Bonhoeffer Fund commentary for the second quarter ended July 2020, providing a case study on Antero Midstream Corp (NYSE:AM).

Q2 2020 hedge fund letters, conferences and more

Dear Partner,

The Bonhoeffer Fund returned 21.7% net of fees in the second quarter of 2020. Given the unique portfolio Bonhoeffer manages, I have struggled to find an appropriate benchmark but have determined that the DFA International Small Cap Value Fund offers the closest representative comparison to Bonhoeffer. Our year-to-date performance is down 19.3% net of fees, compared to DFA International Small Cap Value Fund which is down 20.8%. As of June 30, 2020, our securities have an average earnings/free cash flow yield of 24.4% and an average EV/EBITDA of 3.9. The DFA International Small Cap Value Fund has an average earning yield of 8.9%. The difference between the portfolio’s market valuation and my estimate of intrinsic value is still large (greater than 100%). I remain confident that the gap will close over time and continue to monitor each holding accordingly.

Bonhoeffer Fund Portfolio Overview

Bonhoeffer’s investments have not changed significantly in the last quarter. Our largest country exposures include: South Korea, Italy, South Africa, Hong Kong, United Kingdom, and Philippines. The largest industry exposures include: distribution, consumer products, telecom, and transaction processing.

Since my last letter, we have added a position in a past holding that is going through a holding company transaction similar to Lotte last year. In these holding company transactions, minority equity stakes held by operating companies (OpCos) are aggregated together in a new holding company (HoldCo) and spun out to existing operating firm shareholders. The motivation behind these transactions is to allow heirs of company founders to gain liquidity by selling HoldCo shares to pay estate taxes versus OpCos, where if they were to sell shares they may lose control. So in the end, the shareholders of the OpCo receive shares of the new OpCo and HoldCo. The preferred shares are also included in these transactions.

As mentioned in previous reports, we hold many Korean preferred stocks that sell at substantial discounts to the common shares due to the lack of voting rights and liquidity (however, preferred shares do have higher dividends). Since inception, we have seen more of these preferred shares at a premium to the common and, for some of the more liquid names (like Samsung Electronics), the discounts have narrowed to 10 to 15%.

Bonhoeffer began as a special situations fund investing in compound mispricings, mischaracterized firms, and public LBOs. Over time, modestly priced growth firms have been added to the mix (e.g., Ashtead and Cambria). Many of the special situations were found overseas and had a tilt towards smaller capitalization value firms. The COVID-19 pandemic had an adverse impact on the share prices of most of our small cap value names. Value realization is still in progress in many of these names but the longer-term trends that made them interesting in the first place continue. As a way to organize the portfolio for investors, I will be reporting on holdings by special situation type (i.e., compound mispricing and public LBO) and theme.

Compound Mispricings (50% of Portfolio; Quarterly Average Performance +19%)

These securities include the Korean preferred stocks, the non-voting share of Buzzi, Telecom Italia, and Wilh. Wilhelmsen and some HoldCos. The thesis for the closing of the voting, non-voting, and holding company gap is better governance and liquidity and corporate actions, like spin-offs, sales, or holding company transactions. Telecom Italia’s discount (in Italy) has disappeared over our holding period, but further unlocking of value is happening with a combination of its Italian telecom networks with Enel and an activist on the board of directors, Elliot Management. Buzzi’s discount (also in Italy) still remains large at 43%, making the already favorable growth/valuation of Buzzi even more enticing. Buzzi’s management is focused on creating shareholder value in its primary markets (US/Mexico and Europe) with expanded investments in Brazil and should do well with increased infrastructure spending in the U.

The Korean preferred discounts in our portfolio are still large (20% to 37%). The trends of better governance and liquidity have reduced the discount in names like Samsung Electronics, and more preferred names trade at a premium to common shares. We are also involved in a Korean HoldCo transaction which should provide a catalyst over the next six to 12 months.

