiar or not, that's the standard, but Buffett is on the top five richest person in the world. Everything else is mumbo jumbo.

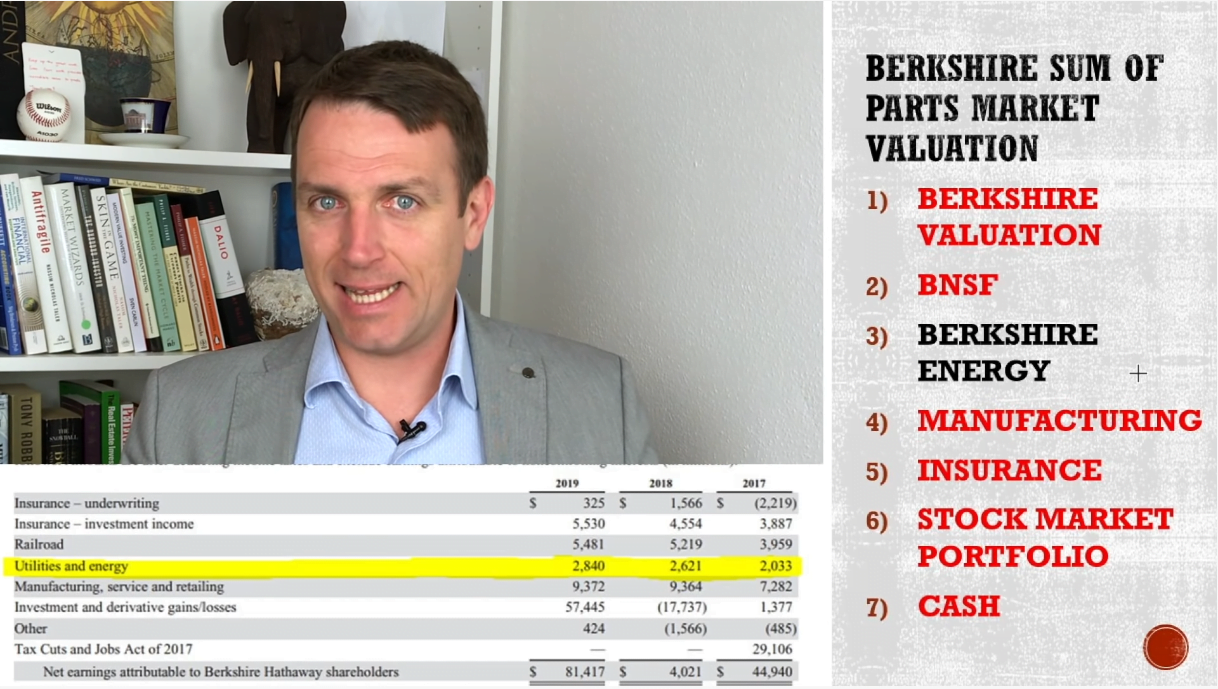

And then again, something that Nasim said nobody is bigger than the market. The railroads have very, very strong buybacks, spending on buybacks, more money that what they make, and yes, railroad stocks have outperformed the s&p 500 over the last five years, over the last 10 years Berkshire i don't think did that over the last 10 years. But remember nobody's bigger than the market, so sooner or later if you do financial engineering to beat the market it's unlikely you will do that for longer. So railroad investors get out and buy Berkshire. And here is the sum of parts valuation we'll go through each one try to keep in mind the score over time and then at the end of the video I'll show you the right value and then you'll see how the market is wrong and you'll see whether you will be wrong too. Because it's a lot to keep in mind each segment each part of Berkshire and the correct valuation. Let's start with this game and let me know in the comments if you got it right at the end.

BNSF

So we already mentioned Burlington Northern Santa Fe earnings 5.4 billion in 2019 i'm going to use 2019 as a benchmark year because i think kovid will pass sooner or later so all businesses will return to normal and will grow alongside the american economy in the future i have looked at the statements of burlington northern and i see that they have paid out almost 6 billion which i'll consider free cash flows they made 9.7 billion in operating cash flows had 3.6 billion of capital expenditures and what's left has been paid out to berkshire so let's say 6 billion free cash flow they have some debt 23 billion okay with the 4.6 interest rate still lower than other companies and when we compare it to others to the free cash flow wheel they have correct this canadian pacific is actually 2.4 so even lower 3 free cash flow year 6 billion 200 billion market valuation plus it's easy to borrow more plus it is a financial for fortress so if any of these guys gets in trouble burlington will be the ba the one buying their assets very interesting typical buffett style.

