Kerrisdale Capital is short shares of AtriCure, Inc.

Q2 2020 hedge fund letters, conferences and more

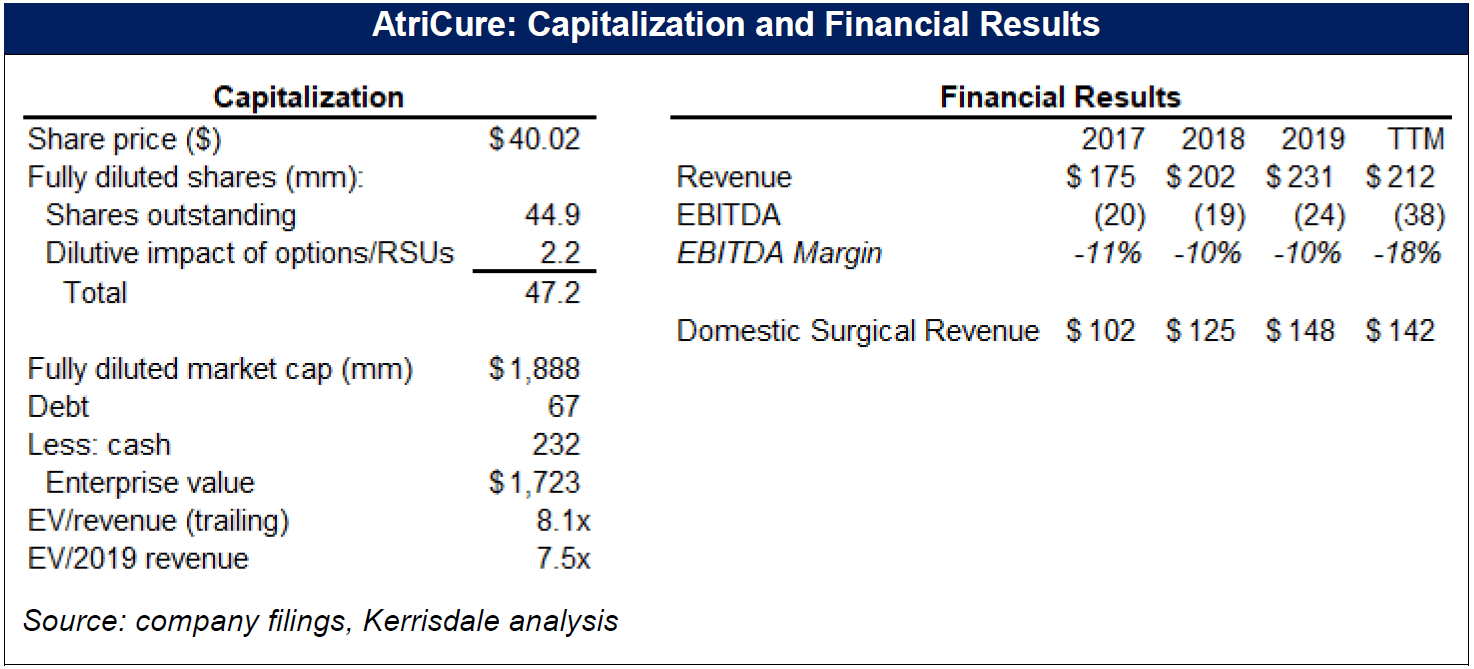

We are short shares of AtriCure, a $1.9bn medical device company that manufactures and sells ablation equipment used in the surgical treatment of atrial fibrillation (AF). At about 7x forward revenues, AtriCure’s valuation implies that the company’s outlook is brighter than at any point in the last decade. But with the company’s core surgical ablation market almost completely saturated, and the relentless improvements in catheter ablation technology accelerating, AtriCure is facing both rapidly decelerating revenue growth and the threat of technological obsolescence, simultaneously.

AtriCure's Reliance On Surgical Cardiac Ablation Procedures

At the root of AtriCure’s impending difficulties is the company’s reliance on surgical cardiac ablation procedures, which underlie roughly 80% of the company’s revenue. The overwhelming majority (over 90%) of these procedures are performed concomitantly with open-heart surgery that patients undergo irrespective of their AF – the chest is already open, so the surgeon takes some extra time to ablate the cardiac structures from which the AF originates. The problem for AtriCure is that, despite demographic tailwinds, the absolute number of open-heart surgeries has stagnated over the past decade as less invasive procedures, and earlier medical intervention, have successfully reduced the need for risky surgery. In stark contrast to AtriCure’s claims, about a tenth of these procedures are performed on patients with preoperative AF, and the proportion of these procedures involving a concomitant ablation has steadily doubled to about 80% over the last decade, leaving little room for growth through further penetration. AtriCure’s inability to turn a profit, even as it dominates an almost fully penetrated market, suggests that its core business is simply structurally unprofitable.