Another group includes multiple HoldCo telecommunications firms such as KT—which should get a boost from its real estate holdings and the implementation of 5G in Korea—or Lotte Chilsung, with its prime land holding (in Seoul’s Gangnam district) and expansion into alcoholic beverages. We also have a few growing net-nets in this group of securities.

Public LBOs (26% of Portfolio; Quarterly Average Performance +48%)

This includes our broadcast TV franchises, leasing and roll-on/roll-off (RORO) shipping, and our natural gas pipeline firms. One trend in these levered firms is the increasing spread between bond yields and the firms’ free cash flow yield. An example is Gray Television, whose FCF yield increased to 24% at June 30, 2020, from 19% at year-end, while its debt yield has increased to 6% from 3% with the bond/equity FCF spread increasing from 16% to 18%. What is unusual today is that the bond yields have returned to 3%, but the free cash flow yield has remained unchanged. Our natural gas pipelines have similarly large debt/DCF yields, as described in detail below in our case study.

Distribution Theme (32% of Portfolio; Quarterly Performance +42%)

This includes our holdings of car and branded capital equipment dealerships, online shopping, and capital equipment leasing firms. One of the main KPIs for dealerships and shopping is inventory turns. We own some of the highest inventory turn dealerships in each market and around the world. These firms have done a better job of matching customer to product than their domestic competitors and thus have a longer-term competitive advantage.

Telecom/Transaction Processing Theme (28% of Portfolio; Quarterly Performance +1%)

This includes our transaction processing and telecom firms. Despite continued expected performance, these firms have lagged in the rebound. The increasing use of transaction processing in our firms’ markets and the roll-out of 5G will provide growth opportunities. Given that most of these firms are holding companies and have multiple components of value (including real estate), the timeline for realization may be longer than for other firms.

Consumer Product Theme (21% of Portfolio; Quarterly Performance +27%)

This includes our holdings of food, consumer product, tire, and beverage firms. The defensive nature of these firms has led to better-than-average performance. We had one take-out offer in the quarter for a beverage firm at a value considerably below intrinsic value. We continue to hold this firm’s equity.

Real Estate/Construction Theme (19% of Portfolio; Quarterly Performance +19%)

This includes our holdings of real estate, residential construction, and cement firms. One area of focus is Hong Kong/China real estate which has been rocked by both the coronavirus and the actions of the Chinese Communist Party in Hong Kong. Despite these actions, the group has performed better than the index. In my opinion, the pricing of our real estate holdings includes both a recession in Hong Kong and a communist takeover of Hong Kong. If the result is better than this, then these stocks should add, instead of detract, from fund performance going forward.

Age of Abundance

We are in the age of abundance. A recent book written by Laurence Siegel, Fewer, Richer, Greener,1 outlines the history and trends that underlie how we got here and where we are going. This is a nice follow-on to the history book we provided shareholders in December, The Birth of Plenty,2 as it outlines the key trends in more detail. The main areas of increased abundance include: time and human capital (increased life expectancy), food, cities, education, freedom, energy, and dematerialization. Each of these areas of abundance, in combination with lower distribution costs, will create winners and losers.

How we think about investments will change as a result of this abundance, as history has been a history of shortages (with those who had what was in short supply generating excess profits). In a shortage world, the distributors become the “gatekeepers” between customers and products. Today, in contrast, if the world has abundance, then those who help or search for this abundance are in key positions in the abundance value chain. Today, these firms (like Google, Netflix, and Amazon) are valued very highly. However, looking forward, once a person finds what they want, the incremental value of search declines. What may evolve is search for new items (where curation is important) but with direct customer connection for recurring purchases. For some activities, such as research, search is the primary action but, for many activities, search is a one-time activity that facilitates recurring purchases.

Disruption

The key disruption today is the availability of additional products and services via lower-cost distribution channels. One result is the age of abundance described above. The cost of distribution has declined, as more distribution networks have been built out by firms such as Amazon, JD.com, and Wayfair, in addition to the traditional nationwide networks of Walmart, Target, Federal Express, UPS, and US Postal Services.