Berkshire Hathaway Energy

After railroads, a business that Buffett loves really much is Berkshire Hathaway energy. And the earnings there have been 2 billion then grow and now they are 2.8 billion for 2019. The earnings there are growing at 10% per year, because Buffett is reinvesting all the earnings. This is very important. Keep it in mind. You'll see later the comparison, reinvesting all the earnings for growth and all the earnings growth is based on that equity reinvestment where Berkshire Hathaway Energy doesn't pay dividends to Berkshire. And that's the key slow growth for Berkshire Hathaway Energy but still growth, which is much better than other companies. You'll see in a moment on a note on Berkshire Hathaway Energy. So a lot of investments in solar, wind, growth, mid American, so really good company like most others, Berkshire Hathaway companies, and their vision is typical Buffett for the next 100 years of providing energy. The debt to assets, if we look at the balance sheet is just 25%. The profits 2.8 billion approximately 10% on the shareholders equity there 2.8 billion on 29 billion shareholders equity likely grow also over the year slow and steady. And the management has said that they have investment opportunities for eight 9% 10% returns on equity invested. This is what Buffett does. And really remember this debt to assets ratio of 25%. If I compare this to other energy companies, the top five in the Energy US ETF then we can see that the debt to assets ratios is insane for Berkshire Hathaway Energy. So really, really low. And everybody else has huge debt to assets ratio. So liabilities, and we know how liabilities backfire. If I look at net income, Berkshire is somewhere there. It's not that these guys are much better. And on the growth just NextEra energy has 10% growth. And we'll discuss that also in a moment alongside similarly similarly as Berkshire Hathaway Energy if I compare the market capitalizations, depending on the price earnings ratio, but if I take a 25 price earnings ratio for Berkshire Hathaway energy, which should be the average, it has grown, it has much less the risk much less that so the market capitalization is 70 billion. It would be a public company not owned under the Berkshire. Umbrella.

Talking about NextEra Energy this is the NextEra stock chart this is the Enron energy company stock chart from the 1990s, any similarities? Well I’m not saying there is fraud with NextEra I’m just saying something that also Nassim Taleb has just explained there is no growth based on debt. So NextEra has the same growth rate as Berkshire Hathaway Energy but Berkshire Hathaway Energy typical Buffett's style doesn't grow on debt. And another thing that Buffett agrees with Nassim Taleb there is no growth based on that if you grow on debt it's no growth very important to note let's compare really NextEra and Berkshire Hathaway completely opposite as I said really low debt for Berkshire Hathaway Energy 8.5 billion lowered even they keep the equity invested and grow on that but if I compare it to NextEra Energy their profits over 2019 were 2.5 billion their assets over the year at the end of 2018 grew 15 billion so Berkshire grows on the assets on the earnings they make that's it no more debt no risk slow and steady NextEra has earnings of 2.5 billion and they managed to grow at 15 billion if this up ends up another Enron. Berkshire Hathaway will have a lot more of buying to do and this is perhaps the reason why Buffett has such a huge cash pile that's also part of the valuation that we'll discuss later and he's just waiting for all of those houses of cards out there you grow assets in seven times more than what is your net earnings and that's something that works until it doesn't when it stops working Buffett comes in and Buffett starts buying like he did in 2009 with Burlington Northern banks and whatever that's warren Buffett his business is set up to work forever most other businesses in corporate America are set up to push the stock price higher until it goes until the party goes and that's something to keep in mind also when valuing Berkshire Hathaway the market doesn't like it the market wants stocks to go higher you want stocks to go higher Berkshire is not a stock that's pushed higher therefore it's valuable therefore it's undervalued and therefore it makes a better investment than 98% of other corporate America. And even Nassim Taleb agrees with all the fundamentals of Warren Buffett, which we'll discuss in next video, so please subscribe to this channel. This is where you get the long term value. So on a valuation 70 billion to Berkshire Hathaway Energy.

Manufacturing

Then we have all the manufacturing service and retailing businesses. We have Clayton Homes, Duracell, Precision Castparts, a lot of busy businesses, Nebraska Furniture Mart, so all these businesses make 9.3 billion in earnings, if I attach a price earnings ratio of 20, which should be okay for these businesses. It's a diversification on America practically price earnings ratio of 20. I think it's fair. So the valuation 180 billion for all the manufacturing businesses out there of Berkshire.