With the plateauing of surgical ablation growth in clear sight, AtriCure has been making a strong push for its “minimally invasive” Convergent procedure. While surgical ablation is usually restricted to patients already undergoing open-heart surgery, Convergent’s minimally invasive nature aims to enable most of the benefits of surgical ablation on a stand-alone basis for all patients with persistent AF. Investor optimism about this market expansion has led to the explosion in AtriCure’s valuation.

But Convergent will fail because it doesn’t consider the role of electrophysiologists at the center of AF treatment. For AtriCure’s gambit to succeed, EPs would have to refer their patients for a Convergent procedure, but they already perform catheter ablations on an outpatient basis, and without the risks of surgery. AtriCure claims that Convergent is far more effective for treating persistent AF than catheter ablation, but the EPs with whom we spoke found that claim laughable. The accelerating improvements in catheter ablation technology over the past decade have made it much easier for EPs to non-invasively create all the same cardiac lesions as Convergent. Asking EPs to split an ablation with a surgeon is tantamount to telling them they’re not skilled enough to do it on their own. We expect that to work out very poorly for AtriCure.

Meanwhile, new technologies, particularly pulsed field ablation (PFA) and real-time electrical mapping, are set to dramatically advance catheter ablation. PFA creates lesions rapidly and precisely without any of the safety issues involved in thermal cardiac tissue ablation, while real-time cardiac mapping allows EPs to identify and eliminate sources of AF with much greater precision. The upshot is that catheter ablation is set to become safer, faster and more effective than ever, making any stand-alone surgical ablation – including Convergent – completely obsolete, while also encroaching on AtriCure’s core surgical business. As Convergent fails and surgical ablation gives way to less invasive treatment modalities, we expect that profits will continue to remain elusive and that AtriCure’s share price will suffer some ablation of its own.

I. Investment Highlights

AtriCure will fail in its attempt to expand the surgical ablation market through the promotion of the Convergent procedure. AtriCure dominates the market for surgical ablation equipment used to treat atrial fibrillation (AF). Surgical ablation is generally performed by cardiac surgeons as an add-on to open-heart surgery at the end of the procedure. If a patient suffering AF undergoes bypass surgery, for example, the surgeon will take the opportunity of an open chest to ablate the cardiac tissue from which AF arrhythmias emanate. In almost every one of these procedures, the surgeon will also clip the patient’s left atrial appendage (LAA), the source of over 90% of AF-related strokes, using AtriCure’s AtriClip. Performing a concomitant ablation has become the standard of care for patients with preoperative AF and, as we discuss at length below, the proportion of these patients undergoing ablation during their surgeries has little room for further growth.

AtriCure has long understood that this growth deceleration would eventually arrive, and it has long attempted to preempt it with a simple strategy: turn surgical ablation into a stand-alone procedure. Restricting surgical ablation to those who are already undergoing open-heart surgery severely limits the addressable market. On an annual basis, there are over five times as many patients suffering from AF that could benefit from an ablation as there are AF patients who undergo open-heart surgery.1

The problem with surgical ablation though is the surgery. From a risk/benefit standpoint, it’s difficult for an EP to recommend cutting open a person’s chest in order to fix (or attempt to fix) a chronic condition that’s generally managed conservatively with medication, lifestyle adjustments, or cardioversion. At a certain degree of severity, an EP will treat AF by performing an ablation exclusively from the inside of the heart (endocardium) with a catheter that is inserted into the patient through the femoral veins. But stand-alone surgical ablation has remained incredibly rare. AtriCure has long tried to change that by trying to advance a variety of “minimally invasive” surgical ablation procedures, which would theoretically alleviate some of the risks of open-heart surgery and minimize recovery time for the patient. Each of these successive attempts over the course of the last decade has been quietly abandoned by AtriCure with little explanation, though it’s clear that the complication rates in trials of the procedures were unacceptably high – higher even than ablation complication rates in open-heart procedures – and thus wouldn’t meet the bar for device-approval by the FDA.

Convergent, the minimally invasive procedure currently being touted by AtriCure, has avoided the safety issues that have plagued the company’s previous attempts. But like those failed procedures, its minimally invasive nature poses significant limitations. In the first half of the Convergent procedure, a surgeon gains access to the exterior of the heart (epicardium) by way of a small abdominal incision through which a tubular ablation device is inserted. The small incision means the device can only access a small section of cardiac tissue for ablation – the posterior left atrial wall – leaving the pulmonary veins, which are the most frequent trigger of AF, untouched. As a result, Convergent requires a second procedure – a standard endocardial catheter ablation, performed by an EP, to isolate the pulmonary veins, which are the most frequent trigger source of AF.

This “hybrid” approach to stand-alone ablation – combining a minimally invasive epicardial ablation with a standard endocardial catheter ablation – made some sense when the concept was first introduced about ten years ago. Pulmonary vein isolation (PVI) via catheter ablation was just being perfected, and it wasn’t effective in most patients suffering from persistent AF, in which other areas of the heart besides the pulmonary veins also triggered arrhythmias. The addition of a minimally invasive procedure to ablate some of those other sources – as Convergent does with the posterior wall – would improve the efficacy of ablation for these patients.

Read the full report here by Kerrisdale Capital