In the 20th century, product distribution was primarily via physical bricks and mortar shelf space. Shelf space was a scarce commodity, so the product makers would compete for the limited shelf space. The focus of distributors/retailers is being a “gatekeeper” between customers and producers. With internet distribution, shelf space has become infinite, so the scarce resource has flipped from supply aggregation (shelf space) to demand aggregation. Those who have aggregated demand can provide a customer base to a supplier and thus lower the supplier’s customer acquisition cost. In either case, a KPI for distribution is inventory turnover, as this illustrates the velocity of transactions or how fast retailers/distributors can match product to customer.

Investing Tools

The evolution of investing tools has also followed the trend of scientific progress of tools over time. Static snapshots of a firm’s current position are what early Graham analysis was composed of (discounts to net asset value and looking at relative multiples), similar to statics analysis by ancient Greeks. Dynamic (velocity) analysis of firm value was introduced by Graham and refined by Buffett with the idea of buying growing businesses at non-growth prices. In science, this advancement was formulated by Newton in his thoughts on Newtonian mechanics. Acceleration analysis is the current stage of firm value tool development, using frameworks such as unit economics and scaling to accelerate the velocity of transactions. This is analogous to relativity in the science world as formulated by Einstein. As in science, each preceding set of tools is a specialized case of the latter.

I am always looking for new tools to examine businesses’ competitive dynamics. In reviewing the approaches of more acceleration-analysis-based managers (such as ShawSpring, managed by Dennis Hong and his team), I have found some interesting types of analysis that we will be applying to our holdings going forward, including identifying and tracking KPIs and a closer examination of a firm’s supplier, employee and customer ecosystem.

Conclusion

As always, if you would like to discuss any of the philosophies or investments in deeper detail, then please do not hesitate to reach out. Until next quarter, thank you for your confidence in our work and have a safe and restful remainder of the summer season.

Warm Regards,

Keith D. Smith, CFA

Case Study: Antero Midstream (AM)

Antero Midstream (AM) is a natural gas pipeline firm located in the United States. AM provides the gathering and processing for Antero Resources (AR), a large upstream natural gas firm with a focus on the Marcellus Basin. AM also provides and treats water to AR for fracking and has a joint venture with MPLX, which fractionates and distributes natural gas liquids (NGLs). The Marcellus Basin is the lowest-cost basin in the US ($1.77 to $2.43/mcfe wellhead breakeven price) excluding those basins that generate associated gas from oil drilling like the Permian and Eagle Ford basins. AM’s current gas wellhead breakeven is $2.14/mcfe, a figure that has been declining by 5% per year over the last two years.

Key points of the Antero Midstream thesis include: (1) gas prices received by AR will be supported by a decline in natural gas supply (EIA expects long-term prices of $2.75 to $3.75/mcfe) both from the reduction in associated gas production from the fracking glut gone bust and the bankruptcy of large natural gas producers such as Chesapeake; (2) a 5% yearly decline in production costs; (3) an increasing liquified natural gas (LNG) demand of about 4% per year; and (4) AM being at an inflection point in pipeline development, having already completed the backbone and infrastructure (investing in success-based flexible connections to the backbone still remains). This inflection will result in robust free cash flows going forward. Evidence of AM’s density economics can be seen in AM’s high EBITA margins. AM has amongst the higher EBITA margins amongst gathering and processing pipelines at 55% and one of the best returns on equity (17%).

Antero Midstream’s management has a returns-oriented framework (only building where there are acceptable RoICs), having delivered an average return on invested capital of 12% over the past six years, ranging from 9% to 14% per year. With a 2019 debt level of 53% debt/invested capital, that results in a return on equity of 17%. Management is expecting a return on investment capital of 14 to 16% in 2020, incorporating the revised fee schedule negotiated with AR earlier this year.

