Alluvial Fund commentary for the second quarter ended June 2020, discussing the virtures of a negative working capital cycle.

Q2 2020 hedge fund letters, conferences and more

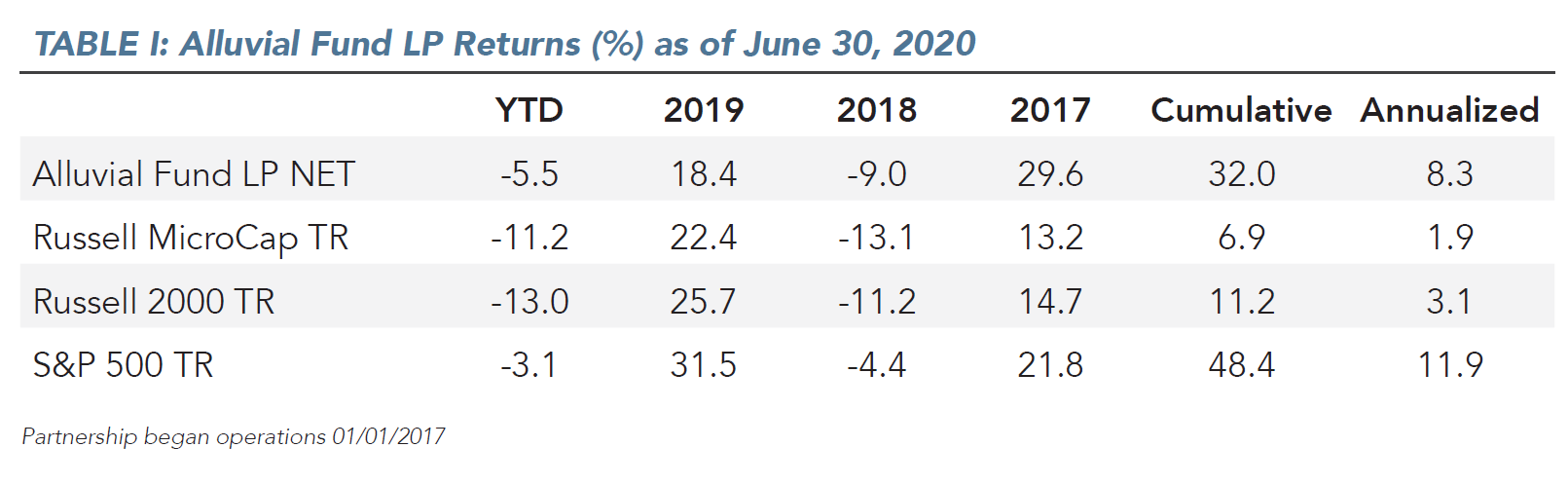

Alluvial Fund rose 14.8% in the second quarter, recouping most of the first quarter’s losses. As I write in late July, the fund has reached approximately break-even for the year while small-cap and micro-cap indexes remain down by double digit percentages, with “value” indexes faring significantly worse. While break-even is certainly not an exciting result, I am happy to have succeeded in preserving our capital amidst a thoroughly dispiriting environment for investors in small companies and less liquid securities..

Most of our portfolio holdings are showing strong resilience in the face of the economic slowdown. Those that have been stung by the pandemic have the operational flexibility and balance sheet strength to manage through the downturn. Just as our often unlisted, often thinly-traded holdings tend to outperform when fear and panic rule the day, they tend to lag when euphoria reigns. As market indexes roared from March’s lows, many of the companies in our universe experienced only a modest bounce, or none at all. I am reminded of the months and years following the financial crisis of 2008, where investors only slowly regained the confidence needed to purchase lesserknown securities despite the economic and market recovery taking place. Of course, brave souls who were willing to buy these shares were amply rewarded in due time. I continue to seek out the best of these opportunities for Alluvial Fund.

In most of these letters, I highlight a few holdings that are new, or have reported substantial business developments since my last communication. I thought partners would appreciate me taking a more comprehensive approach in this letter and providing a run-down of all the fund’s materially-sized positions. I believe each of these companies is dramatically under-valued either on its present-day assets and cash flows, or on a conservative estimate of the present value of all growth and reinvestment opportunities.

Portfolio Review

P10 Holdings continues to be the fund’s largest position. I added to our position when shares fell to $1.50 during March’s panic. With fears of economic catastrophe fading, P10 shares have since soared to new highs. I believe P10 shares are currently worth between $3.50 and $4.00, and potentially far more in future years depending on the company’s ability to acquire additional highmargin, predictable fee streams from alternative investments managers. COVID-19 has not slowed down P10’s ability to form relationships with new clients. In May, P10 subsidiary RCP Advisors won a mandate from a Dutch pension group to invest $500 million over five years.