Insurance

Then we have insurance and Berkshire Hathaway is one of the biggest insurers out there. And this valuation might surprise you. Because insurance, the underwriting part, it's the focus is not on making profit. And Buffett says yes, they have made 25-28 billion in profits over the last 15 years. But that's not the goal. The goal is to create the float, therefore, it's worth to sacrifice the profits over the last year. It was just a breakeven. So let's not calculate this as value. Let's just calculate the value in the stock market portfolio which is under the insurance arm and therefore put a low valuation on the insurance. If we look at MetLife, Prudential it's what 24 billion market cap, MetLife 43 billion so not something crazy there. I'm going to put, let's say a valuation of 25 billion on the insurance part because the value is in the float in the stocks and the value of the stock market portfolio. That's very easy. We have here, CNBC with the Berkshire stock market portfolio tracker 227 million, 597 million. Oh, very easy value, remember 227 million. Sorry. And this is very interesting. If you go to Berkshire's annual letter to shareholders, you see that they don't see that the stock prices going up and down. They see this stock holdings as an agglomeration of businesses that have a 20% return on equity. And that's what they are focused on. They are business owners, not business traders, not stock market traders.

Berkshire Cash Pile

And that's always the main message with Buffett. And that's why I also think he has immense value, because those businesses giving 20% return on equity invested, and therefore it's likely they're going to compound for the very, very long term, but the market 227 billion, let's take that as a value. Then another discussion on cash, these are the assets. And on that balance sheet, you have 125 137 million in let's say cash or cash equivalents. If I deduct all the liabilities for earning potential insurance liabilities, total 87 billion in debt 65 billion in tax liabilities, I get to equity of 428 billion, deduct the stock market valuation that we already calculated, I'm down to 180 billion other liabilities potential, we can assume that the 143 billion in cash there can be considered as value because Buffett can do whatever he wants with that even pay a dividend. Yes, I said it Sorry about that. I know you don't want to do that. But I said it.

Berkshire Hathaway Stock Valuation

So the total market valuation perspective on Berkshire Hathaway would be $845 million. Compare that to the market valuation current of 514 billion and you see a huge discrepancy. Why do you see a discrepancy? Because Warren Buffett isn't crazy about getting leverage to do buybacks like most of corporate America, that pushes stock prices higher, higher and higher higher valuations, Buffett doesn't do it, Buffett stock will not go crazy up like many others can go therefore there is not so much interest, but investing is about the long term. What are is your horizon 10 2030 years can you sell if a company is doing buybacks to take advantage of that you have to sell at some point, the buyback party will end at some point. And then you have to be out how long it will last? We don't know Buffett is not playing that game, Buffett is playing the business game that will surely be there over the next 1020 years. And the market is actually punishing him because of that, as Buffett say price is what you pay value is what you get.

In this case with Berkshire. If you pay the price of 514 billion, you get more value than what you are actually paying. Because Berkshire is Berkshire. And the question is what kind of assets do you want in your portfolio? What kind of businesses? What kind of investing mindset? You want the long term investing mindset that is a financial fortress that renounces taking leverage to chase returns to look like next year I energy, but you want safety you want certainty that in 20 years, they will be a little bit bigger as others don't know where next year energy will go bankrupt or not. But when some of those playing that game goes bankrupt. Warren Buffett comes in with 9% convertible notes to help them that's the kind of strategy you have to see and see what fits your portfolio.

So please subscribe if you enjoyed this analysis. On Friday we'll discuss a more economical discussion with Nassim Taleb view on the economy, the main investment risks, how a fits with Warren Buffett how his thoughts and fit what Warren Buffett is actually doing very, very surprising. As I said, I'm long a little bit on Berkshire always watch it. I cover it on my stock market research platform. And this is always like to see it's always too good to keep the right mindset. And you get that by just looking at what Warren Buffett is doing, is still doing has been doing for the last 70 years. And that has actually worked for the last 70 years. If you want to check anything that I do, please check everything in the links below from my modern value investing book to my research where I analyse different companies, commodities, emerging markets, etc. If you're interested in it, you might find some value. Thank you for subscribing. We are reaching almost 100,000 hopefully soon. Thank you for that. I'm looking forward to your comments, and I'll see you in the next video on Friday.