Antero Midstream is compensated based upon a fixed fee per volume transported. The gathering and processing (G&P) contracts have a remaining life of more than 15 years with inflation escalators. AM’s utilization rates for its G&P pipelines have increased from 65% in 2014, to 89% in Q1 2020, and the MPLX joint venture (JV) has had utilization rates that have been about 95% since 2017. A majority of the infrastructure costs have been incurred for the G&P, water, and JV projects, and they are expecting to be generating high levels of free cash flows going forward. This is why the dividend rate has not been cut despite the low coverage ratio (1.03). AM’s debt level of 3.7x EBITDA is lower than comparable G&P pipelines.

Management expects 9% organic gas production volume (7% if the recent OTTI royalty in included) in 2020. As a result of the renegotiated fees, Antero Midstream’s revenues are expected to decline by 12% in 2020 but are expected to increase by 8% in 2021, as a full year of the new fees are reflected in revenues and production growth continues. According to the US Energy Information Administration, the overall US natural gas market demand is expected to grow by 2% per year, and the NGL market demand to grow by 4% per year from 2020 to 2024.

A significant factor in the decline of natural gas pricing has been the associated gas production from oil production, primarily in the Permian, Eagle Ford, SCOOP/STACK, and DJ Niobrara. The gas production from some of these oil fields is negative if the well costs can be covered by the sale of oil. Sales from the Permian and Eagle Ford basins have lower wellhead break-evens than the Marcellus Basin. However, with the recent decline in oil prices and the leverage that many of these firms incurred, oil and gas drilling rig count has declined 66% in the 2Q of 2020. The corresponding decline in gas production was 25% and 66% in NGLs.

An interesting fact associated with pipelines is that there is traded debt associated with the pipeline and the pipeline’s customer(s). Therefore, there are valuation benchmarks from both the pipeline’s debt and equity holders and the customers’ debtholders. If we can find a situation where the debt market values a firm with a considerably higher value (lower yield) than the equity, then there may be an interesting situation. In the case of Antero Midstream, which has one customer (AR), three benchmarks are available. AM’s dividend yield is 22.4%, while AM’s debt yield is 9.6% and rated BB. Given a BB rating, AM probability of default adjusted dividend yield3 is 19.7% (22.4% * (1-12%)). The debt/equity spread was 10.1%, a steep equity risk premium compared to the market level of 5%. AR’s debt has a yield of 18.4%, implying an equivalent customer yield premium of 4.0%.

Antero Resources' Fulcrum Security

Antero Midstream can also be viewed as a fulcrum security in the capital structure of AR. AR is an Appalachian gas and NGL firm with properties in West Virginia, Ohio, and Pennsylvania. AR is expected to be cash flow positive by $190 million by year-end 2020.

In 2019, AR had 3.4bcfe/d of production. One issue with AR is debt coming due over the next few years. AR has $1.4 billion face value ($1.0 billion market value) debt coming due in the remainder of 2020 and 2021, with $1.4 billion in liquidity before $500 million of additional asset sales over the next 18 months.

AR’s half-cycle pre-tax rate of return (using current STRIP prices) is 41% for AR wells with the existing hedge book in place. AR’s current operating cost of natural gas production is $2.14/mcfe, and total cost of production is $2.48/mcfe. Currently, these costs are declining 5% annually.

Antero Midstream receives a recurring set of cash flows similar to AR unsecured bonds or the recent OTTI deal done with TPG Capital. The current yield of AR bonds of 18% and the IRR for the OTTI deal of 13% are significantly below the current DCF and dividend yield of AM of 22%.

US Natural Gas Pipeline Business

The US pipeline business can be divided into gathering and processing, transportation, long-haul pipelines, and refining and logistics. Gathering and processing pipelines gather gas from the fields and process the gas before it is injected into long-haul pipelines which transport the gas to refineries or its end users. G&P pipeline revenues are dependent upon gas flowing in them. If the wells in the fields that they are providing transport for are closed in, then they will lose revenue. The spacing of the wells can also create economies of scale. Since the capital investment has to be made before gas starts to flow, many pipeline projects have minimum volume requirements (MVRs). Antero Midstream has MVRs of 70 to 75% of capacity.