Intred SpA is (thus far) our most successful discovery from the Borsa Italiana’s AIM segment. Shares have more than tripled since our initial purchases. This fiber-optic network operator continues to sign up new clients for its ultra-high-speed network, and recently acquired a competitor. The company is no longer an obvious value based on free cash flow yield, but Intred continues to enjoy a strong set of investment opportunities, both internal and external. What’s more, Intred has created a negative working capital cycle where it gets paid in advance for its services, effectively creating investment “float” and subsidizing its investment needs. I have become increasingly interested in firms with sustainably negative working capital positions. More on the topic later in this letter. Intred Shares remain attractive under €10.

Bredband2 i Skandinavien continues to thrive as a low-cost provider of high-speed internet in Sweden. Unlike Intred, Bredband2 is largely non-asset-based, providing its services on networks owned by other parties. Like Intred, Bredband2 generates substantial cash from advance payments by customers. The magnitude of these payments allows Bredband2 to operate with negative invested capital and fund all its capex needs from customer pre-payments. Astonishing. Bredband2 is a bargain below SEK 2.00 per share, though I would be hesitant to sell our shares even at that level based on the company’s long runway for growth and rare cash flow characteristics.

Following Bredband2 is LICT Corporation. LICT is in prime position in the telecom industry. LICT has invested heavily over the years and now boasts a fiber-heavy, state-of-the-art network that is well-positioned to deliver broadband to rural Americans for decades to come. The company enjoys a substantial net cash position, enabling it to return virtually all its earnings to shareholders via share repurchases. I wrote about LICT in a little more detail on OTC Adventures recently. Shares are conservatively worth $25,000, a figure that will only grow as the company companies to shrink its share count.

Nuvera Communications has been a long-time stalwart for Alluvial Fund. The company will benefit from increased need for quality consumer and business broadband connections in its Minnesota and Iowa service territories. I am hard-pressed to find a better combination of robust free cash flow generation, low risk operations and a healthy balance sheet. The company is not exactly exciting or communicative (despite the name) and perhaps that is why Nuvera shares languish at 8.3x free cash flow and 7.4x cash earnings (net income plus intangibles amortization). Nuvera has a history of acquiring small Minnesota telecoms, and I expect the company to go on the hunt once again as it pays down the low-cost debt it took on to purchase Scott-Rice Telephone in 2018. I believe Nuvera should trade at a free cash flow yield of ~7-8%, which would value shares at $25-29. While Nuvera does not have the highest long-term return potential in the Alluvial Fund portfolio, it offers attractive upside potential with minimal risk.

Rand Worldwide has been a wonderful holding for Alluvial Fund, and I expect the best is yet to come. Rand is a value-added software reseller of Autodesk products. Customers come to Rand because they need assistance with training, software integration, and support. Autodesk software is the gold standard in the engineering and design fields, and Autodesk is making every effort to increase its sales by transitioning to a software-as-a-service model and beginning to crack down on unauthorized users. Rand Worldwide is the beneficiary of these trends, and its revenues have soared. Rand requires little investment and produces copious free cash flow, allowing the firm to buy competitors and return capital. I would not sell Rand for less than $16 today, and I expect the company’s value to grow quickly under the leadership of majority owner Peter Kamin.

Crawford United is one of our “stung” holdings. The company’s industrial subsidiaries were set to have a record year until the pandemic came along and walloped the aerospace and construction industries. This year’s results will not be impressive, but I continue to like the company’s longterm strategy of acquiring small, good quality industrial firms in the Midwest. There are thousands of potential acquisition targets. Acquiring these niche companies at low multiples of operating income using responsible amounts of debt financing is a winning strategy that is both repeatable and scalable. I continue to believe shares of Crawford are worth at least $25 today and potentially far more in years to come.

Polaris Infrastructure has been a wild ride for shareholders, but the company’s core business has never been stronger. The next 12 months will be an extraordinary time for Polaris. All of the company’s Peruvian assets will come online, the company will very likely complete a hydro power acquisition in Panama, and there is a strong chance the company will complete a refinancing of its Nicaragua debt, lowering its cost and freeing up current cash flow. I expect the company to continue making attractive purchases of renewable power resources in Latin America and South America and sharing the resulting cash flow with shareholders. A 10% free cash flow yield would be a fair price for Polaris, which would value shares well over $20 Canadian. Once the company’s Nicaragua assets no longer account for the majority of the company’s value, I expect the free cash flow yield to compress and for fair value to rise into the $30s.