One of the key drivers for pipeline capacity is increased natural gas and NGL demand for baseline power production and export to other countries via LNG transportation (pipelines and tankers). Over the next four years, US natural gas and LNG demand is expected to grow by 3% and 4% per year, respectively. International demand is also expected to grow and will increase LNG demand above the US demand numbers. Longer-term demand will be driven by the increased electricity demand for electric transportation. Although solar and wind power can provide electricity, intermittency and storage will leave us dependent upon gas to provide baseline and “peak” power for some time.

A big question is the timing and how much natural gas demand will be disrupted by renewables for electricity production and COVID-19. This disruption will reduce the demand for gas as an energy source. The expectation is that the US base power demand currently provided by coal will be phased out and replaced by natural gas. The other potential source of baseline power is nuclear; however, there are political and safety consideration issues in the US in regard to nuclear power.

Downside Protection

US gas pipeline risks include both operational leverage and financial leverage. One way to measure operational risk and reward is the utilization of the pipeline, given the variable nature, by utilization of the capacity payments and the fixed nature of the initial investment. Antero Midstream has had stable and growing utilization since its IPO, so operational risk has declined over time.

The other risk with low natural gas prices is contract renegotiation with its sole customer, AR. This is partially offset by AR’s large hedge book for gas of 96% in 2020 and 100% in 2021, and 100% for NGL in 2020. In addition, AR is expected to be cash flow break even, in part due to Antero Midstream providing AR fee reductions based upon volume growth from 2020 to 2023 over the past 12 months. These effects can be seen in the decline in 2020 revenue versus 2019.

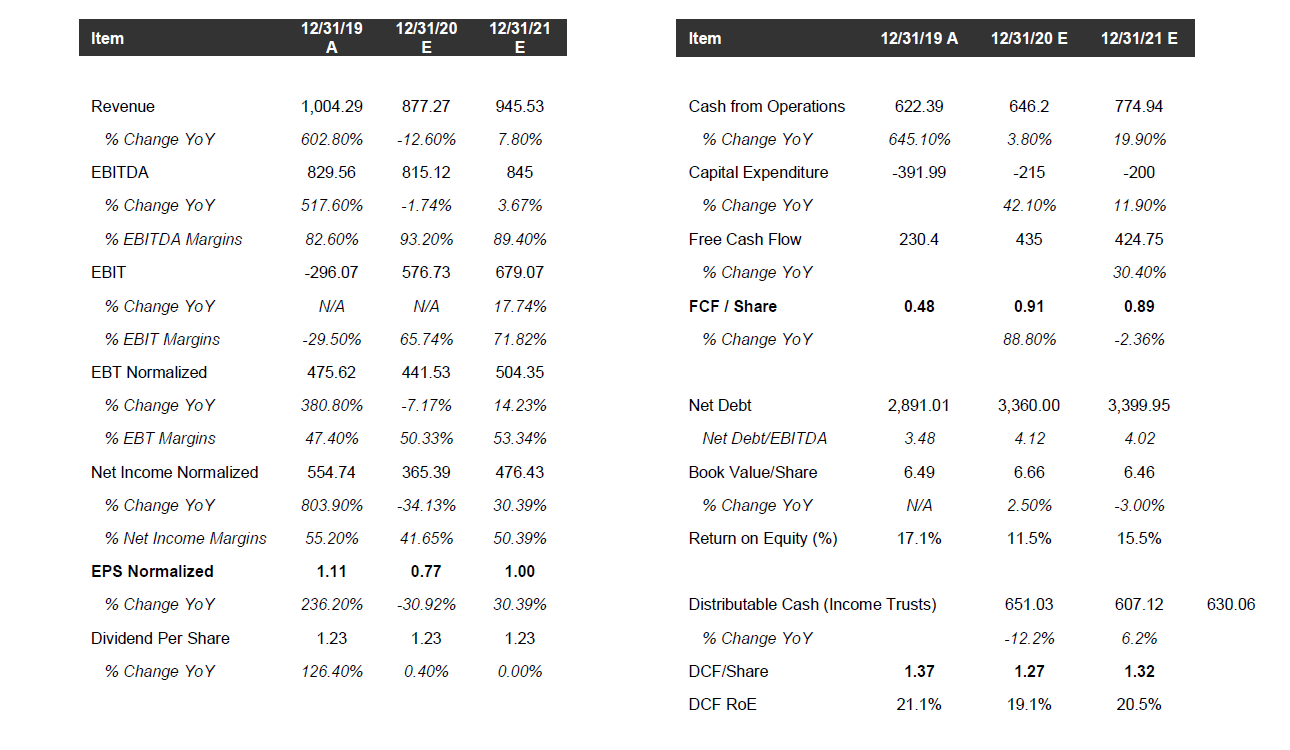

Financial leverage can be measured by the Debt/EBITDA ratio. Antero Midstream has a lower Debt/EBITDA than other G&P pipelines (3.7x EBITDA versus 4.4x for the other G&P pipelines). AM has done well in the current oil and gas recession/decline, with a revenue decline of only 7% in 2020. The historical/projected financial performance for AM is illustrated in Addendum A.

One driver in the valuation of Antero Midstream is the expected growth rate. The current valuation implies an earnings/DCF decline of 2.8% into perpetuity using the Graham formula ((8.5 + 2g)*(4.4/AAA bond rate)). The expected increase in production is expected to be 7% next year and trail off to 3% over the next five years. Longer-term natural gas demand in the US is expected to increase by 3% per year, and LNG exports will grow by 4% per year. Analysts that have a price target close to the current price assume an average 10% decline in DCF over the next ten years.

Our bet here is that Antero Midstream’s DCF and dividends will increase rather than decline due to increased demand, increased drilling by AR, and the large number of AR sites that can be drilled from the same areas that AR is now drilling. If AR can achieve revenue growth, then AM has some of the best economics in the G&P space and should be able to generate high free cash flow growth.

Comparables/Benchmarking

Addendum A includes firms engaged in the G&P gas pipeline market that have high margins and returns on equity (comparables) due to their density economics. Compared to the comparables, Antero Midstream has one of the highest returns on equity. AM has a lower payout coverage ratio than the comparables, but it is also further along in the completion of its pipeline projects. AM also has the lowest DCF multiple, and its credit rating is in-line with the comparables.

Management and Incentives

Antero Midstream’s management has been focused on creating value by building value accreting extensions of its pipeline. The CEO currently holds 14.9 million shares ($82 million) which is more than six times his average 2017-2019 salary and bonus. His salary and bonus are about 2% of DCF. The CEO’s total compensation is about 10% salary and 90% bonus. The bonus is based upon financial KPIs (return on invested capital, leverage, DCF/share growth, and safety metrics). The CEO of AR is the CEO of AM, as well. Currently, the stake the CEO has in AM has a larger value that the stake he has in AR ($45 million). Given the higher valuation multiple attributed to AM versus AR, management has an economic incentive to maximize Antero Midstream’s cash flows versus AR. Management has been opportunistically purchasing common stock from AR and in the open market ($142 million at an average price of $5.12 per share over the past 15 months). AR’s management has also been buying back debt at a discount ($163 million for $196 million face value).

Risks

The primary risks are:

- lower than expected growth in sales/cash flows (demand due to COVID);

- replacement of future gas demand from more nuclear power plants; and

- AR not reaching profitability or going bankrupt (12% based upon AR current credit ratings).

Potential Upside/Catalyst

The primary catalysts are:

- an increase in natural gas prices due to the decline in supply from associated gas;

- the continued cost of production declines; and

- more share repurchases.

Timeline/Investment Horizon

If we look at a growth rate close to the natural gas growth rate of 3%, then it implies almost 4x the current price. The first step is if the market no longer thinks DCF will go down, then over time this results in a 3x increase in the current price to $16.83. A longer-term target is the 3% US natural gas demand growth assumption or 4x the current price or $27.