Next is MMA Capital Holdings, another long-time Alluvial holding. MMAC has been among Alluvial’s most successful investments to date, though shareholders have little to show for the last three years. Despite the market’s disinterest, the firm’s book value continues to grow at a healthy pace. Earnings are growing proportionally as the solar construction lending business scales. MMA was formerly a voracious repurchaser of its own shares but reduced its activity in favor of building out its core business and preserving liquidity as credit markets came under stress earlier this year. I am hopeful that with the worst of COVID-related fears behind us and shares still trading at a 25% discount to book value (excluding tax assets) the company will resume buying back shares. I believe MMA should trade somewhere in the upper $30s, much closer to book value.

Butler National Corporation rounds out our meaningful holdings. Butler, an aerospace provider with a casino company attached, would seem to be at the epicenter of industries most affected by COVID-19. Indeed, Butler’s Kansas casino was closed for 66 days. However, the casino has experienced good levels of traffic since reopening and is actually on track for a record July. The much more important aerospace segment saw its profit slip to just under breakeven for the quarter ended April 30, but backlog remains strong and the company is confident it will continue experiencing healthy demand for its aircraft upgrades, modifications, and systems. Butler’s balance sheet is as strong as ever with 15 cents in net cash per share, casino lease excluded. I struggle to see how Butler shares could be worth less than $1.00, though it may take time for investors to regain their confidence in Butler’s continued profitability.

Missing is Meritage Hospitality Group, which I sold in the second quarter after holding shares for years. Ultimately, I decided I was no longer comfortable with the firm’s aggressive use of debt and its high operating leverage given the extreme economic uncertainty that prevailed. The risk that a long period of depressed revenue would force Meritage to raise equity capital on deeply disadvantageous terms, or even force the firm into bankruptcy, was unacceptably high. Additionally, other opportunities promised better upside with substantially less risk. Fortunately for Meritage, a worst-case scenario has not come to pass, and the company has dealt with its challenges effectively. Fortunately for us, the securities I purchased with the proceeds from our Meritage shares (mainly P10 and Polaris) have performed very well.

On Negative Working Capital Cycles

As I mentioned when discussing Intred and Bredband2, I have become fascinated by business models that feature a negative working capital cycle. Working capital may not be the flashiest subject, but a company’s working capital characteristics will have a significant effect on its ability to grow profitably and how it will manage the ups and downs of the business cycle. Nearly all firms operate with positive working capital. Simply put, they receive cash some length of time after they record revenue. Their operating cash, inventory, and receivables, less payables, is a positive figure. A positive working capital balance represents invested capital that must be funded with debt or equity. As the company’s revenue grows, so do its working capital requirements and the amount of capital required. Working capital needs act as a drag on returns on capital and on the firm’s ability to produce profitable growth.

Rarely, a firm figures out how to reverse the normal pattern and collect significant cash before it delivers its good or services. Most often, these are companies offering some kind of high-margin intangible service that requires minimal physical inventory. For a firm that operates with negative working capital, growth actually provides a capital subsidy as additional cash rolls in. Instead of requiring incremental capital to support its working capital needs, the firm is free to use excess cash to subsidize investment in fixed assets, perform acquisitions, or return capital to shareholders without sacrificing growth opportunities.

Bredband2 i Skandinavien is a shining example. From 2015 to 2019, Bredband2 grew its revenues from SEK 364 million to SEK 671 million, an increase of 84%. Over the same period, the company’s non-cash net working capital went from negative SEK 65 million to negative SEK 119 million. That’s a stunning figure. One would think an increase of 307 million in annual revenue would require some increase in working capital, but not for Bredband2. Instead, the firm’s growth has freed up over SEK 50 million in cash. The firm’s incredible cash generation is one reason Bredband2 has been able to grow at a high-teens rate while distributing virtually all its earnings to shareholders. Now, it must be said that the virtues of a negative working capital cycle only continue for as long as a firm grows its revenue. If revenues fall, working capital consumes cash rather than providing it. The long-term benefits of a negative working capital model only accrue to companies offering products and services that will experience long-term growth in demand with minimal cyclicality. Hmm, sounds a lot like broadband internet…

I am working to identify other small, little-known businesses that generate float through a negative working capital cycle. One company I have found is a provider of custom, high-end travel packages that gets paid by clients months in advance of their actual vacations. (Obviously, this business faces short-term challenges from the pandemic.) If this company ends up in the Alluvial Fund portfolio, I will be sure to provide a more complete description in my next letter.

Concluding Thoughts

Thank you for your confidence in Alluvial. I remain available any time for questions regarding our strategy and portfolio, so please do not hesitate to contact me. As always, my entire investable capital is committed to Alluvial Fund, and I spend each day looking for ways to make our collective investment grow! I hope you and your families are happy and healthy despite the disruption we are all experiencing. I look forward to writing to you again in October.

Regards,

Dave Waters, CFA

Alluvial Capital Management, LLC

This article firs appeared on ValueWalk Premium.